Could a routine digital notification from your bank soon become a formal inquiry into your eligibility for state support? While headlines often lean toward sensationalism, the reality of the upcoming 2026 legislative shifts requires a more measured perspective. We understand that many individuals feel a genuine sense of unease regarding the proposed Data Protection and Digital Information Bill. It’s natural to feel concerned about privacy when the distinction between HMRC’s long-standing powers and the new dwp bank account checks remains unclear to the public.

Our objective is to replace that uncertainty with professional clarity. We’ll provide a bespoke analysis of these updated financial surveillance powers, ensuring you have the necessary information to remain fully compliant with statutory requirements. By examining the specific data sharing protocols and the 2026 timeline, we’ll outline the pragmatic steps you can take to keep your financial records in order. This guide ensures you’re well-advised and prepared for a changing regulatory environment through a lens of quiet excellence.

Key Takeaways

- Distinguish between the statutory reality of the 2026 data-gathering powers and the common misconceptions regarding real-time transaction monitoring.

- Learn how to navigate the upcoming dwp bank account checks by maintaining precise records of capital limits and the applicable taper rates for savings.

- Implement a proactive strategy for financial compliance by conducting a thorough audit of all personal and joint holdings to ensure accurate reporting to HMRC.

- Discover how bespoke professional advice can provide clarity and security for individuals managing complex or international financial interests under increased scrutiny.

- Gain the necessary insights to protect your financial reputation through a measured, well-constructed approach to capital management and benefit eligibility.

Understanding the 2026 DWP Bank Account Check Powers

The legislative landscape governing welfare administration undergoes a significant transition in 2026. Central to this change is the introduction of Third-Party Data Gathering powers, a mechanism designed to modernise how the Department for Work and Pensions (DWP) identifies financial discrepancies. These dwp bank account checks aren’t merely administrative updates; they represent a move towards automated, systemic oversight of claimant capital and residency. By targeting the UK’s 15 largest financial institutions first, the government aims to monitor the vast majority of claimant accounts, ensuring a broad reach to address the billions lost annually to fraud and error in the welfare system.

The primary purpose of these powers is to identify instances where claimants’ financial circumstances don’t align with their benefit applications. This typically involves capital exceeding the £16,000 threshold for means-tested support or evidence of extended periods spent abroad. It’s a proactive approach, moving away from reactive investigations and towards a model of continuous verification that protects the integrity of public funds.

The Legal Framework for Financial Surveillance

The Data Protection and Digital Information (DPDI) framework provides the statutory basis for these expanded powers. Under this 2026 mandate, the DWP compels banks to provide automated data feeds rather than responding to individual, manual requests. This shift is legally significant. It moves the threshold for intervention from “reasonable suspicion” of a specific individual to a model of continuous, systemic oversight. Banks don’t share every transaction detail; instead, they flag accounts that breach specific criteria. This allows the department to maintain a high level of scrutiny without the need for prior evidence of wrongdoing, representing a fundamental change in the relationship between the state and private financial records.

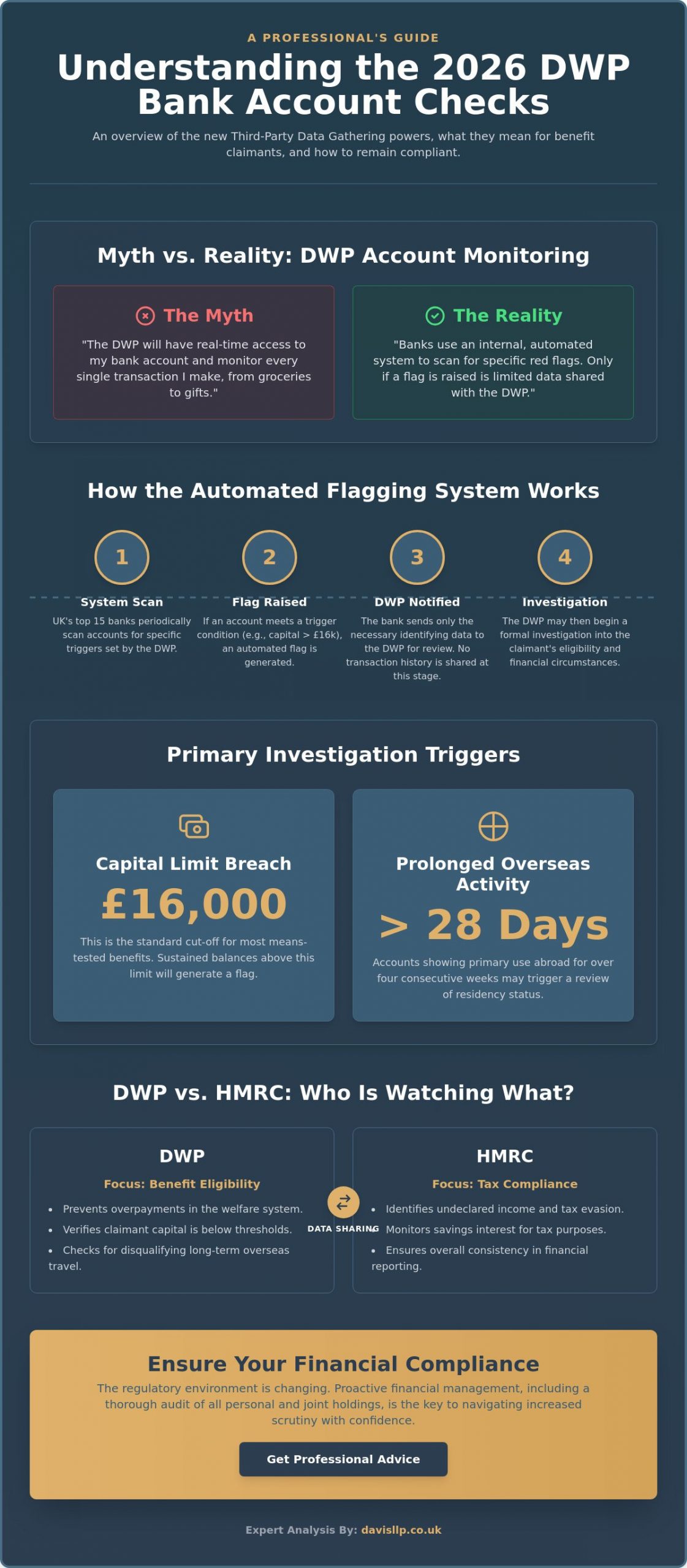

HMRC vs. DWP: Who is Watching Your Finances?

Distinguishing between the mandates of different government bodies is essential for maintaining financial clarity. While the DWP focuses on benefit eligibility and capital thresholds, HMRC maintains its focus on tax compliance and undeclared income. The 2026 environment has seen an evolution in data sharing, where information regarding savings interest flows more freely between departments to ensure consistency. However, the DWP’s primary concern remains the prevention of overpayments within the welfare system. For those concerned about how these broader surveillance trends affect their personal tax position, we recommend reviewing our analysis of the HMRC Tax Warning 2026. Understanding these distinct mandates helps in navigating the complexities of modern financial compliance and ensures you remain well-advised in an era of increased transparency.

Myth vs. Reality: What the DWP Can and Cannot See

Public discourse regarding the 2026 legislative shifts often suggests a level of surveillance that exceeds the actual statutory framework. A common misconception is that the Department for Work and Pensions (DWP) will monitor every individual transaction in real-time. In reality, the dwp bank account checks rely on an automated third-party data gathering model. Banks won’t provide a live feed of your daily spending; instead, they’re required to scan their own systems for specific data points that suggest a breach of benefit eligibility criteria.

The UK Parliament’s Public Accounts Committee has expressed concerns about the scale of these powers, yet the technical application remains targeted. You won’t find a government official scrutinising your supermarket receipts or leisure spending. The data transferred is restricted to account balances and indicators of prolonged overseas residency. This focus ensures the department identifies capital surpluses or potential fraud without accessing the granular details of your lifestyle choices.

The Automated Flagging System Explained

Financial institutions use algorithms to identify accounts that exceed the £16,000 capital threshold, which is the standard cut-off for most means-tested benefits. When a balance remains above this limit for a sustained period, the system generates a flag. These triggers also apply to residency, identifying accounts used primarily abroad for more than 28 consecutive days. Once a flag is raised, the bank notifies the DWP, providing only the necessary identifying information to justify a formal investigation. It’s a binary system of compliance rather than a narrative of your personal life.

Joint Accounts and Shared Financial Responsibility

Joint accounts present a complex layer of risk. The DWP typically views the full balance of a shared account as being available to the claimant, regardless of who deposited the funds. This can lead to a scenario where a partner’s or relative’s savings inadvertently jeopardise your benefit status. Understanding the tax and legal implications of these arrangements is essential for protecting your financial standing. You can find more detail on this in our guide to HMRC Joint Bank Accounts and Savings Tax.

If you’re concerned about how your specific banking arrangements might be interpreted under the 2026 rules, our private client team can provide a bespoke review of your financial structure to ensure full statutory compliance.

The £16,000 Threshold: Managing Capital and Savings

For individuals claiming Universal Credit, the £16,000 capital limit represents a definitive statutory ceiling. If your total capital exceeds this figure, eligibility for the benefit ceases immediately. For savings held between £6,000 and £16,000, the DWP applies a “taper rate” or tariff income. This calculation assumes a monthly income of £4.35 for every £250 of capital held above the £6,000 floor. Pension Credit operates under different parameters, where the first £10,000 is typically ignored, but every £500 over that amount is treated as £1 of weekly income.

Accuracy in reporting is paramount. Claimants frequently overlook assets that the DWP considers part of their total capital. These include Individual Savings Accounts (ISAs), Premium Bonds, and funds held in offshore accounts. The introduction of enhanced dwp bank account checks means that discrepancies between declared savings and actual bank balances are likely to be identified with greater speed. We advise clients that any change in financial circumstances, such as receiving a small inheritance or a redundancy payout, must be communicated to the DWP to prevent overpayments and potential civil penalties.

What Counts as Capital in 2026?

Capital is generally defined as “liquid assets,” which encompasses cash, stocks, and shares. However, certain items remain “disregarded capital,” such as the home you live in and personal possessions like furniture or vehicles. For self-employed claimants, assets used specifically for their business are usually excluded from the personal capital assessment. It’s a pragmatic distinction that allows businesses to remain viable. Nevertheless, one-off payments like a redundancy settlement or a divorce payout are treated as capital. As noted by The Independent on the new DWP powers, the legislative shift aims to ensure that state support is targeted precisely at those who meet the strict financial criteria.

Deprivation of Capital: The Risks of Giving Money Away

The DWP maintains a rigorous stance on the “deprivation of capital.” This occurs when a claimant intentionally reduces their assets to remain below the £16,000 threshold or to increase their benefit entitlement. Common examples include gifting large sums to family members or paying off debts that aren’t yet due. If the DWP determines that the primary motive for a transfer was to secure benefits, they may treat the claimant as still possessing that “notional capital.” There’s no fixed look-back period for these dwp bank account checks; instead, the department examines the timing and the intent behind significant financial shifts. Our experience suggests that transparency is the most effective safeguard against allegations of benefit fraud.

Proactive Financial Management: Safeguarding Your Compliance

Preparing for the implementation of the 2026 data-sharing powers requires a methodical approach to one’s personal and commercial finances. The introduction of automated dwp bank account checks means that inconsistencies between reported capital and actual bank balances will be flagged with greater frequency. To maintain compliance and ensure peace of mind, we recommend a structured four-step review of your financial position.

- Step 1: Conduct a comprehensive audit of all personal and joint financial holdings. This includes ISAs, premium bonds, and secondary current accounts that may have remained dormant but still contribute to your total capital limit.

- Step 2: Verify that all income and accrued savings interest are correctly reported to HMRC. Under the 2024/25 tax year rules, interest exceeding your Personal Savings Allowance must be declared to avoid discrepancies during cross-departmental data matching.

- Step 3: Establish a robust audit trail for significant transactions. Whether you’ve received a family gift of £5,000 or sold a vehicle, having a clear record of the source and intent of these funds prevents them from being mischaracterised as undisclosed income.

- Step 4: Consult a professional accountant for complex international interests. Assets held overseas are subject to the Common Reporting Standard, and the DWP’s new powers will likely leverage these existing international transparency frameworks.

The Importance of Accurate Record Keeping

Standard bank statements often lack the context required to explain specific capital fluctuations during a formal enquiry. If the dwp bank account checks trigger an automated alert, the burden of proof frequently rests with the individual to demonstrate that they haven’t exceeded the £6,000 or £16,000 capital thresholds. We advise using digital accounting tools to track capital growth in real time. It’s essential that your UTR number and associated tax filings mirror the information provided in benefit declarations. Misalignment between these records is a primary catalyst for fraud investigations.

Managing Scrutiny with Professional Gravitas

Should the DWP request further information or an interview, your response should be measured and evidence-led. A calm, transparent partnership with regulatory bodies often resolves queries before they escalate into protracted disputes. We’ve seen that involving a professional accountant early in the process provides the necessary validation of your financial history. This professional oversight ensures that your disclosures are accurate and that your rights are protected throughout the investigation. Our role is to provide the strategic clarity needed to resolve these matters with minimal disruption to your private or professional life.

If you require assistance in reviewing your financial structures to ensure full compliance with evolving UK regulations, contact our private client team today for a confidential consultation.

Navigating Regulatory Scrutiny with Davis & Co LLP

The landscape of financial privacy in the United Kingdom is undergoing a fundamental shift. As the 2026 implementation of the Data Protection and Digital Information Bill draws closer, the prospect of dwp bank account checks represents a new level of state oversight. We provide the clarity and peace of mind necessary to navigate this transition with composure. Our bespoke personal tax services aren’t merely about filing returns; they’re about building a robust framework for your financial life. For individuals with international interests or multi-layered asset structures, we offer strategic advice that anticipates regulatory shifts before they impact your daily affairs.

Davis LLP operates with a philosophy of quiet excellence. We understand that sensitive financial disclosures require a delicate touch and a deep understanding of the law. We position ourselves as your trusted partner for long-term compliance, ensuring that your financial history is a testament to integrity rather than a source of anxiety. Our role is to provide a calm, authoritative voice in an increasingly complex regulatory environment.

Bespoke Solutions for Private Clients

We help our clients audit their assets to ensure every account and investment aligns with current regulatory requirements. This process is essential for those balancing inheritance tax planning with strict capital limits. For example, the £16,000 capital threshold for many state-supported benefits can create complex challenges for families managing intergenerational wealth transfers. We apply intellectual rigour to these intersections, ensuring your estate planning doesn’t trigger unnecessary dwp bank account checks or investigations. Our commitment to discretion means your private matters remain exactly that, even as we ensure they meet the highest standards of statutory transparency.

Contacting Your Strategic Advisor

Initiating a personal tax or compliance review is the first step toward securing your financial future. You can begin a consultation by contacting our private client team to discuss your specific circumstances. In an era of increased surveillance, where the government aims to monitor millions of accounts to recover an estimated £600 million in annual overpayments by 2028, a professional partnership is a vital safeguard.

We believe that proactive transparency is your best defence. By maintaining impeccable records and clear lines of communication, we ensure you remain beyond reproach. Our advisors are ready to help you maintain your financial standing with the precision and reliability that Davis LLP is known for. A professional review today prevents the uncertainty of an investigation tomorrow. We invite you to reach out to our team to ensure your financial interests are managed with the care and expertise they deserve.

Securing Your Financial Future in a Transparent Era

The implementation of the 2026 Data Protection and Digital Information Bill represents a significant evolution in statutory oversight. These new dwp bank account checks are specifically designed to verify that capital remains within the £16,000 limit required for means-tested benefits, rather than providing a window into your private lifestyle. By distinguishing between legislative reality and common misconceptions, you can manage your assets with greater clarity. Davis & Co LLP has operated with professional gravitas since 1901, helping clients navigate the complexities of HMRC and statutory compliance. As Chartered Certified Accountants, we provide bespoke tax solutions that reflect your unique circumstances. It’s vital to address these changes early to maintain your peace of mind. Our firm acts as a strategic partner, ensuring your financial records are accurate and fully compliant with the latest UK regulations. We invite you to ensure your financial compliance with expert tax advice from Davis & Co LLP. With the right professional partnership, you’ll meet these new standards with total confidence and a clear path forward.

Frequently Asked Questions

Can the DWP see my bank account without me knowing?

Under the proposed 2026 legislative framework, the DWP won’t need to notify you before receiving data from your financial institution. Banks will be required to scan their systems for specific flags, such as capital limit breaches, and report these directly to the department. This shift represents a move from individual suspicion to automated monitoring. We understand this change causes concern for those seeking to maintain their privacy while remaining compliant with statutory obligations.

Does the DWP check everyone’s bank account every month?

The DWP won’t monitor every individual transaction manually every month. Instead, the 15 largest UK banks will use automated systems to flag accounts that exceed capital thresholds or show signs of overseas residency. These 15 institutions account for roughly 80% of all benefit claimants’ accounts. It’s a targeted process designed to identify approximately 3% of cases where fraud or error is most likely to occur.

What happens if I have more than £16,000 in my savings account?

If your savings exceed the £16,000 threshold, your eligibility for means-tested benefits like Universal Credit or Housing Benefit ends immediately. For balances between £6,000 and £16,000, the DWP applies a tariff income deduction. They calculate this as £4.35 per month for every £250 you hold over the £6,000 lower limit. We provide bespoke advice to help clients navigate these complex capital rules and protect their financial interests.

Will the DWP check my accounts if I am on the State Pension?

DWP bank account checks won’t apply to you if you only receive the State Pension. The government confirmed in the 2023 Autumn Statement that these new powers focus on means-tested benefits where capital limits apply. Since the State Pension isn’t based on your savings, your private bank data remains outside the scope of these automated checks. This protection also extends to other non-means-tested payments like Personal Independence Payment (PIP).

Can the DWP see my PayPal or Monzo transactions?

The DWP has the legal authority to request data from any financial institution, including digital-only banks like Monzo and payment platforms like PayPal. These entities must comply with the same statutory requirements as traditional high-street banks. If you use these platforms to manage your finances, ensure your records are accurate. We’ve seen an increase in queries regarding digital assets as the 2026 rollout approaches for dwp bank account checks.

How far back can the DWP go when checking bank statements?

The DWP can typically request bank statements covering the last 12 months for routine eligibility reviews. However, if they suspect fraud, the Limitation Act 1980 allows them to investigate records dating back 12 years. This is why maintaining clear financial records is vital for your long-term security. Our team provides strategic guidance to ensure you’re prepared for any historical data requests the department might initiate during an investigation.

Do DWP bank checks apply to joint accounts with someone not on benefits?

The DWP can check joint accounts even if the other account holder doesn’t receive benefits. They generally assume the claimant owns 50% of the funds in a joint account. If the total balance exceeds the £6,000 or £16,000 limits, it may affect your payments. You’ll need to provide evidence if you believe the funds belong entirely to the other person to avoid unfair deductions from your monthly entitlement.

What should I do if the DWP contacts me about my bank account?

You must respond to any formal request for information within the timeframe specified in their letter, which is usually 1 month. Failing to provide statements can lead to an immediate suspension of your benefits. We recommend reviewing your accounts against the current dwp bank account checks criteria before submitting documents. Seeking professional legal advice early can help resolve disputes before they escalate into formal litigation or recovery action.