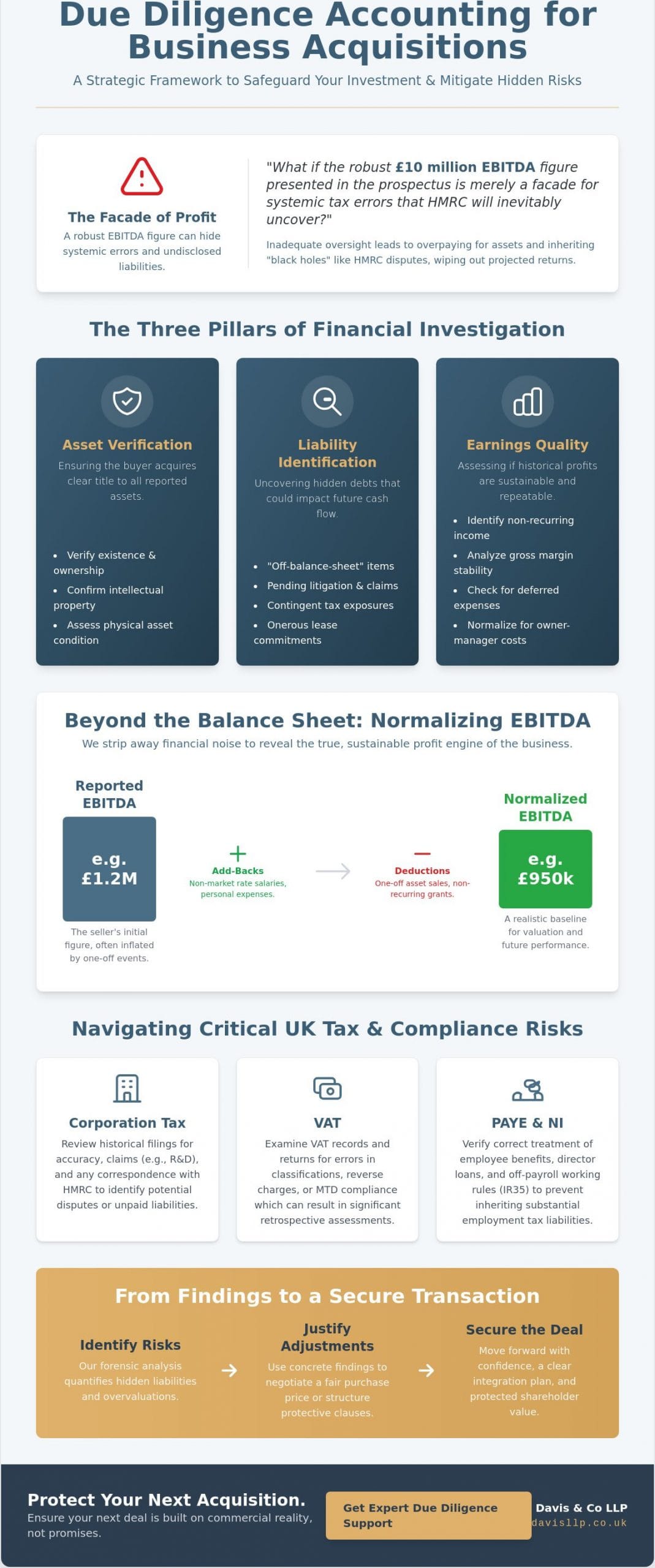

What if the robust £10 million EBITDA figure presented in the prospectus is merely a facade for systemic tax errors that HMRC will inevitably uncover? For many UK directors, the prospect of acquiring a competitor is often clouded by the fear of inheriting “black holes” or undisclosed liabilities that could compromise the firm’s future. Comprehensive due diligence accounting for business acquisition isn’t merely a box-ticking exercise; it’s the clinical process of verifying a seller’s claims to ensure the purchase price reflects the commercial reality. You likely recognise that a successful deal depends on total transparency, yet finding that clarity within complex sets of accounts remains a significant challenge.

This guide provides a clear, risk-mitigated path to your next acquisition by addressing these uncertainties directly. We’ll help you master the intricacies of financial scrutiny to verify valuations and identify historical tax risks before they become your burden. You’ll gain a strategic framework for the 2026 market that secures your investment and establishes a bespoke plan for post-deal growth. We’ll examine the critical steps required to move from the initial offer to a successful, stable transition.

Key Takeaways

- Safeguard shareholder value by employing forensic financial analysis to verify the Quality of Earnings and expose hidden anomalies that sit beyond the standard balance sheet.

- Execute a structured framework for due diligence accounting for business acquisition, ensuring every financial risk is identified and quantified before any formal commitment is made.

- Mitigate significant UK compliance risks and potential liabilities by rigorously reviewing historical tax records for Corporation Tax, VAT, and PAYE.

- Utilise professional findings to strategically justify price adjustments or earn-out structures, facilitating a more secure transition into the post-acquisition integration phase.

The Strategic Role of Due Diligence Accounting in Business Acquisitions

In the high-stakes environment of a UK corporate transaction, due diligence accounting for business acquisition serves as a forensic investigation into a target company’s financial health. It’s far more than a routine box-ticking exercise. It’s a strategic necessity that provides the independent verification required to protect shareholder value and ensure long-term stability. While a standard statutory audit focuses on whether historical accounts provide a “true and fair” view for compliance purposes, Understanding Due Diligence reveals its true purpose: assessing future commercial viability. This specialized financial review acts as a vital catalyst for final price negotiations, allowing buyers to structure deals that reflect the actual risks and opportunities discovered during the process.

The Objectives of a Financial Investigation

A thorough financial investigation aims to strip back the layers of reported figures to reveal the operational truth of the target. Our approach focuses on three critical pillars:

- Asset Verification: We verify the existence and legal ownership of all reported assets, including intellectual property registered with the UK Intellectual Property Office, to ensure the buyer acquires clear title.

- Liability Identification: We identify “off-balance-sheet” liabilities, such as pending litigation, onerous lease commitments, or contingent tax exposures, that could impact future cash flow.

- Earnings Quality: We assess the sustainability of historical earnings. This involves checking if profit margins are genuinely repeatable or if they’ve been bolstered by non-recurring contracts or deferred capital expenditure.

By conducting a bespoke investigation, we ensure that the due diligence accounting for business acquisition provides a clear-eyed view of the target’s financial trajectory under new ownership.

The Risks of Inadequate Financial Oversight

The consequences of superficial oversight are often expensive. Inheriting undisclosed HMRC disputes or tax arrears can lead to immediate liquidity crises post-completion. We’ve seen instances where “window-dressed” accounts, which manipulate timing differences to show peak performance, lead to significant overvaluation. If a buyer fails to identify these patterns, they risk overpaying by millions of pounds based on ephemeral data. In some cases, undisclosed liabilities related to the 2024/25 tax year can trigger penalties that wipe out the first year’s projected dividends. Due diligence is the bridge between a seller’s promise and a buyer’s reality.

Forensic Financial Analysis: Beyond the Balance Sheet

Numbers rarely tell the whole story. While a balance sheet provides a snapshot of a company’s position at a specific moment, it often fails to capture the underlying health of the operation. Effective due diligence accounting for business acquisition requires a forensic approach, stripping away the varnish of optimistic management reporting to reveal the true economic engine. We’ve seen cases where reported profits were inflated by 12% simply through aggressive revenue recognition policies that didn’t align with actual cash receipts.

A critical component involves reconciling management accounts against statutory filings held at Companies House. Discrepancies here often signal weaknesses in internal controls or, in more concerning cases, deliberate manipulation. We examine the 2025 financial records to ensure that the systems producing these reports are robust enough to support the business under new ownership. Identifying customer concentration risks is also paramount; if a single client accounts for more than 25% of total revenue, the acquisition’s risk profile changes significantly.

Quality of Earnings and EBITDA Adjustments

EBITDA is a common starting point for valuation, but it’s rarely the final word. We focus on “normalising” this figure by identifying one-off events that won’t recur. If a target business sold a delivery vehicle for a £5,000 profit or received a non-recurring government grant, these gains are stripped out. Conversely, we look for “owner-manager” expenses. It’s common for private directors to run personal car leases or non-market salaries through the business. Adjusting these to market rates provides a clearer picture of the sustainable profit margin.

- Gross Margin Analysis: We break down margins by product line. A 35% overall margin might hide a failing service department propped up by a legacy product.

- Non-recurring Income: Identifying anomalies like legal settlements or one-time insurance rebates.

- Cost Normalisation: Ensuring staff costs reflect current UK market rates for 2026.

Working Capital and Cash Flow Predictability

Acquiring a company only to find it lacks the liquidity to fund its own growth is a common pitfall. We calculate the “normalised” working capital by looking at the last 24 months of cycles. This prevents sellers from artificially boosting cash by delaying payments to suppliers or aggressively collecting debts just before completion. If the average debtor cycle has stretched from 30 to 48 days over the last year, it suggests potential credit risks or a softening market.

Future capital expenditure (CapEx) is equally vital. We assess whether the current equipment or IT infrastructure will require a significant £75,000 upgrade within the first 12 months. Understanding these requirements allows for a bespoke financial advisory approach that protects your investment from unforeseen cash drains. Our analysis ensures you aren’t just buying history, but a predictable future.

Navigating Tax Due Diligence and Compliance Risks

Tax liabilities often represent the most significant hidden costs in a transaction. When conducting due diligence accounting for business acquisition, we scrutinise the target’s historical tax advice UK to confirm that previous positions remain defensible under current HMRC scrutiny. It’s not enough to verify that returns were filed; we must assess the quality of the underlying logic used to justify specific deductions or tax structures.

We focus on identifying “tax traps” within Corporation Tax, VAT, and PAYE records. A common oversight involves the VAT Capital Goods Scheme, where a failure to adjust for changes in use can lead to unexpected repayments. In PAYE, the misclassification of benefits or errors in National Insurance contributions frequently trigger substantial penalties. We also evaluate the target’s status regarding IR35 and contractor compliance. Since the April 2021 off-payroll working reforms, the burden of determination has shifted to the engager. If a target has failed to issue accurate Status Determination Statements (SDS), the buyer could inherit a legacy of unpaid tax and interest.

Historical R&D tax credit claims require equal rigour. HMRC’s 2024 compliance reports indicated a 20% increase in enquiries into SME claims. If a target has been overly aggressive in its R&D filings, the risk of a clawback becomes a material concern for the new owner. We quantify these exposures to ensure they’re reflected in the final purchase price or protected via robust tax indemnities.

International Tax and Cross-Border Considerations

For targets with international subsidiaries, we evaluate transfer pricing arrangements to ensure they align with the arm’s length principle. Our review integrates international tax planning standards to mitigate the risk of double taxation or diverted profits. We also verify that withholding tax obligations on cross-border payments, such as dividends or royalties, have been correctly managed under the relevant bilateral treaties to avoid late payment surcharges.

Sector-Specific Tax Nuances

Specific industries carry bespoke risks. In the property sector, we assess the complexities of the Option to Tax and Stamp Duty Land Tax (SDLT) mitigation strategies. Healthcare and dental practice acquisitions require a precise analysis of VAT-exempt medical services versus taxable cosmetic treatments. Tax due diligence is about quantifying risk as much as finding efficiency. This detailed approach ensures that the due diligence accounting for business acquisition process provides a clear, risk-adjusted view of the target’s true value.

The Due Diligence Process: A Practical Framework for Success

Executing a successful acquisition requires more than a cursory glance at a balance sheet. It demands a structured, multidisciplinary approach. We assemble a team of forensic accountants, corporate solicitors, and sector specialists to scrutinise every facet of the target entity. This collaborative effort ensures that financial data is interpreted within the correct legal and operational context. The scope of our investigation isn’t a fixed template; it’s a bespoke strategy dictated by the deal’s risk profile. For a £5 million local acquisition, we might focus heavily on cash flow and client concentration. For a £50 million corporate merger, the scope broadens to include complex cross-border tax structures and intricate intellectual property valuations.

Security and efficiency are paramount. We establish a secure Virtual Data Room (VDR) at the earliest opportunity to centralise document exchange. This platform maintains a rigorous audit trail and ensures sensitive commercial data remains confidential. The timeline for a thorough investigation typically spans six to eight weeks. It moves from the initial enquiry and data gathering through to management interviews and, finally, the delivery of a comprehensive report. This document acts as the foundation for the final Sale and Purchase Agreement (SPA).

Key Documents and Information Requests

A granular view of the target’s financial history is essential. We require specific documentation to verify the health of the business, including:

- Statutory accounts: Full HMRC tax returns and audited accounts for the previous five years to identify long-term trends.

- Employee obligations: A detailed breakdown of payroll, including PAYE compliance, National Insurance contributions, and defined benefit pension scheme liabilities.

- Asset registers: Comprehensive schedules of fixed assets, commercial leases, and any outstanding hire purchase agreements.

- Management accounts: Monthly reports from the current financial year to assess performance against original budgets.

Identifying and Managing Red Flags

Missing documentation or inconsistent financial explanations are rarely accidental. They often signal deeper systemic issues. If a target company cannot reconcile its reported EBITDA or shows irregularities in VAT filings, these are immediate red flags. Our role is to determine if these issues can be mitigated through price adjustments or if they represent a fundamental threat to the deal’s viability. If the due diligence accounting for business acquisition uncovers undisclosed liabilities or evidence of aggressive revenue recognition, walking away is often the most pragmatic solution.

To manage residual risks that cannot be fully audited, we frequently advise on the use of Warranties and Indemnities (W&I) insurance. This product has seen a 20% increase in adoption within UK mid-market transactions since 2023, providing a vital safety net for the buyer. It allows the transaction to proceed with an extra layer of financial protection against future claims.

Our firm provides the intellectual rigour and discretion necessary for complex transactions. Discover how our bespoke advisory services can protect your commercial interests during an acquisition.

From Findings to Integration: Optimising Your New Asset

The transition from investigation to ownership requires a pragmatic shift in focus. Once the due diligence accounting for business acquisition is complete, the resulting report serves as your primary lever for final negotiations. It isn’t merely a list of risks; it’s a roadmap for long-term value preservation. We use these findings to justify “price chips” in instances where assets were overvalued or liabilities were understated during initial discussions. By addressing these discrepancies before completion, you ensure the purchase price reflects the true economic reality of the target.

Refining the Business Valuation

Accounting red flags must translate directly into specific valuation adjustments. If a review uncovers a £75,000 discrepancy in aged debtors or unrecorded holiday pay, these figures should be deducted from the final headline price. We often recommend negotiating retention sums. This involves holding a portion of the purchase price in escrow for 12 to 24 months to cover potential historical tax liabilities that might emerge after the keys change hands. Structuring the deal with earn-outs further protects your capital, ensuring the seller’s incentives remain aligned with the target’s actual performance during your first year of ownership.

Strategic Growth and Future Planning

The first 100 days are critical for successful financial integration. A small business accountant plays a vital role during this period, moving beyond the audit to establish robust management accounts. These reports allow you to monitor KPIs from day one, ensuring the transition doesn’t disrupt liquidity or client service. We leverage due diligence findings to identify cost-saving synergies, such as consolidating supplier contracts or automating redundant payroll processes that were previously handled manually.

Effective cash flow management is the immediate priority. By implementing more efficient treasury systems early, you can capture the 15% to 20% operational efficiency gains often identified during the review process. A bespoke tax strategy should also be established immediately, particularly if you’re planning to expand the business nationally or into international markets by 2026. This proactive approach turns the due diligence accounting for business acquisition from a defensive necessity into a strategic advantage. It’s about ensuring the business you bought is the business you actually lead into the future, supported by a framework of financial clarity and commercial rigour.

Securing Your 2026 Acquisition Strategy

Navigating the complexities of a 2026 acquisition requires more than a cursory glance at financial statements. Success rests on forensic scrutiny that uncovers hidden liabilities and identifies genuine growth levers. By prioritising rigorous tax compliance and a structured framework for post-deal integration, you ensure the transition remains both profitable and stable. Effective due diligence accounting for business acquisition isn’t just a defensive measure; it’s a strategic tool for value creation that protects your capital.

At Davis & Co LLP, our Chartered Certified Accountants draw upon over a century of professional expertise to guide you through these high-stakes transitions. We specialise in international tax and complex growth advisory, providing the intellectual rigour needed to navigate the UK’s evolving regulatory landscape. Our reputation for discretion and understated professional excellence ensures your commercial interests are protected with the quiet confidence your business deserves. We focus on delivering bespoke solutions that align with your specific commercial objectives and long-term vision.

Secure your acquisition with bespoke due diligence from Davis & Co LLP. We look forward to supporting your next strategic milestone with the care and precision it demands.

Frequently Asked Questions

How long does financial due diligence usually take for a UK business acquisition?

Financial due diligence typically requires between four and eight weeks to complete. Smaller transactions involving owner-managed businesses might conclude within 30 days, while complex mid-market acquisitions often extend to 60 days or more. This timeline depends heavily on the quality of the target’s records and the responsiveness of their finance team. We recommend initiating this process as early as possible to avoid delays in the overall transaction timetable.

What is the difference between legal due diligence and accounting due diligence?

Legal due diligence examines the corporate structure, employment contracts, and potential litigation risks facing the business. In contrast, due diligence accounting for business acquisition focuses on the accuracy of financial statements, tax compliance, and historical cash flow. While legal teams secure the contractual protections, the accounting review ensures you’re paying a fair price based on verified earnings. Both streams must operate in parallel to provide a complete risk profile.

Is a “Quality of Earnings” report the same as a standard audit?

A Quality of Earnings report differs significantly from a statutory audit. While an audit verifies that financial statements follow accounting standards, a QoE report analyses the sustainability and “normalised” nature of the company’s profits. It identifies one-off gains or hidden expenses that an audit might ignore. For instance, industry data from 2024 shows that 72% of buyers identified EBITDA adjustments through QoE reports that weren’t visible in audited accounts.

Can due diligence findings help me negotiate a lower purchase price?

Findings often lead to a direct reduction in the final purchase price or an adjustment to the deal structure. If the process reveals undisclosed liabilities or overstated assets, you’ll have the evidence needed to renegotiate the Enterprise Value. We’ve seen cases where identifying aged debtors or tax risks resulted in a 10% to 15% reduction in the initial offer. It’s a pragmatic tool for ensuring the investment aligns with reality.

What are the most common financial red flags in small business acquisitions?

Common red flags include declining gross margins and high customer concentration where a single client represents over 20% of revenue. You should also watch for significant discrepancies between management accounts and VAT returns. In small UK firms, the commingling of personal and business expenses is frequent. If 15% of expenses appear unrelated to core operations, it suggests the reported profit figures require deep scrutiny before you commit capital.

How much does a professional due diligence report typically cost?

Professional fees for financial due diligence usually range from £5,000 for very small businesses to over £25,000 for mid-market transactions. According to 2024 market benchmarks, buyers should budget approximately 1% to 2% of the total deal value for comprehensive professional advice. This investment acts as an insurance policy against future losses. We provide bespoke quotes tailored to the specific complexity and turnover of the target company.

Should I conduct due diligence before or after signing a Letter of Intent (LOI)?

You’ll typically perform the bulk of your due diligence accounting for business acquisition after signing a Letter of Intent. The LOI provides a period of exclusivity; this ensures the seller doesn’t negotiate with others while you spend money on professional fees. However, performing “red flag” checks on basic tax and turnover data before the LOI is signed is a wise strategy. It prevents you from wasting time on fundamentally flawed deals.

What happens if the seller refuses to provide certain financial documents?

A seller’s refusal to disclose financial information is a serious warning sign that often halts a transaction. If the documents are sensitive, we suggest using a secure virtual data room with restricted access or a “clean team” arrangement. If they still won’t comply, you should consider walking away or insisting on robust warranties and indemnities. Transparency is the foundation of a successful acquisition; its absence usually indicates hidden liabilities.