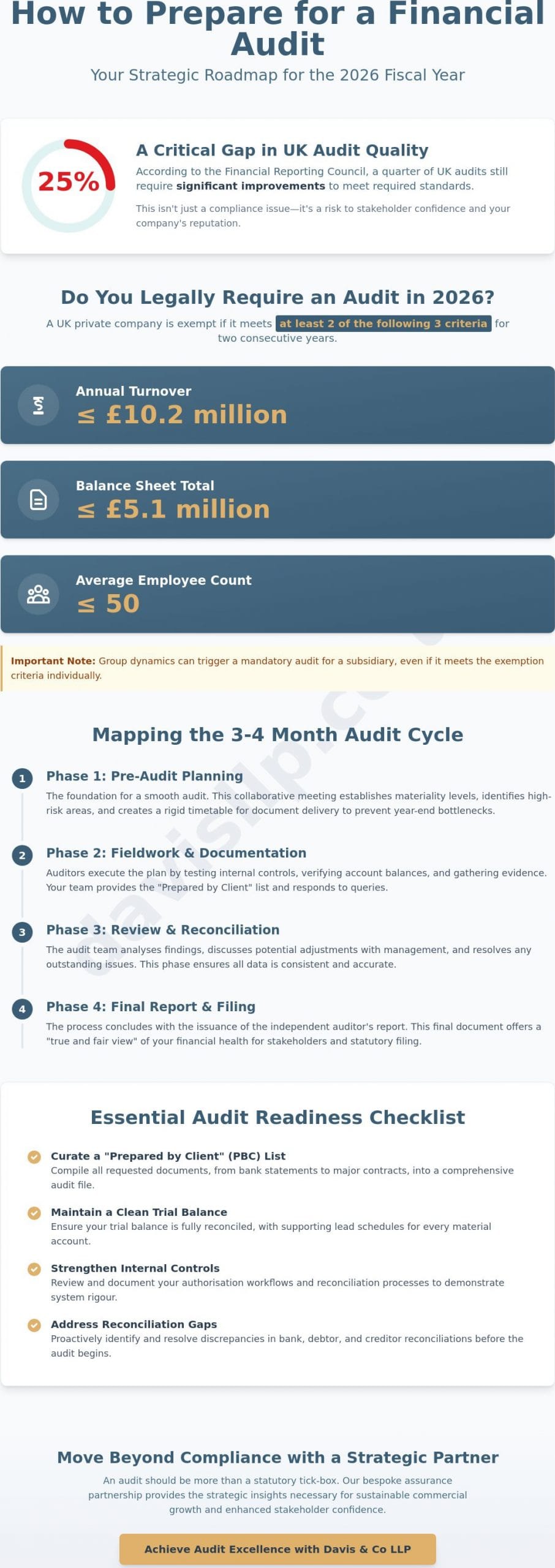

According to the Financial Reporting Council’s latest inspection findings, 25% of audits in the UK still require significant improvements to meet required standards. For most directors, the annual review feels like an intrusive drain on internal resources rather than a constructive exercise. You likely recognise the tension of balancing daily operations with these rigorous demands, often fearing that a minor oversight might lead to material misstatements or reputational damage. Understanding how to prepare for a financial audit with precision is no longer just a compliance task; it’s a strategic necessity for the 2026 fiscal year.

We believe the audit process should offer more than just a statutory tick. Our framework ensures you achieve a clean report while identifying pragmatic ways to refine your internal controls and bolster stakeholder confidence. By following this structured approach, you’ll reduce the time your finance team spends on reactive queries and enhance your credibility with lenders. We’ll examine the essential documentation, the timeline for preparation, and the bespoke strategies that turn a complex obligation into a clear roadmap for commercial growth.

Key Takeaways

- Identify whether your business meets the 2026 UK statutory audit thresholds for turnover, balance sheet total, and employee count to ensure full regulatory compliance.

- Master the 3-4 month audit cycle by prioritising the planning phase, a critical step to avoiding year-end bottlenecks and ensuring a smooth reporting process.

- Learn exactly how to prepare for a financial audit by curating a comprehensive “Prepared by Client” (PBC) list and maintaining a clean Trial Balance with supporting lead schedules.

- Strengthen your internal controls and authorisation workflows to address common reconciliation gaps and demonstrate the rigour of your accounting systems.

- Discover how a bespoke assurance partnership moves beyond basic compliance to provide the strategic insights necessary for sustainable commercial growth.

Understanding Statutory Thresholds and the Strategic Value of Assurance

A financial audit serves as a rigorous, independent examination of an entity’s financial statements to ensure they provide a true and fair view of its fiscal health. For UK directors, understanding these requirements is the first step in learning how to prepare for a financial audit effectively. While the process is often viewed through the lens of compliance, we view it as a strategic tool for assurance. This concept moves beyond mere arithmetic; it provides a verified narrative of stability to shareholders, creditors, and potential investors. By providing this level of transparency, a business demonstrates a commitment to governance that resonates with high-calibre stakeholders.

Do You Legally Require an Audit in 2026?

Under current UK legislation, a private limited company is generally exempt from a statutory audit if it qualifies as a small company. To maintain this exemption in 2026, a business must meet at least two of the following three criteria for two consecutive years: an annual turnover of no more than £10.2 million, a balance sheet total of not more than £5.1 million, and an average of 50 or fewer employees. The Financial Reporting Council (FRC) oversees these standards to maintain market integrity and ensure that larger entities remain accountable to the public interest. Complexity arises with subsidiary companies. If a parent company guarantees the liabilities of a subsidiary, that subsidiary might bypass the audit; however, being part of a larger group can often trigger a mandatory audit regardless of the individual entity’s size. We often find that mid-market firms overlook these group dynamics, leading to last-minute compliance hurdles.

The Business Case for Voluntary Audits

Many boards opt for a voluntary audit to facilitate smoother transitions in management accounting or to prepare for aggressive growth phases. High-street lenders and international partners often require audited accounts as a prerequisite for substantial credit facilities or joint ventures. This level of transparency is vital when seeking private equity investment, where rigorous due diligence is the standard. Engaging a small business accountant with specific expertise in 2026 regulations ensures that your internal controls are robust enough to withstand such scrutiny. When you consider how to prepare for a financial audit, treating it as a value-add exercise rather than a legal burden allows for more precise strategic planning. It identifies systemic weaknesses before they become liabilities, offering a bespoke roadmap for fiscal improvement. This proactive approach builds a foundation of trust that is indispensable for any firm looking to expand its footprint in a competitive global market.

Mapping the Audit Timeline: From Planning to Final Report

A standard UK corporate audit isn’t a week-long event. It’s a structured cycle that typically spans three to four months. We view this period as a collaborative effort between your internal finance team and the lead auditor. The lead auditor acts as a primary point of contact, ensuring that communication remains transparent and that expectations are aligned from the outset. Early engagement helps us avoid the common bottlenecks that occur when businesses wait until the final quarter to organise their records. Knowing how to prepare for a financial audit involves understanding that the process is a marathon of precision, not a sprint to the filing deadline.

Phase 1: The Pre-Audit Planning Meeting

The pre-audit planning meeting serves as the foundation for a successful engagement. During this session, we establish materiality levels. For a mid-sized UK firm with a turnover of £25 million, a materiality threshold might be set at 1% to 2% of revenue, depending on the specific risk profile. Identifying high-risk areas early allows the team to focus resources where they matter most. To facilitate an efficient audit, this phase must produce a rigid timetable for document delivery. This prevents operational friction and ensures that statutory deadlines, such as the nine-month filing window for private limited companies at Companies House, are met without haste. We also define the scope for any specialised requirements, such as international reporting standards if you operate across borders.

Phase 2: Fieldwork and Substantive Testing

Fieldwork represents the most intensive stage of the process. Whether auditors work on-site at your offices or remotely via cloud-based accounting software, the objective remains the same. They’ll perform substantive testing. This includes verifying physical assets, checking transaction samples, and seeking third-party confirmations for bank balances or trade debtors. Managing “Audit Queries” efficiently is the best way to prevent delays. We recommend appointing a dedicated liaison within your finance department to handle these requests promptly. This structured approach is central to our bespoke advisory services, ensuring that the audit process supports rather than hinders your commercial objectives.

The cycle concludes with the completion phase. This is when the lead auditor reviews the findings and discusses any necessary adjustments with your board. By the time the final audit opinion is issued, there should be no surprises. The goal is a clean report that provides stakeholders with the assurance they require. Understanding how to prepare for a financial audit in this way ensures that the final report is a true reflection of your company’s financial health, issued with the professional gravitas your stakeholders expect.

Essential Documentation: Creating Your Audit Readiness File

Understanding how to prepare for a financial audit begins with the construction of a robust “Prepared by Client” (PBC) list. This isn’t merely a folder of receipts; it’s a structured evidence base that validates every figure within your accounts. We’ve observed that businesses providing a clean Trial Balance alongside detailed lead schedules for every balance sheet item can reduce audit duration by up to 25%. Precision at this stage prevents the protracted queries that often inflate professional fees and disrupt daily operations.

Digital record-keeping plays a decisive role in modern compliance. By 2026, the transition to cloud-based evidence is expected to be the standard for UK mid-market firms. Centralising invoices, receipts, and reconciliations in a digital environment allows auditors to perform verification tasks remotely. This accelerates the process and ensures that the “audit trail” is visible, chronological, and tamper-proof.

Financial Statements and Lead Schedules

Your audit file should contain a final draft of the profit and loss account, the balance sheet, and a comprehensive cash flow statement. Each line item requires a supporting lead schedule that breaks down the aggregate figure. For fixed assets, you must provide a register detailing original costs, additions, disposals, and specific depreciation calculations. We find that reconciling bank statements, loan agreements, and hire purchase (HP) contracts to the exact penny is vital. Even a minor discrepancy of £10 in a £250,000 balance can trigger wider sample testing, so accuracy is paramount.

- Trade Debtors: Provide an aged debtor report that matches the balance sheet total.

- Trade Creditors: Include supplier statements for your top ten creditors by value.

- Accruals and Prepayments: Maintain a clear spreadsheet showing the period each cost relates to.

Legal and Statutory Documentation

Statutory records are frequently overlooked, yet they’re often the first items a diligent auditor examines. You must ensure your Company Secretarial records match Companies House filings exactly. This includes up-to-date share registers and signed board minutes from the entire financial year. These minutes provide the legal context for major business decisions, such as dividend declarations or capital expenditure approvals.

You’ll also need to provide copies of major commercial contracts, property leases, and employment agreements for key personnel. For firms with global footprints, clear documentation regarding international tax planning is essential to justify cross-border transfer pricing and specific tax treatments. Having these legal documents indexed and ready demonstrates a level of corporate governance that instils immediate confidence. It transforms the audit from a stressful interrogation into a structured validation of your firm’s integrity.

Strengthening Internal Controls and Addressing Reconciliation Gaps

Auditors view your financial statements as the final output of a wider operational engine. They don’t just verify the figures on the page; they scrutinise the design and efficacy of the accounting system itself. Understanding this systemic focus is a vital component of knowing how to prepare for a financial audit effectively. If your internal controls are deemed weak, the audit team will likely increase the volume of testing, leading to higher costs and longer timelines. A 2024 report by the Financial Reporting Council highlighted that internal control failures contributed to 22% of audit quality concerns in the UK, a figure that businesses should aim to avoid through proactive preparation.

Conducting a “pre-audit” internal review is a pragmatic step to identify obvious errors in VAT returns or payroll records. We recommend reviewing your PAYE settlements and ensuring that your VAT 100 reports align perfectly with your general ledger. This process allows you to address discrepancies before they’re flagged by external eyes. The goal is to present a clean trial balance that reflects a disciplined financial environment.

The Importance of Segregation of Duties

In many UK SMEs, a single individual often manages a transaction from its inception to the final payment. This lack of oversight represents a significant risk profile. Ideally, the person who authorises a purchase order shouldn’t be the same individual who records the invoice or executes the bank transfer. For smaller teams where staff numbers are limited, we suggest implementing digital authorisation limits within your accounting software. Platforms like Xero or Sage allow for bespoke permission levels, ensuring that a “four-eyes” principle is applied to high-value transactions. These digital footprints provide the quiet assurance of oversight that auditors value during their risk assessment.

Closing the Month-End and Year-End Gaps

Cut-off procedures are a frequent source of friction during the audit process. You must ensure that revenue is recognised in the correct period, particularly for services delivered across the financial year-end. This requires a rigorous review of accrued and deferred income. Similarly, inter-company balances must be reconciled and formally agreed upon by all parties before the audit commences. Discrepancies in these areas often signal wider control failures to the audit team. Substantive testing is the process of verifying account balances through direct evidence. By preparing this evidence in advance, you streamline the auditor’s ability to confirm your figures.

The audit process shouldn’t be viewed as a purely retrospective exercise. The resulting Management Letter provides a strategic roadmap, highlighting operational improvements and control enhancements for the following fiscal year. It’s a valuable tool for long-term commercial stability.

If you require assistance in refining your internal frameworks before your next statutory deadline, our advisory team provides bespoke reviews to ensure your business is audit-ready.

Navigating the Audit with Davis & Co LLP: A Composed Partnership

We view the audit process as an opportunity for refinement rather than a mere statutory obligation. Our Audit and Assurance service provides the intellectual rigour required to transform raw data into a strategic roadmap for your firm. By maintaining a sense of composed partnership, we ensure that the transition through the reporting season is steady and deliberate. This approach moves beyond basic compliance, allowing us to identify operational inefficiencies that might otherwise remain obscured. In our experience, a well-executed audit can identify bottlenecks that, when resolved, can unlock up to 15% more liquidity within annual cash flow cycles.

Our commitment to discretion and professional gravitas means we respect the sensitive nature of your commercial data. We don’t just deliver a report; we provide a high-calibre analysis of your business’s health. This includes:

- Identifying risks before they escalate into structural liabilities.

- Evaluating the strength of internal controls to prevent financial leakage.

- Providing a clear, objective perspective that reassures stakeholders and lenders.

- Ensuring your financial statements reflect the true value and potential of your enterprise.

Bespoke Solutions for Complex Financial Structures

For entities operating across borders or within niche markets, a standard approach is rarely sufficient. We specialise in managing the intricacies of international tax and multi-jurisdictional reporting, ensuring your UK operations remain aligned with global standards. Whether you are managing a dental practice with complex associate contracts or a property investment portfolio with diverse holding structures, our team applies industry-specific expertise to your unique situation. We seamlessly integrate expert tax advice into our broader assurance framework, ensuring that tax efficiency and statutory compliance work in tandem. This holistic view is vital for maintaining the integrity of complex financial hierarchies.

Your Next Steps Toward Audit Readiness

The most effective way to manage the pressure of a deadline is through early engagement. Understanding how to prepare for a financial audit effectively allows a business to treat the process as a diagnostic tool for future scaling. We recommend an initial consultation to assess your current systems and identify any gaps in your documentation. Moving from basic bookkeeping to an audit-ready financial function requires a logical progression, and we’re here to guide that transition with precision. Our preliminary reviews help ensure that by the time the formal audit commences, your team is confident and your records are beyond reproach.

If you require a partner who values quiet excellence and strategic clarity, we invite you to reach out. Contact Davis & Co LLP to discuss your audit and assurance requirements and secure the future of your financial reporting.

Securing Your Commercial Future Through Audit Readiness

A successful audit in 2026 requires a proactive stance that begins long before the first site visit. By addressing reconciliation gaps and establishing a comprehensive audit readiness file, you ensure your business meets the statutory turnover threshold of £10.2 million with total transparency. This process shouldn’t be viewed as a mere year-end hurdle; it’s a rigorous health check that validates your internal controls and supports your broader commercial objectives.

Mastering how to prepare for a financial audit allows your leadership team to focus on complex growth and international tax strategies without the distraction of avoidable compliance delays. Drawing on our 120-year heritage as Chartered Certified Accountants, we provide the steady hand and technical precision required to navigate these regulatory waters. We act as strategic advisors, ensuring your financial reporting reflects the true strength of your enterprise.

Partner with Davis & Co LLP for bespoke audit and assurance services to gain the clarity your business deserves. We’re here to help you turn compliance into a cornerstone of your success.

Frequently Asked Questions

What are the UK audit thresholds for 2026?

For the 2026 financial year, a UK company generally requires a statutory audit if it meets at least two of the following criteria: an annual turnover exceeding £15 million, gross assets over £7.5 million, or more than 50 employees. These revised thresholds, introduced by the Department for Business and Trade, aim to reduce the regulatory burden on medium sized entities. We recommend reviewing your specific group structure, as subsidiary status or shareholder requests can often mandate an audit regardless of these limits.

How long does a typical financial audit take for a UK SME?

A typical financial audit for a UK SME usually spans between four and six weeks from the initial planning phase to the final signing of the accounts. The intensive fieldwork stage, where auditors work within your systems, typically lasts two weeks. Understanding how to prepare for a financial audit effectively can reduce this timeline. Delays often stem from incomplete documentation or complex technical accounting treatments that require additional partner review.

What is the difference between a financial audit and an independent review?

A financial audit provides “reasonable assurance” through substantive testing and evidence gathering to confirm that accounts are free from material misstatement. In contrast, an independent review offers “limited assurance” and relies primarily on analytical procedures and management enquiries. While a review is less invasive and more cost effective, it doesn’t provide the same level of comfort to external stakeholders like lenders or institutional investors.

Can my own bookkeeper perform our statutory audit?

Your internal bookkeeper or the firm that prepares your statutory accounts cannot perform your audit due to strict independence requirements under the FRC Ethical Standard. An auditor must remain objective and cannot audit their own work or provide significant non audit services that create a self review threat. This separation ensures the integrity of the financial statements and maintains the trust of your shareholders and creditors.

What happens if the auditors find an error in our accounts?

If an auditor identifies an error, they’ll propose an adjustment for your team to process before the accounts are finalised. If the error is material and management refuses to correct it, the auditor may issue a qualified opinion or an adverse report. We find that most discrepancies are resolved through transparent dialogue and technical adjustments during the closing stages of the engagement.

Is a voluntary audit worth the investment for a growing business?

Choosing a voluntary audit is often a strategic decision for businesses planning an exit or seeking significant external funding. It demonstrates a commitment to financial transparency and robust internal controls, which can increase a company’s valuation during due diligence. Many of our clients find that the discipline required for an audit prepares the finance function for future scaling and provides peace of mind to minority shareholders.

How much does a financial audit cost in the UK?

Audit fees in the UK vary significantly based on turnover and sector complexity, with small to medium sized enterprises typically paying between £10,000 and £35,000. Larger or more complex entities with international subsidiaries may see fees exceeding £50,000. These figures reflect the professional time required to meet the rigorous standards set by the Financial Reporting Council and the specific risk profile of the business.

What is a PBC list in auditing terms?

A PBC list, or “Provided By Client” list, is a comprehensive schedule of documents and data that the auditors require to begin their testing. This typically includes bank reconciliations, aged debtor reports, and lead schedules for all balance sheet accounts. Providing these items accurately and on time is the most critical step in learning how to prepare for a financial audit, as it prevents bottlenecks during the fieldwork phase.