What if the property you inherited or the home you couldn’t sell is actually a sophisticated tax trap waiting to be triggered? For many, becoming a landlord was never a deliberate career choice, but the 2026/27 tax year demands that you treat it with the same rigour as a commercial enterprise. Seeking expert tax advice for accidental landlords is no longer a luxury; it’s a necessity for those who wish to avoid the 24% Capital Gains Tax rate on residential property or the implications of the frozen £12,570 Personal Allowance.

We understand that you may feel overwhelmed by the transition from homeowner to property manager, especially with the fear of HMRC penalties for non-disclosure looming. This guide will show you how to master the complexities of property taxation and transform an unexpected rental into a strategically managed asset. We’ll provide a clear roadmap for long-term management, offering the bespoke insight required to handle the 20% mortgage interest tax credit and the mandatory digital record-keeping requirements starting 6 April 2026.

Key Takeaways

- Understand how your rental income is aggregated with your existing salary, which may trigger higher tax bands and affect your available Personal Allowance.

- Learn to distinguish between deductible revenue expenses and capital improvements to ensure your property remains a tax-efficient asset under current statutory rules.

- Prepare for the eventual disposal of your property by navigating the 18% and 24% Capital Gains Tax rates through the strategic application of available reliefs.

- Discover why professional tax advice for accidental landlords is essential for identifying bespoke mitigation opportunities that automated software often overlooks.

- Align your property management with the 2026 Making Tax Digital requirements to maintain full compliance and ensure a seamless transition to quarterly reporting.

Defining the Accidental Landlord: Common Scenarios and 2026 Obligations

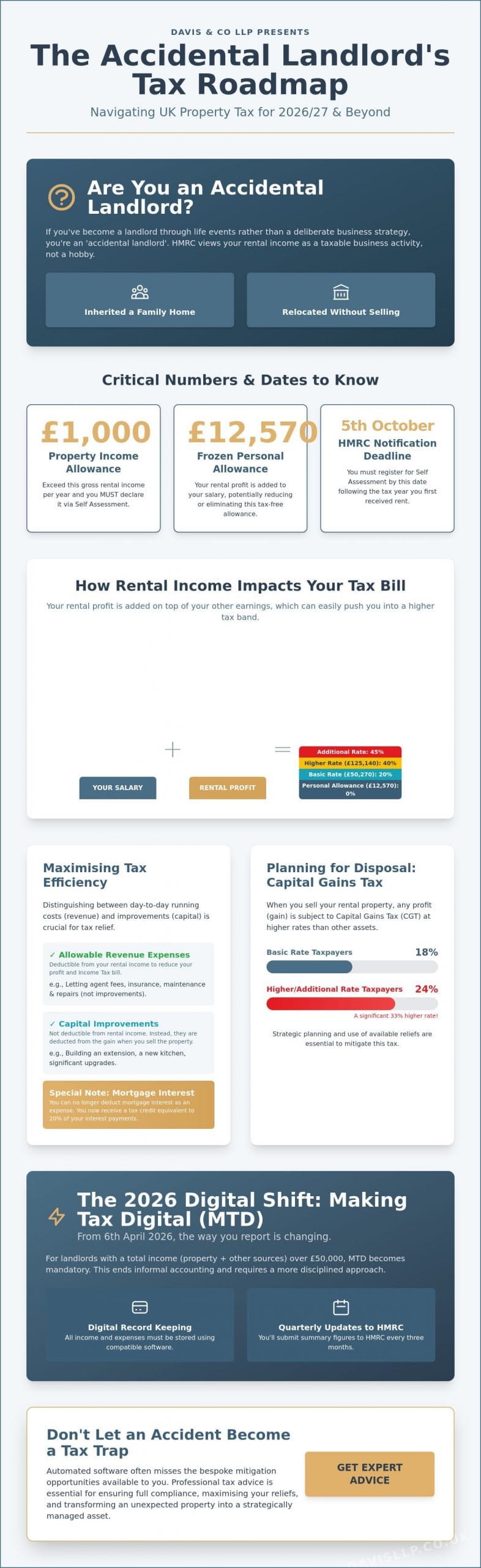

Becoming an accidental landlord often happens through life events rather than a deliberate commercial strategy. Whether you’ve inherited a family home or relocated for a professional opportunity without selling your primary residence, you’ve entered the complex framework of the UK tax system. While you might view the arrangement as a temporary solution or a side project, HMRC considers any rental income above the £1,000 Property Income Allowance to be a taxable business activity. Failing to recognise this transition can lead to significant penalties, especially as we approach the stricter digital reporting standards of 2026. Seeking professional tax advice for accidental landlords ensures that these unexpected assets are managed with the same intellectual rigour as a dedicated property portfolio.

HMRC does not recognise the concept of a “hobby landlord” if financial thresholds are met. If you receive more than £1,000 in gross rental income annually, you’re required to declare it. We often see clients surprised by the speed at which a personal asset becomes a statutory obligation. This is why our bespoke approach focuses so heavily on the 2026/27 transition; the introduction of Making Tax Digital (MTD) for those earning over £50,000 on 6 April 2026 leaves no room for informal accounting. We’re here to ensure your transition is a strategic move rather than a compliance risk.

The Immediate Compliance Checklist

Your first obligation is to notify HMRC by 5 October following the end of the tax year in which you first received rental income. You’ll need a Unique Taxpayer Reference (UTR) to file through Self Assessment, even if you don’t expect to make a profit initially. Beyond the Revenue, you must obtain “Consent to Let” from your mortgage provider and update your buildings insurance to a landlord-specific policy. Ignoring these steps can invalidate your coverage or breach your lending terms, creating unnecessary financial exposure.

Property Ownership and Tax Liability

When a property is owned jointly, typically with a spouse or civil partner, HMRC usually assumes a 50/50 split of income for tax purposes. If your actual ownership shares are different, you must submit Form 17 to ensure your tax liability reflects the true distribution of income. This is a vital component of tax advice for accidental landlords, as it can prevent one partner from being unnecessarily pushed into a higher tax bracket. Beneficial interest is the right to receive income or profit from a property, regardless of whose name appears on the legal title. We work with you to ensure these interests are documented correctly, providing a stable foundation for your long-term property accounting.

Navigating Income Tax and the Self Assessment Framework

Rental income isn’t taxed in isolation. It’s aggregated with your salary, pension, and other earnings, which often catches accidental landlords off guard. For the 2026/27 tax year, the Basic Rate of 20% applies to income between £12,571 and £50,270. If your combined income exceeds £50,271, you’ll enter the 40% Higher Rate band. For those with significant earnings, the 45% Additional Rate now triggers at £125,141. We find that many clients inadvertently cross these thresholds once rental profits are added to their professional salaries. Comprehensive tax advice for accidental landlords is essential to prepare for these shifts in your marginal tax rate.

The official government guidance on rental income highlights the £1,000 Property Income Allowance. This is a tax-free amount you can use if your expenses are minimal. However, if your costs for maintenance, insurance, and management exceed £1,000, it’s almost always more efficient to claim actual expenses instead. You can’t claim both, so we meticulously analyse your records to determine which path offers the greatest relief. Managing the Self Assessment cycle requires a steady, disciplined approach. The tax year ends on 5 April, and you have until 31 January 2027 to file online and pay your balancing payment for the 2025/26 year. If your tax bill exceeds £1,000, you’ll also likely face “payments on account” in January and July, which can significantly impact your cash flow if you haven’t prepared.

The Impact of Frozen Personal Allowances

The Personal Allowance remains frozen at £12,570 in 2026, a policy expected to last until 2031. This creates “fiscal drag,” where inflation-linked rent increases push you into higher tax brackets while your tax-free threshold stays static. Additionally, if your total income exceeds the High Income Child Benefit Charge (HICBC) threshold, you may lose some or all of your Child Benefit. Seeking expert tax advice in the UK allows us to identify bespoke strategies to mitigate these hidden costs. If you’re concerned about how these thresholds affect your net position, we can provide a tailored review of your personal tax services.

International Considerations for Non-Resident Landlords

If you’ve relocated abroad but kept your UK home as a rental, you fall under the Non-Resident Landlord Scheme (NRLS). By default, letting agents must withhold 20% tax from your rent and pay it to HMRC. However, we can assist you in applying for an exemption to receive rent gross, provided your tax affairs are up to date. Our expertise in international tax planning ensures that you remain compliant across jurisdictions while avoiding the complexities of double taxation. This proactive approach ensures your move abroad doesn’t result in unnecessary cash flow restrictions.

Maximising Tax Efficiency: Allowable Expenses and Interest Relief

Identifying the distinction between what can be deducted from your rental income and what must be capitalised is fundamental to protecting your yields. HMRC applies a strict “wholly and exclusively” test to all property expenses. This means any cost you claim must be incurred solely for the purpose of your rental business. For many, professional tax advice for accidental landlords is the only way to ensure that these boundaries are respected while still minimising the overall tax burden. Proper classification of these costs ensures you don’t inadvertently trigger an enquiry through aggressive or incorrect deductions.

Revenue expenditure refers to the day-to-day running costs of the property, such as insurance, letting agent fees, and general maintenance. These are fully deductible from your rental income before tax is applied. Conversely, capital expenditure includes costs that add value to the property or extend its life, such as a loft conversion or a full kitchen upgrade. While these cannot be deducted from your annual income tax, they’re essential for reducing your Capital Gains Tax liability when you eventually sell the asset. We also advise clients on the Replacement of Domestic Items Relief, which allows you to deduct the cost of replacing furniture, appliances, and floor coverings, provided the new item is a like-for-like replacement and not a significant upgrade.

Understanding the Section 24 Interest Restriction

The most significant challenge for modern landlords is the Section 24 restriction on mortgage interest. You can no longer deduct mortgage interest or other finance costs from your rental income to arrive at a taxable profit. Instead, you receive a basic rate tax credit equal to 20% of your interest payments. This change disproportionately affects those in the higher or additional rate tax bands. Under the Section 24 regime, landlords are taxed on their total rental income before mortgage interest is considered; they then receive a 20% tax credit on those interest payments, which can lead to a situation where the tax due actually exceeds the net cash profit for those in the 40% or 45% brackets.

Common Deductible vs. Non-Deductible Costs

Differentiating between a “repair” and an “improvement” is a common area of confusion. Replacing a broken window with a modern double-glazed equivalent is generally considered a repair and is therefore deductible. However, adding a conservatory where none existed is an improvement and must be treated as capital expenditure. To ensure your records are robust, you should maintain a digital ledger of all receipts and invoices. This is particularly vital as we prepare for the 2026 Making Tax Digital requirements. Professional fees for property accounting are also deductible, and many clients find that the insight provided by a small business accountant pays for itself by uncovering legitimate reliefs that might otherwise be overlooked. We recommend keeping these records for at least six years to meet statutory requirements and defend your position in the event of an HMRC audit.

Strategic Planning for Disposal: Capital Gains Tax and Reliefs

Selling a property that was once your home involves more than finding a buyer; it requires a precise calculation of your Capital Gains Tax (CGT) liability. For the 2026/27 tax year, residential property gains are taxed at 18% for basic rate taxpayers and 24% for those in the higher or additional brackets. Unlike other assets, the UK government enforces a strict 60-day window from the date of completion to report the disposal and pay the tax due. This applies to non-resident landlords as well, who must often report the sale even if no tax is owed. Missing this deadline triggers immediate penalties, making timely tax advice for accidental landlords a critical component of the sale process.

The clock starts immediately upon completion. Obtaining a professional valuation at the point the property was first let is a strategic necessity. This figure helps establish the base cost for the period the property functioned as an investment rather than a residence. Without this data, you risk overpaying tax or failing to justify your calculations during an HMRC audit. We recommend securing these valuations early to ensure your long-term property accounting remains robust and defensible. It’s much harder to argue for a historical value years after the fact.

Private Residence Relief (PRR) and Letting Relief

PRR remains the most significant tool for reducing your tax bill. It exempts the proportion of the gain relating to the time you occupied the property as your only or main residence. Under current 2026 rules, the final 9 months of ownership are also qualifying periods, regardless of whether you lived there. However, the generous Letting Relief that once benefited many was severely restricted in April 2020. It’s now only available to landlords who lived in the property alongside their tenants, which effectively excludes the vast majority of accidental landlords who have moved out entirely.

Offseting Capital Costs

While you can’t deduct improvements from your annual income tax, these costs are vital for reducing your capital gain. Structural changes, such as a loft conversion or a new central heating system, are all deductible upon sale. You should also include acquisition and disposal costs, such as Stamp Duty Land Tax paid at purchase, legal fees, and estate agent commissions. Maintaining meticulous records of these capital items over several years is essential for a successful disposal. If you’re planning an exit from your property investment, our personal tax services can help you quantify these reliefs and ensure full compliance with the 60-day reporting mandate.

Beyond Compliance: Professional Property Accounting and Bespoke Advisory

While digital tools can facilitate basic data entry, they’re no substitute for the intellectual rigour of a dedicated advisor. Compliance is merely the baseline of our service. Our goal is to move you beyond simple filing and into a state of strategic clarity. For those seeking tax advice for accidental landlords, the difference between a software-generated return and a bespoke plan can represent thousands of pounds in saved liability over the 2026/27 tax year. We pride ourselves on a philosophy of quiet excellence, where our reputation is built on the stability and precision we offer our clients.

Software often overlooks the commercial realities of your life. It won’t tell you if you’re overpaying on your mortgage interest because of a poorly timed renovation, nor will it flag the long-term Inheritance Tax (IHT) implications of your new rental income. A Chartered Accountant identifies these nuances, providing a pragmatic bridge between statutory requirements and your personal financial goals. We ensure your records are not just compliant but are also robust enough to withstand the most rigorous HMRC enquiry. Property assets held for the long term can become significant IHT liabilities if not structured correctly, and we work to ensure that your unexpected entry into the rental market doesn’t compromise your family’s future security.

The Value of Bespoke Tax Planning

Tailored advice is the only effective shield against “tax traps” like the High Income Child Benefit Charge or the tapering of the Personal Allowance for those earning over £100,000. Professional property accounting allows you to manage your cash flow with confidence, ensuring you have the liquidity required for your January and July tax payments. We act as a strategic partner. Our approach helps both private individuals and commercial entities navigate the complexities of the 2026 fiscal environment. This collaborative partnership ensures you feel secure and well-advised at every turn, turning an accidental asset into a cornerstone of your wealth.

Ensuring Long-Term Security

Reliability is the cornerstone of our practice. We provide audit-ready financial reporting that gives you peace of mind, knowing your property assets are managed with absolute discretion and expertise. The process of becoming a client is deliberate and considered, beginning with a thorough review of your current position and long-term objectives. This rhythmic consistency helps to build a sense of trust and stability in an often volatile regulatory environment. If you’re ready to transition your property from an accidental burden to a strategically managed asset, we invite you to contact us for a consultation on property tax strategy.

Strategising for Longevity in a Shifting Fiscal Environment

The transition from homeowner to landlord is a significant professional shift that demands technical precision and foresight. We’ve explored how navigating the 2026/27 tax bands and mastering the 60-day Capital Gains Tax reporting window are no longer optional tasks for the modern property owner. By correctly distinguishing between revenue and capital expenditure and preparing for the 6 April 2026 digital reporting mandate, you can transform an unexpected rental into a resilient, high-performing asset.

Expert tax advice for accidental landlords provides the intellectual rigour necessary to navigate these complexities without the stress of potential HMRC penalties. As Chartered Certified Accountants with over 120 years of expertise, we specialise in international and property tax planning for high-net-worth and professional clients. We offer bespoke solutions that ensure your portfolio remains efficient, compliant, and audit-ready in an increasingly digital landscape.

Consult Davis & Co LLP for bespoke tax advice for accidental landlords to ensure your property remains a secure foundation for your long-term wealth. We’re here to provide the steady, deliberate guidance you need to move forward with confidence.

Frequently Asked Questions

Do I have to pay tax if the rent is lower than my mortgage payment?

You may still have a tax liability even if your rental income doesn’t cover your monthly mortgage payment. HMRC calculates tax on profit rather than cash flow; since mortgage capital repayments aren’t deductible and interest relief is restricted to a 20% tax credit, your taxable profit might exceed the actual cash you have remaining. This often surprises those who view their property through a purely personal financial lens rather than a statutory one.

How do I register as a landlord with HMRC for the first time?

You must register for Self Assessment by 5 October following the end of the tax year in which you first received rental income. This process generates a Unique Taxpayer Reference (UTR), which is essential for filing your annual returns. If you’re earning over £50,000 in gross property income, you’ll also need to ensure your registration is compatible with the Making Tax Digital requirements starting 6 April 2026.

What happens if I forget to declare my rental income for several years?

Failing to declare income can lead to significant penalties and interest charges from HMRC. It’s advisable to use the Let Property Campaign to make a voluntary disclosure; this proactive approach often results in lower penalties than if HMRC discovers the non-disclosure through its own data-matching systems. Seeking professional tax advice for accidental landlords is the most reliable way to regularise your affairs while minimising potential exposure.

Can I still claim wear and tear allowance on my rental property?

The 10% Wear and Tear Allowance was abolished in April 2016 and replaced by the Replacement of Domestic Items Relief. This allows you to deduct the actual cost of replacing furniture, appliances, and floor coverings on a like-for-like basis. You can’t claim for the initial purchase of these items when you first let the property, only for their subsequent replacement when they’re no longer fit for purpose.

Is it better to put my rental property into a limited company?

Incorporation can be tax-efficient for higher-rate taxpayers seeking to reinvest profits, but it isn’t a universal solution. Moving an existing property into a company triggers Stamp Duty Land Tax and Capital Gains Tax, so bespoke tax advice for accidental landlords is necessary to determine if the long-term benefits outweigh these immediate entry costs. We often find that for a single property, the administrative costs of a company may outweigh the tax savings.

Do I need to pay Stamp Duty if I inherit a property and decide to rent it out?

You generally don’t pay Stamp Duty Land Tax on properties you inherit through a will. However, if you choose to purchase an additional share from another beneficiary or take over an existing mortgage on the property, SDLT may become due based on the value of the consideration given. It’s important to document these transactions carefully to ensure your base cost is accurately recorded for future Capital Gains Tax calculations.

How does living abroad affect the tax I pay on my UK rental property?

Living abroad places you under the Non-Resident Landlord Scheme, where letting agents must withhold 20% of your rent for HMRC unless you’ve been granted an exemption. You’re still liable for UK tax on UK property income, though most UK nationals and EEA residents retain their £12,570 Personal Allowance to offset against these profits. We assist many clients in navigating these cross-border obligations to ensure they don’t suffer from double taxation.

What is the 60-day rule for Capital Gains Tax on property sales?

The 60-day rule requires you to report the sale of a UK residential property and pay any Capital Gains Tax due within 60 days of the completion date. This is a mandatory statutory deadline; failure to comply results in immediate late-filing penalties and accruing interest. This rule applies even if you’re already registered for Self Assessment, as the disposal must be reported through a separate capital gains property account.