The traditional model of individual property ownership is no longer just inefficient; for many, it’s becoming a liability. As the 2026/27 fiscal year unfolds, the combination of frozen thresholds and the persistent weight of Section 24 finance cost restrictions continues to erode the margins of even the most seasoned investors. Achieving genuine property portfolio tax optimisation now requires a shift from reactive accounting to proactive, multi-generational structuring. We understand that seeing your hard-earned rental profits diminished by a 20 percent tax credit cap, while facing a 24 percent Capital Gains Tax on disposals, creates a profound sense of frustration for those seeking to grow their wealth.

This guide provides a clear roadmap to help you reclaim control over your net cash flow and protect your family’s legacy. We’ll explore how sophisticated structural alignment, including the strategic use of limited companies and trust tax services, can mitigate the impact of the significant tax rate increases scheduled for April 2027. By the end of this article, you’ll have a comprehensive understanding of how to balance immediate liquidity with a secure succession plan that respects the new one million pound cap on business property relief. Our goal is to ensure your portfolio remains a robust vehicle for long-term prosperity in a shifting regulatory environment.

Key Takeaways

- Identify the core shifts in the 2026 fiscal landscape that necessitate a move from reactive compliance to strategic, multi-layered planning.

- Evaluate the efficiency of corporate structures and Family Investment Companies in preserving margins against rising Corporation Tax and income tax bands.

- Master property portfolio tax optimisation techniques to bypass the “phantom profit” trap caused by Section 24 finance cost restrictions.

- Secure your family’s future by integrating trust tax services into your succession planning to manage the inherent Inheritance Tax risks of residential assets.

- Learn how a structured Portfolio Health Check ensures your investments are prepared for the significant property tax rate adjustments arriving in April 2027.

Navigating the Property Tax Landscape in 2026

The 2026 fiscal year marks a definitive turning point for UK property investors. Genuine property portfolio tax optimisation is no longer a seasonal exercise in compliance; it’s a proactive, multi-layered financial strategy designed to protect capital in an increasingly hostile environment. HMRC has structured the UK Property Tax Landscape to reward professionalised business structures while placing significant pressure on individual ownership. To preserve your yields, you must move beyond simple bookkeeping and embrace a holistic approach that aligns your corporate structure with your long-term wealth objectives.

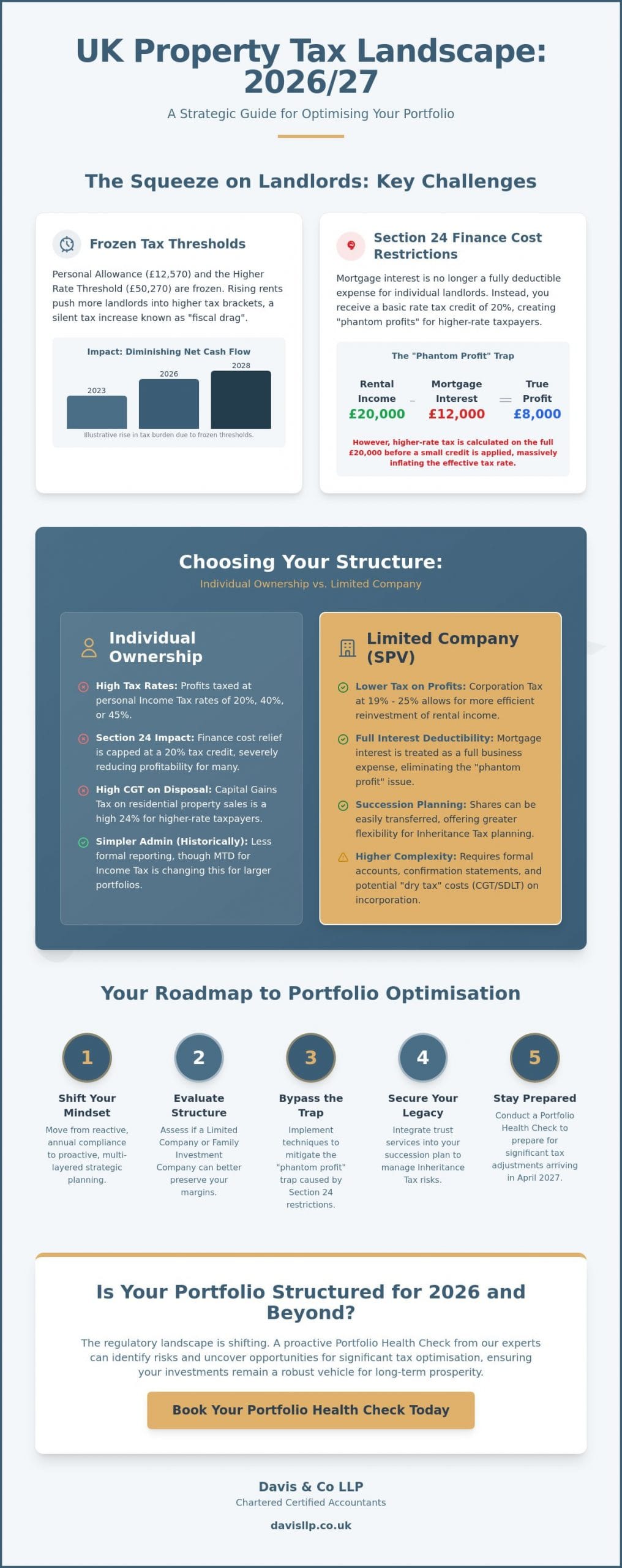

For the 2026/27 tax year, income tax rates on property remain at 20 percent for basic rate taxpayers, 40 percent for higher rate taxpayers, and 45 percent for the additional rate. However, the true challenge lies in fiscal drag. With the personal allowance frozen at £12,570 and the higher rate threshold at £50,270 until 2031/32, rising rents are pulling more landlords into higher tax brackets. This silent tax increase diminishes your net cash flow even if your gross margins remain stable. We believe that understanding these mechanics is the first step toward reclaiming your portfolio’s profitability.

The Shift from Passive Landlord to Property Business

The era of the “casual landlord” has effectively ended. HMRC now favours active, business-like operations over passive investment. From April 2026, Making Tax Digital (MTD) for Income Tax is mandatory for landlords with property income exceeding £50,000. This requires quarterly digital updates, making robust property accounting an operational necessity rather than an administrative choice. Transitioning to a professionalised model ensures you meet these reporting requirements while providing the granular data needed for sophisticated tax planning.

Current Challenges: Rates, Reliefs, and Regulations

Investors must also contend with the first full year following the 2025 abolition of the Furnished Holiday Let (FHL) regime. FHLs are now taxed as standard buy-to-lets, meaning mortgage interest relief is limited to a 20 percent tax credit. When combined with 2026 interest rates, many individual landlords find themselves at a tipping point. If your finance costs are high, your effective tax rate can easily exceed 50 percent of your actual profit. We often find that once a portfolio reaches a certain scale, the transition to a corporate wrapper or a Family Investment Company becomes the only viable path to maintaining structural efficiency.

Structural Foundations: Limited Companies vs. Family Investment Companies

Selecting the appropriate legal vehicle is the cornerstone of property portfolio tax optimisation. In the 2026 financial landscape, the disparity between personal income tax rates and Corporation Tax remains a primary driver for restructuring. For the financial year starting April 1, 2026, companies with profits of £50,000 or less benefit from the 19 percent small profits rate. Conversely, those with profits exceeding £250,000 are subject to the 25 percent main rate, with marginal relief providing a tapered increase for those situated in between. This corporate framework often allows for more efficient reinvestment of rental yields compared to personal ownership, where higher rate taxpayers face immediate 40 percent or 45 percent charges on their income.

However, transferring an existing portfolio into a company is not without friction. Investors must carefully weigh the long term benefits against immediate “dry tax” liabilities. Moving properties from personal names into a corporate wrapper typically triggers Capital Gains Tax (CGT) at 18 percent or 24 percent, alongside Stamp Duty Land Tax (SDLT) based on the market value. High value portfolios must also account for shifting regulatory sentiment. Recent analysis of the UK ‘Mansion Tax’ suggests that properties valued over £2 million may face additional council tax surcharges by 2028. Such developments make structural foresight essential for maintaining portfolio viability.

The Limited Company Model in 2026

The primary advantage of the limited company model remains the full deductibility of mortgage interest as a business expense. This bypasses the restrictive 20 percent tax credit faced by individual landlords. We focus on helping clients extract profits through a balanced mix of salaries, dividends, and employer pension contributions to maximise personal allowances. Furthermore, the ability to use inter-company loans allows for the seamless movement of capital between different Special Purpose Vehicles (SPVs), facilitating portfolio expansion without personal tax leakage.

Family Investment Companies (FICs) for Wealth Preservation

For high value estates, a Family Investment Company (FIC) provides a sophisticated alternative to a standard SPV. By utilising different share classes, we can help you separate voting control from economic value. This allows you to retain management of the assets while gifting non-voting shares to the next generation. Given that the standard Inheritance Tax nil-rate band is frozen at £325,000 for 2026, FICs serve as a vital tool for shifting future capital growth out of your taxable estate. If you are evaluating the merits of these structures, our property accounting specialists can provide a detailed comparison tailored to your specific asset base.

International Dimensions for Non-Resident Landlords

Investors with cross border interests face a unique set of 2026 regulations. Non-resident landlords must report disposals of UK residential property and pay the relevant tax within 60 days of completion. Our expertise in international tax planning ensures that global investors remain compliant with Non-Resident Capital Gains Tax (NRCGT) rules while navigating the complexities of double taxation treaties. We provide the steady guidance necessary to manage these obligations without disrupting your broader investment strategy.

Mitigating the Impact of Section 24 and Finance Costs

The “phantom profit” trap remains one of the most significant hurdles for individual landlords in 2026. This phenomenon occurs when the restriction on mortgage interest relief pushes your taxable income higher than your actual cash surplus. Because individual landlords receive only a 20 percent tax credit on finance costs rather than a full deduction, many find themselves paying tax on income they never truly see. A central pillar of property portfolio tax optimisation involves addressing this structural imbalance to ensure your Cash Flow Management remains robust and sustainable.

For the 2026/27 tax year, the disparity between individual ownership and corporate structures is stark. While individuals struggle with the 20 percent credit, properties held within a limited company continue to benefit from full interest deductibility as a business expense. For those with existing personal portfolios, beneficial interest company transfers (BICT) represent a sophisticated middle ground. This strategy allows for the transfer of economic benefit to a corporate entity without the immediate necessity of legal title change, though it requires meticulous execution and lender consent to avoid breaching mortgage covenants.

Strategic Debt Management

Effective debt restructuring is essential to align your liabilities with your tax-efficient vehicles. We often advise clients on utilizing director loan accounts to offset initial investment costs. When you introduce personal capital into a company to fund acquisitions, you can subsequently withdraw profits tax-free as loan repayments rather than taking taxable dividends. Additionally, we look at the tax implications of refinancing. Extracting capital for further acquisitions must be balanced against the interest costs, ensuring that loans between related entities are structured to optimise the overall group tax position without falling foul of transfer pricing or anti-avoidance rules.

Maximising Allowable Expenses and Capital Allowances

Reducing the taxable pot requires a granular focus on often-overlooked revenue expenses. Beyond standard maintenance, professional fees and specific travel costs can be deducted if they’re incurred wholly and exclusively for the business. In 2026, we place particular emphasis on Capital Allowances for plant and machinery within communal areas of multi-unit blocks or HMOs. This includes items like fire alarm systems, lifts, and even high-end security installations. For standard buy-to-let properties, the “replacement of domestic items” relief provides a vital route to offset the cost of new furniture and appliances against rental income, provided the old items are no longer used in the business. Our role is to ensure every legitimate relief is claimed to protect your net yields.

Succession and Exit: Protecting Your Legacy from Inheritance Tax

Property is often described as a “toxic” asset within the context of Inheritance Tax (IHT). Unlike a traditional trading business, a residential property portfolio generally doesn’t qualify for Business Property Relief (BPR). This means that upon death, the entire value of the portfolio above your available nil-rate bands is typically subject to a 40 percent tax charge. For a high value estate in 2026, where the standard nil-rate band remains frozen at £325,000, this can necessitate the forced sale of assets just to meet the tax bill. Achieving effective property portfolio tax optimisation requires a shift in focus from mere income generation to robust legacy protection.

The use of discretionary trusts remains a cornerstone of sophisticated succession planning. By transferring assets into a trust, you can maintain a degree of control over the portfolio while effectively removing future capital growth from your personal estate. It’s important to remember the 7-year rule for Potentially Exempt Transfers (PETs). If you survive seven years after making a gift, the value of that gift falls outside your estate for IHT purposes. Corporate structures, such as the Family Investment Companies discussed earlier, further facilitate this by allowing the gradual transfer of non-voting shares to descendants without relinquishing management authority.

Inheritance Tax Mitigation Strategies

We often recommend a multi-faceted approach to protecting your wealth. Life insurance can play a critical role here, providing the necessary liquidity to cover potential IHT liabilities without liquidating the portfolio itself. Another effective mechanism involves “freezer shares.” By freezing the value of your current interest in a company and allowing future growth to accrue to a different share class held by your heirs, you effectively cap your own IHT exposure. For more bespoke legacy planning, we suggest you review our expert tax advice in the UK to ensure your strategy aligns with the latest 2026 regulations.

Capital Gains Tax (CGT) Optimisation on Exit

Exiting a property investment requires careful timing to manage Capital Gains Tax. For the 2026/27 tax year, CGT rates for residential property are 18 percent for basic rate taxpayers and 24 percent for higher rate taxpayers. You should aim to utilise the annual exempt amount, which currently stands at £3,000, across multiple family members where possible. If you’re considering moving a personally held business into a company, Incorporation Relief (Section 162) can be invaluable. It allows you to roll over the gain into shares, deferring the tax until those shares are eventually sold. If you require assistance with these complex transitions, our Trust Tax Services team can help you structure a secure and efficient exit.

Strategic Partnership: How Davis & Co LLP Optimises Your Portfolio

The complexities of the 2026 fiscal landscape demand more than just technical accuracy; they require a partnership built on foresight and discretion. At Davis & Co LLP, we position ourselves as strategic advisors who look beyond the immediate tax return to the broader horizon of your wealth. Achieving effective property portfolio tax optimisation is a continuous process of refinement, especially as we approach the significant tax rate adjustments scheduled for April 2027. We offer a bespoke “Portfolio Health Check” for 2026, designed to stress-test your current holdings against upcoming regulatory shifts and identify hidden inefficiencies in your debt or corporate structures.

Our approach combines deep technical knowledge in property accounting with a nuanced understanding of international tax planning. This dual expertise is particularly valuable for investors managing cross-border assets or those considering complex restructuring, such as the implementation of Family Investment Companies or discretionary trusts. We believe every client deserves a strategy as individual as their portfolio, delivered with the quiet excellence that has become our hallmark.

Why a Strategic Approach Matters

Integrating your personal tax objectives with your corporate portfolio performance is essential for long-term stability. When you seek to understand how to find a Chartered Accountant who truly understands the property sector, you’re looking for a partner who values reliability as much as technical skill. We provide a steady, measured hand in a volatile market, ensuring your succession plans and cash flow management are perfectly aligned. Our commitment to discretion means that your commercial and personal matters are handled with the highest level of professional gravitas, fostering a relationship built on trust and mutual success.

Taking the Next Step

The transition to a more optimised structure begins with a thorough onboarding process. We take the time to understand the history of your acquisitions and your future aspirations before proposing any structural changes. Our team coordinates seamlessly with your legal advisors to ensure that every transition, whether it involves beneficial interest transfers or the creation of new share classes, is executed with precision. We invite you to a confidential consultation to explore how we can protect your yields and preserve your legacy. A strategic review today is the most effective way to ensure your portfolio remains resilient throughout 2026 and beyond.

Securing Your Legacy in a Shifting Fiscal Environment

The 2026 tax landscape requires more than just compliance; it demands a fundamental shift in how we view property as a business asset. By moving beyond passive ownership and embracing sophisticated structures like Family Investment Companies, you can effectively counteract the erosion caused by Section 24 and fiscal drag. Protecting your yields today ensures that the wealth you’ve built isn’t compromised by the significant tax rate increases arriving in April 2027. True property portfolio tax optimisation is about aligning your current cash flow needs with a secure, multi-generational succession plan that respects the new caps on business property relief.

As Chartered Certified Accountants founded in 1901, we bring over a century of deep-seated expertise to every client engagement. Our specialists in international and property tax offer a composed, expert partnership approach that prioritises your long-term security and discretion. We’re here to help you navigate these complexities with a steady hand and a clear vision for the future. Secure your portfolio’s future with a strategic tax review from Davis & Co LLP. We look forward to helping you build a more resilient and tax-efficient foundation for your investments.

Frequently Asked Questions

Is it still worth setting up a Limited Company for property in 2026?

Yes, for many investors, the corporate wrapper remains the most efficient vehicle for reinvesting rental income. With the small profits rate at 19 percent for gains under £50,000, companies allow you to retain more capital for portfolio growth compared to the 40 percent or 45 percent personal tax brackets. The ability to deduct mortgage interest in full is often the deciding factor for higher-rate taxpayers.

How does Section 24 affect higher-rate taxpayers differently this year?

Section 24 continues to penalise individual landlords by taxing gross rental income rather than net profit. As a higher-rate taxpayer, you only receive a 20 percent tax credit on your finance costs, which can effectively double your tax liability in some scenarios. This makes property portfolio tax optimisation essential to prevent your tax bill from exceeding your actual cash surplus.

Can I move my existing property portfolio into a company without paying SDLT?

Generally, transferring properties into a limited company is treated as a market value disposal, which triggers both Stamp Duty Land Tax and Capital Gains Tax. While certain partnership reliefs may apply in specific circumstances, most investors will face these “dry tax” costs. We recommend a thorough cost-benefit analysis to ensure the long-term structural savings outweigh these initial transition expenses.

What are the main tax benefits of a Family Investment Company (FIC)?

A FIC provides exceptional flexibility for wealth preservation by allowing you to separate management control from economic ownership. By issuing different share classes, you can gift the right to future capital growth to your children while retaining voting rights. This structure also benefits from the corporate tax regime, making it an ideal vehicle for high-value portfolios.

How can I reduce Inheritance Tax on my rental properties?

Since residential property doesn’t qualify for Business Property Relief, you must use proactive gifting strategies or trust tax services to mitigate a 40 percent IHT charge. Utilising the seven-year rule for potentially exempt transfers or capping your estate value through “freezer shares” are effective methods. We also look at using life insurance to provide the necessary liquidity for your heirs.

What expenses can I legally claim to reduce my property tax bill in 2026?

You can claim for revenue-based costs such as property accounting fees, insurance, and essential maintenance. In 2026, we also focus on capital allowances for plant and machinery in communal areas and the replacement of domestic items relief for furnishings. Accurate digital record-keeping is now mandatory under Making Tax Digital for those with property income over £50,000.

Do non-resident landlords face different tax optimisation rules?

Non-resident landlords are subject to specific Non-Resident Capital Gains Tax (NRCGT) rules and must report disposals within 60 days of completion. Strategic planning for international investors involves navigating double taxation treaties to ensure income isn’t taxed twice. We provide specialised guidance to ensure global holdings are structured to respect both UK and local tax jurisdictions.

How often should I review my property portfolio tax structure?

We suggest a formal review of your holdings at least annually to account for legislative shifts and changes in your personal circumstances. With significant property tax rate increases scheduled for April 2027, a strategic review in 2026 is particularly vital. Regular assessments ensure your structure continues to protect your yields and remains compliant with the latest HMRC requirements.