The fiscal landscape for the 2026 tax year won’t be defined by the headlines you read today, but by the subtle statutory shifts tucked within the budget 2025 announcements. While the initial media reaction focused on immediate levies, the true commercial impact lies in the structural changes to employer National Insurance contributions and the tapering of specific relief schemes. Many business owners feel a justified sense of trepidation as they face a projected 1.2% rise in operational overheads due to these adjustments. We understand that the volume of conflicting reports can make it difficult to identify which legislative updates require your immediate attention and which are merely noise.

You’re likely concerned about how these fiscal measures will affect your practice’s bottom line or your personal international tax standing. We believe that clarity is the most effective hedge against economic volatility. This analysis provides a bespoke roadmap for achieving tax efficiency in 2026, offering a precise breakdown of sector-specific impacts for professionals such as dental practice owners. We’ll examine the technical nuances of the Autumn Budget 2025 to ensure your financial strategy remains both compliant and commercially resilient. We’ll conclude with a clear set of actionable steps to maintain HMRC compliance while protecting your long-term capital.

Key Takeaways

- Understand the core objectives of the budget 2025 and how these revenue-raising measures will dictate your financial trajectory for the 2026 implementation phase.

- Assess the impact of revised National Insurance contributions and Capital Gains Tax on your corporate structure to maintain fiscal resilience.

- Explore tailored strategies for specialist sectors, focusing on the unique challenges facing dental practitioners and non-domiciled residents.

- Learn how to conduct a rigorous tax health check to optimise remuneration packages through a sophisticated balance of salary and dividends.

- Recognise the value of a bespoke, partnership-led approach to Audit and Assurance in navigating a volatile and evolving regulatory environment.

The 2025 Budget in Context: A New Fiscal Landscape for 2026

The fiscal environment for UK enterprises is undergoing its most significant structural shift in a generation. The budget 2025 marks a departure from temporary relief measures toward a sustained period of revenue consolidation. We’ve observed that the Treasury’s primary objective is to address the perceived “fiscal gap” while attempting to stimulate long-term growth through public investment. This transition requires a sophisticated understanding of how immediate policy announcements translate into future liabilities. The core objectives of the budget 2025 focus on “fixing the foundations,” a phrase used by the Chancellor to justify the largest tax increase in decades.

Economic conditions remain delicate. Inflation is projected to settle near the 2.0% target by late 2025, yet GDP growth remains modest, with the Office for Budget Responsibility forecasting a 1.1% expansion for the 2024/25 period. This 2025 United Kingdom Budget overview clarifies how these forecasts underpin the government’s tax strategy. Relying on a “wait and see” approach is often a precursor to avoidable capital loss. Professional tax planning demands a forward-looking perspective that anticipates the 2026 implementation phase well before the new tax year begins. Passive observation often leads to reactive decision-making, which is rarely optimal in a legal or tax context. A proactive stance allows for the orderly revaluation of assets and the potential acceleration of transactions that may be less favourable under the 2026 regime.

Key Revenue-Raising Measures at a Glance

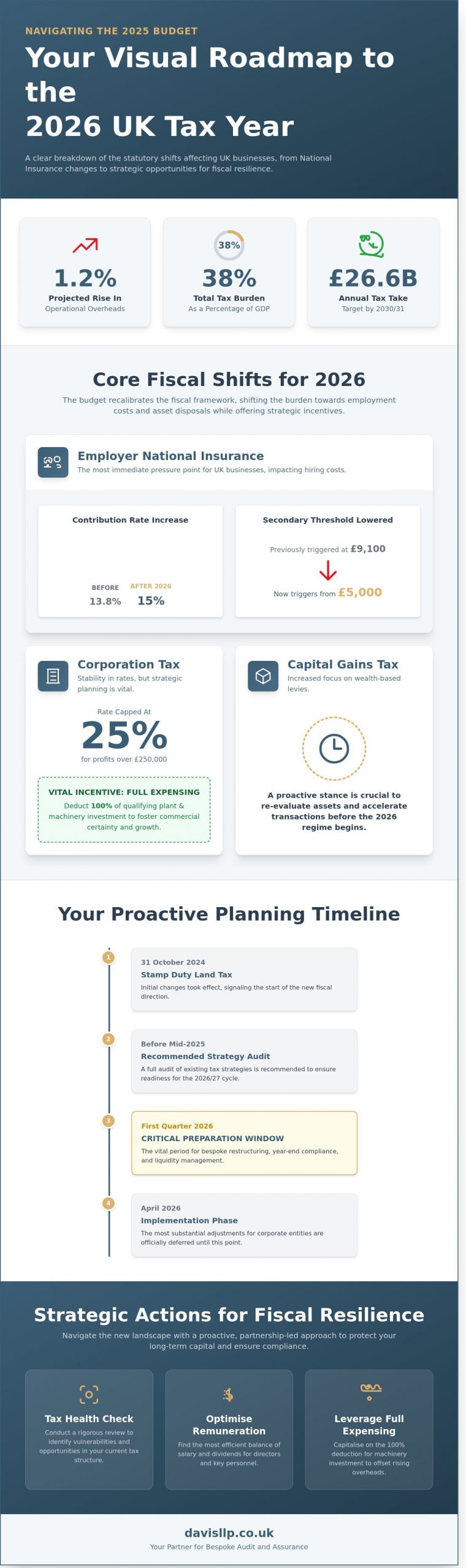

The government aims to secure a £26.6bn annual tax take by the 2030/31 fiscal year. This strategy elevates the total tax burden to 38% of GDP, the highest level since the post-war era. This shift places a considerable weight on the private sector, specifically through adjustments to Employer National Insurance and capital gains. The City’s reaction was one of cautious appraisal; however, 65% of small business owners expressed concerns regarding the impact on hiring costs and long-term investment capacity. We’ve noted that the focus has moved from individual income taxes to corporate and wealth-based levies, necessitating a review of all commercial holding structures to ensure they remain efficient.

The Timeline for Implementation

While some changes to Stamp Duty Land Tax took effect on 31 October 2024, the most substantial adjustments for corporate entities are deferred until April 2026. This delay offers a vital window for bespoke restructuring. Early preparation in the first quarter of 2026 is critical for year-end compliance and liquidity management. The government has set a specific fiscal headroom target of £21.7bn for the 2029/30 period to ensure long-term stability. Understanding this timeline allows us to align your commercial objectives with the new statutory realities. We recommend a full audit of existing tax strategies before the mid-point of 2025 to ensure readiness for the 2026/27 cycle, as waiting for the final deadline often restricts the availability of pragmatic solutions.

Core Tax Changes: Corporation Tax, NI, and Capital Gains

The budget 2025 introduces a recalibrated fiscal framework that demands careful scrutiny from directors and high-net-worth individuals alike. While the headline Corporation Tax rate remains capped at 25% for companies with profits over £250,000, the broader tax burden has shifted significantly toward employment costs and asset disposals. The government’s decision to maintain Full Expensing allows companies to deduct 100% of qualifying plant and machinery investment, providing a vital lever for capital-intensive sectors. Detailed provisions within the Official 2025 Tax Legislation confirm that this stability aims to foster long-term commercial certainty despite rising overheads.

Employer National Insurance (NI) contributions represent the most immediate pressure point for UK businesses. The rate has increased from 13.8% to 15%, while the secondary threshold, the point at which employers start paying NI on an employee’s salary, has been lowered from £9,100 to £5,000. For a firm employing 25 people on average salaries, this change equates to an additional £15,000 in annual payroll liabilities. We recommend a granular review of staff structures to manage these rising costs without compromising service delivery.

Capital Gains Tax (CGT) has also seen a structural shift. The lower rate has risen from 10% to 18%, and the higher rate from 20% to 24%, aligning residential property rates with other asset classes. These adjustments fundamentally alter the exit strategy for business owners and investors. Beyond corporate taxes, the government has addressed social spending by retaining the “two-child limit” on certain benefits. According to data from the Lords Library, this policy affects approximately 1.6 million children, while simultaneous welfare reforms aim to reduce the disability benefits bill by £3 billion by 2029 through stricter work capability assessments.

Business Tax and Employer Obligations

The reduction in the NI threshold creates a sharp decline in SME profitability, particularly in labour-intensive industries like hospitality or professional services. It’s essential to utilise monthly management accounts to forecast the precise impact of these employment costs on your net margins. Strategic use of the merged R&D tax credit scheme remains a viable route to offset these pressures. Companies can still claim a 20% credit for qualifying innovation, which serves as a critical buffer for firms investing in proprietary technology. A review of your current corporate structure can help identify where these new costs might be mitigated.

Personal Wealth and Capital Gains

For private clients, the rise in CGT rates necessitates a more sophisticated approach to asset disposal. Planning for the sale of a business or a secondary property now requires a longer lead time to ensure all available reliefs, such as Business Asset Disposal Relief, are fully utilised before they’re further restricted. The interaction between UK disposals and International Tax Planning is increasingly complex, especially for non-domiciled individuals transitioning to the new residence-based system. We’ve identified a narrow window of opportunity for tax-efficient gifting and trust settlements before the anticipated 2026 adjustments to Inheritance Tax thresholds. Effective wealth preservation now depends on proactive, rather than reactive, legal counsel.

Specialist Sector Impact: Dental Practices and International Clients

The November 2025 UK Budget introduces a series of nuanced adjustments that reach far beyond broad corporate tax rates. For specialised sectors, the fiscal landscape has shifted in ways that require immediate strategic attention. We see a clear intent to balance domestic infrastructure funding with a revised approach to high-net-worth migration and international capital flows. These measures don’t just affect the bottom line; they alter the long-term operational framework for professional practices and global family offices alike. Our role is to ensure these transitions are managed with the precision they deserve.

The Dental Professional’s Perspective

High-street dental practices face a specific set of challenges following the budget 2025 announcements. The government’s decision to adjust business rate multipliers for retail and leisure properties directly impacts clinical spaces that occupy prime commercial locations. For practices with a rateable value below £51,000, the frozen small business multiplier provides some relief, yet those exceeding this threshold must prepare for an inflationary rise of 1.7% or more. This creates a pressure point for cash flow management, particularly when aligned with the new 10-year efficiency projections mandated for healthcare providers. The requirement to demonstrate cost-efficiency while maintaining clinical standards is now a statutory expectation rather than a mere recommendation.

We believe that a proactive approach to capital allowances is now essential. Engaging a Dental tax specialist is the most effective way to manage equipment depreciation under the current rules. With the full expensing regime remaining a permanent fixture, practices should look to synchronise their technology upgrades with these tax windows. We’ve helped clients identify qualifying expenditures on high-value imaging and surgical equipment that can be 100% deducted from taxable profits in the year of purchase. This isn’t just about tax saving; it’s about maintaining a modern, competitive clinical environment through bespoke financial planning.

International and Cross-Border Considerations

The budget 2025 signals a definitive shift in how the UK treats international residents and mobile capital. The formal abolition of the non-domiciled tax status and its replacement with a residence-based system represents a significant change for international family offices. We’re currently advising clients on the four-year transition period, which offers a temporary window for repatriating foreign income at a reduced tax rate. The increase in Air Passenger Duty for private jets, specifically a 50% rise for the largest aircraft, serves as a clear policy signal. It suggests that high-net-worth individuals are expected to contribute a larger share to the national transition towards sustainable infrastructure, potentially influencing the UK’s appeal as a primary hub for global elites.

On the corporate side, the Digital Services Tax reform continues to impact tech-heavy international firms. The budget maintains the 2% levy on revenues derived from UK users, despite ongoing international discussions regarding Pillar One of the OECD agreement. For clients with global investment portfolios, the updated Monetary Policy Remit emphasises price stability, which may influence the pound’s strength against the Euro and Dollar. We suggest that international businesses review their implicit liabilities and customs treatment protocols to ensure they remain compliant with the updated HMRC guidelines for 2026. This level of foresight ensures our clients remain secure in a shifting global market, providing the stability required for long-term growth.

Strategic Planning: Organising Your Finances for 2026

The transition into the 2026 financial year requires a disciplined appraisal of the structural shifts introduced by the budget 2025. It’s no longer sufficient to rely on historical accounting patterns. The fiscal landscape has shifted, and we advise our clients to initiate a comprehensive tax health check to ensure their commercial operations remain resilient. This process involves a forensic review of every tax touchpoint, from employer National Insurance contributions to the long-term treatment of capital assets. By identifying potential leakages early, businesses can adjust their pricing models and capital expenditure plans before the 2026 deadlines arrive.

Updating your cash flow forecasts for the 2026 cycle is a priority. These projections must now incorporate the specific increases in levies and duties announced on 30 October 2024. For instance, the adjustments to the National Living Wage and the potential tapering of business rate reliefs require precise modelling. We’ve observed that firms failing to integrate these “stealth” costs often face liquidity constraints during the second quarter of the following year. A robust forecast acts as a defensive shield, allowing for the strategic reallocation of resources where they’re most needed.

Remuneration and Profit Extraction

The traditional preference for a low-salary, high-dividend model is under renewed pressure. With the narrowing gap between dividend tax rates and income tax, the efficiency of this model for 2026 depends heavily on the specific profit levels of the business. We’re currently helping directors evaluate whether a higher pension contribution or a different mix of benefits-in-kind offers a more tax-efficient route. Our Personal Tax Services play a vital role here, particularly in managing the delicate balance of director loan accounts and annual draws to prevent unnecessary tax charges.

- The National Living Wage increase to £12.21 per hour in April 2025 necessitates a total review of payroll overheads.

- Dividend allowance freezes mean that even modest profit extractions may now trigger higher tax liabilities.

- Salary sacrifice schemes for electric vehicles or cyclical equipment remain a viable way to reduce National Insurance burdens.

Long-term Wealth Preservation

Estate planning has become increasingly vital as the budget 2025 measures begin to settle. The “implicit liabilities” for family-owned businesses have grown, particularly where property assets are involved. We focus on mitigating Inheritance Tax (IHT) exposure through the use of structured gifting and bespoke trust tax services. These vehicles allow for the controlled transfer of wealth to the next generation while maintaining the integrity of the business’s capital base. The 2025 fiscal rule performance showed a £9.2 billion headroom against the debt-to-GDP target, a figure that remains susceptible to shifts in global interest rates and underscores the need for private fiscal stability.

Pension contributions remain one of the few remaining “pure” tax breaks for business owners. Maximising these contributions before the end of the 2025/26 tax year can significantly reduce a company’s Corporation Tax bill while simultaneously building a protected pot for retirement. We recommend a joint review of your corporate and personal balance sheets to ensure these contributions align with your broader wealth preservation objectives. Our approach is always bespoke, ensuring that the legal structures we implement today don’t become the constraints of tomorrow.

We invite you to consult our private client team to review your current estate structure and ensure it remains compliant with the latest statutory requirements.

The Davis & Co Approach: Bespoke Solutions for a Volatile Economy

Reacting to the budget 2025 requires more than a cursory glance at the Chancellor’s headlines; it demands a forensic understanding of how shifting fiscal policy intersects with your specific commercial objectives. At Davis & Co LLP, we provide a steady hand for businesses facing the complexities of the Finance Bill 2025/26. We don’t believe in generic summaries that offer little more than a restatement of public data. Instead, our focus remains on “quiet excellence,” a philosophy where we prioritise intellectual rigour over aggressive marketing to deliver clarity in uncertain times.

Our partnership-led approach to Audit and Assurance ensures that your financial reporting isn’t merely a statutory obligation, but a foundation for future growth. We recognise that the changes introduced in the budget 2025, particularly regarding employer National Insurance contributions and capital gains, require a nuanced response. By integrating our advisory services with your core compliance requirements, we help you maintain a resilient balance sheet while preparing for the next fiscal cycle.

Why Understated Confidence Matters

Since 1901, Davis & Co LLP has supported the business communities of London and Harpenden through countless economic shifts. This century of experience has taught us that the most effective solutions are often the most considered. We avoid the loud, reactionary commentary common in the financial sector, opting for a composed partnership that makes our clients feel secure. Our team understands the delicate balance required to manage both commercial interests and private client sectors, ensuring that your business decisions don’t inadvertently compromise your personal long-term wealth.

Our professionals provide a high-calibre service that is both traditional in its values and contemporary in its application. We offer a level of discretion and precision that is essential for legal and financial practices dealing with sensitive commercial matters. This intellectual polish is what defines our firm; we don’t need to shout because our reputation for delivering bespoke, pragmatic results speaks for itself. Whether you’re a multi-generational family business or a growing corporate entity, our strategic advice is always tailored to your specific reality.

Next Steps: Your 2026 Roadmap

Translating the complexities of the Finance Bill 2025/26 into an actionable plan is a process that requires immediate attention. We don’t wait for the new tax year to begin; our proactive planning starts now. A Davis & Co LLP bespoke tax review involves a comprehensive analysis of your current structure against the new statutory requirements. This process includes:

- Structure Optimisation: Assessing if your current business vehicle remains the most tax-efficient following the latest corporate tax updates.

- Remuneration Planning: Reviewing director salaries and dividends to mitigate the impact of increased National Insurance thresholds.

- Succession and Exit Strategy: Aligning your long-term goals with the revised Capital Gains Tax and Business Property Relief rules.

The 2026 tax position will be significantly different for 85% of our clients compared to previous years. Securing your financial stability requires a partner who looks beyond the immediate horizon. We invite you to book a strategic consultation to review your roadmap for the coming eighteen months. By acting now, you ensure that your business remains a dependable constant in a volatile economy. Let us provide the professional gravitas and expert guidance your legacy deserves.

Securing Your Financial Position for 2026

The budget 2025 introduces a pivotal shift in the UK’s fiscal landscape, demanding a sophisticated response to changes in National Insurance and Capital Gains Tax. Success in the 2026 financial year won’t depend on reactive measures but on the deliberate, strategic planning we’ve championed since 1901. For our specialist dental and international clients, these adjustments require a nuanced understanding of statutory requirements to maintain commercial momentum. We’ve found that early intervention before the April 2026 deadline remains the most reliable method for mitigating tax liabilities and protecting personal wealth.

At Davis & Co LLP, we provide the intellectual rigour and discretion necessary to navigate these volatile periods. Our teams in London and Harpenden specialise in crafting bespoke solutions that align with your specific commercial objectives. It’s time to move beyond general advice and implement a plan that reflects your unique circumstances. We invite you to contact Davis & Co LLP for a bespoke 2026 tax strategy consultation. Let’s work together to ensure your legacy and business interests remain secure through 2026 and beyond.

Frequently Asked Questions

What are the main tax-raising measures in the 2025 Budget?

The primary tax-raising measures in the budget 2025 focus on Employer National Insurance, Capital Gains Tax, and the abolition of non-domiciled status. These specific adjustments aim to raise approximately £40 billion per year for the Treasury. We’ve observed that the 1.2 percentage point rise in National Insurance represents the largest single revenue generator. It’s a significant shift that requires careful commercial planning for the upcoming fiscal year.

How does the 2025 Budget affect Employer National Insurance contributions?

Employer National Insurance contributions will increase to 15% from 6 April 2025. Simultaneously, the secondary threshold at which businesses start paying these contributions will decrease from £9,100 to £5,000 per annum. This dual adjustment creates a higher fiscal obligation for companies of all sizes. We recommend reviewing payroll structures early to accommodate these increased statutory costs. It’s vital to understand how these changes affect your specific headcount and annual overheads.

Are there any changes to Capital Gains Tax in the 2025 Budget for 2026?

Capital Gains Tax rates for most assets have risen to 18% for the lower rate and 24% for the higher rate. Looking toward 2026, Business Asset Disposal Relief will increase from its current 10% level to 14% in April 2025 and eventually 18% by April 2026. These phased adjustments require a strategic approach to asset disposal and long-term liquidity planning. We’re helping clients navigate these thresholds to protect their commercial interests and personal wealth.

How will the 2025 Budget impact dental practices specifically?

Dental practices face a particular challenge due to the 6.7% increase in the National Living Wage to £12.21 per hour. Combined with the lower £5,000 threshold for National Insurance, a practice with ten employees could see annual costs rise by over £8,000. While the 40% relief on business rates provides some cushion, it’s capped at £110,000 per business across all sites. This makes bespoke financial modelling essential for clinical directors and practice owners.

What does the 2025 Budget mean for international residents and non-doms?

The budget 2025 confirms the abolition of the non-domiciled tax regime effective from 6 April 2025. It’ll be replaced by a residence-based system where new arrivals pay no UK tax on foreign income for their first four years. We’re currently advising clients on the transitional arrangements; these include the temporary repatriation facility which allows for lower tax rates on remitted funds. It’s a fundamental change for our international private clients and their global assets.

When do the 2025 Budget changes actually take effect?

Most business-related changes take effect on 6 April 2025, though Capital Gains Tax rate increases applied immediately from 30 October 2024. The adjustments to the National Living Wage and National Insurance thresholds are aligned with the start of the new tax year. We suggest clients update their accounting software and compliance calendars well before these spring deadlines. Early preparation ensures you don’t face unexpected administrative or financial hurdles during the transition period.

Is there any relief for small businesses in the new fiscal plan?

Small businesses benefit from an increase in the Employment Allowance, which rises from £5,000 to £10,500. This change means approximately 865,000 employers won’t pay any National Insurance at all next year. It’s a pragmatic measure designed to protect the smallest firms from the broader rate increases. We can help you determine if your entity qualifies for this relief and how it offsets other tax obligations within your 2025 financial plan.

How should I adjust my 2026 financial forecast based on this Budget?

To adjust your 2026 financial forecast, you should model a 15% rate for Employer National Insurance and a 6.7% rise in baseline staffing costs. Incorporate the £12.21 per hour minimum wage 2025 rate and the phased 18% Business Asset Disposal Relief rate if you’re planning an exit. These concrete figures allow for a more precise commercial outlook. We’re available to provide a bespoke analysis of how these variables impact your long-term corporate strategy.