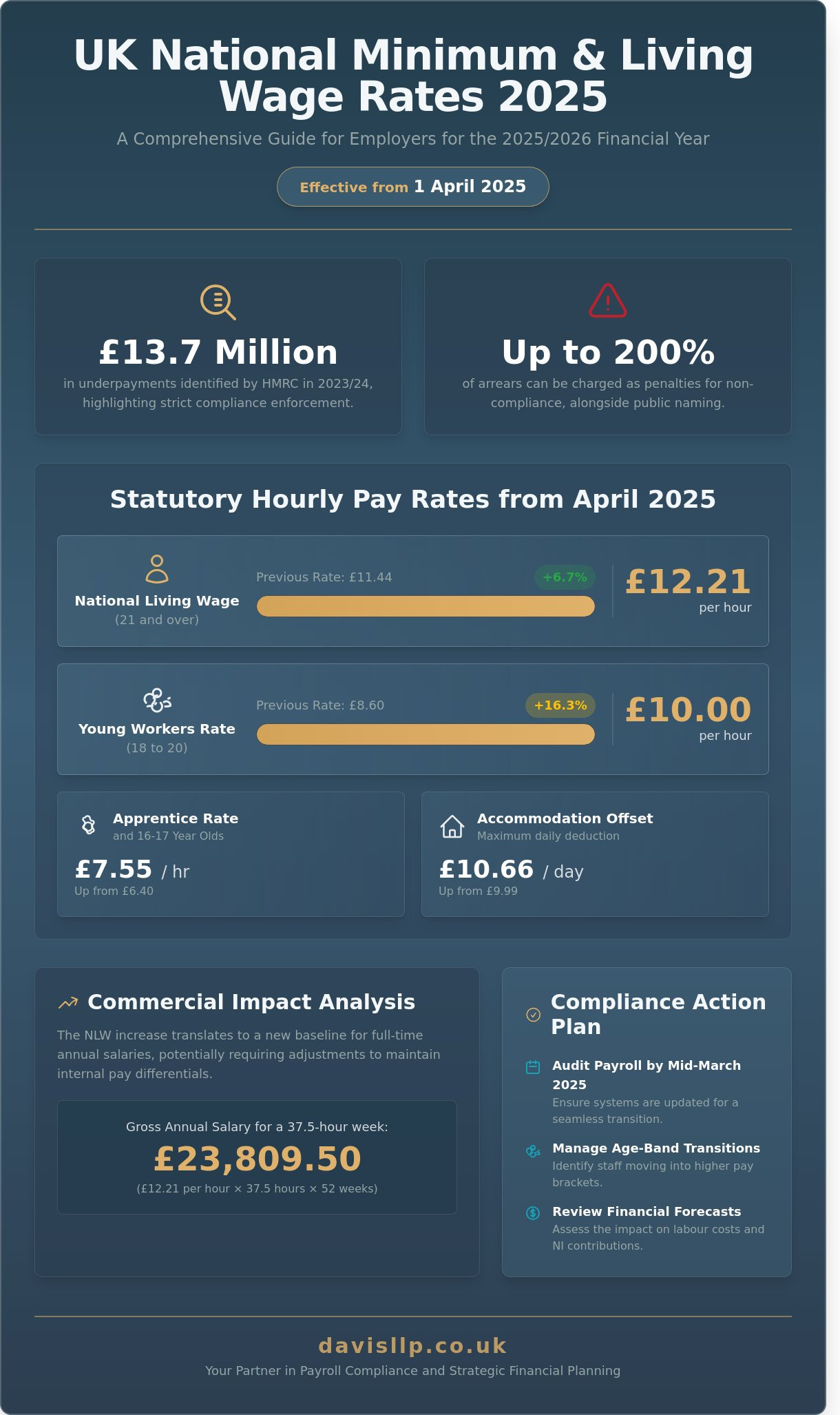

In the 2023/24 financial year, HMRC identified more than £13.7 million in National Minimum Wage underpayments, a statistic that highlights the uncompromising nature of UK payroll compliance. As the minimum wage 2025 thresholds take effect on 1 April, the administrative burden on your business is set to increase. You’re likely concerned about how these rising labour costs will impact your 2025/26 forecasts. It’s a legitimate concern, especially when the cost of a single oversight can include penalties of up to 200% of the arrears.

We’ve created this guide to serve as your definitive reference for the statutory pay rates and their wider implications for the 2026 financial year. It provides a clear framework for adjusting your payroll structures and managing age-band transitions with confidence. We’ll outline the exact figures you need to implement, the specific nuances of the National Living Wage for those aged 21 and over, and the proactive steps required to ensure your firm remains beyond the reach of HMRC’s naming-and-shaming lists. This structured approach ensures your commercial objectives remain aligned with your legal obligations.

Key Takeaways

- Understand the specific statutory adjustments for the minimum wage 2025 and the ongoing transition toward a unified adult rate for all workers aged 18 and over.

- Assess the cumulative impact of these wage increases on commercial profitability, including the critical interaction with employer National Insurance contributions for the 2026 financial year.

- Recognise the common triggers for HMRC payroll investigations to ensure full compliance and avoid the substantial financial penalties associated with statutory underpayment.

- Discover how a bespoke approach to payroll and tax efficiency can provide your organisation with the strategic stability required in an evolving regulatory environment.

Understanding the National Minimum Wage and Living Wage Rates for 2025

The landscape of UK employment law is set for a pivotal transition on 1 April 2025. We recognise that for our commercial clients, maintaining absolute compliance isn’t merely a regulatory hurdle but a cornerstone of ethical governance. The minimum wage 2025 adjustments represent more than a routine fiscal update; they reflect a concerted effort by the Low Pay Commission to align statutory pay with the actual cost of living while narrowing the gap between age brackets.

Since the inception of the National Minimum Wage Act 1998, the framework for base-level compensation has evolved to protect the most vulnerable participants in the workforce. Every UK employer, regardless of their corporate structure or headcount, holds a non-negotiable legal obligation to honour these revised rates. Failure to do so invites not only significant financial penalties from HMRC but also irreparable damage to a firm’s professional reputation.

The Distinction Between NLW and NMW

The National Living Wage (NLW) serves as the statutory floor for workers aged 21 and over. This age threshold was lowered from 23 to 21 in April 2024, a change that remains a critical factor for payroll planning in 2025. It’s vital to distinguish these mandatory figures from the “Real Living Wage,” which is a voluntary rate set by the Living Wage Foundation. Our team often advises that while statutory rates are the legal minimum, bespoke remuneration strategies often involve looking beyond these figures to retain high-calibre talent in a competitive market.

Key Changes Effective from April 2025

From 1 April 2025, the NLW will rise by 6.7 per cent to £12.21 per hour. This increase follows the government’s remit to ensure the minimum wage 2025 reaches two-thirds of median earnings. For those aged 18 to 20, the rate increases significantly to £10.00 per hour, representing a 16.3 per cent rise as the Treasury moves toward a unified adult rate. We recommend that payroll systems are audited by mid-March 2025 to ensure a seamless transition. The specific statutory rates are as follows:

- National Living Wage (21+): £12.21 (up from £11.44)

- 18-20 Year Old Rate: £10.00 (up from £8.60)

- 16-17 and Apprentice Rate: £7.55 (up from £6.40)

- Accommodation Offset: £10.66 (up from £9.99)

Our experience suggests that early preparation is the most effective way to manage the commercial impact of these increases. By identifying which staff members will cross age thresholds or require immediate adjustments, businesses can maintain the precision and intellectual rigour required for long-term financial stability.

A Detailed Breakdown of Hourly Rates by Age Category

The minimum wage 2025 framework represents a decisive shift in UK employment law, reflecting a central policy objective to align pay across different age groups. From 1 April 2025, the National Living Wage (NLW) will increase to £12.21 per hour. This 6.7% rise from the previous year’s rate is designed to maintain the momentum of the Low Pay Commission’s recommendations while addressing the rising cost of living for the UK workforce.

Employers must ensure these statutory adjustments are applied to all qualifying staff members, regardless of their contract type. Whether an individual is on a full-time, part-time, or casual agreement, the legal requirement remains absolute. We’ve observed that failure to update payroll systems in time for the April deadline often leads to unintentional non-compliance, which can carry significant reputational and financial risks. You can verify the specific figures for each group using the official 2025 minimum wage rates to ensure your records are accurate.

The National Living Wage for Workers Aged 21 and Over

For workers aged 21 and over, the £12.21 rate sets a new baseline for annual earnings. For a standard 37.5-hour working week, this hourly rate translates to a gross annual salary of approximately £23,809.50. This increase requires a pragmatic review of internal pay scales, as the narrowing gap between the minimum wage 2025 and mid-level salaries may necessitate wider adjustments to maintain internal pay differentials. We recommend a strategic audit of your current payroll to identify any employees whose total compensation might fall below these new thresholds when factoring in bonuses or commission structures.

Rates for Younger Workers and Apprentices

Significant adjustments are being introduced for those under 21, as the government moves towards a standardised adult rate for everyone over 18. The 18-20 age bracket will see a substantial 16.3% increase, rising to £10.00 per hour. This is a deliberate step to reduce the pay gap between younger workers and their older counterparts. For workers under the age of 18, the rate will rise to £7.55 per hour, which is the same rate applied to apprentices.

- Apprentice Rate: The £7.55 rate applies to apprentices aged under 19, or those aged 19 and over who are in the first year of their apprenticeship.

- Transitioning: Once an apprentice completes their first year and is aged 19 or over, they must be moved to the full age-related minimum wage.

- Under-18s: Those below the school leaving age aren’t typically eligible for the National Minimum Wage, but once they reach 16, the statutory £7.55 rate applies.

When providing living quarters for staff, the accommodation offset limit for 2025 is set at £10.66 per day. This is the maximum amount an employer can deduct from an employee’s pay or take into account when calculating whether the minimum wage has been met. If your business provides housing as part of an employment package, our team can provide bespoke advisory services to ensure these deductions don’t inadvertently lead to a breach of statutory requirements.

The Commercial Impact: Managing Increased Payroll Costs in 2026

Preparing for the April 2026 fiscal year requires a granular understanding of how the minimum wage 2025 adjustments filter through the entire profit and loss account. We’ve observed that a simple increase in the hourly rate often masks a much larger spike in total employment costs. For every £1 increase in gross pay, employers must account for an additional 13.8% in Class 1 National Insurance contributions and a minimum 3% for pension auto-enrolment. According to the Low Pay Commission’s 2025 impact report, these secondary costs significantly tighten the margins of labour-intensive sectors like hospitality and retail.

Maintaining pay differentials is a delicate exercise that requires bespoke planning. If a junior staff member’s salary rises to meet the new statutory floor, senior staff often expect a proportional increase to reflect their additional responsibilities. Failing to address this leads to pay compression. This phenomenon can erode morale and hinder staff retention. We suggest that firms review their entire grading structure to ensure that the gap between entry-level roles and supervisory positions remains meaningful and motivating.

Strategic Cash Flow Management and Budgeting

Strategic budgeting for the minimum wage 2025 transition involves more than just adjusting payroll software. Companies shouldn’t wait until March 2026 to review their pricing models. We recommend a full audit of management accounts to identify exactly where margin erosion is occurring. Approximately 42% of small businesses in the UK report that they’ll need to increase prices to absorb these costs. Accurate cash flow forecasting allows a business to model the impact of the April 2026 adjustments well in advance. This foresight ensures that operational expenditure doesn’t outpace revenue growth. As wages rise and business owners accumulate greater cash reserves, it is equally important to be aware of the HMRC tax warning for 2026 regarding savings interest, as frozen thresholds mean more individuals may face unexpected tax charges on interest earned. Working with a proactive small business accountant who can integrate these rising wage costs into a broader financial strategy is essential for maintaining profitability through 2026.

Secondary Effects on Benefits and Overtime

The statutory increase ripples through every aspect of the remuneration package. Overtime premiums, typically calculated as time-and-a-half or double-time, will rise automatically alongside the base rate. Holiday pay calculations must also reflect these new statutory minimums. It’s a complex area where errors can lead to significant back-pay liabilities. We ensure our clients’ total reward strategies remain sustainable by balancing these mandatory increases with non-financial benefits. This approach helps maintain a competitive edge in the recruitment market without compromising the firm’s long-term financial stability. For employees whose adjusted net income approaches higher tax thresholds as wages rise, it is also worth reviewing the HMRC child benefit changes 2025 to understand how the High Income Child Benefit Charge may affect your workforce’s overall household finances.

- Review all employment contracts for overtime clauses linked to base pay.

- Update pension contribution forecasts to reflect the higher gross salary thresholds.

- Analyse the impact of increased holiday pay on seasonal staffing budgets.

Ensuring Statutory Compliance and Avoiding HMRC Penalties

HMRC’s enforcement strategy has shifted toward proactive data interrogation. During the 2023/24 financial year, the government identified over £13.7 million in arrears for more than 110,000 workers. Investigations are often triggered by worker grievances, yet a significant portion stems from HMRC’s targeted sector sweeps in hospitality and retail. If your business fails to meet the minimum wage 2025 standards, the financial burden is substantial. Penalties reach 200% of the total underpayment, with a ceiling of £20,000 per worker.

Beyond the immediate fiscal impact, the Department for Business and Trade maintains a public naming scheme. In February 2024, 524 employers were publicly identified, causing irreparable brand damage that often outweighs the initial fine. We advise conducting a bespoke internal payroll audit to scrutinise the last six years of pay data. This process identifies historical discrepancies before they escalate into formal litigation or an external investigation.

Common Pitfalls in Minimum Wage Calculations

Compliance errors often arise from technicalities rather than intent. Mandatory training sessions and “unpaid” trial shifts exceeding a few hours are frequently misclassified as non-working time. If a worker buys a specific uniform or safety equipment, and that cost isn’t reimbursed, it can drop their hourly rate below the legal floor. Similarly, misclassifying a staff member as a self-employed contractor to bypass the minimum wage 2025 requirements is a high-risk strategy that HMRC remains focused on dismantling. These oversights, while small individually, create significant cumulative liabilities.

Statutory Record-Keeping Requirements

The National Minimum Wage Act 1998 dictates that employers must retain sufficient records for six years. A “sufficient record” isn’t merely a summary of gross pay; it must evidence the actual hours worked by every individual. Digital payroll systems now play a vital role, but they’re only as reliable as the data entry protocols behind them. HMRC inspectors expect to see precise start and finish times, especially for workers near the NMW threshold. Failure to produce these records creates a legal presumption that the worker’s claim of underpayment is correct.

How Professional Advisory Supports Long-Term Business Stability

Davis & Co LLP acts as a steady hand for firms adjusting to the minimum wage 2025 adjustments. We don’t just process numbers; we align your payroll with long-term commercial objectives. The 6.7% increase for workers aged 21 and over, taking the rate to £12.21 per hour, requires more than a simple budget update. It demands a holistic review of your tax efficiency and international labour cost structures. Our role is to provide the professional gravitas and technical precision necessary to turn these statutory obligations into a foundation for “quiet excellence” and sustained growth.

Bespoke Payroll Services and Compliance Audits

Manual errors in payroll often lead to HMRC interventions that carry heavy reputational and financial costs. These audits can result in penalties reaching 200% of the total underpayment. Our specialists conduct rigorous compliance audits to identify risks before they crystallise into liabilities. This level of scrutiny is essential for dental practices and medical clinics, where complex associate agreements and varying staff grades often complicate statutory pay calculations. We provide a structured framework to ensure:

- Total accuracy in holiday pay and pension contribution calculations.

- Identification of “hidden” work time, such as mandatory training or uniform changes.

- Seamless transition to the new rates effective from 1 April 2025.

Strategic Growth and Management Accounting

Sustainable growth relies on management accounts that reveal the true impact of rising overheads. We advise on how VAT compliance and corporation tax liabilities shift when your wage bill expands. By integrating minimum wage 2025 costs into a broader business acceleration plan, we help you maintain profitability without compromising service quality. We don’t view wage compliance as an isolated task. Instead, it’s a component of a sophisticated financial strategy that accounts for local labour variations and international tax planning. Our approach focuses on pragmatic, bespoke solutions that respect your firm’s unique history and future goals. We invite you to enquire about our payroll and advisory services to secure your firm’s financial health and ensure total regulatory compliance in a volatile economic environment.

Navigating Future Payroll Obligations with Confidence

Adapting to the minimum wage 2025 uplift requires a precise understanding of statutory shifts and their impact on your commercial margins. It’s not just about meeting the new hourly thresholds; it’s about protecting your organisation from the significant financial and reputational risks associated with HMRC’s strict enforcement protocols. We’ve seen how even minor administrative errors can lead to substantial penalties and public naming.

As Chartered Certified Accountants since 1901, we provide the steady guidance needed to maintain equilibrium in a shifting regulatory landscape. We specialise in delivering bespoke management accounting and payroll solutions tailored to both UK and international clients. Our role is to act as your strategic partner, ensuring that every payroll cycle is accurate, compliant, and reflective of your broader business goals. By addressing these changes proactively, you’ll safeguard your firm’s stability and foster a culture of reliability.

Consult with our Chartered Accountants on payroll compliance to discuss how we can support your specific requirements. We’re ready to help you navigate these updates with the quiet excellence your business deserves.

Frequently Asked Questions

Is it legal to pay an apprentice less than the standard minimum wage?

Yes, it’s legal to pay apprentices a specific rate of £7.55 per hour if they’re under 19 or in the first year of their apprenticeship. Once an apprentice reaches age 19 and completes their initial year, they’re entitled to the full statutory rate for their age group. We advise clients to audit their payroll systems ahead of the April 2025 increases to ensure these distinctions are correctly applied to avoid penalties.

Can an employer deduct the cost of a uniform if it brings pay below the 2025 minimum wage?

No, you cannot deduct uniform costs if the deduction reduces a worker’s hourly pay below the minimum wage 2025 threshold. This rule applies even if the worker agrees to the deduction in their employment contract. If a uniform is mandatory, the costs must be managed so the net pay remains compliant with the £12.21 or relevant age-band rate. Failure to observe this often leads to HMRC investigations.

How much is the National Living Wage for over 21s in 2025?

The National Living Wage for workers aged 21 and over is £12.21 per hour as of 1 April 2025. This represents a 6.7% increase from the previous year’s rate of £11.44. Our legal team recommends that businesses review their commercial budgets immediately to account for these rising labour costs. Precise financial planning is essential to maintain your pragmatic objectives while ensuring full compliance with the new statutory requirements.

What happens if a worker turns 21 mid-way through a pay period?

The increased rate becomes mandatory at the start of the next pay reference period following the worker’s 21st birthday. If your payroll runs from the first of each month and an employee turns 21 on 15 May, the higher rate applies from 1 June. It’s a common administrative oversight that can lead to arrears. We provide bespoke advice to help HR departments automate these transitions within their existing management systems.

Does the National Minimum Wage apply to self-employed contractors?

The National Minimum Wage doesn’t apply to individuals who are genuinely self-employed and running their own business. However, the legal definition of a worker is broad and often includes contractors who provide personal service. If a person isn’t truly independent, they might be entitled to the minimum wage 2025 rates. We help organisations assess these relationships to mitigate the risk of costly misclassification claims in employment tribunals.

What records must I keep to prove I am paying the National Minimum Wage?

You’re legally required to keep sufficient records to prove you’ve paid the statutory minimum for at least six years. These records typically include payroll data, hours worked, and any relevant contracts or agreements. Since the burden of proof rests with the employer in disputes, maintaining meticulous documentation is a vital defensive strategy. We suggest digital record-keeping solutions to ensure your business remains resilient during potential HMRC audits or inspections.

Can I include tips or gratuities in the calculation of the minimum wage?

You cannot include tips, gratuities, or service charges when calculating whether a worker has received the minimum wage. All statutory rates must be met through basic gross pay before any discretionary payments are added. Since the Employment (Allocation of Tips) Act 2023 came into force, businesses must also ensure 100% of tips are distributed fairly. It’s a complex area where our bespoke advisory services help maintain both compliance and staff morale.

How often do the National Minimum Wage rates change in the UK?

National Minimum Wage rates typically change once per year on 1 April. The government usually announces these adjustments in the preceding Autumn Statement following recommendations from the Low Pay Commission. Staying informed about these annual cycles allows for better strategic planning and prevents last-minute adjustments to your pricing models. We recommend a proactive approach to these statutory shifts to ensure your commercial interests and legal obligations remain in balance.