What if the financial vehicle you’ve spent a lifetime building as a tax-efficient legacy suddenly becomes the primary focus of a 40% fiscal levy? You’ve likely relied on the long-standing principle that your retirement savings sit safely outside your estate, providing a secure bridge to the next generation. However, the decision to include most unused funds and death benefits within the scope of inheritance tax on pensions starting from 6 April 2027 fundamentally alters the UK’s wealth transfer environment. It’s a significant shift that introduces a complex layer of liability for families who previously felt their long-term plans were settled.

We understand that this legislative transition feels both sudden and intricate. Our role is to provide the calm, expert guidance needed to transform this uncertainty into a structured, resilient plan. You’ll gain a precise understanding of how these new boundaries affect your specific holdings and discover bespoke strategies designed to mitigate the impact of the 2027 changes. We’ll explore the intersection of these rules with existing income tax obligations; we will also present pragmatic alternatives that ensure your family’s financial security remains protected for years to come.

Key Takeaways

- Understand the implications of the April 2027 legislative shift, which will bring most pension types into the taxable estate for the first time.

- Identify how the convergence of beneficiary income tax and inheritance tax on pensions could create an effective tax rate exceeding 70% without proactive planning.

- Discover why the traditional “pension-last” withdrawal strategy may now be counter-productive and how to recalibrate your estate depletion for maximum efficiency.

- Explore bespoke alternatives to pension wealth, including the strategic application of statutory gifting rules to protect your family legacy.

- Learn why a holistic professional review is essential before the 2027 deadline to ensure your long-term financial objectives remain secure under the new regime.

Inheritance Tax on Pensions: The Current 2026 Strategic Landscape

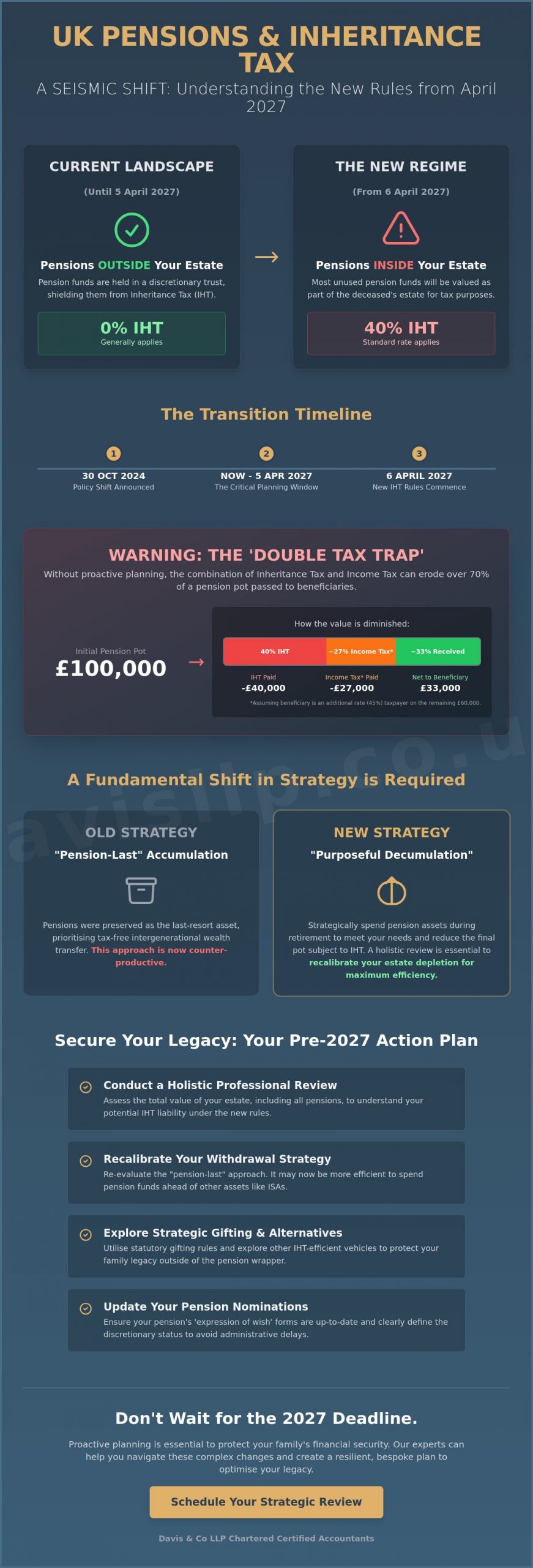

Pensions have traditionally served as the cornerstone of sophisticated estate planning in the United Kingdom. For decades, they functioned as a sanctuary for wealth, shielded from the standard 40% levy that applies to other assets. This protection is not accidental; it’s a deliberate result of the legal structure governing most modern schemes. Because the pension administrator holds discretionary power over who receives benefits, the assets don’t technically belong to the individual’s legal estate. However, the 30 October 2024 Autumn Budget fundamentally challenged this established logic. Chancellor Rachel Reeves announced that from April 2027, most unused pension funds will be brought into the value of the estate for tax purposes.

We’re observing a profound psychological shift among our clients as they prepare for these changes. The priority is moving from accumulating a legacy within a tax-free wrapper to a strategy of purposeful decumulation. The historical role of the pension as a “last resort” asset is fading. Instead, individuals are beginning to view their pots as a primary source of retirement spending, rather than a vehicle for multi-generational wealth transfer. This shift requires a meticulous review of current inheritance tax on pensions strategies before the 2027 deadline arrives.

The Definition of Pension Death Benefits in 2026

The current framework distinguishes between uncrystallised funds, which are sums not yet accessed, and drawdown pots where income has been taken but capital remains. Pension fund death benefits currently enjoy a privileged status, provided the scheme administrator distributes them within a strict two-year window from the date they were notified of the death. If the administrator fails to settle the benefits within this period, the funds can lose their tax-efficient status and become subject to different HMRC charges. Under current legislation, most registered pension schemes operate under discretionary trusts, which ensures they remain outside the member’s estate for inheritance tax purposes.

Why the Legislative Environment is Changing

The Government’s primary objective is to address what it perceives as a “wealth transfer” loophole that has expanded since the 2015 Pension Freedoms. By the 2027/28 tax year, HMRC projections indicate that bringing inheritance tax on pensions into the standard regime will affect approximately 49,000 estates annually. This policy change is expected to raise over £1.4 billion per year by the end of the decade. We often encounter the misconception that all pensions are currently exempt from tax. This isn’t the case. Certain older retirement annuity contracts or schemes that lack clear discretionary clauses already fall within the estate. The upcoming legislation simply standardises this treatment across the vast majority of UK pension providers to ensure fiscal consistency.

- 30 October 2024: The date the policy shift was officially announced.

- 6 April 2027: The scheduled commencement date for the new inheritance tax treatment.

- 8%: The estimated percentage of estates that will face increased tax liabilities due to this change.

The transition from the current landscape to the 2027 regime requires a calm, measured approach. It’s not a matter of panic, but of pragmatic adjustment. We recommend that clients begin auditing their current expressions of wish and nomination forms now. This ensures that the discretionary status is clearly defined and that the transition to the new rules doesn’t result in unnecessary administrative delays or unexpected tax burdens for beneficiaries.

The 2027 Legislative Shift: What Falls Within the Estate?

From 6 April 2027, the legislative landscape governing inheritance tax on pensions will undergo its most significant shift in decades. Under current rules, most unused pension funds and death benefits sit outside the value of a deceased person’s estate. This exclusion has long made pensions a primary tool for intergenerational wealth transfer. However, the government’s new framework ends this status, bringing the vast majority of pension assets into the taxable estate. This change applies to funds held at the date of death for any individual passing away on or after the 2027 deadline.

The scope of the new rules is broad. Most registered pension schemes will be brought into the IHT net, including:

- Defined Contribution (DC) pots, such as SIPPs and personal pensions.

- Unused funds in occupational pension schemes.

- Certain lump-sum death benefits that are not already subject to tax.

While the net is wide, specific exemptions remain. Dependant’s scheme pensions, which provide a guaranteed, lifelong income to a surviving spouse or civil partner, generally stay outside the estate. These are viewed as a continuation of retirement support rather than a transfer of capital. Scheme administrators and personal representatives will face a new era of administrative complexity. Administrators must now report pension values to HMRC, while personal representatives will be responsible for incorporating these figures into the final IHT400 account. We suggest seeking bespoke advice on estate valuation to manage these new reporting obligations effectively.

In-Scope vs. Out-of-Scope Assets

Defined Contribution pots are the primary target of this legislation because they represent a flexible “pot” of money. In contrast, most Defined Benefit (DB) “Death in Service” benefits remain excluded. These payments are typically calculated as a multiple of salary and don’t constitute an “unused fund” in the traditional sense. The 2027 pension IHT changes also clarify that Qualifying Recognised Overseas Pension Schemes (QROPS) will likely see their status aligned with UK schemes to ensure parity and prevent the use of offshore transfers as a tax avoidance measure.

The Valuation Process for IHT Purposes

HMRC intends to value unused pension funds based on their market value at the date of death. This valuation will then be aggregated with other assets like property and savings. This interaction is critical because it directly consumes the Nil Rate Band (NRB) of £325,000 and, where applicable, the Residence Nil Rate Band (RNRB) of £175,000. For an estate that was previously just under the £500,000 threshold, the addition of a £200,000 pension pot could trigger a 40% tax bill on the surplus. Executors don’t always have immediate access to pension data, and the 2027 rules will likely cause delays in probate if providers aren’t prepared for the sudden influx of valuation requests.

The ‘Double Tax Trap’: Navigating the Convergence of IHT and Income Tax

From April 2027, the long-standing exemption of most pension schemes from the value of a deceased person’s estate will cease. This policy shift introduces a significant fiscal challenge where inheritance tax on pensions converges with the beneficiary’s personal income tax liability. We view this as a ‘double tax trap’ because it layers two distinct levies on the same asset, potentially eroding the majority of a hard-earned retirement fund.

The sequence of taxation is particularly punitive. HMRC applies the 40% IHT charge to the pension fund first as part of the estate’s total valuation. The remaining 60% of the pot isn’t considered “tax-paid” in the eyes of the Revenue; it remains subject to the beneficiary’s marginal rate of income tax if the original holder died after age 75. This means the heir receives a net amount that has been twice diminished.

Calculating the Effective Tax Hit

The interaction of different levies creates a tiered depletion of wealth. Consider a hypothetical case where a £100,000 pension pot is passed to a beneficiary after the owner reaches age 75. If the estate exceeds the available nil-rate bands, £40,000 is immediately settled as IHT. The beneficiary is then left with £60,000. If that beneficiary is an additional-rate taxpayer, they’ll pay 45% tax on that remaining balance, which amounts to £27,000.

In this scenario, the total tax bill is £67,000, leaving the heir with just £33,000. The ultimate burden depends heavily on the recipient’s position within the current tax brackets uk, as these bands determine the second layer of the “double tax” applied to the remaining pension value. When the tapering of personal allowances for high earners is factored in, the effective tax rate can easily exceed 70%.

Mitigating the Beneficiary’s Income Tax Burden

We often advise clients that the method of extraction is as important as the timing of the gift. Taking the entire pension as a lump sum post-2027 will likely be the least efficient route for most families. It risks pushing the beneficiary into a higher tax bracket for that specific tax year, unnecessarily inflating the Revenue’s share.

Strategic use of “pension drawdown” for beneficiaries serves as a vital tax-management tool. By keeping the funds within a drawdown wrapper, the beneficiary can:

- Withdraw smaller amounts annually to stay within their existing tax band.

- Utilise their annual personal allowance (£12,570 for the current year) to take a portion of the income tax-free.

- Allow the remaining balance to continue growing in a tax-sheltered environment.

Bespoke Estate Planning: Strategic Alternatives to Pension Wealth

The historical advice to preserve pension pots as a tax-free legacy is fundamentally challenged by the 2027 reforms. Since the pension is now part of the taxable estate, the “spend the pension first” strategy regains its logical footing. We recommend clients review their drawdown schedules to deplete these funds while preserving assets that still benefit from specific reliefs. For instance, portfolios qualifying for Business Relief (BR), such as those on the Alternative Investment Market (AIM), can become exempt from IHT after a two-year holding period. This provides a stark contrast to the new treatment of inheritance tax on pensions.

Whole of Life insurance policies also play a critical role in this new environment. When these policies are written under a bespoke trust, the payout doesn’t form part of your legal estate. Instead, it provides a liquid sum to your beneficiaries, allowing them to settle tax liabilities without the need to sell family assets or liquidate investments at an inopportune time. It’s a pragmatic solution for those with illiquid estates or complex business interests.

- Utilise Business Relief to secure 100% exemption on qualifying assets after two years.

- Accelerate pension drawdown to fund lifestyle costs before touching non-taxable assets.

- Establish Whole of Life cover to provide immediate liquidity for HMRC payments.

Gifting and Potentially Exempt Transfers (PETs)

Clients often overlook the “normal expenditure out of income” exemption. If you have excess pension income, you can gift it immediately without it falling under the seven-year rule, provided it doesn’t diminish your standard of living. For larger capital sums, understanding the inheritance tax gift rules uk is vital to ensure PETs are structured correctly. This might include funding a lifetime isa for first time buyers for grandchildren. It’s an effective way to move wealth down generations while the donor is still alive, reducing the long-term impact of inheritance tax on pensions.

Trusts as a Strategic Alternative

Family Investment Companies (FICs) offer a robust alternative for those seeking to retain control while shifting value. By using different share classes, you can freeze the value of your own interest while passing future growth to your heirs. Discounted Gift Trusts (DGTs) also remain a powerful tool; they allow you to gift a lump sum but retain a lifetime right to fixed payments. This reduces the immediate value of your estate for tax calculations. The precision of a bespoke trust deed is paramount. It ensures the structure withstands regulatory scrutiny and evolving HMRC interpretations.

Strategic Partnership: How Davis & Co LLP Optimises Your Legacy

We approach complex private client matters with a philosophy of quiet excellence. The shifts announced in the Autumn Budget 2024 represent a fundamental change in how the UK treats death benefits. It’s no longer sufficient to treat pension pots as isolated, tax-free vehicles. We provide the intellectual rigour required to navigate the decumulation phase, ensuring your retirement spending doesn’t inadvertently increase the inheritance tax on pensions liabilities for your beneficiaries. Our role is to act as a steady, dependable constant in a volatile regulatory environment.

The 2027 implementation date may seem distant, but the complexity of modern estates requires immediate attention. We don’t believe in hurried solutions. Instead, we offer a measured, deliberate strategy that respects the nuance of your financial life. It’s about securing a legacy that reflects your values while maintaining the necessary professional distance to ensure objective, high-calibre advice.

The Davis & Co Holistic Review Process

Our review begins with a comprehensive audit of your global footprint. We evaluate the critical interplay between international tax planning and your UK-based pension assets. This ensures that assets held in different jurisdictions don’t create conflicting tax burdens or compliance failures. We’ve seen how easily uncoordinated plans can lead to double taxation or missed exemptions.

- Coordination with legal teams to align Wills and expressions of wish.

- Assessment of the 40% tax impact on combined estate values.

- Regular monitoring of HMRC’s draft legislation as it evolves through 2025.

- Strategic rebalancing of “liquid” versus “pension” assets.

We work closely with your legal advisors to ensure your testamentary documents are robust. This is vital because HMRC expects to clarify the technicalities of the 2027 rules throughout the next eighteen months. We stay ahead of these updates to keep your strategy compliant and effective.

Securing Your Professional Advisor

Generic, off-the-shelf solutions often fail when faced with the 2027 changes. The inclusion of pension death benefits in the value of an estate requires proactive planning rather than reactive adjustments. We act as a strategic partner, helping you decide whether to draw down pension funds earlier or gift assets during your lifetime. These decisions carry significant weight and require a bespoke approach tailored to your specific commercial and personal objectives.

The decumulation phase of retirement is now a primary focus for tax efficiency. By managing your withdrawals with precision, we can help in minimising the inheritance tax on pensions that your heirs might otherwise face. Our firm is traditional in its values but contemporary in its application of the law. To protect your family’s financial future and secure a tailored consultation, you can contact Davis & Co LLP for expert tax advice in the UK.

Securing Your Legacy in a Shifting Legislative Landscape

The transition toward the April 2027 legislative framework marks a fundamental shift in how the UK government treats retirement assets. By bringing most unused pension funds into the value of a deceased person’s estate, the new rules introduce a complex layer of inheritance tax on pensions that previously didn’t apply. This convergence of IHT and income tax requires a precise, forward-thinking approach to ensure your beneficiaries don’t face an unnecessary double tax burden. It’s no longer enough to rely on legacy structures; active management is required to preserve capital across generations.

Since 1901, Davis & Co LLP has provided the discretion and technical expertise required to navigate such sensitive statutory changes. As Chartered Certified Accountants, we specialise in bespoke solutions for international family offices and complex private client matters. We’re committed to ensuring your financial architecture remains robust and compliant with the latest regulations. Consult with our specialist tax partners to refine your estate strategy. We’re ready to help you secure a stable and prosperous future for your family.

Frequently Asked Questions

Will my pension be subject to inheritance tax if I die before April 2027?

Your pension assets remain exempt from inheritance tax if death occurs before 6 April 2027. Under current legislation, most UK registered pension schemes are held in discretionary trusts, which keeps them separate from your legal estate. This exemption remains in place for all deaths recorded up to the end of the 2026/27 tax year.

Does the 2027 rule change apply to both Defined Contribution and Defined Benefit pensions?

The 2027 rule changes apply to both Defined Contribution and Defined Benefit schemes. The government’s October 2024 budget confirmed that most unused pension funds and death benefits will be brought into account for inheritance tax. While DC pots are the primary focus, DB lump sum death benefits will also be aggregated with the estate.

How much inheritance tax will be paid on a pension pot of £500,000?

A pension pot of £500,000 could attract a tax bill of £200,000 if your nil-rate bands are already exhausted by other assets. Since the standard inheritance tax rate is 40%, the liability depends on whether the £325,000 nil-rate band or the £175,000 residence nil-rate band applies to the estate. We recommend a bespoke review of your total asset valuation to determine the precise exposure.

Can I avoid inheritance tax on my pension by taking it as a lump sum now?

Withdrawing your pension as a lump sum now will likely increase your tax liability rather than reduce it. Once funds leave the pension wrapper, they enter your bank account and become part of your legal estate immediately. You’ll also face immediate income tax on the withdrawal at your marginal rate, which can be as high as 45% for additional rate taxpayers.

What happens to the “Age 75” income tax rule after the 2027 IHT changes?

The existing income tax rules for beneficiaries will remain in place alongside the new inheritance tax on pensions. If death occurs after age 75, beneficiaries must pay income tax at their marginal rate on any withdrawals. This creates a dual tax charge where the pension’s first reduced by 40% IHT and then the remainder’s taxed as income when accessed by your heirs.

Are overseas pensions (QROPS) affected by the UK inheritance tax changes?

Overseas pensions, including Qualifying Recognised Overseas Pension Schemes (QROPS), fall within the scope of these new regulations for UK-domiciled individuals. HMRC intends to align the treatment of offshore schemes with domestic ones to ensure consistency. If you hold significant assets in a QROPS, it’s vital to assess how these 2027 changes impact your global estate planning strategy.

How do I report pension assets to HMRC as an executor under the new rules?

Executors will be responsible for reporting pension values to HMRC using updated versions of the IHT400 forms. From April 2027, pension scheme administrators will be required to provide the necessary valuation data to the personal representatives of the estate. This process ensures that the inheritance tax on pensions is calculated accurately alongside other assets like property and investments.

Is there any way to keep my pension outside of my estate after 2027?

Options for keeping pension assets outside the estate will be significantly restricted after the 6 April 2027 deadline. Strategic planning might involve gifting from surplus income or utilizing the £3,000 annual exemption to reduce the overall estate value. We focus on providing tailored advice that balances your capital needs with the objective of mitigating the 40% tax charge through legitimate statutory reliefs.