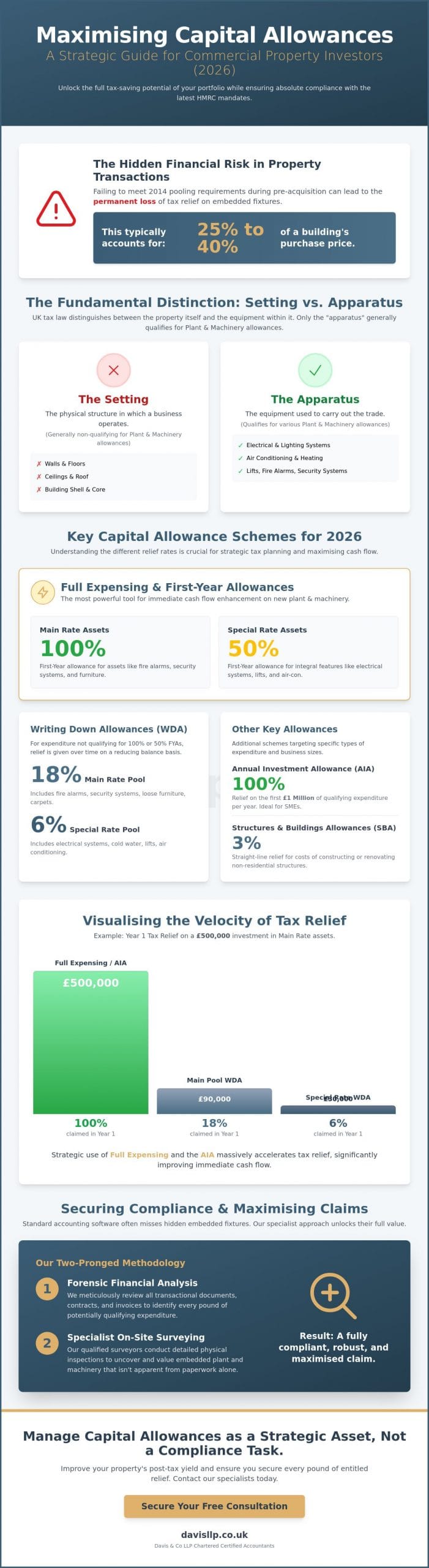

The most significant financial oversight in a property transaction often occurs before the ink is dry on the contract. If your legal team fails to address the 2014 pooling requirements during negotiations, you risk permanently forfeiting tax relief on embedded fixtures that typically account for 25% to 40% of a building’s purchase price. Securing capital allowances for commercial property is not a mere accounting exercise to be settled at year-end; it’s a strategic imperative that requires precise attention during the pre-acquisition phase. We understand that the complexity of current UK legislation can feel like a barrier to entry for even the most seasoned investors.

You likely recognise that missing out on legitimate tax relief is an unnecessary drain on your capital. This guide provides the clarity you need to unlock the full tax-saving potential of your portfolio while ensuring absolute compliance with the latest HMRC mandates. We’ll explore the technical nuances of the 2026 landscape, specifically focusing on the strategic balance between Full Expensing and Structures and Buildings Allowances (SBAs) to help you maximise immediate cash flow and long-term fiscal stability.

Key Takeaways

- Distinguish between the physical setting of a business and the qualifying apparatus within it to identify the appropriate relief rates for your assets.

- Utilise the 2026 Full Expensing regime to accelerate cash flow through 100% and 50% first-year allowances on qualifying plant and machinery.

- Secure your right to claim capital allowances for commercial property by ensuring the seller meets the 2014 pooling requirements before you sign a purchase contract.

- Avoid the limitations of standard accounting software by combining forensic financial analysis with specialist surveying to uncover hidden embedded fixtures.

- Manage capital allowances as a strategic investment asset rather than a routine compliance task to significantly improve your property’s post-tax yield.

The Fundamentals of Capital Allowances for Commercial Property in 2026

A Capital allowance serves as the primary statutory mechanism for businesses to deduct the cost of certain capital assets from their taxable profits. Under the Capital Allowances Act 2001, this relief isn’t a discretionary benefit but a legal entitlement that replaces the accounting concept of depreciation, which is generally not tax-deductible in the UK. When considering capital allowances for commercial property, we must distinguish between the “setting” in which a trade is carried out and the “apparatus” used to perform that trade. A wall is typically the setting. The electrical cabling and air conditioning units within that wall are the apparatus. This distinction is critical. Only the latter generally qualifies for relief under the plant and machinery rules.

The Annual Investment Allowance (AIA) remains a cornerstone of this framework. For the 2026 tax year, the AIA provides 100% immediate relief for qualifying expenditure up to a limit of £1 million. This threshold allows most small to medium-sized enterprises to write off the total cost of their property improvements in a single period, which significantly enhances short-term liquidity and supports further investment.

Identifying Qualifying Capital Expenditure

To claim successfully, the expenditure must be incurred “wholly and exclusively” for the purposes of the trade. While a new building’s shell and core might only yield qualifying assets worth 10% of the total cost, a high-specification internal refurbishment often sees this figure rise to 40% or more. The timing of this expenditure is vital. In 2026, the specific date of “incurring” expenditure often hinges on when the obligation to pay becomes unconditional. This detail can shift a claim between different financial years and impact the available relief rates based on changing statutory requirements.

Freeholders vs. Leaseholders: Who Can Claim?

Entitlement to claim depends on holding the “relevant interest” in the property. While freeholders typically claim for the building’s core integral features, leaseholders are entitled to relief on their specific fit-out costs and improvements. When a landlord provides a capital contribution to a tenant’s fit-out, the tax treatment requires careful structuring. We often see disputes arise when the lease doesn’t clearly define which party retains the property interest in the fixtures. Strategic coordination between parties during the heads of terms phase ensures that capital allowances for commercial property aren’t lost due to ambiguous contractual language.

Evaluating Relief Rates: Main Pool, Special Rate, and SBAs

Strategic allocation of expenditure between the various capital allowance pools determines the velocity of your tax relief. We often find that the most effective approach involves a calculated hierarchy of claims. Because the Annual Investment Allowance (AIA) provides 100% relief, it’s mathematically superior to apply this first to assets that would otherwise fall into the 6% Special Rate pool. This prioritisation ensures that the slowest-moving tax relief is accelerated to the current financial year, preserving the 18% Main Pool for subsequent claims. A detailed guide to capital allowances for commercial property can provide the foundational knowledge required to categorise these assets correctly.

| Allowance Type | Writing Down Allowance (WDA) | Qualifying Assets |

|---|---|---|

| Main Pool | 18% (Reducing Balance) | Fire alarms, security systems, loose furniture, carpets. |

| Special Rate Pool | 6% (Reducing Balance) | Electrical systems, cold water, lifts, air conditioning. |

| SBA | 3% (Straight Line) | Walls, floors, ceilings, external landscaping. |

The Definition of Integral Features

Integral features represent a specific category of plant and machinery that HMRC deems essential to the building’s function. This list includes electrical systems (including lighting), cold water systems, space or water heating, and lifts. We must also consider the “replacement rule” for these features. If you spend more than 10% of the cost of replacing an integral feature within a 12-month period, the entire amount must be treated as capital expenditure rather than a revenue repair. This statutory threshold often changes the tax treatment of routine maintenance programmes. To ensure your asset allocation is optimised for your specific portfolio, you may wish to consult our specialist advisory team for a bespoke assessment.

Structures and Buildings Allowance (SBA) Nuances

The SBA provides a flat 3% annual relief for structural works where the construction contract was signed on or after 29 October 2018. Unlike plant and machinery, SBAs don’t qualify for the AIA or Full Expensing. It’s also vital to distinguish between qualifying structural costs and non-qualifying items like land costs or planning fees. To claim this relief, you must maintain an “Allowance Statement” that documents the date of first use and the total qualifying cost. When you sell the property, the SBA doesn’t trigger a balancing charge; instead, the remaining relief transfers to the new owner, though the total claimed will be deducted from your base cost for Capital Gains Tax purposes. This makes capital allowances for commercial property a critical factor in long-term exit strategies.

Strategic Incentives: Full Expensing and the 2026 40% First-Year Allowance

While the Annual Investment Allowance provides a £1 million ceiling for many, larger capital projects require more robust statutory mechanisms. Full Expensing offers a permanent solution for companies, effectively removing the cap on qualifying expenditure. This regime is a powerful tool for those managing capital allowances for commercial property, yet its application remains nuanced and requires careful navigation of the underlying legislation. We see many investors struggle to reconcile these high-velocity incentives with their long-term tax strategies, particularly when dealing with high-value acquisitions.

Maximising Full Expensing for Corporate Landlords

Full Expensing is strictly reserved for companies within the charge to Corporation Tax. It allows for a 100% first-year deduction on Main Pool assets and a 50% first-year allowance for Special Rate assets. However, a significant hurdle exists in the form of the “leasing” restriction. Under Section 67 of the Capital Allowances Act 2001, assets provided for leasing are generally excluded from these accelerated allowances. For property investors, this means that while loose plant and machinery might be ineligible, “background plant and machinery” such as lifts, heating systems, and air conditioning often remain qualifying. Full Expensing accelerates tax relief for large-scale refurbishments by allowing the immediate deduction of the entire qualifying cost from taxable profits, rather than spreading it over several years through traditional writing-down allowances.

The 2026 40% FYA for Partnerships and Individuals

The landscape changes significantly on 1 January 2026 with the introduction of the 40% First-Year Allowance (FYA) for unincorporated businesses. This incentive is specifically designed for partnerships and individual investors who don’t benefit from corporate Full Expensing. By allowing a 40% deduction in the year of purchase, this allowance offers a substantial advantage over the standard 18% writing-down allowance. For a partnership undertaking a significant office fit-out, this front-loading of relief can be the difference between a project being viable or deferred. Qualifying assets for this 2026 incentive include new and unused plant and machinery, such as specialised security systems or advanced fire suppression equipment. We recommend that clients timing their expenditure around the 1 January 2026 start date consider the impact on their overall capital allowances for commercial property claim to ensure they don’t inadvertently trigger less favourable rates from a previous period.

Transactional Risks: Pooling Requirements and Section 198 Elections

The transfer of commercial real estate is rarely just a matter of title and land. The statutory framework governing capital allowances for commercial property underwent a paradigm shift in April 2014, introducing mandatory pooling and fixed value requirements. These rules dictate that a purchaser’s right to claim relief on embedded fixtures is entirely contingent upon the seller’s prior actions. If a seller hasn’t correctly pooled their expenditure, the buyer is legally barred from making a claim. This creates a significant risk of value erosion that must be addressed during the pre-contract phase. We’ve seen numerous instances where the lack of a structured tax strategy during the inquiry stage led to the permanent forfeiture of six-figure reliefs.

The Section 198 election serves as the formal mechanism to fix the value of fixtures at the point of sale. It’s a joint statement submitted to HMRC that prevents future disputes by establishing a clear, agreed-upon figure. While the default might be to use a portion of the purchase price, strategic investors often negotiate specific values to suit their respective tax positions. Sellers often seek to avoid “balancing charges” that occur if the sale price of the fixtures exceeds their remaining tax value, while buyers naturally want to maximise their future writing-down allowances.

The Section 198 Election: Protecting Investment Value

There’s a distinct strategic benefit in the ‘£2 value’ election when a seller wishes to retain the benefit of their previous claims. This nominal figure allows the buyer to satisfy the pooling requirement without the seller incurring a tax clawback. However, this is only effective if the buyer understands they’re effectively inheriting a zero-tax-value asset for those specific fixtures. Robust pre-contract due diligence is the only way to safeguard these interests. For those involved in cross-border acquisitions, these local requirements must be harmonised with broader international tax planning strategies to ensure global fiscal efficiency.

The Mandatory Pooling Trap

Failing to verify a seller’s capital allowance history is a costly oversight. Prudence dictates that your legal team issues specific enquiries regarding the seller’s tax returns and previous elections. If the seller hasn’t claimed, there’s often a window of opportunity to compel them to pool the expenditure as a condition of the sale. Once the transaction completes, a strict two-year statutory window opens. If an agreement or a tribunal application isn’t made within these 24 months, the right to claim on those specific fixtures is extinguished for the life of the property. Negotiating these tax clauses requires a blend of legal precision and specialist accounting insight. To protect your next acquisition from these transactional risks, contact our commercial property team for a comprehensive review of your heads of terms.

Securing Compliance: The Davis & Co LLP Approach to Property Claims

Standard accounting software generally lacks the granularity to distinguish between non-qualifying structural elements and qualifying plant. Most platforms categorise a property purchase as a single capital entry; they overlook the approximately 20% to 35% of the purchase price that typically resides in embedded fixtures. Relying solely on automated ledger entries often results in significant under-claiming. Successful management of capital allowances for commercial property requires a dual-disciplinary approach that merges forensic accounting with specialist surveying expertise. This ensures that every component, from hidden cabling to complex HVAC systems, is correctly identified and valued according to current statutory standards.

Forensic Identification of Embedded Fixtures

Identifying qualifying costs within general building contracts demands a deep dive beyond the top-line invoice. In many cases, a contractor’s summary valuation misses the technical nuances required for a robust HMRC claim. We perform a look-through analysis on historic property acquisitions to uncover unclaimed relief that may have been overlooked during the initial transaction. The Davis & Co methodology for bespoke property tax analysis combines forensic cost segregation with precise statutory interpretation to identify and value qualifying assets that standard accounting practices often overlook. By providing this level of detail, we ensure that your claim remains defensible under rigorous HMRC scrutiny.

Strategic Advisory for Long-Term Growth

Effective tax planning is an iterative process. As legislation evolves throughout 2026, maintaining a static approach to your portfolio can lead to missed opportunities for reinvestment. These allowances aren’t merely tax savings. They’re a vital component of business growth and management accounting, providing the cash flow necessary to fund future developments or debt reduction. Integrating these claims with broader expert tax advice in the UK ensures that your property strategy remains aligned with your overall corporate objectives. We recommend regular reviews of your asset register to capture the impact of ongoing refurbishments and legislative shifts. To ensure your portfolio is fully optimised for the coming year, you may enquire about a bespoke capital allowance review with our specialist team.

Strategic Planning for Your 2026 Property Portfolio

Mastering the technical landscape of capital allowances for commercial property requires more than just routine compliance. It demands a proactive stance on the 2014 pooling requirements and a precise understanding of how the 2026 incentives, such as the 40% First-Year Allowance, can be leveraged to accelerate your cash flow. By identifying embedded fixtures through forensic analysis rather than basic accounting, you ensure that no legitimate relief is left unclaimed during property acquisitions or refurbishments. These tax-saving opportunities are often lost permanently if you don’t address them within the strict two-year statutory window following a transaction.

As Chartered Certified Accountants with over 120 years of expertise, Davis LLP provides the specialist knowledge required for complex property accounting and international tax matters. Our partner-led service offers the bespoke guidance necessary to manage these statutory requirements with the precision your portfolio deserves. We invite you to contact our specialist property tax team for a bespoke capital allowance assessment to safeguard your investment’s fiscal health. Securing your tax position today provides a solid foundation for your future commercial objectives.

Frequently Asked Questions

What qualifies as plant and machinery in a commercial building?

Plant and machinery include assets used for the trade’s functional operation rather than the building’s structural setting. Common examples include fire alarms, security systems, and air conditioning units. For a typical office, these fixtures often represent 25% of the total acquisition cost. Under the Capital Allowances Act 2001, items like carpets and loose furniture also qualify, provided they aren’t part of the property’s permanent structural fabric.

Can I claim capital allowances on a property I bought years ago?

You can claim on historic purchases as long as you still own the property and the assets remain in use. There is no statutory time limit for making a claim on expenditure incurred in previous years. However, for properties acquired after April 2014, your ability to claim depends entirely on whether the previous owner correctly pooled the expenditure before the sale. This makes a retrospective review of your portfolio a high-value exercise.

What is the difference between repairs and capital expenditure?

Repairs are revenue expenses that restore an asset to its original condition without improving it. Capital expenditure involves the installation of new assets or the substantial replacement of existing ones. If you replace more than 10% of an integral feature, such as a heating system, within a 12-month period, HMRC requires the entire cost to be treated as capital expenditure rather than a deductible repair. This statutory threshold significantly alters the timing of your tax relief.

How does a Section 198 election affect the sale price of a property?

A Section 198 election does not alter the total sale price; it merely fixes the portion of that price attributed to fixtures for tax purposes. This agreement prevents future disputes with HMRC by establishing a clear value for both the buyer and seller. Without this election, the buyer may be unable to claim capital allowances for commercial property, which can negatively impact the property’s long-term investment value and yield.

Can I claim capital allowances on a second-hand commercial property?

You can claim on second-hand properties, provided the mandatory pooling and fixed value requirements are satisfied. The amount you can claim is generally restricted to the lower of the portion of your purchase price allocated to fixtures or the previous owner’s original qualifying expenditure. This makes the review of the seller’s capital allowance history a critical step in your pre-contract due diligence to avoid the permanent loss of relief.

What happens to capital allowances if I demolish the building?

Demolishing a building is treated as a disposal of the qualifying assets within it. This process usually triggers a balancing allowance, which can provide a final tax deduction for any remaining unclaimed value in the capital allowance pools. However, if the scrap value or insurance proceeds exceed the tax written-down value, a balancing charge may arise. This charge effectively adds that excess back to your taxable profits for that period.

Are Structures and Buildings Allowances (SBAs) better than plant and machinery claims?

Plant and machinery claims are typically more beneficial because they offer higher relief rates. While SBAs provide a flat 3% annual deduction over 33 years, plant and machinery can attract 18% or 6% writing-down allowances. Crucially, plant and machinery expenditure often qualifies for the £1 million Annual Investment Allowance. This provides 100% relief in the year of purchase, an advantage that is not available for SBAs.

Do I need a specialist surveyor to claim capital allowances?

Engaging a specialist surveyor is essential for identifying the “embedded” fixtures that aren’t itemised on standard invoices. A surveyor understands construction costs and can provide the technical evidence HMRC requires to support capital allowances for commercial property claims. This forensic approach ensures that your claim is both maximised and compliant, as standard accounting practices often fail to capture the full scope of qualifying assets hidden within a building’s structure.