The traditional approach to property investment often treats fiscal obligations as a secondary concern; however, in the current regulatory environment, your tax strategy is the primary driver of your long-term yield. Since the Stamp Duty surcharge increased to 5% in late 2024, the initial tax on buying a house to rent out has become a substantial capital consideration that requires precise calculation from the outset. We understand that the convergence of Section 24 finance restrictions and the impending April 2026 Making Tax Digital requirements can feel like a daunting hurdle for even the most seasoned landlords.

It’s natural to feel concerned about how these shifting thresholds will impact your bottom line, especially with income tax rates for property income set to rise in 2027. We’ve developed this guide to provide the clarity you need to move forward with confidence. You’ll find a detailed breakdown of acquisition costs, a strategic framework for choosing between personal or company ownership, and a roadmap for meeting the new HMRC digital reporting standards. By the end of this analysis, you’ll have a structured plan to protect your portfolio’s profitability in a more demanding fiscal era.

Key Takeaways

- Calculate your total capital requirements by accounting for the 5% Stamp Duty surcharge and any non-resident levies applicable to the tax on buying a house to rent out.

- Evaluate the financial merits of personal versus limited company ownership to mitigate the impact of Section 24 mortgage interest relief restrictions.

- Prepare for the April 2026 Making Tax Digital transition by establishing digital record-keeping processes that align with HMRC’s new reporting standards.

- Protect your portfolio’s profitability by correctly identifying “wholly and exclusively” allowable expenses to reduce your taxable rental income.

- Strategic disposal planning is essential to manage the 60-day reporting window and current Capital Gains Tax rates when you decide to sell.

The Initial Tax Burden: Stamp Duty and Acquisition Costs in 2026

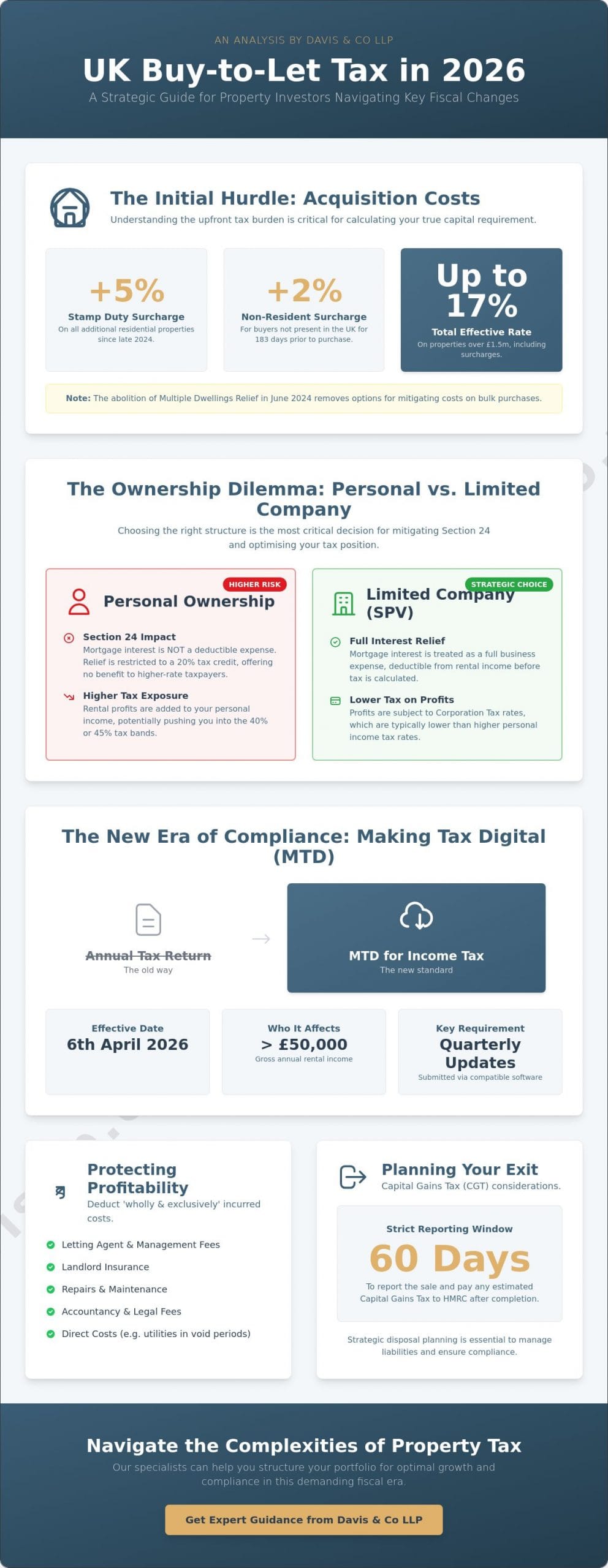

Securing a buy-to-let asset in 2026 begins with a significant capital allocation for the Exchequer. The tax on buying a house to rent out is no longer a marginal cost. It’s a core component of your acquisition budget. Since October 2024, the surcharge for additional residential properties has been set at 5%, applied on top of the standard Stamp Duty Land Tax (SDLT) rates. This means even the lowest price bracket, up to £125,000, incurs a 5% charge. For properties exceeding £1.5 million, the top effective rate reaches 17%. With the abolition of Multiple Dwellings Relief in June 2024, investors can no longer mitigate these costs through bulk purchase adjustments, making precise pre-purchase accounting essential.

Navigating the SDLT Surcharge Framework

Determining your liability requires a binary assessment of your current global property holdings. If you, or your spouse, already own a residential interest anywhere in the world, the 5% surcharge is triggered. There are narrow exceptions for those replacing a main residence, but the criteria are strict. If you buy a new home before selling your old one, you must pay the surcharge upfront. You can apply for a refund if the previous residence is sold within 36 months, yet this creates a temporary but significant cash flow strain. We often assist clients in evaluating these timing risks to ensure their liquidity remains intact. The reason for purchase dictates your initial exposure; a property intended for rental use will almost always attract the higher rates regardless of your intent to occupy it later.

International and Non-Resident Considerations

International investors face an additional layer of complexity that many competitors overlook. If you haven’t been present in the UK for at least 183 days during any continuous 365-day period starting before the purchase, a 2% non-resident surcharge applies. This levy is cumulative. A non-resident individual or company calculating the tax on buying a house to rent out will face a combined 7% surcharge over standard rates.

Strategic timing is vital here. Managing residency-based liabilities often involves careful coordination of purchase dates and travel schedules to ensure you don’t inadvertently trigger the non-resident threshold. While acquisition costs are immediate, we encourage our clients to review Capital Gains Tax rules early in the process. Understanding the eventual exit costs helps in calculating the true net present value of the asset. Our international tax planning services focus on these interactions to prevent unforeseen tax leakage at the point of entry.

Tax on Rental Profits: Navigating the 2026 Landscape

Once the acquisition phase is complete, the focus shifts to the recurring fiscal obligations associated with your yield. It’s essential to recognize that rental income isn’t taxed in isolation; it’s added to your existing earnings, potentially moving you into a higher tax bracket. For the 2026/2027 tax year, the higher rate of 40% applies once your total taxable income exceeds £37,700. When calculating the ongoing tax on buying a house to rent out, you must decide between the £1,000 property allowance and deducting actual expenses. While the allowance offers simplicity for smaller portfolios, most professional investors find that itemizing allowable expenses provides a more efficient tax position. You can find official guidance on paying tax on rental income to help distinguish between these two paths.

The 2026 Transition to Making Tax Digital (MTD)

The most significant shift in property administration arrives on 6 April 2026. Landlords with a gross rental income exceeding £50,000 must comply with Making Tax Digital (MTD) for Income Tax Self-Assessment. This mandate replaces the traditional annual return with a requirement for quarterly digital updates. It’s a move toward real-time transparency that demands a more disciplined approach to financial record-keeping. Utilizing professional management accounts can bridge the gap between simple bookkeeping and the sophisticated reporting HMRC now expects. We’ve observed that early adoption of these digital workflows reduces the administrative burden and provides a clearer view of your investment’s performance throughout the year.

Calculating Taxable Profit in the Modern Era

Transitioning to quarterly reporting requires a nuanced understanding of your cash flow. You’ll need to report your gross income and expenses every three months, which provides a rolling estimate of your tax liability. This prevents the “tax bill shock” often associated with the January deadline but requires consistent digital bookkeeping to ensure accuracy. Maintaining a clear distinction between capital and revenue expenditure is vital to avoid HMRC penalties. If you’re managing a growing portfolio, our personal tax services can assist in aligning your quarterly updates with your broader financial goals. By treating your rental activity with the same rigour as a commercial enterprise, you ensure that your investment remains a source of wealth rather than an administrative burden.

Personal vs. Limited Company: The Ownership Dilemma

Choosing the right vehicle for your investment is a decision that carries long-term fiscal weight. While the initial Stamp Duty Land Tax rates, including the 5% surcharge, apply regardless of whether you buy personally or through a corporate structure, the ongoing tax on buying a house to rent out diverges sharply thereafter. Personal ownership offers simplicity and lower administrative costs, yet it exposes higher-rate taxpayers to significant pressures. In contrast, incorporation can shield profits from high personal tax rates but introduces a secondary layer of taxation when you eventually extract those funds as dividends.

The Impact of Finance Cost Restrictions (Section 24)

The most compelling argument for incorporation often stems from Section 24 of the Finance (No. 2) Act 2015. Individual landlords can’t deduct their mortgage interest from rental income before calculating their tax liability. Instead, they receive a 20% tax credit. For a higher-rate taxpayer, this creates a significant gap; you’re effectively paying 40% tax on the income used to pay the mortgage but only receiving 20% relief.

In practice, this mechanism can turn a cash-flow profit into a taxable loss. Imagine a property generating £15,000 in rent with £12,000 in mortgage interest. Personally, you’re taxed on the full £15,000, with a modest credit applied later. Within a company, you’re only taxed on the £3,000 profit. This disparity is why many of our clients now view personal ownership as a legacy model for all but the smallest portfolios.

The Strategic Use of Special Purpose Vehicles (SPVs)

Holding property within a Limited Company, often structured as a Special Purpose Vehicle (SPV), allows you to access Corporation Tax rates, which range from 19% to 25%. This structure is particularly beneficial if you intend to reinvest profits to grow your portfolio, as the funds aren’t depleted by 40% or 45% income tax before they can be deployed. However, you must account for the “double taxation” effect. Profits are taxed at the corporate level, and then you’ll face dividend tax when moving money to your personal accounts.

Managing these layers of compliance requires meticulous property accounting to ensure your company filings align with your personal tax objectives. We work as a strategic partner to help you navigate these choices, ensuring the administrative costs of a company don’t outweigh the fiscal benefits. Your structure should always reflect your final goal, whether that’s a steady retirement income or a multi-generational legacy for your heirs.

Optimising Yield: Allowable Expenses and Capital Allowances

The profitability of a property investment is determined not just by gross rental income but by the precision with which you manage deductible outgoings. While the initial tax on buying a house to rent out represents a fixed entry cost, your ongoing tax liability is variable and subject to your ability to identify allowable expenses. HMRC applies a strict “wholly and exclusively” test for any deduction. This means the expenditure must be incurred solely for the purpose of your property business. Common examples include landlord insurance, service charges, and ground rent; alongside the Replacement of Domestic Items Relief (RDIR) for furnished properties, which allows you to deduct the cost of replacing sofas, beds, or white goods.

Distinguishing Repairs from Improvements

The distinction between revenue and capital expenditure is a frequent point of scrutiny during tax reviews. Revenue expenditure covers “like-for-like” repairs that maintain the property’s current state, such as replacing broken tiles or repainting between tenancies. These are fully deductible from your annual rental income. In contrast, capital expenditure involves an investment in the property’s value rather than its maintenance. While these improvements aren’t deductible from rental income, they’re essential for reducing your future Capital Gains Tax (CGT) liability when you eventually dispose of the asset. We recommend keeping detailed records of all structural enhancements, such as extensions or loft conversions, to ensure they’re correctly accounted for during an exit.

Maximising Professional and Management Fees

Professional services are a vital category of tax-efficient spending. You can fully deduct fees paid to letting agents, legal costs for drafting tenancy agreements, and specialised tax advice uk. Engaging a professional property manager does more than alleviate administrative pressure; it ensures that every minor expense is tracked and categorised. We see many landlords suffer “yield leakage” because they fail to record small, legitimate costs like safety certificates or emergency call-outs. Precise digital bookkeeping is the only way to safeguard your margins against these oversights. To ensure your portfolio is operating at peak fiscal efficiency, consider our tailored property accounting services to manage your compliance and cash flow.

Strategic Exit Planning: Capital Gains and Inheritance Tax

A truly robust investment strategy considers the complete lifecycle of the asset. While much of your early focus naturally rests on the initial tax on buying a house to rent out, the fiscal implications of disposing of that asset are equally significant. Capital Gains Tax (CGT) remains a primary consideration for residential disposals. For the 2025/2026 tax year, the annual exempt amount has been reduced to £3,000. Any gains above this threshold are taxed at 18% for basic-rate taxpayers and 24% for those in higher brackets. Perhaps the most critical operational detail is the 60-day reporting and payment window; HMRC requires both the return and the full tax payment within two months of completion.

Managing Capital Gains Tax on Disposal

Mitigating your CGT liability requires foresight and meticulous documentation. We often advise clients to offset current gains against any previous capital losses carried forward from earlier tax years. This is where the record-keeping discussed in our previous section becomes invaluable. By accurately tracking capital improvements over decades, you can significantly reduce your taxable gain. In some instances, we explore staggered disposals across different tax years to ensure you remain within lower tax bands, provided this aligns with your broader liquidity requirements. This measured approach prevents unnecessary tax leakage and preserves the capital you’ve worked to build.

Inheritance Tax and Estate Integration

Property is often viewed as a “toxic” asset within an estate because it rarely qualifies for Business Property Relief (BPR). Since buy-to-let activities are generally classified as investments rather than trading businesses, the full value of the property is usually subject to the 40% Inheritance Tax (IHT) rate once the £325,000 nil-rate band is exhausted. To address this, we frequently integrate property portfolios into a trust tax services framework or establish Family Investment Companies (FICs).

These structures allow for a more nuanced transfer of wealth, potentially moving future growth out of your personal estate while you maintain control over the assets. Collaborative planning ensures that your property legacy isn’t eroded by a sudden IHT bill. By treating your portfolio as a dynamic component of your total wealth, we help you transition from simple ownership to a sophisticated estate strategy that protects your beneficiaries for the long term.

Securing Your Property Legacy in a Digital Era

The fiscal landscape for UK landlords has undergone a fundamental transformation, shifting from a passive investment model to one that requires active, digital-first management. We’ve explored how the 5% SDLT surcharge and the abolition of specific reliefs have redefined the initial tax on buying a house to rent out, making early structural decisions more critical than ever. Whether you’re navigating the complexities of Section 24 interest restrictions or preparing for the mandatory transition to Making Tax Digital in April 2026, the success of your portfolio depends on a proactive approach to compliance and yield optimisation.

As Chartered Certified Accountants since 1901, we’ve guided generations of investors through shifting regulatory tides. Our expertise in international and property tax planning ensures that your assets are structured to withstand both current pressures and future transitions. We invite you to consult with our property tax specialists for a tailored acquisition strategy that aligns with your long-term commercial objectives. With our comprehensive support for 2026 MTD requirements, you can focus on growing your portfolio while we ensure your reporting remains precise and efficient. We look forward to building a secure financial future together.

Frequently Asked Questions

Do I pay Stamp Duty if I am a first-time buyer but the house is for buy-to-let?

You don’t qualify for first-time buyer relief if the property is purchased for a buy-to-let purpose. Standard residential rates apply from the prevailing threshold. While you’ll avoid the 5% surcharge if you don’t own any other residential interests, you must still pay the standard SDLT that an owner-occupier would pay without the benefit of first-time buyer exemptions. This is a critical factor when calculating the total tax on buying a house to rent out.

How does the 2026 Making Tax Digital (MTD) rollout affect small landlords?

Landlords with gross rental income exceeding £50,000 will enter the MTD for Income Tax regime on 6 April 2026. This requires you to move away from annual filings in favour of quarterly digital updates and a final declaration. It’s a fundamental shift in how you interact with HMRC, necessitating the use of compatible software to track income and expenses. Preparing your digital workflows now will prevent administrative bottlenecks when the mandate takes effect.

Can I deduct my mortgage repayments from my rental income for tax purposes?

You cannot deduct the capital portion of your mortgage repayments from your rental income. Only the interest element is eligible for tax relief, which is provided as a 20% tax credit for individual landlords. This restriction can significantly impact your net return, particularly for those in the higher or additional tax brackets. If you’re calculating the total tax on buying a house to rent out, consider how this finance restriction affects your long-term cash flow.

What happens if my rental property makes a loss in the 2026/27 tax year?

If your property business incurs a loss in the 2026/27 tax year, you can carry that loss forward to offset against future profits from the same property business. You cannot generally use a property loss to reduce the tax due on your salary or other non-property income. Properly recording these losses is essential; they remain a valuable fiscal asset that can reduce your tax liability in more profitable future years.

Is it better to buy a rental property in my own name or through a company?

The decision between personal or company ownership depends on your wider financial circumstances and your plans for the rental income. Personal ownership is often the most straightforward path for basic-rate taxpayers. However, a limited company structure can offer superior tax efficiency for higher-rate taxpayers by bypassing Section 24 restrictions and accessing lower Corporation Tax rates. We provide detailed property accounting to help you determine which structure delivers the best net yield for your portfolio.

Do I need to pay National Insurance on my rental income?

You don’t usually pay National Insurance on income derived from a standard buy-to-let property. HMRC classifies rental income as investment income rather than earnings from employment or self-employment. This remains true even if you manage the properties yourself. Liability only arises if your property activities are extensive enough to be considered a professional trade, such as running a hotel or providing significant additional services to your tenants.

How long do I have to pay Capital Gains Tax after selling a rental house?

You have 60 days from the date of completion to report and pay any Capital Gains Tax due on the sale of a rental property. This is a strict statutory deadline that requires a specific digital submission to HMRC, separate from your annual tax return. It’s vital to calculate your gain and identify all deductible capital improvements well in advance. Late submissions or payments will result in automatic penalties and interest charges.

Can I claim the £1,000 property allowance if I have high expenses?

You can’t claim the £1,000 property allowance if you intend to deduct your actual business expenses. This allowance is a simplified alternative for those with very low costs. If your total allowable expenses, such as insurance, repairs, and management fees, exceed £1,000, you’ll achieve a lower tax bill by itemising your actual costs instead. Most professional landlords find that their genuine expenses far exceed this threshold, making the allowance redundant.