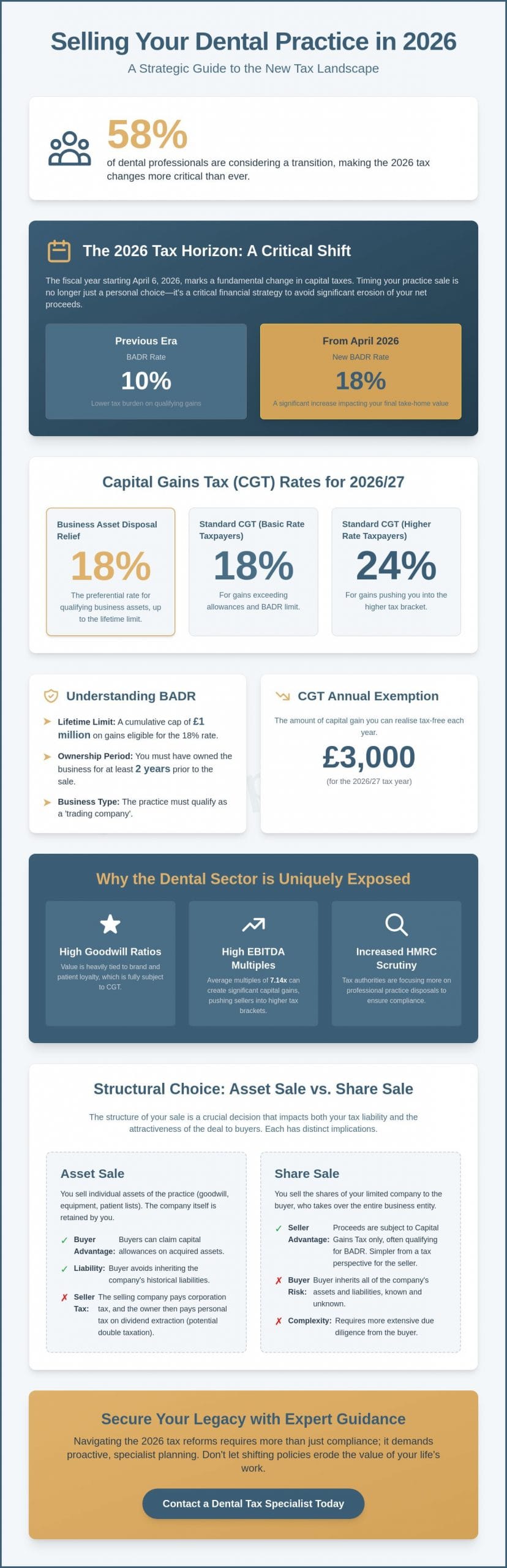

With 58% of dental professionals considering a transition this year, the market is remarkably active, yet many owners risk seeing their hard-earned equity eroded by shifting fiscal policies. If you’re planning an exit, understanding the selling a dental practice tax implications 2026 is no longer a matter of administrative routine; it’s a critical strategic necessity. We recognize that your practice represents years of professional dedication, and the prospect of losing a significant portion of your sale proceeds to HMRC is an unsettling concern.

You deserve a clear path through the complexities of the 2026/27 tax year, where standard Capital Gains Tax rates sit at 18% and 24% and the rate for Business Asset Disposal Relief has moved to 18%. This guide provides the expert insights you need to navigate these changes, offering a strategy to maximize your net proceeds while ensuring full compliance and peace of mind. We’ll explore the nuances of the £3,000 annual exempt amount, the £1 million lifetime limit for relief, and the essential structural differences between asset and share sales to help you secure the full value of your legacy.

Key Takeaways

- Understand why the 2026 fiscal year represents a significant turning point for capital taxes and how to manage the inherent volatility of the dental sector.

- Evaluate the specific selling a dental practice tax implications 2026, particularly the evolving thresholds and eligibility for Business Asset Disposal Relief.

- Determine whether an asset or share sale structure best aligns with your financial objectives and the current buyer appetite in the UK market.

- Learn how proactive pre-sale planning, including optimized pension contributions, can significantly reduce your effective tax bracket prior to a transaction.

- Discover the strategic advantages of a composed partnership with a dental tax specialist to ensure both regulatory compliance and maximum capital retention.

The Evolving Landscape of Dental Practice Disposals in 2026

The 2026 fiscal year represents a fundamental shift in how the UK government treats capital wealth. For clinicians, the selling a dental practice tax implications 2026 are profound. In the previous decade, practice transitions were often driven by retirement dates or clinical burnout. Today, the decision to exit is increasingly dictated by the tax calendar. The dental sector remains uniquely exposed to these changes because a significant portion of a practice’s value is tied up in personal or commercial goodwill, which is subject to the full weight of Capital Gains Tax (CGT).

We’ve observed a distinct transition in mindset among our clients. There’s a clear move away from the traditional “selling when ready” approach, replaced by a “selling when tax-efficient” strategy. This change is necessary as the gap between capital taxes and income taxes continues to narrow. If you misjudge the timing of your disposal, you could see your net proceeds reduced by a substantial margin. Several factors make the dental industry particularly sensitive to this volatility:

- High Goodwill Ratios: Dental valuations often rely heavily on patient loyalty and brand reputation rather than just physical assets.

- EBITDA Multiples: With average multiples reaching 7.14x in 2026, the capital gains involved are often significant enough to push sellers into the highest tax brackets.

- Regulatory Scrutiny: HMRC has increased its focus on professional practice disposals to ensure that capital treatments are applied correctly.

The 2026 Tax Horizon: What Has Changed?

Legislative updates for the 2026/27 tax year have established CGT rates at 18% for basic rate taxpayers and 24% for higher or additional rate taxpayers. This alignment with income tax structures suggests a broader fiscal strategy to capture more revenue from business disposals. When evaluating the selling a dental practice tax implications 2026, the primary concern for many of our clients is the erosion of the net sale price due to these legislative shifts. Compliance is no longer a back-office task; it’s the foundation of a successful exit.

Why Timing is the Most Critical Factor in 2026

The financial difference between a disposal finalized before or after the 6 April 2026 threshold is stark. For those qualifying for Business Asset Disposal Relief, the rate is now 18%, which represents a notable increase from previous years. This has created a market bottleneck as a high volume of sellers attempts to conclude transactions simultaneously. The valuation of dental goodwill faces a distinct tax cliff-edge as the 2026 reforms recalibrate the balance between capital growth and immediate tax liabilities. Managing this transition requires a steady hand and a clear understanding of the evolving fiscal landscape.

Navigating Capital Gains Tax and the 2026 BADR Reforms

For many practitioners, Capital Gains Tax (CGT) is the single largest fiscal liability they’ll encounter during their professional lifecycle. It applies to the gain, or profit, realized when you dispose of business assets. This includes the practice’s goodwill, patient lists, and clinical equipment. When considering the selling a dental practice process, the 2026 landscape introduces a higher baseline for these liabilities. The tax is essentially a levy on the growth of your investment, but the rate at which it’s collected depends heavily on your personal income and the availability of specific reliefs.

Understanding Business Asset Disposal Relief (BADR)

The most significant shift involves the recalibration of Business Asset Disposal Relief. For disposals occurring on or after 6 April 2026, the CGT rate for qualifying gains under BADR is 18%, a sharp increase from the 10% rate that defined the previous era of business exits. To qualify for this lower rate, you must typically have owned the business for at least two years and ensure the practice meets the criteria of a trading company. The £1 million lifetime limit remains a critical threshold; gains exceeding this amount are taxed at the standard higher CGT rate of 24% for additional rate taxpayers. We’ve found that many owners are unaware that this limit is an aggregate of all business disposals throughout their career, not just the final sale of their primary practice.

The Impact of CGT Rate Alignment

Your personal income bracket directly influences your capital tax exposure. Because the gain from a practice sale is added to your other taxable income for the year, most dental owners will find themselves firmly within the 24% CGT bracket for any non-relievable gains. Consider a scenario where a practitioner realizes a £500,000 gain. Under the 2024 regime, qualifying for BADR resulted in a £50,000 tax bill. In 2026, that same qualifying gain incurs a liability of £90,000, representing an 80% increase in the tax paid on the same level of capital growth. This fiscal compression highlights why individualised advice is paramount. The role of the Annual Exempt Amount, which stands at £3,000 for the 2026/27 tax year, provides only a modest buffer against these larger movements.

Managing these shifts requires a composed and strategic approach to ensure you don’t overpay. We recommend consulting a dental tax specialist early in the process to model these scenarios against your specific income profile. Our team focuses on identifying the most efficient pathways to preserve your equity amidst these shifting statutory reliefs, ensuring that your exit strategy remains robust and your financial future secure.

Structural Considerations: Asset Sales vs. Share Sales

The choice between a share sale and an asset disposal is often the most significant point of negotiation in a practice transition. While both pathways lead to a change in ownership, their fiscal outcomes vary considerably. When we analyze the selling a dental practice tax implications 2026, the structural choice determines whether you face a single layer of taxation or a more complex, multi-stage liability. Buyers typically favor asset purchases because they can select specific components of the business while leaving behind historical legal or financial liabilities. Sellers, however, generally find share sales more advantageous for capital retention.

A primary risk in asset-based disposals within a limited company is the potential for “double taxation.” In this scenario, the company first pays Corporation Tax on the profits from the sale of its assets. As of April 2026, the main rate of Corporation Tax remains 25% for companies with profits exceeding £250,000. Once the company has settled its bill, the individual owner must then pay additional tax to extract the remaining cash, either as a dividend or through a formal liquidation. This layered approach can significantly erode the equity you’ve built over decades of clinical practice.

The Share Sale Advantage for Limited Companies

For those operating through a limited company, selling the shares usually provides a cleaner exit. This structure allows the seller to access Business Asset Disposal Relief (BADR) on the entirety of the gain, provided the qualifying conditions are met. However, preparing for a share sale requires meticulous “cleaning” of the balance sheet. We often advise clients to begin this process at least 24 months in advance. This involves identifying and removing non-trading assets, such as personal vehicles or investment properties, which could jeopardize the company’s “trading status” in the eyes of HMRC. Managing excess cash and pre-sale dividends is equally vital; pulling too much cash out immediately before a sale could inadvertently trigger higher-rate income tax charges rather than the preferred capital gains treatment.

Asset Sales: Goodwill and Equipment

In an asset sale, the transaction is broken down into its constituent parts, such as goodwill, equipment, and premises. HMRC treats the sale of dental goodwill as a capital asset, which generally qualifies for capital gains treatment. However, the sale of clinical equipment often triggers “balancing charges.” If you’ve previously claimed full capital allowances on expensive dental chairs or digital imaging systems, selling those items may require you to pay back some of that tax relief to HMRC. Additionally, the dental practice premises require careful handling. If the building is owned personally but used by your company, the tax implications differ significantly from property owned within the corporate shell. We focus on balancing these competing interests to ensure the final contract reflects your long-term financial goals.

Mitigating Liabilities through Proactive Pre-Sale Tax Planning

The complexity of selling a dental practice tax implications 2026 requires more than a reactive approach; it demands a multi-year lead time. We typically advise practitioners to begin their fiscal preparations at least 24 months before their target disposal date. This window allows for the restructuring of income and assets without the urgency that can lead to oversight. One of the most effective levers available is the strategic use of pension contributions. By allocating profits into a pension fund prior to the sale, you can effectively lower your adjusted net income. This shift is critical because non-relievable capital gains are added to your annual income; staying within a lower threshold can significantly reduce the overall percentage HMRC claims from the transaction.

Individualized planning also involves the intelligent use of spouse allowances and share transfers. Transferring a portion of the business to a spouse well in advance of a sale can effectively double your tax-free annual exempt amount and, more importantly, allow for the utilization of two sets of basic rate bands or Business Asset Disposal Relief lifetime limits. This approach requires careful execution to satisfy HMRC’s “settlement” rules, but when integrated into a broader framework of expert tax advice in the UK, it becomes a cornerstone of capital preservation. We focus on ensuring these transfers are commercial and documented to withstand any future scrutiny.

Managing Goodwill and Practice Premises

Separating the freehold property from the clinical business is a nuanced decision that affects both immediate tax and long-term income. If you own the surgery personally and charge the company rent, you may inadvertently restrict your ability to claim the full 18% BADR rate on the property portion of the sale. Conversely, keeping the property within the company shell might lead to higher corporation tax liabilities upon disposal. For disposals in the 2026/27 tax year, commercial property gains that do not qualify for specific business reliefs are taxed at the prevailing standard CGT rates of 18% or 24% depending on the seller’s total income. We help our clients weigh these options to ensure the freehold doesn’t become a tax anchor on the business sale.

Succession and Inheritance Tax (IHT) Integration

A practice sale often transforms a business asset into a cash asset, which has significant implications for Inheritance Tax. While your practice may currently qualify for Business Property Relief (BPR), effectively exempting its value from IHT, cash proceeds do not share this status. Utilizing the “seven-year rule” for gifting or establishing trusts can help move wealth out of your estate while maintaining a level of control or income. This holistic view ensures that the liquidity generated by your exit serves your family’s future rather than just settling a current tax bill. To ensure your exit strategy is as efficient as possible, our dental tax specialists can provide a tailored feasibility study of your current structure.

Securing Your Financial Future with Specialist Dental Tax Advice

Finalizing the disposal of a clinical practice marks the conclusion of a professional chapter and the commencement of a new financial reality. Given the specific selling a dental practice tax implications 2026, the guidance of a small business accountant with deep-seated dental expertise is not merely a convenience; it’s a prerequisite for capital security. A generic approach often fails to account for the intricate revenue streams that define modern dentistry, such as the balance between private fees and Units of Dental Activity (UDA) or the complex tax status of associates.

At Davis & Co LLP, we provide a composed partnership that extends beyond simple compliance. We recognize that the months leading up to a sale are often fraught with administrative pressure. Our role is to act as a stabilizing force, ensuring that your financial data is presented with the intellectual rigour required to satisfy both buyers and HMRC. This coordinated effort requires seamless communication between your accountants, legal representatives, and brokers. When these professional pillars are aligned, the transition from practice owner to private wealth holder is managed with the discretion and precision your legacy deserves.

Why Specialist Dental Accountants are Essential

Niche dental tax specialists understand the nuances of associate-led revenue models and the specific VAT exemptions applicable to health-related services. We’ve found that HMRC often applies a high level of scrutiny to dental goodwill valuations and the treatment of capital allowances. Our experience in negotiating these technical enquiries provides our clients with a significant advantage. By speaking the language of both the clinician and the tax inspector, we ensure that the selling a dental practice tax implications 2026 are managed with professional gravitas, protecting your proceeds from unnecessary erosion.

Your 2026 Exit Strategy Starts Today

The first step toward a successful transition is a comprehensive tax liability forecast. This document provides a clear view of your projected net proceeds after CGT, Corporation Tax, and any relevant reliefs have been applied. It allows you to make informed decisions about your exit date and the structure of your deal. We invite you to engage with our team to begin this modelling process, ensuring that every variable is considered well before the final contracts are drawn. Our approach is steady and measured, reflecting our commitment to your long-term stability.

Contact Davis & Co LLP for a specialist dental tax consultation to secure your financial future and navigate the 2026 landscape with confidence.

Securing Your Legacy in a Shifting Fiscal Environment

The transition from clinical ownership to a successful exit requires a delicate balance of timing, structural precision, and proactive planning. We’ve explored how the 2026 landscape demands a 24-month lead time to navigate the 18% BADR rate and the complexities of share sale “cleaning.” By addressing these factors early, you can mitigate the risk of double taxation and ensure your equity is preserved. Understanding the selling a dental practice tax implications 2026 isn’t just about compliance; it’s about maximizing the value of your career’s work.

As Chartered Certified Accountants since 1901, Davis & Co LLP provides the specialist niche expertise in dental tax compliance necessary for such high-stakes transactions. We pride ourselves on a discreet and professional strategic partnership that puts your long-term financial security first. Consult our specialist dental tax advisors for an exit strategy review to begin your journey toward a secure and rewarding retirement. Your professional legacy deserves a planned and profitable conclusion.

Frequently Asked Questions

What is the current rate of Capital Gains Tax for dental practice sales?

For disposals on or after 6 April 2026, the standard Capital Gains Tax rates are 18% for basic rate taxpayers and 24% for those in higher or additional rate bands. These rates apply to the profit realized above your annual exempt amount, which is £3,000 for the 2026/27 fiscal year. Calculating your specific liability requires a clear understanding of your total taxable income for the year, as the gain is layered on top of your existing earnings.

Will Business Asset Disposal Relief be abolished in 2026?

Business Asset Disposal Relief (BADR) remains available in 2026, although the rate for qualifying gains increases to 18% for disposals occurring on or after 6 April 2026. The lifetime limit for these qualifying gains is currently maintained at £1 million. While the relief hasn’t been abolished, the increase from the previous 10% rate significantly alters the net proceeds for many sellers. Early strategic planning is essential to manage this transition effectively.

How is dental goodwill taxed when I sell my practice?

Dental goodwill is treated as a capital asset by HMRC and is typically the largest component of a practice’s valuation. When analyzing the selling a dental practice tax implications 2026, it’s important to note that gains from goodwill usually qualify for capital gains treatment rather than being taxed as income. Because goodwill represents the intangible value of patient loyalty and brand reputation, its valuation must be robustly supported to withstand potential scrutiny during the disposal process.

Can I reduce my tax bill by gifting shares to my spouse before a sale?

Gifting shares to a spouse before a sale can be a highly effective way to utilize two sets of annual exempt amounts and basic rate tax bands. This strategy can effectively double the threshold for lower tax rates, provided the transfer is genuine and occurs well before the transaction to satisfy HMRC’s settlement rules. We recommend implementing such transfers as part of a long-term strategy rather than an immediate pre-sale adjustment to ensure full compliance.

Does it matter if I sell my dental practice as an asset sale or a share sale?

The choice between an asset sale and a share sale has a profound impact on your final tax liability. A share sale generally allows for a single layer of Capital Gains Tax and easier access to BADR on the entire proceeds. Conversely, an asset sale within a limited company may trigger Corporation Tax on the asset growth followed by personal tax on the extraction of those funds. This structural decision often dictates the overall financial success of the transition.

What happens to my dental practice premises from a tax perspective upon sale?

The tax treatment of your premises depends on whether the property is owned personally or within your limited company. If you own the surgery personally but charge your company a market rent, your eligibility for Business Asset Disposal Relief on the property gain may be restricted. For 2026 disposals, gains on commercial property that don’t qualify for specific reliefs are subject to the standard CGT rates of 18% or 24% based on your income profile.

Should I bring my dental practice sale forward to avoid the 2026 tax changes?

Deciding whether to accelerate a sale to avoid the 2026 tax increases requires a careful comparison between tax savings and practice valuation. While completing a sale before 6 April 2026 could secure a lower tax rate on relievable gains, rushing a disposal might result in a lower EBITDA multiple or unfavorable terms. We focus on modeling the selling a dental practice tax implications 2026 individually to determine if the potential tax saving outweighs the benefits of a more measured exit.