Could your current approach to tax deductions be the very thing inviting HMRC scrutiny rather than protecting your bottom line? For many of the 4.57 million self-employed workers in Britain, the process of identifying allowable expenses for self employed uk remains a source of persistent anxiety. You likely feel the pressure of the 6 April 2026 deadline for Making Tax Digital, which requires those with a qualifying income over £50,000 to transition to quarterly digital reporting. It’s a significant shift that demands more than just basic bookkeeping; it requires a disciplined, strategic mindset to ensure every claim is defensible.

We understand that the nuances of dual-use assets and the “wholly and exclusively” principle can often feel like a moving target. This guide is designed to provide you with the clarity needed to navigate these regulations with confidence, ensuring you maximise tax efficiency without compromising your professional compliance. We’ll examine the specific 2026 rates, such as the 55p simplified mileage allowance, and offer a logical framework for categorising complex deductions. By the end of this discussion, you’ll have a clear roadmap to manage your professional outgoings with the precision and rigour that your business deserves.

Key Takeaways

- Define the “wholly and exclusively” principle as the foundation for all legitimate business claims to ensure full compliance with HMRC standards.

- Identify the specific categories of allowable expenses for self employed uk, from administrative overheads to professional fees, to ensure no valid deduction is overlooked.

- Gain clarity on apportioning dual-use costs, such as home office utilities and travel, using either actual costs or HMRC’s simplified flat rates for 2026.

- Establish robust digital record-keeping practices now to seamlessly transition to the Making Tax Digital (MTD) quarterly reporting requirements effective from April 2026.

- Learn how a strategic, professional approach to expense management can be integrated into wider international tax planning to protect and grow your commercial interests.

The ‘Wholly and Exclusively’ Principle: Navigating HMRC’s Core Rule

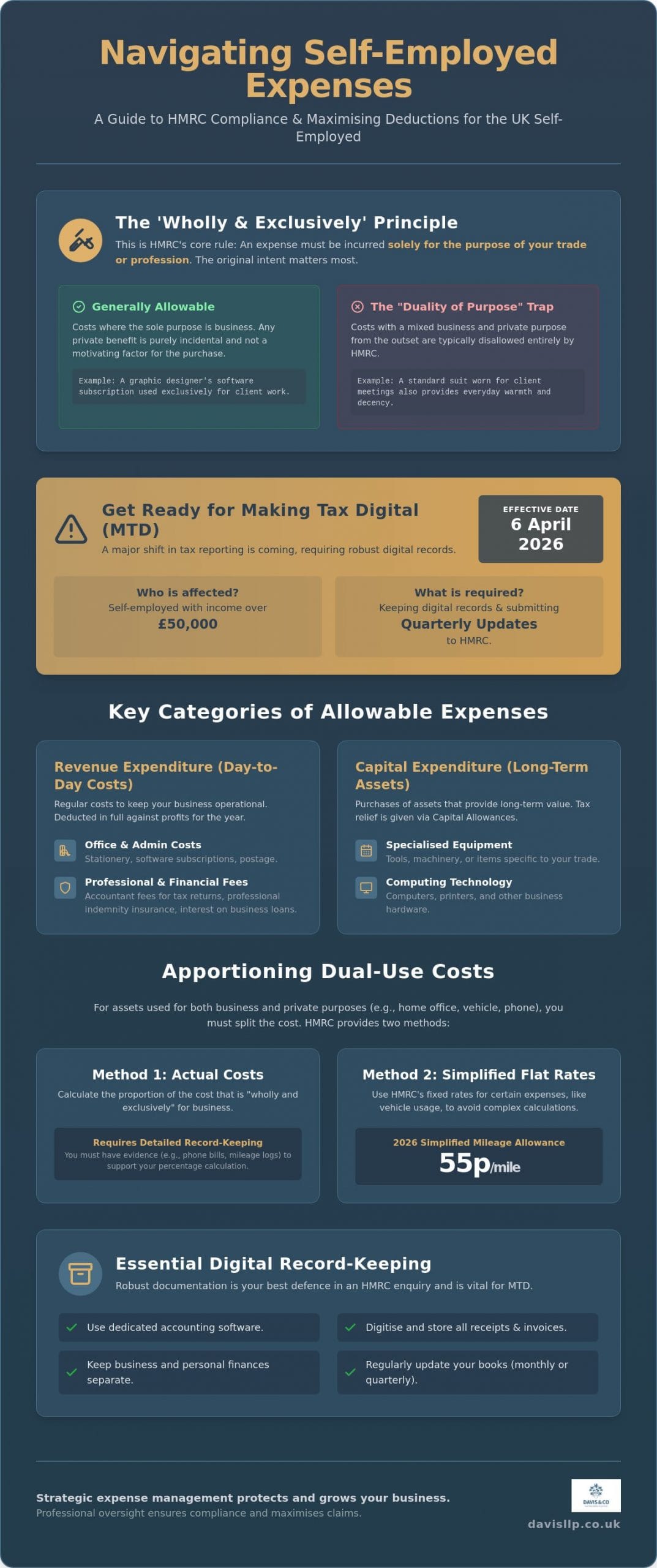

At the heart of managing allowable expenses for self employed uk lies a single, uncompromising standard: the “wholly and exclusively” principle. This legal requirement dictates that for a cost to be deductible, its sole purpose must be the advancement of your trade. While the concept appears straightforward, its application within the broader framework of the UK tax system involves subtle nuances that often determine the outcome of an HMRC enquiry. It’s not merely about whether an item is used for work; it’s about the primary motivation behind the expenditure.

Differentiating between the intent and the result is vital. HMRC focuses on the purpose of the expenditure at the time you incurred it. If a private benefit arises as a purely incidental consequence of a business-driven decision, the expense may still be allowable. However, if the motivation is mixed from the outset, the entire deduction risks being disqualified. Securing expert tax advice in the UK is often the most prudent way to interpret these ambiguous costs, especially as digital reporting standards tighten in 2026.

Revenue vs. Capital Expenditure

Understanding the distinction between revenue and capital expenditure is essential for accurate financial reporting. Revenue expenditure refers to the regular, day-to-day costs required to keep your business operational, such as professional indemnity insurance or office supplies. These are generally deducted in full against your profits for the year. Conversely, capital expenditure involves the acquisition of assets that provide long-term value, such as specialized dental equipment or high-end computing technology. Under the 2026 tax regime, these items are typically handled through capital allowances rather than direct expense deductions, requiring a different method of accounting to maintain compliance.

The Duality of Purpose Trap

The “duality of purpose” remains a primary trigger for HMRC scrutiny. A classic example is everyday clothing; even if you only wear a specific suit for client meetings, it serves the dual purpose of providing basic warmth and decency, making it non-deductible. HMRC’s stance is firm: if a cost serves both a personal and professional need without a clear, identifiable split, it fails the test. We advise clients to use a “reasonable and defensible” basis for apportionment. For instance, if you use a mobile phone for both business and personal calls, you must calculate the business percentage based on actual usage records. This level of detail is increasingly important as allowable expenses for self employed uk come under greater AI-driven analysis by tax authorities.

Operational Expenditure: A Detailed Breakdown of Allowable Business Costs

Managing the daily outgoings of a professional practice requires a granular understanding of which costs qualify for tax relief. While the previous section established the legal foundation of HMRC’s ‘wholly and exclusively’ principle, the practical application often presents more complexity. For those managing allowable expenses for self employed uk, operational expenditure represents the most frequent category of claims, ranging from the mundane costs of stationery to the sophisticated digital infrastructure required in a modern commercial environment.

Professional and Financial Costs

Professional fees are often among the most significant deductions for high-earning individuals. It’s a common misconception that administrative support is the only claimable service. In reality, the fees paid to your small business accountant for preparing your annual accounts and tax returns are fully allowable. This ensures that the cost of maintaining compliance doesn’t unfairly erode your profitability. Beyond accounting, you can also claim for professional indemnity insurance premiums and interest on business loans. However, you should distinguish between personal and business debt; interest on a mortgage for your primary residence is handled differently than interest on a dedicated business credit card or overdraft used to manage liquidity.

Membership fees to professional bodies also fall into this category, provided the organisation appears on HMRC’s approved list. This is particularly relevant for specialists, such as dental professionals, who must maintain specific registrations to practice. If you find your financial structure becoming increasingly complex, our team can provide the strategic management accounts necessary to track these outgoings with precision.

Marketing and Client Acquisition

Strategic reinvestment into your brand is essential for long-term growth. Most costs associated with advertising your services are allowable, including website hosting, SEO services, and lead generation software. The distinction becomes sharper when considering client interaction. While the cost of a LinkedIn advertisement is deductible, the cost of hosting a client for a meal is generally not. HMRC classifies this as business entertainment, which is strictly non-allowable, regardless of its commercial necessity. To maintain a robust audit trail, it’s vital to separate these growth-focused investments from discretionary spending that carries a dual purpose.

Finally, the management of stock and raw materials is a critical component of tax efficiency. If your business involves physical goods, you can deduct the cost of sales, which includes the purchase of stock and the direct costs of production. By accurately tracking these figures, you ensure that your taxable profit reflects your actual commercial success rather than an inflated figure based on gross turnover.

Complex Deductions: Home Offices, Travel, and Dual-Purpose Assets

Identifying clear-cut business costs is relatively straightforward; however, the challenge for many professionals lies in managing dual-purpose assets. These are items or services that serve both your commercial operations and your personal life. When calculating allowable expenses for self employed uk, the burden of proof rests with you to demonstrate a logical and consistent basis for apportionment. HMRC’s scrutiny often intensifies in these areas, particularly as digital records under Making Tax Digital provide tax authorities with more granular visibility into your spending patterns.

The Home Office Calculation

If you operate your business from a residential property, you have two primary methods for claiming relief. The first involves calculating actual costs by apportioning household bills such as heating, lighting, council tax, and rent based on the number of rooms used or the time spent working. While this can yield higher deductions for those with significant overheads, it requires meticulous record-keeping. We often advise caution when designating a room as “exclusively” for business; doing so can inadvertently forfeit your Private Residence Relief, potentially leading to Capital Gains Tax liabilities when you sell the property.

Alternatively, many professionals opt for the simplified expenses flat rate for the 2026/27 tax year. According to UK Government guidance on allowable expenses, these rates are tiered based on your monthly hours:

- 25 to 50 hours: £10 per month

- 51 to 100 hours: £18 per month

- 101 hours or more: £26 per month

Travel, Mileage, and Subsistence

Vehicle expenses represent another area where the choice between actual costs and simplified rates is critical. For the 2026/27 tax year, the simplified mileage allowance stands at 55p per mile for the first 10,000 business miles and 25p thereafter. This rate is designed to cover fuel, insurance, and depreciation. If you’ve transitioned to an electric vehicle (EV), you may find that claiming capital allowances on the purchase price, combined with actual charging costs, offers a more tax-efficient outcome than the standard mileage rate.

It’s vital to distinguish between a business journey and a commute. Travel to a “permanent workplace” is generally non-deductible. A business journey must be to a temporary location or between two places of business. Similarly, subsistence claims for food and drink are only permissible during “itinerant” work or overnight business travel. Finally, remember that training costs are only allowable when they refresh or update existing skills; fees for acquiring entirely new skills are often viewed as capital investment in your personal “human capital” rather than a revenue expense for your current trade.

Compliance and Documentation: Mitigating Risk in a Digital Tax Landscape

Establishing a robust evidence trail for allowable expenses for self employed uk is no longer merely a recommendation; it is a structural necessity. As we approach the 6 April 2026 mandate for Making Tax Digital for Income Tax Self Assessment (MTD for ITSA), the margin for error in record-keeping is narrowing. For individuals with a qualifying gross income exceeding £50,000, the transition to quarterly digital updates requires a move away from retrospective annual accounting. This change demands that every transaction is captured digitally at the point of expenditure, ensuring that your financial data remains accurate and accessible throughout the tax year.

Digital Record-Keeping Requirements

The era of maintaining physical folders of receipts or disconnected spreadsheets is effectively ending. Under the new regulations, HMRC expects records to be kept in MTD-compliant software that can communicate directly with their systems. Digital imaging and cloud storage have become essential tools, allowing you to attach digital copies of invoices to specific transactions instantly. This creates a permanent, searchable archive that simplifies the reconciliation process. At Davis & Co LLP, we work closely with our clients to implement these digital workflows, ensuring that the submission process is streamlined and that all potential deductions are identified in real-time.

HMRC Enquiries and Investigations

HMRC increasingly utilises sophisticated AI-driven tools to identify anomalies in self-assessment returns. Common red flags include expense claims that appear disproportionately high relative to turnover or significant fluctuations in specific cost categories compared to previous years. The strength of your defence during an enquiry regarding allowable expenses for self employed uk depends almost entirely on the quality of your contemporaneous records. These are documents created at the time the expense was incurred, providing clear evidence of the business purpose. Without such documentation, even legitimate claims can be disallowed, leading to potential penalties and interest charges.

It is also vital to remain vigilant against aggressive tax avoidance schemes that promise unrealistic savings. We encourage all professionals to review the latest HMRC tax warnings to ensure their financial planning remains within the bounds of robust professional compliance. If you require assistance in modernising your financial systems, our personal tax services provide the strategic oversight necessary to ensure your digital transition is both seamless and compliant.

Finally, you must adhere to strict retention periods. You are legally required to keep all business records for at least five years after the 31 January submission deadline of the relevant tax year. This discipline ensures that you can provide the necessary evidence should HMRC initiate a formal enquiry several years after a return was filed. Maintaining this level of organisation protects your business from the financial and reputational risks associated with non-compliance.

Strategic Tax Efficiency: How Professional Oversight Maximises Allowable Claims

While software can automate the entry of data, it cannot replace the nuanced judgment required to integrate allowable expenses for self employed uk into a broader wealth preservation strategy. True tax efficiency isn’t found in isolated claims but in a cohesive plan that considers your entire professional and personal profile. This requires foresight. By shifting the focus from simple compliance to proactive oversight, we ensure that every deduction serves a larger commercial purpose and withstands the rigour of HMRC’s 2026 digital standards.

Sector-Specific Expense Optimisation

Specialist sectors demand a more granular approach to deduction. Dental professionals, for instance, must manage significant outgoings related to laboratory fees, associate payments, and the maintenance of clinical equipment. These require precise categorisation to ensure they are handled as revenue expenses rather than capital investments where appropriate. Similarly, property investors must be particularly cautious when distinguishing between routine repairs, which are allowable revenue expenses, and property improvements, which are capital in nature and handled through different tax mechanisms.

High-earning consultants working across borders face even more complex challenges. Managing cross-border travel and dual-residency expenses requires a deep understanding of international treaties. Integrating these allowable expenses for self employed uk into a holistic international tax planning strategy is essential to avoid double taxation and to protect your global commercial interests. We focus on these highly individualised details to ensure your tax position is as efficient as it is compliant.

The Davis & Co LLP Approach

Our approach transcends basic bookkeeping. We act as a strategic partner, providing regular management accounts that allow you to track your expense ratios throughout the year. This real-time visibility means we can identify opportunities for tax savings long before the January deadline. By appointing us through a 64-8 authorisation, you grant us the authority to act as your professional agent. This significantly reduces your administrative burden and ensures that all communications with HMRC are handled with professional gravitas and technical precision.

We invite you to contact Davis & Co LLP for a comprehensive strategic tax review. By aligning your expense management with your broader business growth goals, we help you move from basic compliance to a position of secure, long-term wealth preservation. Our history of success in handling complex tax matters ensures that your professional practice is well-advised and prepared for the evolving regulatory landscape of 2026.

Securing Your Financial Future Through Professional Tax Oversight

Navigating the evolving landscape of allowable expenses for self employed uk requires a shift from passive record-keeping to proactive financial management. As the April 2026 Making Tax Digital mandate approaches, the precision of your digital audit trail becomes as important as the deductions themselves. By mastering the “wholly and exclusively” principle and correctly apportioning complex dual-use costs, you protect your professional interests from unnecessary HMRC scrutiny while ensuring your tax liability remains at its legal minimum.

We believe that tax efficiency is most effective when it’s integrated into a broader commercial strategy. Since 1901, Davis & Co LLP has served as a trusted partner for high-earning individuals, offering specialized dental and international tax expertise. Our status as Chartered Certified Accountants provides the composed, reassuring authority you need to navigate these regulatory shifts with complete confidence. We invite you to Contact Davis & Co LLP for Strategic Tax Advice to refine your approach and secure your commercial legacy. You don’t have to manage these complexities alone; professional partnership ensures your business remains both compliant and highly efficient.

Frequently Asked Questions

What is the £1,000 trading allowance and can I use it with expenses?

You cannot claim the £1,000 trading allowance alongside actual business expenses. This allowance is designed for individuals with very low overheads; if your gross income exceeds £1,000, you must choose between the flat-rate deduction or your actual costs. For many professionals, tracking allowable expenses for self employed uk provides a much higher level of tax relief than the simplified allowance.

Can I claim for my gym membership or health insurance if I am self-employed?

Gym memberships are almost never allowable because they fail the “wholly and exclusively” test. HMRC views physical fitness as a personal benefit, even if you believe it’s necessary for your professional performance. Similarly, private health insurance for a solo self-employed individual is generally considered a personal expense. It doesn’t qualify for tax relief against your trading profits as it serves a dual purpose of personal well-being.

How do I calculate the business use percentage of my mobile phone bill?

You should calculate your deduction by identifying the professional proportion of your total usage. This involves reviewing your itemised statements over a representative period to determine the ratio of business calls and data versus personal use. Once you establish a consistent percentage, you can apply it to your monthly bills. We recommend keeping these workings as part of your digital records to justify the apportionment to HMRC.

Are training courses for a completely new career path tax-deductible?

Training courses designed to launch a completely new career path are not tax-deductible. HMRC categorises these costs as capital investment in your personal skills rather than revenue expenditure. You can only claim for training that updates, refreshes, or enhances existing skills used within your current trade. If the course is intended to help you start a fundamentally different business, the fees won’t be allowable against your current profits.

Can I claim for clothing if it has my business logo on it?

You can claim for clothing that features a prominent, permanent business logo, as this qualifies the garment as a uniform or promotional attire. While standard business suits are strictly non-deductible because they can be worn for personal occasions, branded workwear or specialized protective clothing is allowable. This distinction is a vital part of managing allowable expenses for self employed uk without triggering an enquiry into dual-purpose items.

What happens if I lose a receipt but the expense is legitimate?

If you lose a receipt, you can sometimes use bank or credit card statements as secondary evidence of the transaction. However, HMRC expects you to maintain primary records for all claims. With the transition to Making Tax Digital in 2026, we strongly advise using compliant software to capture digital images of receipts at the point of purchase. Relying on bank statements alone is a higher-risk strategy during a formal compliance check.

Are entertaining clients or potential leads an allowable expense in 2026?

Entertaining clients, suppliers, or potential leads remains strictly non-allowable under current UK tax law. Regardless of how essential a business lunch or event may be for securing a contract, HMRC does not permit tax relief on hospitality. These costs must be funded from your post-tax income. It’s important to keep these expenses separate from your allowable marketing costs, such as advertising or digital SEO services, to maintain compliance.

Can I claim for my commute from home to my regular office?

You cannot claim for the cost of commuting between your home and a permanent place of work. HMRC defines this journey as private travel, regardless of the distance or time involved. You can only claim travel expenses for journeys to temporary locations or between two different places of business. Understanding the specific definition of a “permanent workplace” is essential for ensuring your travel and mileage claims are defensible under 2026 regulations.