For many UK families, the threshold for the High Income Child Benefit Charge remains a source of frustration rather than a mark of success. The upcoming hmrc child benefit changes 2025 represent a pivotal shift in how the government assesses household eligibility and tax liabilities. We recognise that the current system often feels unfairly weighted against single-income households, particularly when you’re tasked with the intricate calculation of adjusted net income to avoid an unexpected Self Assessment bill.

Our objective is to provide the clarity you require to manage these transitions effectively. You’ll gain a precise understanding of the new rates taking effect from 6 April 2025 and learn how to employ bespoke tax planning to mitigate the impact of the HICBC. We’ll also address the essential role of National Insurance credits in protecting the non-earning partner’s state pension. This strategic overview ensures your family’s finances are both compliant and optimised for the year ahead.

Key Takeaways

- Identify the new weekly rates for eldest and additional children to accurately forecast your household income following the hmrc child benefit changes 2025.

- Gain clarity on the High Income Child Benefit Charge (HICBC) mechanics, specifically the £60,000 to £80,000 taper and the 1% charge for every £200 earned above the threshold.

- Prepare for the strategic shift towards a household-based assessment system, aimed at resolving the long-standing inequities of the current individual-earner model.

- Learn how to employ “Pension Power” by using SIPP or workplace contributions to legitimately lower your adjusted net income and protect your benefit eligibility.

- Understand the value of a bespoke tax review to ensure your Self Assessment is both compliant with HMRC regulations and optimised for your family’s unique financial position.

The 2025 Child Benefit Landscape: New Rates and Thresholds

From 6 April 2025, the UK’s fiscal framework for families will see a statutory adjustment. These hmrc child benefit changes 2025 are designed to align support with the evolving economic environment, particularly the inflationary pressures that have impacted household budgets since 2023. At Davis LLP, we recognise that these adjustments are not merely administrative; they represent a strategic component of a family’s broader financial planning and long-term security.

The uplift serves a dual purpose. While the immediate financial injection is the most visible aspect, the underlying administrative link to National Insurance records is equally significant. For a parent who chooses to stay at home or work reduced hours, claiming the benefit ensures they continue to accrue National Insurance credits. This protects their eligibility for the State Pension, a detail that requires careful foresight. Considering the Child Benefit history in the UK, the payment has consistently evolved from its post-war origins to its current role as a targeted yet essential pillar of the welfare state.

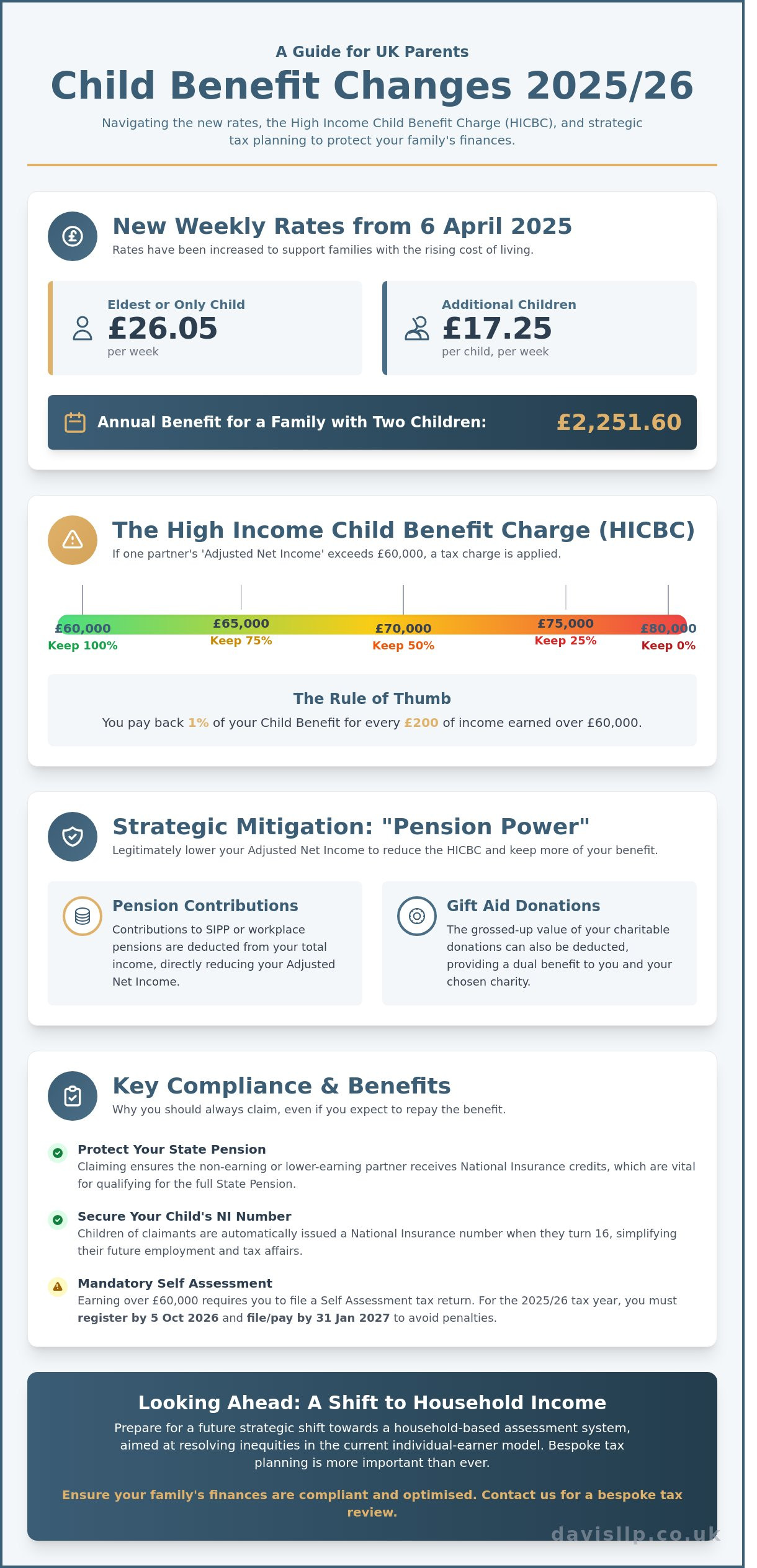

Child Benefit Rates for the 2025/26 Tax Year

The new rates reflect a calculated increase to support the rising costs of child-rearing. For the 2025/26 tax year, the weekly amounts are set as follows:

- Eldest or only child: £26.05 per week.

- Additional children: £17.25 per child, per week.

For a standard family with two children, this creates an annualised benefit value of £2,251.60. This represents a tangible increase from previous years, providing a more robust buffer against the cost of living. We advise clients to view this as a guaranteed component of their liquidity management, regardless of their wider investment portfolio or commercial interests.

Eligibility and the “Earning Over the Threshold” Warning

Eligibility remains broad, yet the High Income Child Benefit Charge (HICBC) continues to apply to those with an individual income exceeding the current statutory limits. Even if your earnings necessitate a partial or full repayment of the benefit through Self Assessment, we recommend maintaining the claim. Opting out of the payment while keeping the claim active ensures the National Insurance credits remain intact. You’ll also ensure your child receives a National Insurance number automatically when they turn 16. It’s also vital to consider how these rates interact with the Benefit Cap, which limits the total amount of support a household can receive. Our team often finds that bespoke tax planning can mitigate the impact of the HICBC, ensuring your family retains the maximum possible value from the hmrc child benefit changes 2025.

High Income Child Benefit Charge (HICBC) in 2025

Understanding the hmrc child benefit changes 2025 requires a precise focus on the High Income Child Benefit Charge. Following the threshold adjustments implemented in 2024, the 2025/26 tax year operates under a revised taper zone that starts at £60,000 and concludes at £80,000. This range is critical for middle and high-earning households to monitor. HMRC applies a tax charge of 1% for every £200 of income earned above the £60,000 floor. This mechanism ensures a gradual reduction in the net value of the benefit rather than an immediate loss. Once a single parent or partner reaches the £80,000 “cliff edge,” the charge equals the total benefit received, effectively clawing back the full amount. Referencing the Official 2025/26 Child Benefit Rates provides the necessary baseline for calculating these figures against your projected earnings.

Calculating Your Adjusted Net Income

Your Adjusted Net Income is the only figure HMRC considers when determining HICBC liability. It represents your total taxable income before personal allowances, but after specific statutory deductions. You can reduce this figure through grossed-up pension contributions and Gift Aid donations. A common oversight involves failing to account for interest earned on savings or dividend income, which can push an individual unexpectedly into the taper zone. Precise calculation is essential to avoid underpayment. We find that bespoke tax reviews often uncover opportunities to manage this figure through strategic financial planning.

The Self Assessment Requirement

Exceeding the £60,000 threshold triggers a mandatory requirement to file a Self Assessment tax return, even if you’re taxed via PAYE for your primary salary. For the 2025/26 tax year, you must register with HMRC by 5 October 2026. The deadline for filing and paying the charge is 31 January 2027. HMRC’s penalty regime for “failure to notify” is strict. Fines can reach 30% of the tax due for non-deliberate errors, and significantly more if the omission is viewed as intentional. Maintaining an organised record of all income sources ensures you remain compliant with these evolving statutory demands.

The Shift to Household Income: What Parents Must Anticipate

The government’s commitment to reforming the High Income Child Benefit Charge (HICBC) represents a fundamental pivot in UK tax policy. By April 2026, the assessment will transition from an individual earner model to a household-based system. This change seeks to rectify the “Single Parent Trap”. Under current rules, a single parent earning £61,000 pays the charge, while a couple each earning £59,000, a combined £118,000, remains exempt. It’s a disparity that has long undermined the perceived fairness of the system.

While the full transition is slated for 2026, the hmrc child benefit changes 2025 act as a crucial preparatory phase. We advise clients to view 2025 as the period for data alignment. HMRC faces a significant administrative challenge in linking household records. The UK tax system is historically built on individual accountability. You’ll need to be proactive. Understanding how the hmrc child benefit changes 2025 impact your specific filing requirements is the first step toward long-term compliance.

Individual vs. Household Assessment

The move to household assessment will likely bring many dual-earner families into the scope of the charge for the first time. If both partners earn £50,000, they currently escape the HICBC. Under a household model, their combined £100,000 would almost certainly trigger a full clawback. We recommend couples on the border of these thresholds review their total income now. Strategic use of pension contributions or gift aid can reduce your adjusted net income, potentially keeping the household below the new thresholds once they’re finalised.

Preparing for Future Compliance

Organising your financial affairs requires a pragmatic approach to record-keeping. HMRC will require clarity on who the Lead Claimant is, particularly for the purposes of National Insurance credits. These credits are vital for your future state pension. Consider these steps to ensure your household is ready for the 2026 shift:

- Audit the adjusted net income for both residents in the household to identify potential future liabilities.

- Review any Opt-Out decisions made when the threshold was £50,000; the new 2024/25 threshold of £60,000 makes many families eligible again.

- Keep precise records of any salary sacrifice schemes that affect your gross pay.

- Ensure both partners’ addresses are correctly linked with HMRC to avoid administrative delays.

Effective planning ensures that the shift to household metrics doesn’t compromise your family’s long-term financial stability. We anticipate further technical guidance from HMRC as the 2026 implementation date approaches, making 2025 a vital year for bespoke financial review.

Strategic Mitigation: How to Keep More of Your Child Benefit

Managing the impact of the High Income Child Benefit Charge (HICBC) requires a proactive approach to your Adjusted Net Income (ANI). While the threshold rose to £60,000 in April 2024, many households still find themselves within the taper zone where benefit is gradually clawed back. By implementing specific financial adjustments, you can effectively lower your ANI and preserve your family’s entitlement. These hmrc child benefit changes 2025 reward those who take a structured, long-term view of their taxable income rather than simply accepting the default assessment.

The Pension Contribution Strategy

The most effective tool for mitigation is the strategic use of pension contributions. HMRC calculates your ANI after deducting gross pension contributions. For instance, consider a parent earning £65,000 per annum. Under current rules, they’d lose 50% of their Child Benefit through the tax charge. By making a £5,000 gross contribution into a SIPP or a workplace scheme, their ANI drops to £60,000. This action secures 100% of their Child Benefit. For a family with two children, this preserves approximately £2,212 in annual payments. You also receive 40% tax relief on the contribution, creating a combined financial uplift that far exceeds the initial outlay. We suggest timing these payments well before the 5 April tax year end to ensure your records are precise.

Gift Aid and Other Deductions

Charitable giving via Gift Aid provides a legitimate mechanism to reduce your taxable threshold. When you donate to a registered charity, the “grossed-up” value of that gift is deducted from your ANI. A £100 donation is treated as a £125 deduction in the eyes of HMRC. It’s a simple yet overlooked method to shave hundreds off your total income figure. You must report these donations correctly on your Self Assessment return to see the benefit reflected in your HICBC calculation. Additionally, certain employment expenses and professional subscriptions can be utilised to further trim your ANI. We recommend a thorough audit of your annual outgoings to identify every allowable statutory deduction.

- Salary Sacrifice: Opting for an electric vehicle or the Cycle to Work scheme reduces your gross pay before it’s even reported to HMRC. For employed parents, understanding how the minimum wage 2025 thresholds interact with salary sacrifice arrangements is essential, as reductions to gross pay must not bring earnings below statutory minimums.

- Workplace Benefits: Health screenings or specific training courses can sometimes be structured to lower your taxable salary.

- Bespoke Planning: Every household’s financial architecture is unique; generic advice often fails to account for the nuances of complex remuneration packages.

The hmrc child benefit changes 2025 demand a more sophisticated level of fiscal discipline. Our team provides bespoke tax planning advice to help you retain your benefits while remaining fully compliant with statutory requirements.

Professional Assistance with HMRC Compliance and Tax Planning

The landscape of UK taxation is becoming increasingly granular. With the hmrc child benefit changes 2025 moving toward a household-based assessment model, the margin for error in Self Assessment filings has narrowed. We provide a bespoke tax review that looks beyond simple data entry. Our team examines the interplay between your various income streams to ensure you aren’t inadvertently overpaying the High Income Child Benefit Charge. Precision is our standard. We manage your affairs with the discretion expected by high-net-worth individuals, ensuring all statutory obligations are met without sacrificing fiscal efficiency.

Our approach moves beyond basic compliance. We help families understand how the April 2025 transition affects their specific financial ecosystem. By analyzing your adjusted net income, we identify legitimate ways to maintain benefit eligibility through structured financial decisions. This level of professional oversight is essential for those whose income fluctuates near the £60,000 and £80,000 thresholds established in the 2024 Spring Budget.

Bespoke Personal Tax Services

For the professional or business owner, the distinction between corporate profits and personal benefit eligibility is often blurred. Our advisors offer tailored guidance to help you structure withdrawals effectively. This is particularly relevant as the hmrc child benefit changes 2025 require a more holistic view of domestic income. We ensure your tax position remains optimised while maintaining full compliance. For a deeper look at our approach to long-term fiscal health, you may refer to our UK Personal Tax & Inheritance Planning Guide.

Securing Your Family’s Financial Future

Effective tax planning isn’t a reactive task; it’s a pillar of long-term wealth management. By integrating Child Benefit considerations into your broader strategy, such as pension contributions or Gift Aid, we can often reduce your adjusted net income below critical thresholds. This proactive stance provides the “quiet excellence” our clients value. We take the administrative burden away, allowing you to focus on your professional and family life. If you require a refined approach to your 2025 tax liabilities, contact Davis & Co LLP for a professional tax consultation.

- Detailed analysis of household income vs. benefit thresholds

- Strategic use of pension contributions to lower adjusted net income

- Comprehensive support for complex Self Assessment returns

- Discreet management of international and domestic tax assets

Securing Your Family’s Financial Position

The transition toward a household income model represents a fundamental shift in how the UK government assesses eligibility. While the revised High Income Child Benefit Charge thresholds offer a reprieve for many, the complexity of these hmrc child benefit changes 2025 requires a proactive approach to tax planning. Effective mitigation often involves strategic pension contributions or Gift Aid declarations to manage your adjusted net income effectively. Navigating these statutory adjustments ensures your family retains the maximum support available while remaining fully compliant with evolving regulations. It’s vital to act before the new tax year begins to ensure your strategy is robust.

As Chartered Certified Accountants since 1901, we provide the seasoned expertise necessary to handle complex personal tax and international planning. Our firm adopts a composed partnership approach; we ensure your financial affairs are managed with discretion and intellectual rigour. We invite you to consult our tax specialists to optimise your 2025 tax position and secure a bespoke strategy for your household. Taking these steps now provides the clarity and stability your family’s long-term financial health deserves.

Frequently Asked Questions

Do I need to pay back Child Benefit if I earn over £60,000 in 2025?

Yes, you’ll be liable for the High Income Child Benefit Charge if your adjusted net income exceeds £60,000. This tax charge applies at a rate of 1% of the benefit for every £200 earned above this threshold. Once your income reaches £80,000, the charge equals the full amount of the benefit received, effectively requiring a total repayment.

We recommend reviewing your annual earnings to ensure accurate Self Assessment reporting. Our advisors help clients navigate these statutory obligations to avoid unexpected tax bills at the end of the financial year.

Can I still claim Child Benefit if my partner earns more than me?

You can still claim Child Benefit regardless of your partner’s income, but the partner with the higher income is responsible for paying the tax charge if they earn over £60,000. It’s often beneficial for the lower earner to make the claim to maintain their National Insurance record.

We assist families in structuring their affairs to ensure they meet HMRC requirements while protecting individual benefit entitlements. This collaborative approach ensures both partners understand their respective legal and financial positions.

How does HMRC calculate the High Income Child Benefit Charge?

HMRC calculates the charge based on your adjusted net income, which includes your total taxable income minus specific deductions like gift aid or pension contributions. For every £200 you earn above the £60,000 threshold, you must repay 1% of the total Child Benefit received.

This tapered calculation continues until your income hits the £80,000 limit. At this point, the tax charge matches the benefit amount exactly. We provide bespoke calculations for our clients to help them understand their precise liability before the tax year concludes.

Will Child Benefit be based on household income in 2025?

No, Child Benefit remains based on individual income for the 2025/26 tax year despite proposed reforms. While the government announced plans in the 2024 Spring Budget to move to a household-based system by April 2026, these **hmrc child benefit changes 2025** focus on the established individual thresholds.

Currently, a household with two parents earning £59,000 each receives full benefits. Conversely, a single parent earning £80,000 receives none after the tax charge. We monitor these policy shifts closely to provide our clients with timely, strategic advice as regulations evolve.

What happens if I forget to tell HMRC I am liable for the charge?

Failure to notify HMRC of your liability results in a penalty alongside the repayment of the unpaid tax and accrued interest. These penalties typically range from 10% to 100% of the tax due, depending on whether the omission was deemed deliberate or unprompted.

HMRC uses data matching technology to identify individuals who’ve received benefits while earning over the threshold. We advise immediate disclosure if you’ve missed previous deadlines, as a proactive approach often leads to more favourable treatment from the authorities.

Is it better to opt out of Child Benefit payments entirely?

You should consider opting out of payments if your income exceeds £80,000 to avoid the administrative burden of a Self Assessment return. However, it’s vital to still claim the benefit but choose not to receive the money. This ensures you continue to receive National Insurance credits toward your State Pension.

Opting out of the payment rather than the claim itself is a pragmatic solution for high earners. We help our clients evaluate these options to ensure their long-term financial security isn’t compromised by short-term tax considerations.

How do pension contributions affect my Child Benefit eligibility?

Pension contributions effectively lower your adjusted net income, which can keep you below the £60,000 threshold or reduce the charge you owe. If you earn £62,000 but contribute £2,000 to a private pension, your income for benefit purposes becomes £60,000.

This is a highly effective way to retain your benefits while building your retirement fund. Our team often identifies such strategic opportunities to help clients manage their tax positions with precision and foresight.

Do I still get National Insurance credits if I don’t receive the payments?

Yes, you’ll continue to receive National Insurance credits as long as you complete the Child Benefit claim form and select the zero payment option. These credits are essential for parents who aren’t working or earn less than £123 per week.

You need 35 qualifying years of contributions to receive the full State Pension. Protecting these credits is a core component of our private client advisory services, ensuring that your future entitlements remain secure even if you don’t receive monthly cash payments now.