The era of the simple low-salary, high-dividend strategy has effectively ended for the sophisticated business owner. With the higher dividend tax rate now at 35.75% and corporation tax reaching 25% for many, the margin for financial inefficiency has never been slimmer. Achieving truly tax efficient profit extraction for directors in 2026 requires a more nuanced, multi-layered approach that looks beyond basic monthly drawings. We recognize that it’s increasingly difficult to balance personal liquidity with the need to protect your company’s hard-earned reserves from fiscal drag and rising levies.

We’ll provide you with a clear roadmap to navigate these complexities, ensuring your extraction strategy maximizes net take-home pay while remaining fully compliant with 2026 HMRC regulations. This guide explores how to integrate employer pension contributions, electric vehicle benefits, and refined exit planning to build lasting wealth. We’ll move past traditional methods to examine a strategic framework that treats your corporate and personal tax positions as a single, cohesive entity. It’s time to transition from a reactive stance to one of composed, long-term financial authority.

Key Takeaways

- Understand why the traditional low-salary, high-dividend approach requires a strategic recalibration to remain effective against 2026’s higher tax thresholds.

- Explore how a balanced combination of salary, dividends, and employer pension contributions can significantly reduce your overall corporate and personal tax burden.

- Discover the specific criteria for using alternative methods, such as home office rental and electric vehicle benefits, to achieve tax efficient profit extraction for directors.

- Evaluate how international residency and strategic exit planning influence your remuneration choices and long-term wealth preservation.

- Establish a clear framework for a bespoke profit extraction plan that provides both immediate liquidity and a secure financial future.

Understanding the 2026 Landscape for Director Remuneration

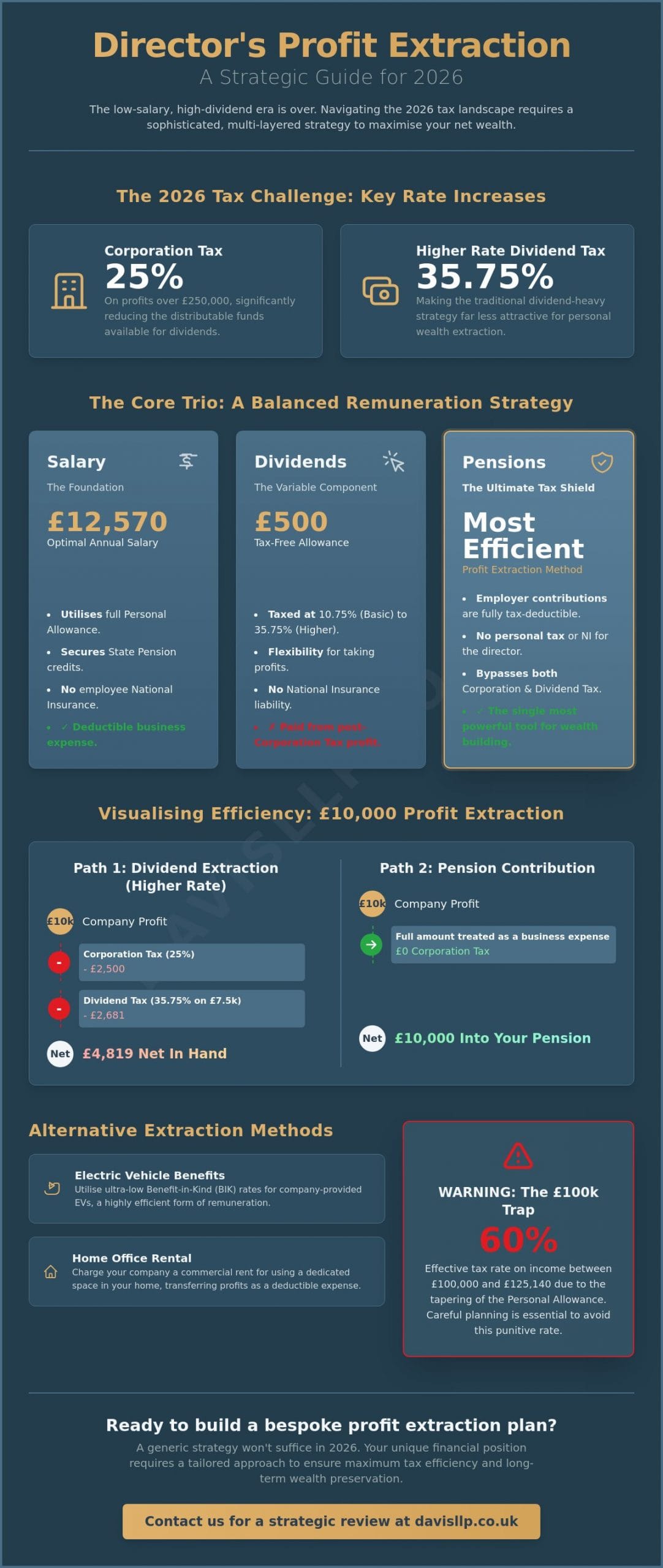

Tax-efficient profit extraction for directors is no longer a simple matter of choosing between a salary and a dividend. It represents a deliberate, multi-layered calibration of personal and corporate tax liabilities to ensure that the maximum amount of wealth remains within your control. The historical preference for a minimal salary and substantial dividends is facing unprecedented pressure. This shift is largely driven by the current UK corporation tax system, where rates of 25% for profits over £250,000 significantly reduce the pool of distributable funds available to shareholders. For many, achieving tax efficient profit extraction for directors now requires looking beyond the obvious to find more sophisticated avenues for wealth transfer.

We must consider the “Total Tax Take”. This concept describes the cumulative impact of Corporation Tax, Income Tax, and National Insurance on every pound earned by the business and eventually received by the director. When these elements interact, they can create a combined tax burden that surprises even seasoned business owners. Strategy in 2026 is about identifying the point of diminishing returns for each extraction method and pivoting before the tax burden becomes punitive.

The Impact of 2026 Tax Thresholds

The fiscal landscape for the 2026/27 tax year is defined by frozen thresholds and rising rates. The personal allowance remains at £12,570. Any income beyond this is subject to tax. For most directors, maintaining a salary at exactly this level is the most efficient baseline. It utilizes the full allowance while securing state pension credits without incurring employee National Insurance. However, the dividend landscape has become more challenging. The dividend allowance is now just £500. Beyond this tiny tax-free window, basic rate taxpayers pay 10.75%, while higher rate taxpayers face a 35.75% charge. These increased rates mean that the traditional dividend-heavy approach often results in a significantly higher personal tax bill than in previous years.

Why a Bespoke Strategy is Essential

Generic advice fails because it ignores the complexity of your broader financial life. If you have rental income, pension drawdowns, or other investments, the math of tax efficient profit extraction for directors changes instantly. One of the most significant risks is the 60% effective tax rate that occurs when the personal allowance begins to taper for those earning over £100,000. Without careful planning, you can easily fall into these high-tax traps that erode your net position. This is where expert tax advice in the UK becomes a strategic necessity. We focus on a composed, forward-looking approach that anticipates these threshold interactions before they become liabilities. A truly effective plan doesn’t just look at the current month; it builds a foundation for long-term wealth preservation.

The Core Trio: Optimising Salary, Dividends, and Pensions

While the foundational elements of director remuneration remain constant, the weighting of each component has shifted significantly. In 2026, the trio of salary, dividends, and pensions must be balanced with precision to achieve true tax efficient profit extraction for directors. When evaluating different profit extraction methods, it’s clear that the interplay between corporate and personal liabilities has reached a new level of complexity. Salary and employer pension contributions are particularly valuable because they’re treated as business expenses, reducing the company’s taxable profit before the 25% Corporation Tax rate is applied. Dividends, conversely, are paid from profits that have already been taxed, making the 2026 rate increases a critical consideration in your total tax take.

The “sweet spot” for a director’s salary in the 2026/27 tax year remains at £12,570 for most individuals. By setting your salary at this level, you utilize your full personal allowance and ensure the year counts toward your State Pension without triggering employee National Insurance contributions. From the company’s perspective, this salary is a deductible expense, providing a modest but reliable reduction in Corporation Tax. While some directors consider a higher salary to boost their personal borrowing capacity, the 13.8% employer National Insurance charge usually makes this a less efficient route for pure profit extraction.

Pensions: The Most Efficient Extraction Tool?

Employer pension contributions often represent the most robust tool in our arsenal. Unlike salary, they attract no National Insurance contributions from either the employer or the employee. With the annual allowance currently at £60,000 for 2026, and the ability to utilize three years of carry-forward rules, directors can move substantial sums into a tax-sheltered environment. This dual benefit of Corporation Tax relief and zero National Insurance makes pensions the gold standard for long-term wealth building. It’s an area where a strategic small business accountant can provide significant value by calculating the exact contribution levels that align with your company’s cash flow.

Balancing Dividends for Liquidity

Dividends remain essential for immediate liquidity, yet they require meticulous administration. You must ensure the company has sufficient distributable reserves; otherwise, HMRC may reclassify payments as illegal dividends or overdrawn loan accounts. In 2026, the dividend allowance is just £500, with rates set at 10.75% for basic rate and 35.75% for higher rate payers. When we compare a £10,000 dividend to a £10,000 bonus, the dividend often yields a higher net take-home pay because it avoids the heavy burden of National Insurance. However, the lack of Corporation Tax relief on dividends means the gap is narrowing, requiring a bespoke calculation for every director’s unique circumstances.

Alternative Extraction Methods: Rents, Loans, and Benefits in Kind

While the core trio of salary, dividends, and pensions forms the backbone of most strategies, a truly sophisticated approach to tax efficient profit extraction for directors explores more granular opportunities. These alternative methods allow you to leverage personal assets and company resources to enhance liquidity while maintaining a lower overall tax profile. However, these techniques require a higher degree of administrative rigour. Every transaction must be defensible under the “wholly and exclusively” rule, meaning the expense must be incurred solely for the purposes of the trade. Without professional valuation and meticulous documentation, these methods can attract unwanted scrutiny from HMRC.

Charging Rent for Business Use of Personal Assets

One of the most frequent questions we encounter is whether it’s legal to rent a home office to your own company. The answer is a definitive yes, provided the arrangement is commercial and documented through a formal license agreement. By charging the company rent for office space or storage, the business receives Corporation Tax relief on the payments. You will pay income tax on this rental income at your marginal rate, but crucially, no National Insurance is due. It’s vital to ensure the rent reflects local market rates. You should also be aware that using a dedicated area of your home exclusively for business can occasionally impact your Capital Gains Tax private residence relief when you eventually sell the property.

Director Loan Accounts (DLA) and Interest

The Director’s Loan Account is a flexible tool that requires careful management. If you borrow from the company and the balance isn’t repaid within nine months and one day of the year-end, the company faces a Section 455 tax charge, which has increased to 35.75% as of April 2026. Conversely, if you have lent your own money to the business, charging the company interest is an excellent way to extract profit. This interest is a deductible expense for the company, and for you, it may fall within your Personal Savings Allowance, potentially allowing you to receive up to £1,000 in interest tax-free, depending on your total income bracket.

Tax-Efficient Benefits in Kind (BIK)

In the 2026 landscape, the most compelling Benefit in Kind remains the electric vehicle. Even with the BIK rate increasing to 4% this year, it remains vastly more efficient than petrol or diesel equivalents, which can reach rates of 37%. For a director in the higher tax bracket, the monthly tax cost of a high-end electric company car is often less than £100. We also encourage our clients to utilize “trivial benefits.” You can provide yourself with non-cash gifts, such as store vouchers, up to a value of £50 per instance, capped at £300 per year. These small extractions are entirely tax-free and don’t require reporting on a P11D, provided they aren’t a reward for performance.

Strategic Considerations: International Interests and Exit Planning

For directors whose commercial activities or personal lives extend beyond UK borders, the pursuit of tax efficient profit extraction for directors involves managing a complex web of overlapping jurisdictions. It’s no longer sufficient to consider UK tax rates in isolation; residency and domicile status play a pivotal role in determining where and how your income is taxed. For those with a global footprint, international tax planning is not merely an optional extra but a fundamental component of wealth preservation. We focus on ensuring that profits moved across borders don’t suffer from unnecessary leakage due to withholding taxes or mismatched fiscal years.

A long-term view often suggests that the most effective way to extract value from a company isn’t through annual income at all. Instead, it involves building capital value within the business to be extracted at a lower tax rate upon exit. This shift from an income-focused mindset to a capital-focused one requires patience and a clear understanding of the 2026 regulatory environment. If your business has international reach, we invite you to discuss your specific requirements with our team at davisllp.co.uk to ensure your global strategy is as robust as your local one.

Managing Cross-Border Interests

Double Tax Treaties are essential tools for directors with international interests, as they prevent the same profit from being taxed twice. However, these treaties are complex and require careful application to dividend and interest payments. We also closely monitor the risk of “Permanent Establishment.” If a director performs significant duties while physically located abroad, they may inadvertently create a taxable presence for the company in that jurisdiction. This is a particular concern for family offices and international SMEs where the lines between personal residency and corporate management can become blurred. Specialized advice is critical to ensure that your extraction methods don’t trigger unforeseen corporate tax obligations in multiple countries.

Exit Strategies and Capital Extraction

The decision to retain profits within the company rather than extracting them as dividends can be a powerful wealth-building strategy. By doing so, you may eventually extract these funds as capital when you sell or liquidate the business. Business Asset Disposal Relief (BADR) remains a cornerstone of this approach, though the fiscal environment has changed. As of 6 April 2026, the CGT rate for BADR increased to 18%, up from the previous 14%. While this is a notable increase, it still compares favourably to the 35.75% higher rate on dividends.

- Eligibility: Ensure you meet the two-year qualifying period as an employee or office holder with at least 5% shareholding.

- Retention: Weigh the immediate need for liquidity against the long-term benefit of an 18% tax rate on a lifetime limit of £1 million.

- Compliance: Maintain precise records to prove the company remains a trading entity rather than an investment vehicle.

Successfully executing this strategy requires a composed, multi-year perspective that aligns your business growth with your personal retirement goals.

Implementing a Bespoke Profit Extraction Strategy

The transition from understanding individual tax rules to executing a cohesive financial plan is where true value is created. A robust 2026 remuneration strategy isn’t a static document; it’s a living framework that must adapt to your company’s performance and your personal aspirations. Achieving tax efficient profit extraction for directors requires a move away from “off-the-shelf” solutions toward a highly individualized approach. We view this process as a composed partnership, where the technical precision of a small business accountant provides the stability you need to make confident commercial decisions. By aligning your corporate structure with your personal tax profile, we ensure that every pound extracted is done so with the highest level of fiscal integrity.

Tax efficiency is far more than a compliance exercise. It’s a strategic tool for wealth creation that protects your business’s capital from the erosion of fiscal drag. As we’ve explored, the interaction between different income streams can lead to punitive effective tax rates if not managed with care. Implementation is about timing and documentation, ensuring that every dividend voucher, board minute, and rental agreement is prepared with the foresight to withstand official scrutiny.

The Annual Review Process

We recommend a formal review of your extraction mix at least three months before the end of your fiscal year. This timing is critical because it allows us to adjust your strategy based on actual profitability rather than projections. If your company has experienced a stronger-than-expected quarter, we might pivot toward higher employer pension contributions to mitigate a rising Corporation Tax bill. Conversely, if personal cash flow needs have changed, we can recalibrate your dividend schedule. We rely on accurate management accounts to make these real-time decisions, transforming accounting data into a strategic roadmap for your personal wealth.

How Davis & Co LLP Supports Directors

Our firm provides the deep-seated expertise required to navigate the sensitive interaction between corporate and personal tax positions. We offer comprehensive Personal Tax Services that go beyond simple self-assessment filings, focusing instead on the long-term human impact of complex tax legislation. In an era of increased transparency, we help our clients interpret and respond to the latest hmrc tax warnings, ensuring that your tax efficient profit extraction for directors remains both innovative and fully compliant. We invite you to schedule a strategic consultation to review your 2026 planning. This is an opportunity to move beyond traditional accounting and establish a professional partnership built on reliability, discretion, and quiet excellence.

Securing Your Financial Future in 2026

The complexity of the 2026 fiscal environment demands a departure from static remuneration models. Success now depends on a multi-layered strategy that looks beyond the simple salary and dividend binary to incorporate long-term capital preservation and robust pension growth. Achieving truly tax efficient profit extraction for directors requires a holistic view of your corporate and personal liabilities, ensuring that every financial decision supports your broader wealth-building objectives. By integrating real-time management accounts with sophisticated planning, we help you stay ahead of threshold changes and shifting regulations.

As Chartered Certified Accountants with a legacy dating back to 1901, we bring a wealth of experience to every client relationship. We act as strategic partners for UK SMEs and family offices, offering specialized expertise in both international and personal tax services. Our goal is to provide the steady, reliable authority you need to manage sensitive commercial and personal matters with absolute confidence. We invite you to consult Davis & Co LLP for a bespoke 2026 tax strategy that aligns with your specific professional and personal goals. It’s time to ensure your profit extraction is as efficient as the business that generates it.

Frequently Asked Questions

What is the most tax-efficient salary for a director in 2026?

The most tax-efficient salary for the majority of directors in the 2026/27 tax year is £12,570. This specific figure aligns with the frozen personal allowance, ensuring you pay no income tax on this portion of your earnings. Because it sits above the Lower Earnings Limit, you continue to accrue qualifying years for your State Pension without triggering employee or employer National Insurance contributions. This approach provides a foundational layer for tax efficient profit extraction for directors.

Can I still use the £500 dividend allowance in 2026?

Yes, the dividend allowance remains available in 2026, though it is limited to £500 per individual. Any dividend income received above this threshold is subject to tax at rates of 10.75% for basic rate payers and 35.75% for those in the higher rate bracket. While the allowance is modest, it still offers a small tax-free window that should be utilized as part of your broader annual distribution plan to maximize your net position.

Is it better to take a bonus or a dividend in 2026?

Dividends generally remain more tax-efficient than bonuses for directors, despite the recent 2% rate increase. A dividend avoids the 13.8% employer National Insurance and the employee National Insurance that apply to a bonus. Although a bonus is a deductible expense for Corporation Tax purposes, the combined National Insurance and Income Tax burden usually outweighs the Corporation Tax saving. We provide bespoke calculations to confirm which method yields the highest net take-home pay for your specific profit level.

How do employer pension contributions reduce my company’s tax bill?

Employer pension contributions are treated as a deductible business expense, which directly reduces your company’s taxable profits and its subsequent Corporation Tax liability. In the 2026 landscape, this can result in a saving of up to 25% for companies with profits exceeding £250,000. Unlike salary or bonuses, these contributions are not subject to National Insurance, making them one of the most effective tools for tax efficient profit extraction for directors seeking long-term wealth.

What are the risks of an overdrawn Director’s Loan Account?

The primary risk of an overdrawn Director’s Loan Account is the Section 455 tax charge, which has risen to 35.75% for the 2026/27 tax year. This tax is payable if the loan isn’t repaid within nine months and one day of your company’s year-end. Additionally, HMRC has increased its scrutiny of these accounts, frequently issuing nudge letters. Loans exceeding £10,000 that are interest-free also trigger a taxable Benefit in Kind for the director, creating a further personal tax liability.

Can I pay my spouse a salary to reduce my overall family tax burden?

You can pay your spouse a salary, provided the amount is “wholly and exclusively” for the purposes of the business and reflects the actual work they perform. This strategy is an effective way to utilize their £12,570 personal allowance and lower tax brackets, reducing the overall family tax burden. However, you must maintain clear records of their role and ensure the remuneration is commercially justifiable to avoid challenges during an HMRC compliance review or audit.

Does Business Asset Disposal Relief still apply to company liquidations in 2026?

Business Asset Disposal Relief (BADR) remains available in 2026, though the applicable Capital Gains Tax rate has increased to 18% as of 6 April 2026. The lifetime limit for the relief stays at £1 million. This remains a highly efficient way to extract value when closing or selling a business, particularly when compared to the 35.75% higher rate for dividends. We assist directors in ensuring their company meets the strict qualifying criteria leading up to a formal liquidation.

How does working from abroad affect my UK profit extraction strategy?

Working from abroad introduces the risk of creating a “Permanent Establishment” in another jurisdiction, which could subject your company to foreign tax laws. Your UK profit extraction strategy must also account for Double Tax Treaties to ensure you aren’t taxed twice on the same income. Residency status significantly impacts how dividends and salaries are treated, making it essential to align your extraction methods with both UK regulations and the tax requirements of your host country to maintain global efficiency.