The most straightforward path to transferring real estate often leads to the most significant loss of strategic influence. While many investors lean toward simplicity, the choice between a bare trust vs discretionary trust for property is rarely about ease; it’s about the trade-off between immediate tax transparency and long-term security. We recognise that for many, the fear of losing control to young beneficiaries is just as pressing as the complexities of the Relevant Property Regime or opaque SDLT rules.

We’ve developed this guide to help you navigate these structures with precision. You’ll gain a clear framework for choosing the right vehicle to protect your assets from third-party claims while ensuring an optimised tax position for 2026 and beyond. We’ll examine the 45% tax rate on discretionary income, the nuances of the £325,000 nil-rate band, and the strategic advantages of maintaining trustee discretion over your real estate portfolio. By understanding these mechanisms, you can secure your legacy without sacrificing the professional oversight your assets require.

Key Takeaways

- Evaluate the 18-year-old threshold where absolute entitlement in a bare trust may compromise your long-term strategic objectives for property control.

- Compare the tax efficiencies of a bare trust vs discretionary trust for property to determine which structure best aligns with your specific income and capital gains profile.

- Master the complexities of the “Relevant Property” regime, including entry charges and the 10-year periodic charge, to ensure your real estate assets remain protected.

- Learn how integrated property accounting can help you manage the transition of assets into trust structures while minimising exposure to Stamp Duty Land Tax and Capital Gains Tax.

- Establish a robust framework for asset protection that shields your property from third-party claims while maintaining flexibility for future distributions to beneficiaries.

Understanding Trust Structures for Property Assets

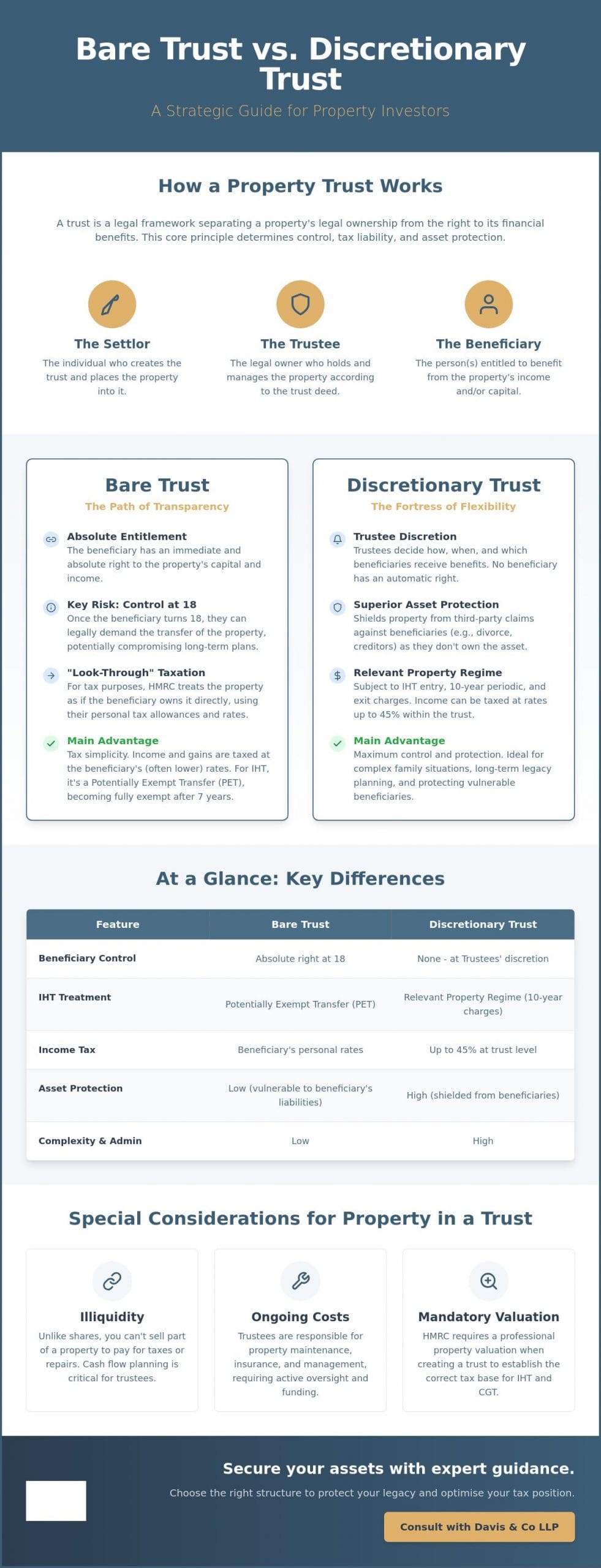

A trust acts as a robust legal framework that separates the legal title of a property from the right to enjoy its financial benefits. This separation is the cornerstone of English trust law. When you establish a trust, you aren’t simply shifting a title; you’re creating a fiduciary relationship where one party holds the asset for the benefit of another. For those weighing up a bare trust vs discretionary trust for property, this distinction determines who ultimately directs the asset’s future and who bears the tax liability.

The settlor, as the person creating the trust, must carefully manage “entry” events. These include potential lifetime Inheritance Tax charges or Capital Gains Tax implications. The trustees then carry the fiduciary burden. Managing real estate is rarely passive. It involves maintenance, insurance, and the complexities of letting. We’ve seen that trustees must act with unwavering diligence to protect the beneficiaries’ interests. The beneficiary’s position varies significantly depending on the structure. They may have an absolute right to the property or merely a potential interest that remains at the trustees’ discretion.

The Core Components of a Property Trust

When deciding on a bare trust vs discretionary trust for property, the split between legal and beneficial ownership is vital. Trustees appear on the Land Registry as the legal owners, while beneficiaries hold the “equitable” interest. We believe a bespoke Trust Deed is essential for property portfolios. It shouldn’t be a generic template. It needs to specify how repair costs are funded and what happens if a beneficiary wishes to reside in the property. By 2026, compliance with the Trust Registration Service (TRS) is a non-negotiable requirement for all taxable property trusts to ensure transparency with HMRC.

Property as a Unique Trust Asset

Property is fundamentally illiquid. Unlike a share portfolio, you can’t easily sell a small portion of a building to pay a tax bill or a repair invoice. Trustees must plan for cash flow to cover ongoing insurance and maintenance. There’s also a natural tension between capital growth and rental income. Different trusts treat these value streams with varying degrees of flexibility. Finally, precise valuation is mandatory. HMRC requires professional valuations upon the creation of the trust to establish the correct tax base for the “Relevant Property” regime or potential hold-over relief. We help our clients ensure these valuations are robust enough to withstand scrutiny.

Bare Trusts for Property: Transparency and Absolute Entitlement

Bare trusts are often perceived as the simplest form of property holding. In this arrangement, the trustee acts merely as a nominee, holding the legal title while the beneficiary retains the absolute right to both the capital and any income generated. According to UK government guidance on trust types, the beneficiary is the true owner for tax purposes. When evaluating a bare trust vs discretionary trust for property, the transparency of the bare trust is its defining feature. It offers a direct line between the asset and the individual intended to benefit from it.

The “look-through” principle dictates how HMRC views these assets. Rental income isn’t taxed at specialized trust rates; instead, it flows directly to the beneficiary’s tax return. Similarly, if the property is sold, Capital Gains Tax (CGT) is calculated based on the beneficiary’s personal circumstances and annual exemptions. This is particularly relevant for property investors looking to leverage a child’s or grandchild’s lower tax bands. However, transferring a property into a bare trust is a disposal for CGT purposes for the settlor, a detail often overlooked in more general financial discussions. It’s a permanent move with immediate tax consequences.

Tax Advantages of the Bare Trust Structure

The primary appeal lies in fiscal efficiency and administrative ease. Because the assets are treated as belonging to the beneficiary, they can utilise their personal allowance and lower tax brackets for rental profits. From an Inheritance Tax (IHT) perspective, transfers into a bare trust are Potentially Exempt Transfers (PETs). If the settlor survives seven years, the property value falls outside their estate entirely. There is no “Relevant Property” regime to navigate, meaning you avoid 10-year periodic charges and exit fees. Our team provides Personal Tax Services to ensure these transfers are executed with full compliance and strategic foresight.

Strategic Risks for Property Owners

Simplicity comes at the cost of control. Once a beneficiary reaches 18 in England and Wales, they gain absolute entitlement. They can legally demand that the trustees transfer the property title into their own name. This lack of a “gatekeeper” function makes the property vulnerable. If the beneficiary faces a divorce or bankruptcy, the property is considered their personal asset and is fully exposed to third-party claims. Unlike other structures, you cannot change the beneficiary once the deed is signed. This permanence requires a high degree of certainty before commitment. You’re effectively handing over the keys on a fixed date, regardless of the beneficiary’s maturity or financial stability at that time.

Discretionary Trusts: Control, Flexibility, and Property Management

The choice between a bare trust vs discretionary trust for property often hinges on the desire for enduring control. While a bare trust offers transparency, the discretionary model provides a sophisticated layer of protection. In this structure, no single beneficiary has an absolute right to the property or its income. Instead, the trustees act as gatekeepers, deciding how and when to distribute assets from a defined pool of potential beneficiaries. This lack of individual entitlement is precisely what shields the property from a beneficiary’s personal creditors, matrimonial claims, or potential insolvency.

Transfers of real estate into discretionary trusts are not neutral events for Stamp Duty Land Tax (SDLT). Unlike simple transfers to individuals, moving property into a discretionary trust often triggers the higher rate surcharge, as the trust is typically treated as a non-natural person or an additional property owner. We’ve observed that many investors overlook this immediate capital outlay in favour of long-term IHT benefits. It’s a critical factor that requires careful calculation before the trust deed is finalised.

The Relevant Property Tax Lifecycle

Most discretionary trusts fall under the “Relevant Property” regime, which creates a specific tax lifecycle. If the value of the property transferred exceeds the current nil-rate band of £325,000, an immediate 20% lifetime Inheritance Tax entry charge applies. The complexity doesn’t end at the entry point. Every ten years, the trust faces a periodic charge of up to 6% on the value of the assets held above the nil-rate band. Finally, when property or capital is distributed to a beneficiary, an exit charge may be due. We provide specialised Trust Tax Services to help trustees navigate these recurring liabilities and ensure compliance with HMRC’s stringent reporting deadlines.

Income Tax and Rental Profits

For the 2026/27 tax year, discretionary trusts face a 45% tax rate on non-dividend income, such as rental profits, after a modest £500 tax-free allowance. This is significantly higher than the personal rates many beneficiaries might pay. However, this tax isn’t necessarily a final cost. When trustees distribute income, they provide the beneficiary with an R185 form. This certificate allows the beneficiary to reclaim the difference if their personal tax rate is lower than the 45% already paid by the trust. To manage these high headline rates, we employ rigorous Property Accounting to ensure every allowable expense, from maintenance to insurance, is deducted to reduce the trust’s taxable profit.

Bare Trust vs Discretionary Trust: A Comparison Framework

The decision-making process for real estate succession requires a clear understanding of the trade-offs between immediate tax transparency and long-term strategic control. When comparing a bare trust vs discretionary trust for property, we see a fundamental split in how rights are distributed. In a bare trust, the beneficiary’s rights are absolute; they eventually own the asset. In a discretionary trust, the settlor’s intent is preserved through the trustees’ ongoing decision-making power. This choice dictates everything from the initial tax entry charges to the eventual exit strategy.

Inheritance Tax (IHT) treatment is perhaps the most stark differentiator. A bare trust operates under the Potentially Exempt Transfer (PET) rules, where the gift falls out of the settlor’s estate after seven years. Conversely, discretionary trusts face immediate 20% lifetime charges on transfers exceeding the £325,000 nil-rate band. While the bare trust is fiscally simpler, it lacks the adaptable distributions that allow a discretionary trust to respond to changing family circumstances or tax legislation over several decades. It’s a choice between the certainty of a fixed gift and the resilience of a managed legacy.

Which Structure Suits Your Property Goals?

Your choice depends on the specific commercial and personal objectives you wish to achieve. We typically categorise these into three distinct scenarios:

- Scenario A: Gifting a single buy-to-let. If your goal is to provide a child with a specific asset to fund their future education, a bare trust is often the most efficient route. It utilizes their personal tax bands and avoids the complexities of the 10-year charge, provided you’re comfortable with them gaining full control at age 18.

- Scenario B: Protecting a multi-property portfolio. For larger holdings intended to support multiple generations, the discretionary trust is superior. It prevents the fragmentation of the portfolio and keeps the assets shielded from individual beneficiary risks like divorce or personal debt.

- Scenario C: Managing property for a vulnerable beneficiary. When a beneficiary cannot manage their own financial affairs, a specialist discretionary trust provides the necessary structure to ensure their long-term care without giving them direct legal title.

Operational Costs and Compliance

Maintaining these structures involves more than just a one-off legal fee. Trustees must ensure annual tax returns (SA900) are filed and that meticulous bookkeeping is maintained to track rental income and expenses. For discretionary trusts, periodic professional valuations are a mandatory part of calculating the 10-year anniversary charges. These valuations must be robust enough to satisfy HMRC’s scrutiny of the property’s market value. Given the high stakes of real estate assets, investing in professional trust tax services is a necessary step to mitigate the risk of costly compliance errors. If you require a tailored assessment of your portfolio’s needs, you can contact our specialist team for a consultation.

Strategic Implementation with Davis & Co LLP

Implementing a property trust requires more than just formal legal documentation; it demands a continuous, integrated approach to financial management. When you’re weighing the merits of a bare trust vs discretionary trust for property, the transition phase is where the most significant fiscal risks reside. We focus on managing this transition with precision, ensuring that the movement of real estate into a trust structure is executed in a way that minimises exposure to Stamp Duty Land Tax and Capital Gains Tax. Our role is to act as your strategic partner, providing the professional distance of an expert while maintaining the close, collaborative relationship necessary for sensitive family matters.

The 2026 regulatory environment necessitates a proactive stance on compliance. We don’t merely react to changes; we anticipate them. By aligning your property portfolio with current HMRC expectations, we ensure your trust remains a viable vehicle for wealth preservation. This involves moving beyond basic service delivery to offer a comprehensive oversight that considers both the individual and organisational impacts of trust management. Our goal is to provide you with the security that comes from knowing your real estate assets are managed with intellectual rigour and professional gravitas.

Specialist Property Accounting

Managing the financial health of trust-held property requires a specific set of accounting skills. We handle the meticulous preparation of rental accounts and the strategic allocation of expenses to ensure the trust’s taxable profit is accurately stated. This operational excellence extends to Capital Gains Tax reporting for property disposals and robust representation when liaising with HMRC on complex SA900 trust tax returns. We ensure that every deduction is claimed and every reporting deadline is met, allowing trustees to focus on their broader fiduciary responsibilities without the burden of administrative complexity.

Trust Tax Planning for 2026

As we move through 2026, we provide rigorous reviews of existing trust structures to ensure they remain compliant with the latest legislative shifts. For clients with global interests, our expertise in international tax planning is vital when managing the unique challenges faced by non-UK resident trustees or beneficiaries. We focus on creating stability in an often volatile tax environment. Davis & Co LLP provides bespoke trust tax services that align your property portfolio with your family’s long-term financial objectives. By partnering with us, you gain access to a level of quiet excellence that reinforces the long-term viability of your property legacy.

Securing Your Real Estate Legacy for 2026 and Beyond

The strategic decision between a bare trust vs discretionary trust for property rests on your specific priorities for asset protection and the long-term fiscal profile of your portfolio. While a bare trust offers the clarity of personal tax rates and PET status, it doesn’t provide the defensive depth required for complex, multi-generational holdings. Conversely, the discretionary model provides a sophisticated shield against third-party claims, although it demands precise management of the 10-year periodic charge and high trust tax rates.

We view a well-structured trust as a dynamic asset rather than a static legal document. As Chartered Certified Accountants since 1901, we’ve spent over a century providing the reliability and discretion required for such sensitive matters. Our specialists in Property Accounting and Trust Tax, coupled with our expertise in International Tax Planning, ensure your structures remain robust under the latest 2026 regulations. We’re here to help you navigate these complexities with composed partnership and intellectual rigour.

Consult our trust tax specialists to structure your property portfolio effectively. Taking the time to align your legal framework with your family’s financial objectives today provides the stability your real estate assets deserve for the future.

Frequently Asked Questions

What is the main difference between a bare trust and a discretionary trust for property?

The primary distinction lies in the nature of the beneficiary’s entitlement. In a bare trust, the beneficiary has an absolute and immediate right to the property and its income; the trustee acts simply as a nominee. A discretionary trust allows trustees to decide which individuals from a pool of beneficiaries receive distributions. This choice between a bare trust vs discretionary trust for property determines whether the settlor maintains long-term strategic control or transfers ownership immediately.

Do I pay Stamp Duty Land Tax (SDLT) when transferring property into a trust?

Transfers into a trust generally attract SDLT if there’s “chargeable consideration,” such as the assumption of an existing mortgage. Even if no money changes hands, transfers into discretionary trusts are often subject to the higher rate surcharge because the trust is viewed as an additional property owner. It’s vital to calculate these costs before the transfer, as they represent an immediate capital outlay that can impact the overall efficiency of the structure.

Can I live in a property held in a discretionary trust?

A beneficiary can reside in a trust-held property if the trust deed grants them a right of occupation or if the trustees exercise their discretion to allow it. If the settlor continues to live in the property after transferring it, the arrangement may be classified as a “gift with reservation of benefit.” This would likely mean the property remains part of the settlor’s estate for Inheritance Tax purposes, defeating one of the primary reasons for the trust.

How is rental income from a trust-held property taxed in 2026?

For the 2026/27 tax year, discretionary trusts pay a flat rate of 45% on rental income exceeding the £500 tax-free allowance. This is the highest tax bracket, though beneficiaries can often reclaim a portion of this tax if their personal income levels are lower. In a bare trust, the rental profits are taxed directly at the beneficiary’s personal rates, allowing for the use of their individual tax-free allowances and lower tax bands from the outset.

What happens to a bare trust when the beneficiary turns 18?

The beneficiary gains the legal right to demand the transfer of the property into their own name once they reach the age of 18 in England and Wales. At this point, the trustees’ role effectively ends, and the beneficiary assumes full control over the asset. This lack of a “gatekeeper” is a significant factor to consider when evaluating a bare trust vs discretionary trust for property, as it removes the settlor’s ability to influence the asset’s future use or sale.

Is a discretionary trust better for Inheritance Tax planning?

Discretionary trusts offer superior flexibility and asset protection, but they come with a more complex tax regime. Transfers into these trusts are immediate lifetime charges at 20% if they exceed the £325,000 nil-rate band. Bare trusts are treated as Potentially Exempt Transfers, meaning they fall out of the estate entirely after seven years. The “better” option depends on whether you value immediate tax simplicity or long-term control and protection from third-party claims.

Can I be a trustee of my own property trust?

A settlor can certainly act as a trustee, and many choose to do so to maintain a level of management over the property’s maintenance and letting. However, if the settlor or their spouse can also benefit from the trust, it becomes a “settlor-interested” trust. In such cases, the settlor remains personally liable for income tax on the trust’s profits, which can negate many of the intended tax benefits of the structure.

How often must a discretionary trust pay the 10-year anniversary charge?

The periodic charge is calculated every ten years from the date the trust was originally established. This tax can be up to 6% of the value of the trust assets that exceed the £325,000 nil-rate band. Trustees must ensure they have a professional valuation of the property at each ten-year milestone to satisfy HMRC requirements and avoid penalties for underpayment. Regular valuations are a necessary part of the trust’s ongoing compliance lifecycle.