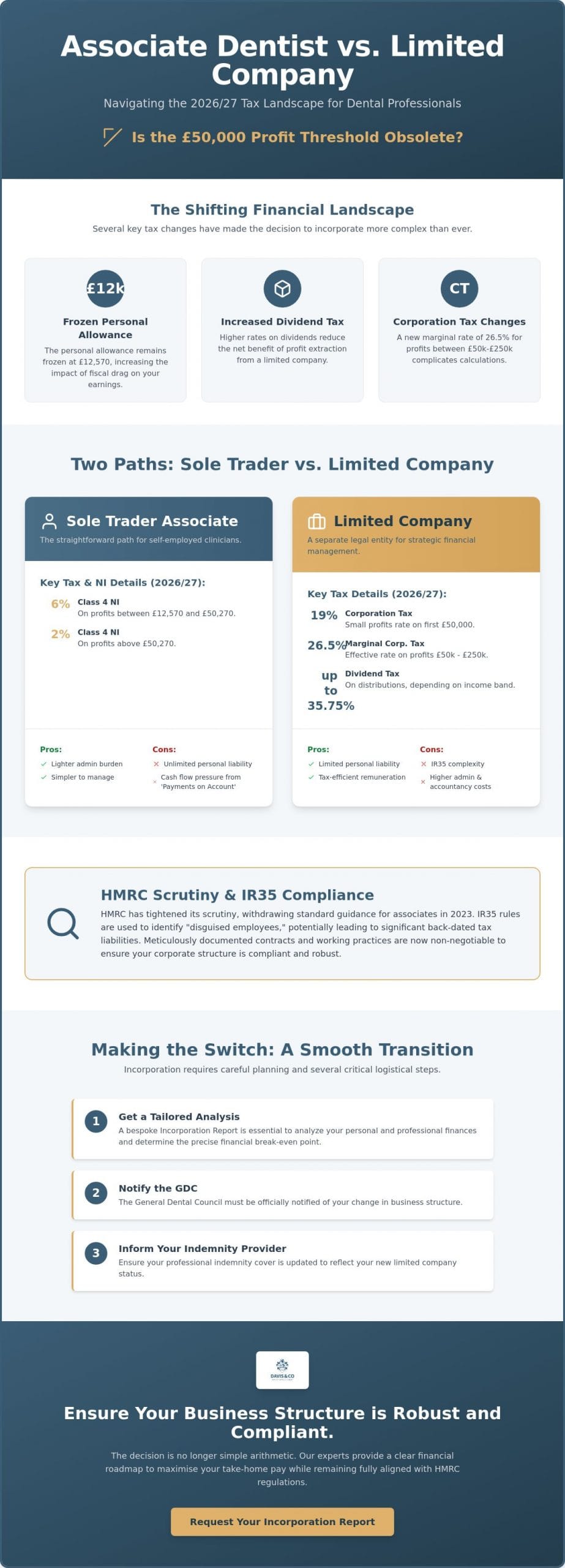

Is the £50,000 profit threshold still the gold standard for incorporating your dental practice, or has the 2026 tax landscape rendered this traditional wisdom obsolete? Deciding between an associate dentist vs limited company tax structure is no longer a simple arithmetic exercise. With the personal allowance frozen at £12,570 and dividend tax rates having increased in April 2026, the margin for financial error has narrowed. We understand the frustration of seeing your hard-earned clinical income diminished by fiscal drag and the increasing administrative weight of HMRC compliance.

We’ll help you identify the most tax-efficient path forward by comparing the flexibility of sole trader status against the strategic benefits of incorporation. This guide provides a clear financial roadmap to maximise your take-home pay while remaining fully aligned with IR35 and dental-specific guidance. We’ll examine the specific 2026/27 thresholds for switching structures, the impact of Making Tax Digital, and the critical interplay between your business model and your NHS pension benefits.

Key Takeaways

- Evaluate the shifting 2026 regulatory landscape to determine whether remaining a sole trader or incorporating offers the superior route for your specific career trajectory.

- Identify the precise financial break-even point for associate dentist vs limited company tax efficiency by accounting for the latest Corporation Tax tapering relief and dividend rate changes.

- Understand the implications of HMRC’s tightened scrutiny on employment status and how to navigate the complexities of IR35 following the withdrawal of standard associate guidance.

- Learn the logistical requirements for a smooth transition to incorporation, including critical notifications for the General Dental Council and your indemnity provider.

- Discover how a bespoke Incorporation Report provides a tailored analysis of your personal and professional finances to ensure your business structure remains robust and compliant.

The Associate Dentist Tax Landscape in 2026

The financial framework for dental professionals has undergone a profound transformation over the last few years. Historically, the transition from a self-employed associate to a limited company director was often viewed as a standard milestone in a successful clinical career. This shift was largely driven by the potential for significant National Insurance savings and the flexibility of dividend extraction. However, the 2026 tax landscape is considerably more nuanced. HMRC’s 2023 withdrawal of the standard employment status guidance for associates marked the beginning of a period of heightened scrutiny. Today, the choice between an associate dentist vs limited company tax structure requires a sophisticated analysis of your net profit, your long-term retirement goals, and your appetite for administrative responsibility.

Your chosen structure acts as the foundation for your entire financial life. It doesn’t just dictate your annual tax bill; it influences your NHS pension contributions, your personal liability, and your ability to secure competitive mortgage rates. While a limited company offers a robust shield of limited liability, it can also complicate your borrowing power if your salary is kept intentionally low for tax purposes. We find that a composed, strategic approach is essential to ensure your business model supports both your professional ambitions and your personal financial security.

The Sole Trader Associate Model

Operating as a sole trader remains the most straightforward path for many clinicians. In this model, you’re considered self-employed, and your clinical income is taxed as personal earnings after allowable expenses. For the 2026/27 tax year, you’ll navigate Class 4 National Insurance contributions of 6% on profits between £12,570 and £50,270, dropping to 2% on earnings above that threshold. While the administrative burden is lighter than a company, you must manage the cash flow impact of “Payments on Account.” These biannual deadlines in January and July require you to pay tax in advance, which can create significant pressure on your liquid reserves if not managed with precision.

The Limited Company (Incorporation) Model

Incorporation establishes your practice as a separate legal entity, distinct from your personal identity. As a director and shareholder, you’re no longer simply earning a fee; you’re managing a corporate structure. This model allows for a sophisticated remuneration strategy, typically combining a small, tax-efficient salary with dividend distributions. While this can lower your overall tax exposure, it introduces complexities regarding the UK’s anti-avoidance tax legislation (IR35). HMRC uses these rules to determine if a dentist is a “disguised employee,” which could lead to substantial back-dated tax liabilities if your contracts and working practices aren’t meticulously documented. We work closely with our clients to ensure their corporate structures are both efficient and fully compliant with these evolving standards.

Calculating the Financial Threshold for Incorporation

The decision to incorporate is no longer a binary choice based on gross earnings. In the 2026/27 tax year, the financial “break-even” point has become more elusive due to the interplay of frozen personal allowances and the marginal relief system for Corporation Tax. For profits between £50,001 and £250,000, companies face an effective marginal rate of 26.5%, a significant jump from the 19% small profits rate. When evaluating associate dentist vs limited company tax efficiency, we must also account for the increased administrative costs, including company secretarial services and higher accountancy fees, which can erode the perceived tax savings of a lower-earning associate.

Determining the exact moment to switch requires a forensic look at your net profit after all clinical expenses. While a profit of £50,000 was traditionally the threshold for incorporation, current dividend tax rates of 10.75% for basic rate taxpayers and 35.75% for higher rate taxpayers mean the gap is closing. We also consider HMRC’s guidance on employment status, which dictates how your income is classified and assessed, ensuring your chosen structure stands up to rigorous inspection.

Tax Comparison: Sole Trader vs. Limited Company

The following table illustrates the estimated total tax liability for the 2026/27 tax year, comparing a self-employed associate with a limited company director utilizing a tax-efficient salary and dividend split. These figures include Income Tax, Corporation Tax, and National Insurance.

| Net Profit | Sole Trader Total Tax | Limited Company Total Tax | Potential Saving |

|---|---|---|---|

| £60,000 | £14,524 | £13,150 | £1,374 |

| £90,000 | £26,524 | £24,380 | £2,144 |

| £120,000 | £41,650 | £37,850 | £3,800 |

A critical factor at the £120,000 level is the withdrawal of the Personal Allowance. For every £2 earned over £100,000, you lose £1 of your allowance, creating an effective 60% tax trap. A limited company can help mitigate this by retaining profits within the business to keep your personal reportable income below that £100,000 threshold.

The Dividend Strategy in 2026

Optimising your remuneration involves a delicate balance. Most dental directors opt for a salary that meets the Lower Earnings Limit for National Insurance to protect their state pension record without triggering unnecessary contributions. The remaining profit is extracted as dividends, which don’t attract National Insurance. However, you must be wary of “alphabet shares” or income shifting to family members. While splitting dividends can be tax-efficient, HMRC’s settlements legislation remains a risk if the arrangement isn’t commercial. Consulting a dental tax specialist is the most reliable way to ensure your dividend policy is both efficient and defensible.

HMRC Scrutiny: Employment Status and IR35 for Dentists

The landscape of dental taxation shifted fundamentally on 6 April 2023, when HMRC withdrew its long-standing “standard” guidance regarding the employment status of associate dentists. Previously, the industry relied on a relatively stable presumption of self-employment. Now, every engagement is assessed on its individual merits. This change has made the debate between an associate dentist vs limited company tax structure far more complex. If you operate through a personal service company, you’re subject to the IR35 rules, which seek to identify “disguised employees” who are effectively working as staff members but receiving the tax benefits of a corporate entity.

Central to this scrutiny is the “Substitution” test. HMRC examines whether you have a genuine right to provide a suitably qualified replacement to perform your clinical duties if you’re unavailable. In a dental setting, this is often challenging. If the practice owner or the NHS contract requires you personally to treat patients, the right of substitution may be deemed non-existent. Your Associate Agreement must not only contain a substitution clause but also reflect a working reality where such a substitution is practically possible. Discrepancies between your contract and your daily surgery life are a primary target for tax inspectors.

The HMRC “Check Employment Status for Tax” (CEST) Tool

HMRC’s CEST tool is often the first port of call for determining status, yet it frequently returns an “Undetermined” result for dental professionals. This happens because the tool struggles with the unique clinical autonomy dentists possess. To defend your status, we focus on three pillars: Control, Mutuality of Obligation (MoO), and Financial Risk. Who decides your clinical hours? Is the practice obligated to provide a minimum number of UDAs? Do you bear the financial cost of remedial work? If your company is deemed “Inside IR35,” your take-home pay can drop significantly, as you’ll be taxed similarly to an employee without receiving the associated employment rights or benefits.

Mitigating the Risk of a Tax Investigation

Securing your financial position requires more than just a well-drafted contract; it requires a robust audit trail of independence. We recommend clinicians review the British Dental Association advice on incorporation to ensure their corporate governance aligns with industry standards. Defending your status is about proving you’re in business on your own account. This involves managing your own indemnity, providing your own small equipment where applicable, and accepting the risk of profit and loss. We’ve seen a marked increase in compliance checks following the HMRC tax warning 2026, making it essential to have specialist dental accountants who can provide a tailored defense of your self-employed or corporate status.

Practical Steps for Transitioning to a Limited Company

Transitioning to a corporate structure requires a meticulous approach to administrative detail to ensure the tax benefits aren’t undermined by procedural errors. While many clinicians wait for the start of a new tax year on 6 April, incorporation can occur at any point. However, mid-year transitions require a precise cut-off for your clinical income and expenses to avoid double-taxation or accounting overlaps. When weighing the associate dentist vs limited company tax dilemma, you must also consider the logistical burden of shifting your professional identity from an individual to a corporate entity.

The most critical legal step is the novation of your Associate Agreement. This process replaces your personal contract with a new agreement between the practice owner and your limited company. Without this, HMRC may argue that the income belongs to you personally rather than the company, negating any corporate tax advantages. You must also notify the General Dental Council (GDC) and your indemnity provider. Most insurers require a specific “entity cover” to protect the company itself, alongside your personal clinical indemnity. This ensures your professional protection aligns with your new business structure.

Modern compliance also demands a digital-first mindset. With Making Tax Digital (MTD) for Income Tax applying to self-employed individuals earning over £50,000 from April 2026, setting up dedicated business banking and cloud-based accounting software is no longer optional. These tools provide the transparency needed to manage your director’s loan account and dividend distributions with the precision HMRC expects. If you require a bespoke analysis of your practice’s potential, our dental tax specialist team can provide the necessary clarity.

Company Formation and Compliance

Establishing your company involves registering with Companies House and appointing yourself as a director, which carries specific fiduciary duties. You’ll need to understand how to find a chartered accountant who understands the dental sector to guide you through this setup. A major consideration is your NHS pension; only salary is pensionable, so a low-salary corporate strategy may significantly reduce your pension accrual compared to sole trader status.

Ongoing Administrative Responsibilities

As a director, you’re responsible for maintaining statutory registers and filing an annual Confirmation Statement. You must also manage the nine-month deadline for Corporation Tax payments following your company’s year-end. Given the complexity of quarterly reporting and director payroll, utilizing professional bookkeeping services is often the most reliable way to maintain compliance while focusing on your clinical work.

Strategic Tax Planning with Davis & Co LLP

Deciding on the optimal business structure is a pivotal moment in your clinical career, yet the choice between an associate dentist vs limited company tax model is rarely static. As your clinical sessions increase or your personal circumstances evolve, the structure that served you last year may no longer be the most efficient. At Davis & Co LLP, we position ourselves as more than just service providers; we act as strategic partners to dental professionals across the UK. Our niche expertise as specialist dental tax accountants allows us to look beyond the balance sheet, ensuring your financial arrangements reflect the specific realities of modern dentistry.

We believe that clarity is the foundation of confidence. This is why we provide a tailored “Incorporation Report” for every associate considering a transition. This bespoke document provides a side-by-side comparison of your projected take-home pay, accounting for the 2026/27 Corporation Tax rates and the potential impact on your NHS pension accrual. By quantifying the potential savings against the increased administrative costs discussed in previous sections, we help you identify the exact moment when incorporation becomes a strategic advantage rather than an administrative burden.

Our support extends into business growth acceleration and proactive cash flow management. We understand that a successful career requires a steady hand on organizational finances as much as clinical excellence. By maintaining a partner-led relationship, we provide the reliable oversight necessary to navigate sensitive commercial matters with discretion and intellectual rigour. We aim to make you feel secure and well-advised, providing a dependable constant in a volatile regulatory environment.

Comprehensive Dental Tax Solutions

Maintaining compliance in an era of quarterly digital reporting requires a proactive approach. We offer expert tax advice in the UK that covers annual compliance, director payroll, and strategic dividend planning. Our team monitors HMRC trends and dental industry shifts in real-time, allowing us to adjust your strategy before regulatory changes impact your bottom line. This level of individualized service ensures your practice remains robust against the scrutiny of IR35 and employment status reviews.

Secure Your Financial Future

Your professional structure should never exist in a vacuum. We integrate your business model with your personal tax services to ensure your long-term wealth is protected and your borrowing power remains strong. Whether you’re navigating the 2026 dividend tax increases or planning for a future practice purchase, our specialist team provides the sophisticated guidance your career deserves. Contact Davis & Co LLP for a specialist dental tax review to begin your consultation and secure your financial roadmap for 2026 and beyond.

Securing Your Clinical Income for the 2026 Tax Year

Navigating the choice between an associate dentist vs limited company tax model is a strategic journey that requires constant calibration. The 2026 tax landscape has moved beyond simple arithmetic; it’s now vital to balance corporate efficiency with the clinical autonomy HMRC expects. Success hinges on recognizing the precise financial thresholds for incorporation while ensuring your Associate Agreement remains robust under the scrutiny of IR35. Whether you’re optimizing your dividend strategy or safeguarding your NHS pension, your structure must reflect the specific nuances of your career stage.

We’ve been trusted advisors to the dental community as Chartered Certified Accountants since 1901. Our partner-led approach delivers the discretion and deep-seated expertise required to manage sensitive financial matters with professional gravitas. We encourage you to Book a Specialist Dental Tax Consultation with Davis & Co LLP for a tailored review of your professional trajectory. Your financial security is a vital component of your clinical success. We’re committed to ensuring your business structure provides the stability you need to focus on what matters most: your patients.

Frequently Asked Questions

Is a limited company always better for a dentist earning over £50,000?

No. While £50,000 was traditionally the benchmark for incorporation, the 2026 tax landscape requires a more nuanced analysis. The effective marginal Corporation Tax rate of 26.5% for profits above this level, combined with increased dividend tax rates, means the savings may be marginal. When you account for higher accountancy fees and the loss of NHS pension benefits, some associates find that remaining a sole trader is more financially sound.

Can I still claim my NHS pension if I work through a limited company?

Yes, but your contributions will be limited. In a corporate structure, only the salary you draw from the company is considered pensionable income; dividends are excluded entirely. This often leads to a significant reduction in your long-term pension accrual compared to the associate dentist vs limited company tax considerations for a sole trader, whose entire net profit (up to the cap) is typically pensionable.

What are the main disadvantages of incorporating my dental associate income?

The primary disadvantages include a significantly higher administrative burden and increased professional costs for company secretarial services. You also face stricter HMRC scrutiny regarding IR35 and employment status. Furthermore, as a company director, you’ll have legal fiduciary duties and must manage complex filing deadlines. The potential tax savings must be weighed against these ongoing operational requirements and the loss of pensionable earnings.

How does IR35 affect dental associates in 2026?

IR35 remains a critical concern for any dentist operating through a personal service company. HMRC uses these rules to identify “disguised employees” who should be taxed as staff members. In 2026, the focus is on clinical control and the genuine right of substitution. If your contract doesn’t reflect your actual working practices, you risk being deemed “Inside IR35,” which eliminates the tax advantages of incorporation.

Do I need a new contract with my dental practice if I incorporate?

Yes, you must undergo a process called novation to replace your existing personal contract with one between the practice owner and your new limited company. This is a vital step for tax compliance. Without a correctly drafted corporate contract, HMRC may argue that the clinical income belongs to you personally, which could negate the tax benefits of your corporate structure and trigger an investigation.

How much can I save in National Insurance by becoming a limited company?

Savings primarily arise because dividends are not subject to National Insurance contributions. For a self-employed associate, Class 4 National Insurance is 6% on profits up to £50,270 and 2% above that. While a limited company can reduce this liability, these savings are now frequently offset by the 2026 Corporation Tax rates and the frozen personal allowance, making a bespoke financial review essential before you decide.

What happens to my equipment and expenses when I move from sole trader to company?

You can typically sell your clinical equipment to your new company at its current market value. This transaction can create a credit on your director’s loan account, allowing you to withdraw that amount from the company tax-free later. Moving forward, all professional expenses must be paid directly from the company bank account to ensure they remain deductible against your Corporation Tax liability and maintain clear financial separation.

How often should I review my dental business structure with an accountant?

We recommend a formal review at least once a year, ideally well before the April tax year transition. However, you should seek a consultation immediately if your clinical sessions change significantly or if there are major shifts in government fiscal policy. Regular reviews ensure your structure remains optimized for your current profit levels and compliant with the latest HMRC guidance for the dental profession.