A workplace pension scheme is often viewed as a mere regulatory burden, yet it remains one of the most underutilised levers for corporate tax efficiency and talent retention in the UK. For many business owners, the complexity surrounding auto enrolment pension duties for employers feels like a constant administrative hurdle, particularly with the three-year re-enrolment cycles and the ever-present risk of The Pensions Regulator (TPR) fines. We understand that managing opt-outs and calculating qualifying earnings against the current £10,000 trigger can be taxing on your internal resources.

We’re here to help you move beyond the fear of non-compliance and transform these obligations into a strategic financial advantage. This guide provides the clarity you need to master your duties under the Pensions Act, ensuring every payroll run is precise and every contribution is optimised for your firm’s tax position. We’ll explore the latest 2026/27 thresholds, efficient payroll integration techniques, and how salary sacrifice structures can benefit both your organisation and your workforce.

Key Takeaways

- Understand how to accurately categorise staff to satisfy auto enrolment pension duties for employers and avoid common Real Time Information (RTI) reporting errors.

- Discover how implementing salary sacrifice arrangements can reduce your firm’s Class 1 National Insurance liabilities by 13.8% on qualifying contributions.

- Learn to manage the cyclical re-enrolment process with precision, ensuring all eligible staff who previously opted out are correctly reassessed.

- Align your workplace pension structure with your wider corporate strategy to optimise Corporation Tax positions and director remuneration.

The Architecture of Auto Enrolment Pension Duties for Employers

The legal framework governing workplace pensions has evolved significantly since the inception of the Pensions Act 2008. For the 2026 landscape, auto enrolment pension duties for employers represent more than a statutory box-ticking exercise; they’re a core element of corporate governance. The Pensions Regulator (TPR) continues to intensify its enforcement activities, focusing on firms that fail to maintain accurate records or neglect their ongoing Declaration of Compliance. This declaration must be submitted within five months of the duties start date and updated every three years during the re-enrolment window. Failing to do so signals a lack of internal control, often inviting closer scrutiny from regulatory bodies.

We view these duties as a baseline for professional practice. Beyond the initial setup, the complexity lies in the continuous assessment of a fluctuating workforce. Whether you’re managing a stable team or a high-turnover operation, the responsibility to identify and enrol eligible staff remains absolute. Compliance isn’t a static achievement but a rhythmic process that must be integrated into your monthly financial cycles. This ensures that the business remains protected from the escalating scale of TPR fines, which are designed to penalise persistent administrative negligence.

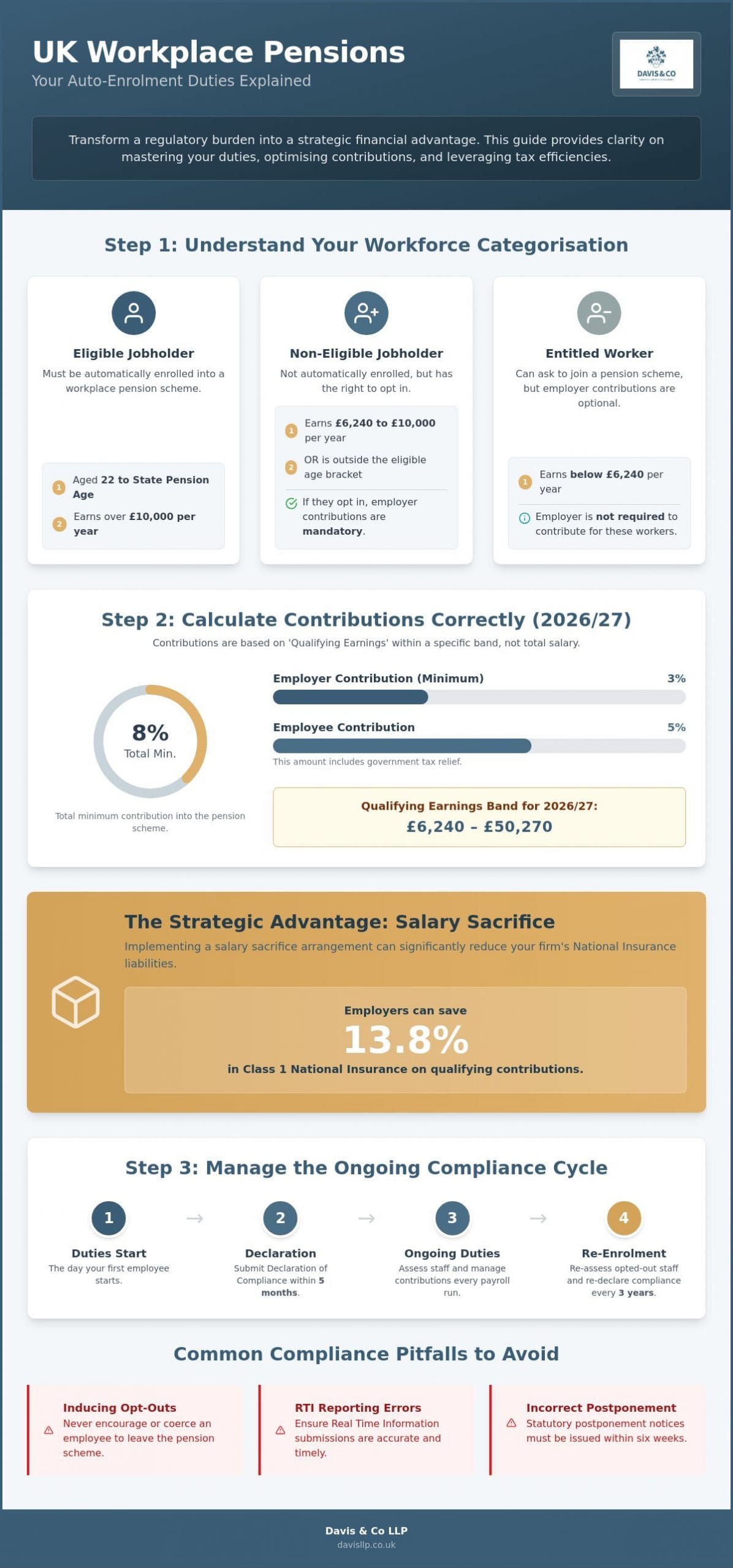

Determining Worker Status and Eligibility

Precision in worker categorisation is vital to avoid overpayment or the exclusion of entitled staff. Eligible jobholders are those aged between 22 and the State Pension age who earn more than the £10,000 annual earnings trigger. In the current high-inflation environment, wage growth often pushes staff across this threshold mid-year, requiring vigilant monthly monitoring. Non-eligible jobholders, who earn between £6,240 and £10,000 or fall outside the age bracket, have a right to opt-in. This action triggers mandatory employer contributions. Entitled workers earning below £6,240 may join a scheme, though you aren’t legally required to contribute to their fund.

The 2026 Contribution Framework

The financial architecture of a compliant scheme rests on the 8% total minimum contribution. Under the 2026/27 guidelines, employers must contribute at least 3% of qualifying earnings, while the employee provides the remaining 5%, inclusive of tax relief. It’s essential to distinguish between basic pay and qualifying earnings. For the 2026/27 tax year, qualifying earnings are calculated on the band between £6,240 and £50,270. As wages rise to meet market pressures, the total cost of these contributions increases proportionally. We find that integrating auto enrolment pension duties for employers directly into a robust payroll system is the most effective way to ensure accuracy while mitigating the administrative burden on your finance team.

Compliance Beyond the Basics: Avoiding Technical Breaches

Technical compliance often falters at the intersection of payroll data and regulatory reporting. While the initial setup of a scheme is a significant milestone, the ongoing auto enrolment pension duties for employers require meticulous attention to Real Time Information (RTI) submissions. Discrepancies between your internal payroll records and the data held by HMRC or The Pensions Regulator (TPR) are frequently the catalyst for a compliance check. These technical breaches often arise from simple timing errors or the miscalculation of contributions during pro-rata pay periods, such as when a new starter joins mid-month.

A clear understanding of your employer’s responsibilities is essential when managing the ‘opt-out’ window. You must remain entirely neutral throughout this period. Any suggestion that an employee should opt out to save the company money, or any attempt to coerce a worker into ceasing contributions, is strictly prohibited. Such actions carry severe penalties and reputational risks. To safeguard against these pitfalls, we recommend incorporating professional audit and assurance into your annual review process, ensuring that your internal communications and payroll logic remain beyond reproach.

Postponement and Assessment Strategies

Employers may choose to delay the assessment of a worker for up to three months, a tactic known as postponement. This is particularly effective for seasonal staff or roles with high initial turnover. However, this isn’t an automatic right; you must issue a statutory postponement notice to the individual within six weeks of the date they became eligible. Automating these triggers through tailored accounting services for small business ensures that no deadlines are missed. This protects the firm from administrative oversight while providing the flexibility needed to manage a dynamic workforce efficiently.

Record Keeping and Regulatory Scrutiny

The Pensions Regulator expects a robust and accessible audit trail. You’re required to retain records of all pension activities, including opt-out notices and contribution calculations, for at least six years. This requirement must be balanced with UK GDPR obligations, ensuring that sensitive personal data is stored securely and accessed only for compliance purposes. Preparing for a TPR audit involves more than just having the files; it requires a proactive approach to documentation that proves your systems are both accurate and consistent. Maintaining a precise record of your auto enrolment pension duties for employers ensures that you can respond to any regulatory inquiry with absolute confidence. Integrating these checks into your broader accounting services for small business provides a layer of security that internal teams often lack.

The Strategic Advantage: Salary Sacrifice and Cash Flow

While the previous sections focused on the architecture of compliance, viewing auto enrolment pension duties for employers solely as a cost centre is a missed opportunity. Sophisticated firms recognise that workplace pensions can be structured as a financial tool to enhance cash flow and corporate value. By moving beyond the basic contribution model and implementing salary sacrifice, also known as SMART (Salary Management and Retention) pensions, you can transform a statutory obligation into a fiscal advantage. This arrangement involves an employee agreeing to reduce their gross salary by an amount equal to their pension contribution, which the employer then pays directly into the scheme on their behalf.

The primary benefit for the organisation lies in the reduction of Class 1 National Insurance contributions. Because the employee’s gross pay is lower, the employer’s 13.8% NI liability is calculated on a reduced figure. For a firm with a significant headcount, these cumulative savings provide a meaningful boost to the bottom line. These retained funds aren’t merely administrative windfalls; they can be strategically redeployed into business growth acceleration. Reinvesting these NI savings can improve your EBITDA and overall company valuation, while the pension contributions themselves remain a deductible expense for Corporation Tax purposes.

Implementing Salary Sacrifice Correctly

Execution is everything. To stay compliant, you must update employment contracts to reflect that the reduction in pay is a permanent, contractual change rather than a temporary deduction. We also must ensure that no employee’s pay falls below the National Minimum Wage after the sacrifice is applied. Clear communication is the final pillar of a successful implementation. When staff understand that salary sacrifice often results in higher take-home pay due to their own NI savings, the scheme becomes a point of mutual benefit rather than a source of confusion.

Pensions as a Recruitment and Retention Tool

In the 2026 talent market, offering only the 3% mandatory minimum is rarely enough to attract high-calibre professionals. Many of our clients now utilise tiered contribution structures, where employer contributions increase based on seniority or length of service. This approach is particularly effective for senior management and directors, where pension planning often intersects with international tax planning for those with global interests. By positioning your auto enrolment pension duties for employers as a central part of a premium remuneration package, you foster long-term loyalty while maintaining a highly efficient tax profile for the business.

The Cyclical Burden: Re-enrolment and Ongoing Governance

The initial setup of a pension scheme is often seen as the primary hurdle, but the long-term integrity of your compliance relies on mastering the three-year re-enrolment cycle. This recurring obligation ensures that employees who previously opted out are given a fresh opportunity to save for retirement. For many directors, managing these periodic auto enrolment pension duties for employers becomes a significant administrative drain, especially when internal teams lose track of the specific deadlines set by The Pensions Regulator (TPR). We’ve observed that the most frequent point of failure isn’t the enrolment itself, but the secondary administrative steps that follow.

The re-declaration of compliance is perhaps the most critical document in this cycle. It’s not enough to simply re-enrol staff; you must formally notify the TPR that you’ve fulfilled your duties. This must be completed within five months of your third anniversary, even if you had no staff to re-enrol. Missing this deadline is a common trigger for automated fines. Our payroll services are designed to remove this uncertainty, providing a managed framework that handles assessment and reporting with clinical precision.

The 2026 Re-enrolment Framework

To maintain a compliant status, we recommend following a structured four-step process every three years:

- Step 1: Identify your re-enrolment date. You have a six-month window to choose a date, which typically falls three years from your original staging or last re-enrolment.

- Step 2: Assess your workforce. Review all staff who previously opted out or ceased contributions more than 12 months prior to your chosen date.

- Step 3: Issue statutory communications. You’re legally required to write to those being re-enrolled within six weeks of your re-enrolment date.

- Step 4: Submit the re-declaration. Complete the TPR online portal submission within five months of the anniversary of your staging date.

Managing Pension Provider Relations

Governance extends beyond the payroll file. In 2026, it’s vital to assess whether your chosen pension provider remains fit for purpose. High management charges or poor digital integration can erode the value of the benefit you’re providing. We often find that data discrepancies arise at the point of transfer between payroll software and the provider’s portal. Ensuring member data accuracy, such as correct National Insurance numbers and addresses, prevents the administrative headache of ‘lost’ pensions. To secure your firm against the risks of cyclical non-compliance, we invite you to explore how our tailored payroll services can manage these obligations on your behalf.

Professional Advisory: Integrating Pensions into Corporate Strategy

We view the management of auto enrolment pension duties for employers as a fundamental pillar of expert tax advice in the UK. It’s no longer sufficient to treat these requirements as a standalone payroll task. Instead, we integrate pension structures into a broader conversation about Corporation Tax efficiency and director remuneration. For directors, the ability to make significant employer contributions can be a highly effective way to extract profits from a company while reducing the immediate tax burden. This is particularly relevant for international firms operating UK subsidiaries, where local compliance must align with global corporate standards without exposing the parent company to unnecessary regulatory risk.

The intersection of these duties and corporate profitability is where professional oversight becomes invaluable. We help you move from viewing pensions as an administrative cost to seeing them as a strategic investment in your firm’s stability. By ensuring that your contribution levels and scheme choices are reviewed annually, we protect your EBITDA and enhance the overall financial health of the organisation. This proactive stance ensures that you aren’t just meeting the minimum requirements, but are actively using the framework to benefit the business’s long-term cash flow.

A Holistic Approach to Compliance and Growth

Our approach ensures that your pension strategies are never developed in isolation. They must align with your firm’s wider business growth and management accounting goals. As we look toward 2027, the legislative environment remains fluid. Potential shifts in the minimum enrolment age and contribution levels are already being discussed in policy circles. Having a Chartered Certified Accountant at your side allows you to anticipate these changes rather than reacting to them. We provide the intellectual rigour needed to mitigate TPR enforcement risks, ensuring your documentation is robust enough to withstand any regulatory audit.

Securing Your Business Future

Davis & Co LLP brings a sense of professional gravitas to every engagement. We understand that dealing with sensitive commercial matters requires a partner who is both traditional in values and modern in application. From our offices, we support national clients with complex payroll structures and multi-jurisdictional tax requirements. We don’t just process numbers; we provide a composed partnership that makes you feel secure in your advisory choices. To ensure your current systems are resilient for the years ahead, we recommend scheduling a strategic review of your auto enrolment pension duties for employers and your wider payroll infrastructure.

Securing Your Firm’s Strategic Resilience for 2027 and Beyond

The transition from viewing workplace pensions as a mandatory expense to a sophisticated financial asset is a hallmark of successful corporate governance. By mastering the technicalities of worker assessment and the significant National Insurance savings available through salary sacrifice, you protect your firm’s cash flow while fulfilling your legal obligations. We’ve seen how maintaining precise records and navigating the three-year re-enrolment cycle are essential for avoiding regulatory scrutiny and protecting your organisation’s EBITDA.

Effectively managing auto enrolment pension duties for employers requires a partner with deep-seated expertise and a history of success. Since 1901, Davis & Co LLP has acted as a trusted advisor, providing Chartered Certified expertise in complex payroll, international tax planning, and comprehensive management accounting. We invite you to consult with Davis & Co LLP for strategic payroll and pension compliance advice to ensure your organisation remains both compliant and competitive. Taking a proactive approach today ensures that your pension scheme remains a pillar of strength for your business and your workforce.

Frequently Asked Questions

What are the exact auto enrolment pension duties for employers in 2026?

Auto enrolment pension duties for employers in 2026 involve a continuous cycle of assessment, enrolment, and reporting. You must automatically enrol any worker aged 22 to State Pension age earning over £10,000 per year into a qualifying scheme. Beyond this, you’re required to make minimum contributions, issue statutory communications, and maintain a valid Declaration of Compliance with The Pensions Regulator. These duties ensure your payroll processes remain aligned with the statutory mandates of the Pensions Act.

How do I calculate the 8% minimum pension contribution correctly?

To calculate the 8% minimum correctly, you must apply the relevant percentages to the worker’s qualifying earnings. For the 2026/27 tax year, this is the band of gross pay between £6,240 and £50,270. The employer contributes a minimum of 3%, while the employee provides 5%, which typically includes government tax relief. You may also calculate contributions based on total earnings or basic pay, provided the resulting amount meets or exceeds the statutory minimum.

Can an employer opt out of auto enrolment duties?

No, an employer cannot opt out of these legal obligations. If you employ at least one person who meets the criteria for a worker, you have a statutory duty to provide a workplace pension. Even if your staff choose to opt out after being enrolled, your initial auto enrolment pension duties for employers remain mandatory. Attempting to avoid these responsibilities is a direct breach of the Pensions Act 2008 and carries significant legal risk.

What happens if I miss the re-enrolment deadline?

Missing the re-enrolment or re-declaration deadline typically triggers an immediate compliance check from The Pensions Regulator. You may receive a fixed penalty notice of £400 as an initial deterrent. If the breach isn’t rectified promptly, the regulator can issue escalating penalty notices that accrue on a daily basis. We recommend setting internal milestones six months ahead of your three-year anniversary to ensure all statutory filings are completed with precision.

Does auto enrolment apply to directors without employment contracts?

Auto enrolment generally doesn’t apply to a business if the only people working for it are directors who don’t have employment contracts. However, if a director has a contract of employment and at least one other person works for the company, the duties may be triggered for that director. This is a nuanced area of corporate governance, and we advise a specific review of your contractual arrangements to confirm your firm’s exemption status.

How does salary sacrifice affect my National Insurance as an employer?

Salary sacrifice arrangements lower your employer National Insurance (NI) liability because they reduce the employee’s gross contractual pay. By paying the pension contribution directly as an employer cost, you avoid the 13.8% Class 1 NI charge on that specific portion of earnings. This creates a more efficient tax structure for the organisation while potentially increasing the employee’s net take-home pay, provided the arrangement is correctly reflected in their terms of employment.

What are the penalties for non-compliance with The Pensions Regulator?

The Pensions Regulator utilizes a tiered penalty system to enforce compliance across the UK. Initial fixed penalties are usually £400, but escalating penalties can reach between £50 and £10,000 per day depending on your total headcount. These fines are designed to be punitive and are rarely waived for simple administrative oversights. Maintaining a robust and transparent audit trail is the only reliable defense against such regulatory action and the associated financial loss.

Do I need to pay into a pension for staff who earn less than £10,000?

You aren’t required to automatically enrol staff earning less than the £10,000 trigger, but you may still have mandatory contribution duties. If a worker earns between £6,240 and £10,000, they are classified as non-eligible jobholders and have the right to opt in to your scheme. If they exercise this right, you must pay the 3% employer contribution. For those earning below £6,240, you must provide access to a pension, but employer contributions remain optional.