The 2025 Budget has fundamentally redefined the United Kingdom’s fiscal identity, transitioning the nation into a high-investment “new normal” where passive compliance is no longer a viable strategy for wealth preservation. For those managing global portfolios, the uk budget impact on international investors represents a significant shift in how capital must be structured to remain efficient. We recognize that the prospect of a 25% main rate for Corporation Tax and the freezing of personal allowances until 2031 introduces a layer of complexity that can feel restrictive.

We’ve prepared this strategic analysis to help you manage these changes with the composure that comes from deep expertise. You’ll gain a clear understanding of the new five-tier business rate multipliers and the £2.5 million cap on Agricultural and Business Property Relief effective from April 2026. This guide provides a refined framework for adapting your cross-border financial strategies, ensuring your UK interests remain resilient and fully compliant within this evolving landscape. We’ll examine the specific thresholds and relief adjustments that will define your fiscal obligations in the coming year.

Key Takeaways

- Evaluate the long-term uk budget impact on international investors as the national fiscal policy shifts toward a 38% tax-to-GDP ratio.

- Gain clarity on the new five-tier business rate multipliers to protect your UK-based hospitality and retail profit margins.

- Prepare for the 2026 Inheritance Tax changes by understanding the new relief caps on agricultural and business assets.

- Implement a structured tax health check to ensure your cross-border financial strategies remain compliant with the latest UK sustainability reports.

- Discover how highly individualized tax planning can secure your personal and organizational wealth against rising fiscal drag.

The 2025 Budget and the UK Economic Landscape for 2026

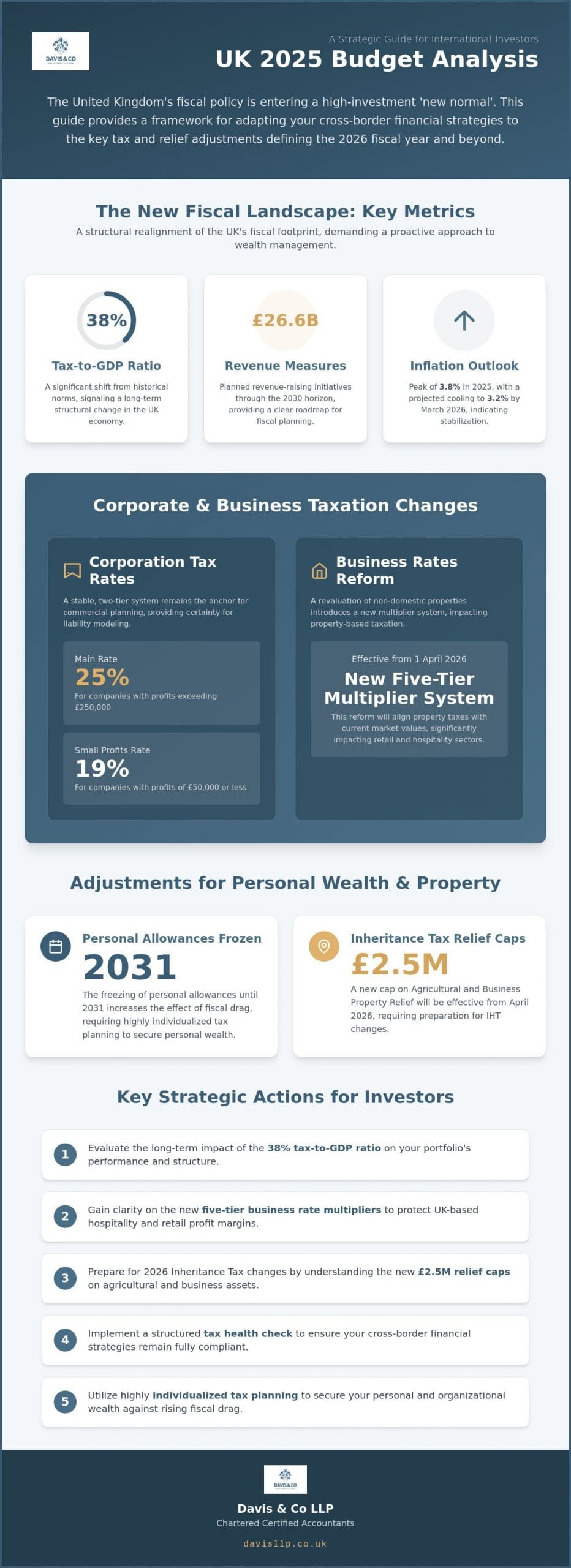

The Chancellor’s second budget, delivered in late 2025, established a definitive trajectory for the British economy. It signalled a transition toward a 38% tax-to-GDP ratio, a level that represents a significant departure from historical norms. For those overseeing global capital, the uk budget impact on international investors is not merely found in immediate tax rates, but in the long-term structural realignment of the state’s fiscal footprint. This shift is supported by £26.6bn in revenue-raising measures planned through the 2030 horizon. It provides a clear, if demanding, roadmap for the years ahead, allowing for more precise cross-border financial planning and risk assessment.

Planning for the 2026 fiscal year requires a nuanced understanding of the 2025 inflationary peak. With inflation reaching 3.8% in 2025, businesses have had to adjust their cost structures and pricing models with care. This peak informs the more measured approach we see in 2026. The emphasis has shifted from crisis management to sustainable growth within a higher-tax environment. We find that this context is vital for organizations looking to maintain profit margins while navigating the complexities of the new fiscal landscape. It’s a period that rewards those who prioritize stability over aggressive, high-risk expansion.

The Macro-Economic Context for 2026

The UK Economic Landscape for 2026 is defined by a focus on “Strong Foundations” and public investment. While GDP growth remains modest, the Bank of England’s 3.2% inflation projection for March 2026 suggests cooling price pressures. This stabilization is essential for international investors who rely on predictable monetary conditions. Stability here isn’t just about low taxes; it’s about the reliability of the fiscal rules governing the market. We believe this predictability is a cornerstone of business stability, allowing for more confident long-term capital commitments in a volatile global market.

Key Revenue-Raising Objectives

The government’s primary challenge remains the balance between necessary public spending and fiscal sustainability. The 2025 Budget prioritises long-term fiscal sustainability by anchoring public spending against a 38% tax-to-GDP target, ensuring that revenue-raising measures align with the government’s broader economic stability goals. When evaluating the uk budget impact on international investors, one must look at how these objectives create a more predictable operating environment. The “fiscal headroom” buffer, cited at £21.7bn for the 2029/30 period, acts as a safeguard for the state. Recognizing this commitment helps us structure your interests with the confidence that the fiscal ground remains stable.

Corporate Tax and Business Rates: Implications for UK Companies

While the broader fiscal landscape has shifted, the relative stability of the UK’s Corporation Tax regime remains a vital anchor for commercial planning. The main rate of 25% for companies with profits exceeding £250,000, alongside the 19% small profits rate for those earning £50,000 or less, provides a baseline for assessing the uk budget impact on international investors. This consistency allows organizations to model their long-term liabilities with a degree of certainty that is often absent in other jurisdictions. However, this stability at the top level is balanced by more granular changes in property-based taxation and operational costs that require careful attention.

The 1 April 2026 revaluation of non-domestic properties introduces a new five-tier multiplier system in England. This reform is particularly pertinent for those holding extensive commercial property portfolios or operating within the retail and hospitality sectors. High-value multipliers may exert downward pressure on net yields, necessitating a proactive approach to overhead management. We find that the impact on physical retail overheads in 2026 will be significant for firms that haven’t yet adjusted their valuation expectations.

Business Rates Reform and Investment

Businesses should also monitor the ongoing ‘Call for Evidence’ on Business Rates, as the findings will likely shape the next phase of property tax reform. The government’s focus on revaluation reflects a desire to align property taxes more closely with current market values, though this can create volatility for long-term leaseholders. Effective cash flow management is essential here to offset these rising property-based taxes and maintain operational liquidity. It’s a matter of ensuring that your growth strategy accounts for these localized cost increases before they impact your bottom line.

Operational Compliance and Customs

Operational compliance is also evolving, specifically regarding the customs treatment of low-value imports. These reforms aim to modernize e-commerce frameworks but may initially increase administrative burdens for firms relying on international supply chains. We’re also seeing a continued focus on the Digital Services Tax and efficiency projections from the Office for Value for Money. These measures suggest a lean approach to future public sector spending and a rigorous environment for tech-enabled firms. Preparing for these efficiency benchmarks is a prudent step for any organization looking to demonstrate value in the UK market.

The uk budget impact on international investors often manifests in these operational nuances rather than headline rate changes. Aligning your business structure with these changes requires a partner who understands the nuance of UK compliance; our team provides the international tax planning expertise needed to protect your commercial interests and ensure your UK operations remain resilient.

Personal Wealth and Property: Strategic Adjustments for 2026

The transition into the 2026 fiscal year requires a refined approach to personal wealth preservation, particularly as the uk budget impact on international investors becomes more pronounced through the mechanism of fiscal drag. While headline income tax rates have remained stable, the decision to maintain the freeze on the personal allowance at £12,570 until 2031 means that more of your global income may fall into higher tax brackets as nominal values rise. For high-net-worth individuals, the adjustments to Air Passenger Duty on private aviation further signal a shift toward taxing lifestyle assets, necessitating a broader review of annual expenditure and liquidity requirements.

Managing a property portfolio in this high-interest, high-tax environment requires sophisticated property accounting. With the Bank of England base rate at 3.75% as of June 2026, the cost of debt remains a significant factor in net profitability. Investors must now balance these financing costs against the 24% Capital Gains Tax rate for higher-rate taxpayers and the non-resident Stamp Duty Land Tax surcharges, which can reach 14% for properties above £1.5 million. We help our clients navigate these implicit liabilities by ensuring their balance sheet frameworks are optimized for both current cash flow and long-term capital appreciation.

Inheritance Tax and Estate Planning

The 2026 Inheritance Tax landscape is defined by the introduction of a £2.5 million cap on 100% Agricultural and Business Property Relief, effective from 6 April 2026. This change represents a fundamental shift for those with significant UK business interests or landed estates, as value exceeding this threshold will now attract a 20% effective tax rate. Integrating international tax planning into your estate strategy is no longer optional; it’s a requirement for maintaining the integrity of cross-border legacies. Our trust tax services focus on maintaining compliance within this shifting regulatory framework, ensuring that gifting strategies are executed with precision to maximize available exemptions.

Specialist Considerations for Professionals

As a dental tax specialist, we’ve observed that the 2025 Budget announcements have directly influenced practice valuations and associate pay structures. The combination of business rate adjustments and the evolving tax treatment of professional goodwill requires a proactive stance on practice accounting. For property investors and medical professionals alike, the nil-rate band for Inheritance Tax remains frozen at £325,000 until April 2031, a policy that continues to increase the effective tax burden through fiscal drag. We work closely with our clients to implement highly individualized strategies that address these niche pressures, ensuring that both organizational and personal wealth are protected against the complexities of the 2026 fiscal landscape.

Strategic Tax Planning: Future-Proofing Your UK Interests

The transition into the 2026 fiscal landscape necessitates a move from reactive compliance to a forward-looking strategy. Conducting a comprehensive 2026 tax health check is the foundational step for any organisation seeking to maintain its competitive edge. This process involves more than just reviewing current liabilities; it requires a deep analysis of how the uk budget impact on international investors will affect long-term capital allocation. By identifying potential vulnerabilities early, we can implement structures that protect your profit margins and ensure your UK operations remain a robust component of your global portfolio.

Optimising International and Cross-Border Tax

Responding to the 2025 fiscal risks requires a sophisticated understanding of the interaction between domestic policy and global standards. As the UK aligns with global minimum tax standards, the strategic use of double taxation treaties becomes paramount for maintaining fiscal efficiency. We focus on ensuring that your cross-border interests are not only compliant but also structured to leverage available reliefs. Securing expert tax advice in the UK allows you to manage these complexities with the confidence that your wealth is being overseen by professionals who understand the nuances of international law. This proactive approach is essential for mitigating the impact of rising tax-to-GDP ratios on your mobility and capital growth.

Growth Acceleration and Cash Flow

Accelerating business growth in a high-tax environment relies on the intelligent use of R&D and investment allowances. These incentives remain a cornerstone of the UK’s strategy to attract high-value industries like life sciences and clean energy. We utilise detailed management accounts to identify tax-efficient reinvestment opportunities, ensuring that every pound of expenditure is working toward your long-term objectives. Management accounts are no longer just a reporting tool; they are a strategic asset for monitoring the fiscal headroom at the firm level. They allow you to respond to 10-year efficiency projections with agility and precision.

Bridging the gap between simple compliance and strategic advisory is where Chartered Certified Accountants provide the greatest value. Our team acts as a strategic partner, helping you manage the organizational impact of complex fiscal issues while maintaining the necessary professional distance of a trusted advisor. If you are ready to secure your UK interests against the upcoming fiscal shifts, contact our specialist team to begin your 2026 strategic review.

Navigating Fiscal Uncertainty with Davis & Co LLP

The complexities of the 2026 fiscal year require more than just technical expertise; they demand a relationship rooted in composed partnership and professional gravitas. As we’ve detailed, the uk budget impact on international investors is multifaceted, touching everything from inheritance tax caps to corporate multipliers. We don’t believe in one-size-fits-all solutions. Instead, our approach moves logically from understanding the general economic context to delivering highly individualized, actionable solutions for our clients. Whether you’re an international family managing cross-border assets or an SME adjusting to new business rate tiers, we provide the steady guidance needed to protect your interests.

Reliability and discretion are the cornerstones of our practice. We understand that personal and commercial tax matters are sensitive. Our role as a strategic partner is to ensure you feel secure and well-advised, maintaining the necessary professional distance to offer objective, high-calibre advice. By focusing on the human and organizational impact of these complex issues, we bridge the gap between abstract policy and practical reality. This ensures that every decision is made with a clear understanding of its long-term implications for your wealth and operations.

Why a Strategic Partner Matters in 2026

In a high-scrutiny environment, the value of independent audit and assurance cannot be overstated. It provides the intellectual rigour necessary to validate your financial position and ensure long-term stability. Our 125-year history as Chartered Certified Accountants informs our contemporary application of tax law, allowing us to draw on a legacy of success while addressing modern challenges like global minimum tax standards. This history isn’t just a record of the past; it’s a foundation of deep-seated expertise that we bring to every bespoke tax plan. We apply the same precision required in complex analytical thought to every client’s specific needs, ensuring that organizational and individual service areas receive equal weight.

Next Steps for Your 2026 Financial Strategy

Proactive planning is the only effective hedge against fiscal uncertainty. We recommend beginning with a comprehensive tax review to assess the specific Budget 2025 impacts on your portfolio. Our specialist teams are available to provide tailored advice for your unique circumstances:

- International Tax Planning: Ensuring cross-border efficiency and compliance with evolving global standards.

- Dental Tax Specialist: Addressing the specific practice valuation and associate pay pressures facing medical professionals.

- Property Accounting: Optimising balance sheets for investors navigating high-interest environments.

Engaging our specialists early allows you to transition into the 2026 fiscal landscape with confidence. We’re here to ensure your financial strategy remains resilient, serving as the dependable constant in an often volatile fiscal world.

Securing Your Fiscal Resilience for the 2026 Landscape

The transition to a more demanding fiscal environment requires a fundamental shift from simple compliance to a sophisticated, cross-border architecture. We’ve explored how the uk budget impact on international investors manifests through the mechanism of fiscal drag, the freezing of personal allowances until 2031, and the new £2.5 million cap on business property reliefs. Managing these variables with precision ensures that your UK interests remain a source of resilience within your broader global portfolio. It’s about transforming these regulatory shifts into a structured plan for long-term growth.

As Chartered Certified Accountants since 1901, we bring over a century of reliability to the management of your financial affairs. Our specialist dental tax experts and practitioners in expert international tax planning provide the nuanced, highly individualized guidance necessary for sensitive commercial and personal matters. By aligning your strategy with the latest sustainability reports and fiscal rules, we help you maintain the confidence that your wealth is well-protected. We invite you to secure your 2026 financial future with a strategic tax consultation from Davis & Co LLP. We’re ready to help you navigate these changes with clarity and the reassurance of a composed partnership.

Frequently Asked Questions

What were the main revenue-raising measures in the 2025 Budget?

The primary revenue-raising measures involve a £26.6bn target through the 2030 horizon, aimed at establishing a 38% tax-to-GDP ratio. These adjustments focus on structural fiscal sustainability rather than singular headline rate hikes. For investors, this signals a long-term commitment to public investment funded by a broader tax base. Understanding these objectives is essential for assessing the stability of the UK as a destination for global capital.

How does the 2025 Budget affect UK Corporation Tax in 2026?

Corporation Tax remains stable in 2026, with the main rate held at 25% for companies with profits exceeding £250,000. Smaller entities continue to benefit from the 19% small profits rate on earnings of £50,000 or less. This tiered system, including marginal relief for profits in between, provides a predictable framework for business investment. We view this stability as a cornerstone of the current fiscal landscape for corporate entities.

Are there changes to Inheritance Tax (IHT) following the latest Budget?

Significant adjustments to Inheritance Tax take effect on 6 April 2026, specifically regarding Agricultural and Business Property Relief. A new £2.5 million cap applies to 100% relief; value exceeding this threshold receives 50% relief, resulting in an effective tax rate of 20%. The nil-rate band remains frozen at £325,000 until 2031. These changes necessitate a thorough review of estate planning and gifting strategies to protect family legacies.

What is the ‘fiscal headroom’ mentioned in the Budget 2025 forecasts?

Fiscal headroom refers to the margin between the government’s current spending plans and its self-imposed fiscal rules. The 2025 Budget forecasts a headroom of £21.7bn for the 2029/30 period. This buffer is designed to absorb economic shocks without requiring immediate tax increases or spending cuts. For international investors, a healthy headroom suggests a more stable and predictable fiscal environment, reducing the likelihood of sudden policy reversals.

How should dental professionals adapt to the 2025 Budget changes?

Dental professionals should focus on practice valuations and associate pay structures, which are directly influenced by business rate reforms and evolving tax treatments of professional goodwill. The 2025 Budget changes require a proactive stance on practice accounting to maintain profit margins. As a dental tax specialist, we recommend a strategic review of your balance sheet to manage implicit liabilities and ensure your practice remains financially resilient.

Will Business Rates increase for retail and hospitality in 2026?

Yes, a revaluation of non-domestic properties takes effect on 1 April 2026, introducing a new five-tier multiplier system in England. This reform will specifically impact the overheads of physical retail and hospitality businesses. High-value commercial properties may face increased rates, making strategic cash flow management essential. Businesses should monitor these multipliers closely to adjust their 2026 operational budgets and protect their bottom line.

What does the 38% tax-to-GDP ratio mean for my personal tax planning?

A 38% tax-to-GDP ratio indicates a transition to a high-tax, high-investment economy where fiscal drag becomes a primary concern. With personal tax thresholds frozen until 2031, rising nominal wages will naturally pull more taxpayers into the 40% and 45% brackets. This environment rewards sophisticated tax planning that utilizes all available reliefs and allowances. It’s a shift that requires a more structured approach to personal wealth preservation.

How can an international tax advisor help with the 2025 Budget adjustments?

An international tax advisor provides the expertise needed to navigate the uk budget impact on international investors by optimizing cross-border interests through double taxation treaties. We help you respond to fiscal risks with highly individualized strategies that bridge the gap between compliance and advisory. Our role is to act as a strategic partner, ensuring your global portfolio remains efficient while adhering to the UK’s evolving regulatory standards.