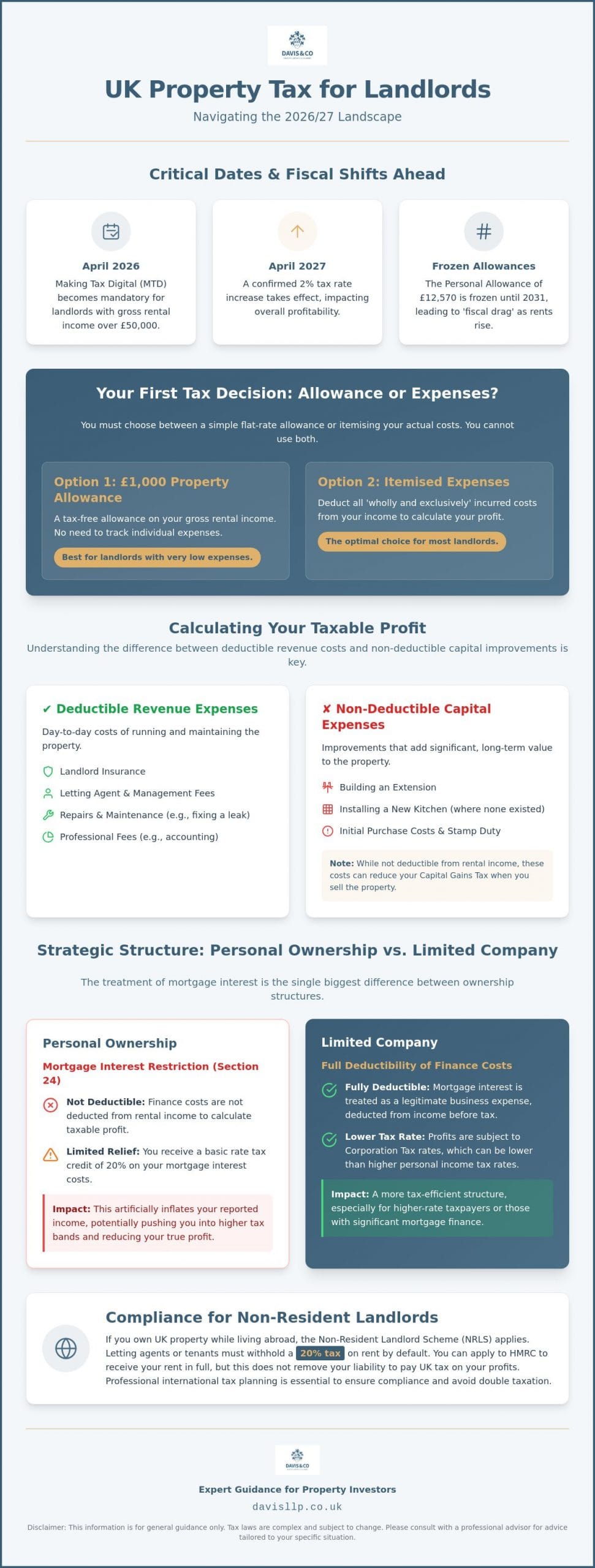

With the arrival of April 2026, more than 500,000 property owners have been pushed into higher tax brackets, fundamentally changing the landscape for tax on rental income uk. The transition to Making Tax Digital for Income Tax is no longer a future concern; it’s a live requirement for those with gross rental income exceeding £50,000. We understand that the pressure of quarterly reporting, alongside the intricate limitations of the 20% mortgage tax credit, can create a sense of unease regarding HMRC compliance.

We’re here to provide the professional clarity needed to manage these obligations with confidence. This guide explores how to maximize your tax efficiency through a precise application of allowable expenses and provides a clear roadmap for the new digital reporting standards. We’ll also help you determine if a limited company structure offers a more sustainable path for your portfolio before the confirmed 2% tax rate increase takes effect in April 2027. Our approach focuses on long-term stability, ensuring your property investments remain both compliant and profitable in an evolving fiscal environment.

Key Takeaways

- Understand the critical distinction between the £1,000 property allowance and itemised expenses to ensure you secure the most beneficial relief.

- Identify deductible revenue expenses under the ‘wholly and exclusively’ rule to mitigate your liability for tax on rental income uk.

- Compare the long-term fiscal benefits of personal ownership against limited company incorporation, particularly concerning mortgage interest relief.

- Navigate the mandatory shift to Making Tax Digital for ITSA ahead of the April 2026 deadline for landlords with rental income exceeding £50,000.

- Leverage professional property accounting to align your tax obligations with broader wealth preservation and strategic portfolio growth.

Understanding the UK Rental Income Tax Framework for 2026

In the UK, rental income tax is applied to the net profits you generate from letting out residential or commercial property. It’s not a standalone tax; instead, your property profits are aggregated with your other income sources, such as salary or dividends, to determine your overall liability. For the 2026/27 tax year, the UK Personal Allowance remains at £12,570. This means you only begin paying tax on rental income uk once your total taxable income exceeds this threshold. Because income tax thresholds are frozen until 2031, many landlords find themselves drifting into higher tax bands as rents rise, a phenomenon known as fiscal drag.

HMRC provides a £1,000 tax-free property allowance for individuals with modest rental receipts. If your gross income is below this amount, it’s effectively tax-free and doesn’t need to be declared. However, for most established landlords, actual deductible expenses far exceed this figure. You must choose between claiming the flat £1,000 allowance or deducting your actual costs; you cannot do both. If your annual rental income falls between £2,500 and £10,000 after allowable expenses, you generally report this via a Self Assessment tax return. For those earning more, the reporting requirements become more rigorous, particularly with the onset of digital transitions.

What Counts as Taxable Rental Income?

Taxable income extends beyond the monthly rent check. It encompasses any payments received for services you provide as a landlord, including utility payments, service charges, or even non-refundable deposits you’ve kept at the end of a tenancy. Following recent legislative shifts, the preferential treatment of Furnished Holiday Lets has been largely removed, aligning them more closely with standard buy-to-let properties. Gross rental income is the total amount of money received from tenants before any deductions, allowances, or expenses are applied for tax purposes.

Non-Resident Landlords and International Tax

Owning property in the UK while residing abroad introduces specific compliance challenges. Under the Non-Resident Landlord Scheme (NRLS), letting agents or tenants are typically required to withhold 20% of the rent to cover potential tax liabilities. You can apply to HMRC to receive your rent in full, but this doesn’t exempt you from the underlying tax obligation. Managing these cross-border complexities requires a nuanced approach to International tax planning to ensure you aren’t subject to double taxation or unnecessary penalties. We work closely with our clients to reconcile UK property profits with their global tax positions, maintaining full transparency with HMRC.

Calculating Taxable Profit: Allowable Expenses and Finance Costs

Determining your taxable profit requires a disciplined approach to record-keeping. The primary criterion for any deduction is the ‘wholly and exclusively’ rule. This standard dictates that an expense must be incurred solely for the purpose of your property business to be eligible for relief. Common examples include letting agent management fees, landlord insurance premiums, and the costs associated with professional property accounting. When you are paying tax on your rental income, ensuring these costs are meticulously documented is vital for both efficiency and compliance. Our team regularly assists clients in structuring their accounts to reflect these nuances accurately, providing a foundation for long-term fiscal health.

A frequent point of confusion involves the distinction between revenue and capital expenditure. Revenue costs are those incurred during the day-to-day maintenance of a property, such as repairing a leaking roof, replacing a broken window, or repainting between tenancies. These are fully deductible from your rental income. Capital expenditure, conversely, involves improvements that add significant value or extend the property’s life, like building an extension or installing a completely new kitchen where a basic one previously existed. While these aren’t deductible from your annual rental profits, they’re often essential for reducing future Capital Gains Tax liabilities when you eventually dispose of the asset.

Managing Mortgage Interest and Section 24

The landscape for finance costs remains defined by the Section 24 restrictions. You can’t deduct mortgage interest or other finance costs from your rental income before calculating your tax liability. Instead, you receive a tax reduction equal to 20% of these costs. This mechanism is particularly impactful for higher-rate taxpayers. Because the tax on rental income uk is calculated on the gross profit before interest is considered, it’s common for landlords to find themselves pushed into the 40% or 45% bands. This occurs because the total income, including the disallowed interest, is used to determine your marginal tax rate, even if your actual cash flow is significantly lower.

Capital Allowances and Replacement of Domestic Items

For residential lets, the Replacement of Domestic Items relief allows you to claim for the cost of replacing furniture, appliances, and floor coverings. It’s important to differentiate between a ‘renewal’ and an ‘improvement.’ Replacing a worn carpet with one of similar quality is a renewal; upgrading to premium hardwood flooring is likely an improvement. This relief applies only to the replacement of items, not the initial furnishing of a property. For those managing more complex portfolios or commercial assets, seeking Expert tax advice uk can help clarify these distinctions and ensure no legitimate relief is overlooked, particularly where capital allowances for integral features might apply.

Strategic Structure: Personal Ownership vs. Limited Companies

Choosing the right legal vehicle for property investments is a decision that extends far beyond immediate cash flow. Personal ownership remains the default for many, but the widening gap between personal income tax and corporation tax rates has prompted a significant shift toward incorporation. While personal owners benefit from the official government guidance on tax regarding the use of their personal allowance, higher-rate taxpayers often find the inability to deduct mortgage interest from their gross receipts a significant burden. In a limited company, finance costs are treated as a standard business expense, allowing for full deductibility before corporation tax is applied. This structural nuance is a primary factor when calculating the long-term tax on rental income uk for expanding portfolios.

We often advise clients to consider the friction costs of transitioning between these structures. Transferring an existing property into a limited company is legally treated as a sale at market value. This event triggers Capital Gains Tax for the individual and Stamp Duty Land Tax for the company, including the surcharge for additional dwellings. For many landlords, these upfront costs can outweigh the annual tax savings for several years, making incorporation a strategy more suited to new purchases rather than the restructuring of existing assets.

When a Limited Company Makes Strategic Sense

For those focused on portfolio expansion, a corporate structure serves as an efficient engine for reinvestment. Profits retained within the company aren’t subject to personal income tax, providing a larger pool of capital for further acquisitions. This approach is also effective for succession planning, as shares can be transferred to heirs more flexibly than physical property titles. Engaging a Small business accountant is essential to navigate the administrative complexities and ensure the company remains compliant with both Companies House and HMRC standards.

The Personal Ownership Advantage

Personal ownership offers a level of simplicity and immediate access to funds that a company cannot match. Individuals benefit from a £3,000 Capital Gains Tax exempt amount and lower reporting overheads compared to the statutory filing requirements of a limited company. However, extracting profit from a company involves navigating dividend tax rates, which increased in April 2026 to 10.75% for basic rate and 35.75% for upper rate taxpayers. Corporate landlords face a distinct risk of double taxation where profits are taxed first at the corporate level and then again upon personal extraction as dividends. This makes personal ownership a compelling choice for those who require regular access to their tax on rental income uk profits for personal lifestyle costs.

Compliance and the Shift to Making Tax Digital (MTD) in 2026

The April 2026 deadline marks a definitive shift for landlords with gross rental income exceeding £50,000. This isn’t merely a change in format; it’s a fundamental restructuring of how you interact with HMRC. Managing the tax on rental income uk now requires a transition from retrospective annual reporting to a proactive, digital-first approach. Under Making Tax Digital (MTD) for Income Tax Self-Assessment (ITSA), the traditional once-a-year filing is replaced by a requirement to maintain digital records and provide quarterly summaries of your income and expenses.

These quarterly updates provide HMRC with a more frequent view of your financial position, though they don’t necessitate a full tax payment every three months. Instead, they act as a digital bridge toward your final liability. To ensure accuracy, you must use functional compatible software that can connect directly to HMRC’s systems via an Application Programming Interface (API). Failure to adhere to these timelines now triggers a points-based penalty system. Each late submission results in a point; once a specific threshold is reached, a financial penalty is applied, making consistent compliance a prerequisite for avoiding unnecessary costs. This system is designed to penalise persistent lateness rather than isolated errors, yet the cumulative effect can be significant for complex portfolios.

Preparing Your Property Records for MTD

Transitioning to digital record-keeping shouldn’t be a solitary endeavour. While many software options exist, selecting a platform that aligns with your specific portfolio complexity is vital. We work with our clients to implement systems that not only meet HMRC requirements but also provide real-time insights into cash flow and profitability. This level of oversight is particularly important given the recent HMRC tax warning regarding broader compliance checks. If you’re concerned about your readiness for these digital obligations, our property accounting services can provide the necessary structural support to ensure a seamless transition.

MTD Roadmap for 2027 and Beyond

The current threshold of £50,000 is only the first phase of a broader rollout. From April 2027, the mandate extends to those with rental income over £30,000, and eventually to those earning over £20,000 by 2028. Proactive digitisation of your records today avoids the friction of a rushed transition as these deadlines approach. The Final Declaration serves as the definitive annual consolidation of your property profits alongside any non-business income, effectively replacing the traditional Self Assessment return. By consolidating your data through a single digital channel, you reduce the risk of reporting discrepancies that often trigger tax on rental income uk investigations.

Strategic Property Tax Planning with Davis & Co LLP

Effective management of your property assets requires a transition from reactive filing to proactive fiscal stewardship. At Davis & Co LLP, we view the tax on rental income uk not as an isolated annual obligation, but as a critical component of your broader financial architecture. Our role as strategic partners is to provide the foresight necessary to navigate a landscape where thresholds are frozen and reporting requirements are increasingly digitised. By integrating property accounting with a deep understanding of your long-term objectives, we help you maintain a portfolio that is both tax-efficient and resilient to the fiscal drag currently impacting many UK landlords.

We specialise in helping clients mitigate the restrictive effects of Section 24. While the 20% tax credit is a fixed mechanism, the way your portfolio is structured can significantly alter your effective tax rate. Whether through income splitting, the strategic use of trusts, or the incorporation models discussed earlier, we provide the analytical rigour required to make informed decisions. For international investors, our expertise in international tax planning ensures that UK property interests are managed with full consideration of cross-border obligations and treaty benefits. We draw on over 120 years of history to provide a level of reliability that is essential for complex, high-value portfolios.

Our Approach to Individualised Service

The complexity of modern HMRC compliance demands a higher level of professional scrutiny. We provide a discreet and highly individualised service, acting as a robust shield against the risks of incorrect reporting or late MTD submissions. For those managing assets through complex trusts or family offices, our approach focuses on maintaining the delicate balance between transparency and discretion. Knowing how to find a chartered accountant who understands the nuances of high-value property portfolios is the first step toward securing your financial standing and peace of mind.

Securing Your Property Legacy

A successful property strategy must account for the eventual transfer of wealth. We assist our clients in aligning their current tax on rental income uk obligations with their inheritance tax and succession goals. Our strategic planning focuses on several key areas:

- Structuring assets to facilitate tax-efficient succession for future generations.

- Protecting the portfolio against the 2% tax increase confirmed for April 2027.

- Maintaining liquidity while reinvesting profits into strategic growth.

This long-term perspective ensures that the value you’ve built isn’t eroded by future legislative shifts or unplanned tax events. By positioning your portfolio within a stable and considered framework, we help you preserve your assets for the next generation. To discuss how we can refine your current property structure for 2026 and beyond, we invite you to consult with our property tax specialists today.

Securing Your Property Assets for a Digital Future

The arrival of 2026 marks a significant juncture where property ownership intersects with mandatory digital transparency. Successfully managing tax on rental income uk now requires a shift from retrospective reporting to a live, strategic oversight of your portfolio. By prioritising accurate expense classification and selecting the optimal ownership structure, you position your investments to withstand both fiscal drag and upcoming rate increases. We believe that clarity in these matters isn’t just a compliance requirement; it’s the foundation of long-term financial security.

As Chartered Certified Accountants with a history of excellence since 1901, Davis & Co LLP offers the deep-seated expertise required to manage complex property and international tax interests. We act as your strategic partner, ensuring that every digital submission and structural decision aligns with your broader financial goals. Our focus remains on providing the discreet, high-calibre advice that has defined our practice for over a century. Partner with Davis & Co LLP for expert property tax planning and ensure your portfolio is prepared for the challenges of the coming decade. With a disciplined approach to planning, you can move forward with complete confidence in your financial future.

Frequently Asked Questions

Do I have to pay tax on rental income if I have a mortgage?

Yes, you’re liable for tax on rental income uk regardless of whether the property is mortgaged. You can’t deduct mortgage interest payments from your rental income to reduce your taxable profit. Instead, you receive a tax credit equal to 20% of your mortgage interest costs, which is applied as a reduction to your final tax bill.

How much rental income is tax-free in the UK for 2026?

Landlords can utilise the £1,000 Property Allowance, which allows you to earn this amount gross without paying tax or reporting it to HMRC. Additionally, if your property income is your only source of earnings, it stays tax-free up to the Personal Allowance threshold of £12,570 for the 2026/27 tax year.

What happens if my rental property makes a loss?

If your allowable expenses exceed your rental income, you’ve incurred a property loss. You can’t offset this loss against other types of income, such as your salary, but you can carry it forward to offset against future profits from the same property business. This effectively reduces your future liability for tax on rental income uk.

Can I split rental income with my spouse to reduce tax?

You can split rental income if you own the property jointly with your spouse or civil partner. HMRC typically assumes a 50/50 split for tax purposes. If your actual ownership proportions differ, you can file a Form 17 to ensure the income is taxed according to your specific beneficial interests, potentially lowering your household’s overall tax band.

When is the deadline for paying tax on rental income in 2026?

The deadline for paying tax for the 2025/26 tax year is 31 January 2027. However, the introduction of Making Tax Digital in April 2026 means many landlords must now provide digital updates every quarter. While these quarterly submissions don’t require immediate payment, failing to meet the digital deadlines can result in points-based penalties.

Is MTD for ITSA mandatory for all landlords in 2026?

Making Tax Digital for Income Tax becomes mandatory on 6 April 2026 only for landlords with a gross rental income exceeding £50,000. If your income is between £30,000 and £50,000, you won’t be required to join the scheme until April 2027. Landlords earning above £20,000 are currently scheduled to join from April 2028.

How do I calculate the 20% tax credit for mortgage interest?

To calculate your credit, identify the lowest of three figures: your total finance costs, your property business profit, or your total adjusted income exceeding the personal allowance. You then multiply this lowest amount by 20%. This resulting figure is deducted directly from your income tax liability rather than being treated as an expense.

Do I need to pay National Insurance on my rental income?

Most landlords don’t pay National Insurance on rental income as it’s typically treated as investment income rather than earned income. This remains a key distinction in the UK tax system. Only in rare cases where you’re deemed to be running a professional property business providing significant extra services would National Insurance considerations change.