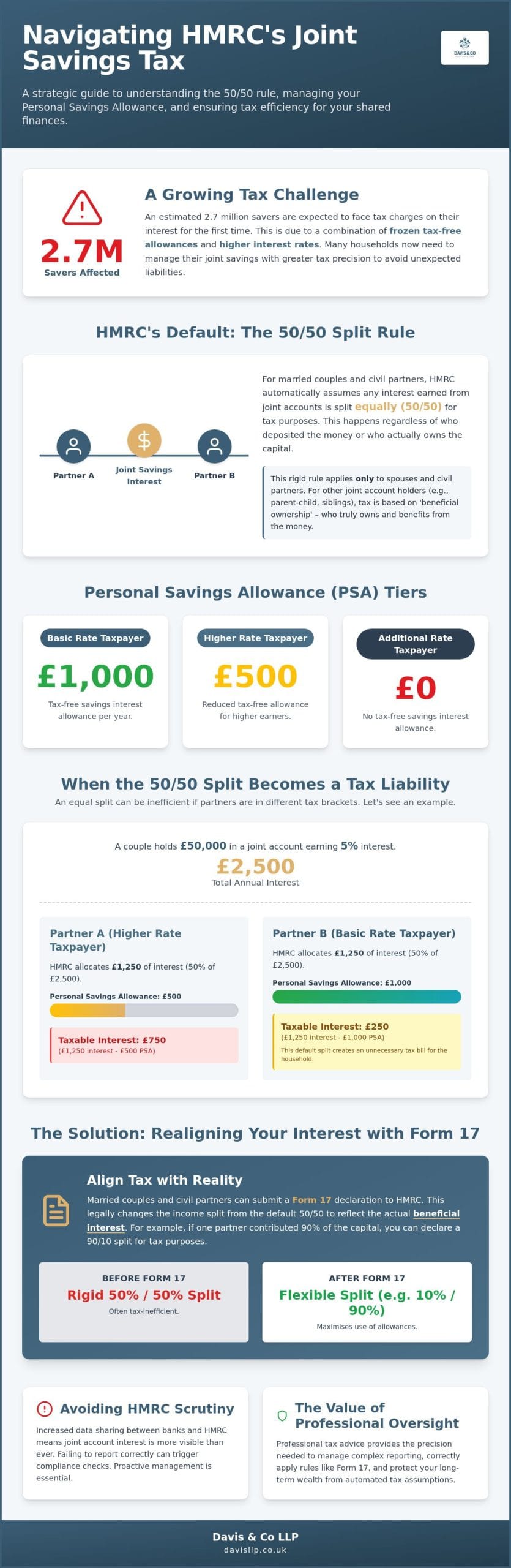

An estimated 2.7 million savers are expected to face tax charges on their interest for the first time this year, a consequence of frozen thresholds and higher interest rates. This shift means that many households must now treat their shared finances with a level of technical rigour previously reserved for high-net-worth portfolios. You likely view your shared finances as a matter of simple convenience, but failing to proactively manage hmrc joint bank accounts savings tax can lead to unexpected liabilities. It’s a common concern that HMRC’s rigid 50/50 default split may not reflect your actual financial reality, potentially resulting in an inefficient use of your available allowances.

We believe that professional oversight is the most effective way to secure your financial position against such automated assumptions. This guide provides the strategic insight required to address these regulations and ensure your interest is split with precision. We’ll explore the mechanics of the 50/50 rule, the legal requirements for reallocating beneficial interest, and the correct application of Form 17 for married couples. By the end of this discussion, you’ll possess a clear framework for HMRC compliance that protects your wealth and restores your peace of mind.

Key Takeaways

- Understand the implications of HMRC’s default 50/50 split and why it doesn’t always represent the most tax-efficient structure for your shared savings.

- Review the 2026 Personal Savings Allowance tiers to see how joint interest affects your individual tax bracket and reporting requirements.

- Discover how to use Form 17 to align your hmrc joint bank accounts savings tax with your actual beneficial interest rather than the default split.

- Identify the compliance red flags that arise from increased data sharing between banks and HMRC so you don’t trigger unnecessary scrutiny.

- Learn how professional tax oversight provides the precision needed to manage complex reporting and protect your long-term wealth.

Understanding the HMRC Default: The 50/50 Rule for Joint Savings

In the eyes of HM Revenue and Customs (HMRC), simplicity often dictates the initial assessment of shared finances. The 50/50 rule is the statutory baseline for taxing income from assets held in joint names by spouses and civil partners. This regulation mandates that any interest earned is treated as belonging to both parties in equal shares, regardless of the actual contribution or source of the underlying capital. It’s a rigid framework that ignores the practical nuances of how couples manage their money, focusing instead on a uniform distribution of tax liability.

Managing hmrc joint bank accounts savings tax requires a clear understanding that this default assumption is not merely a suggestion. Even if one individual provided the entirety of the deposit from an inheritance or personal salary, the law presumes an equal split of the resulting interest. For many, this automated approach simplifies reporting, but for those with significant cash reserves, it often leads to a structural tax inefficiency that we believe warrants professional attention. It’s the starting point from which all strategic tax planning for joint assets must begin.

Who Does the 50/50 Rule Apply To?

The 50/50 rule specifically targets married couples and civil partners living together. It doesn’t apply to other joint account holders, such as business partners, siblings, or friends. For these non-spousal arrangements, tax is typically assessed based on beneficial ownership, which looks at who actually owns the money and is entitled to the interest. When accounts are held with children or elderly parents, HMRC expects the interest to be reported according to who truly benefits from the funds. We often see confusion here; if a parent places funds in a joint account with a child but retains full control and benefit, the parent remains liable for the tax on all interest earned.

When the Default Split Becomes a Tax Liability

The danger of the default split lies in its indifference to your individual tax brackets. If one partner is a higher-rate taxpayer and the other is a basic-rate or non-taxpayer, an equal split of interest can be unnecessarily expensive. The higher earner will pay 40% tax on their half of the interest, while the lower earner’s Personal Savings Allowance might sit partially unused. In more extreme cases, a substantial interest payment split 50/50 can push a lower-earning spouse into a higher tax bracket, triggering a loss of benefits or personal allowances. We recommend a regular review of your joint holdings alongside your individual tax codes to ensure your household isn’t overpaying due to a lack of proactive planning.

The 2026 Personal Savings Allowance (PSA) and Joint Interest

The 2026 fiscal year presents a challenging environment for savers. With the Personal Savings Allowance (PSA) remaining frozen while interest rates remain elevated, the margin for error has narrowed significantly. For a basic rate taxpayer, the allowance is £1,000. Higher rate taxpayers receive a reduced allowance of £500, while additional rate taxpayers have no allowance at all. When you hold funds together, managing hmrc joint bank accounts savings tax requires a granular look at how these individual thresholds are consumed by shared income. It’s no longer a matter of passive accumulation; it’s a matter of active threshold management.

The “savings starter rate” offers a 0% rate on up to £5,000 of savings income, but this is only available if your non-savings income is relatively low. For most high-calibre professionals we advise, this allowance isn’t a factor. Instead, the focus remains on the PSA. According to HMRC’s official guidance on joint accounts, the interest is attributed to you based on the legal split, usually 50/50. This means half of the total interest earned on a joint account is “sliced” into your personal allowance before any sole savings are even considered. If you don’t account for this, you may find yourself unexpectedly paying tax on interest you assumed was covered.

Calculating Your Individual Share of Interest

Consider a couple with £50,000 in a shared account earning 5% interest. This generates £2,500 annually. Under the default rule, £1,250 is attributed to each partner. If both are higher rate taxpayers with a £500 PSA, they’ve each exceeded their allowance by £750 before accounting for any personal accounts. You’ve got to aggregate interest from all sources, including sole accounts and ISAs, though ISA interest remains tax-free. Banks now report this data directly to the authorities, making it easier for discrepancies to trigger a review. We find that many clients overlook interest from smaller, forgotten accounts, which can lead to inadvertent non-compliance.

The Risk of PSA Breach in 2026

A “set and forget” approach to cash management is no longer viable. In the current climate, even modest balances can push you over the limit. When you breach your PSA, HMRC typically adjusts your PAYE tax code to collect the debt or requires disclosure via Self Assessment. This automated process doesn’t always account for the nuances of your wider financial life. For a broader perspective on managing these obligations, you might find our Expert Tax Advice in the UK: A Comprehensive Guide for 2026 helpful.

Proactive monitoring is the only way to avoid the administrative burden of corrected tax codes. If your shared interest is likely to exceed your combined allowances, it’s time to consider a more sophisticated distribution of your capital. At Davis & Co LLP, we specialise in personal tax services that ensure your savings remain as tax-efficient as possible.

Reallocating Interest: Beneficial Interest and Form 17

While the 50/50 rule serves as the default, it doesn’t always reflect the underlying economic reality of a household’s assets. To manage your tax position effectively, you must distinguish between legal title and beneficial interest. Legal title refers simply to whose names are on the account. Beneficial interest, however, identifies who truly owns the capital and is entitled to the income it generates. For those seeking to optimise their hmrc joint bank accounts savings tax, aligning your tax reporting with this beneficial ownership is a powerful, albeit technically demanding, strategy.

For married couples and civil partners, HMRC permits a departure from the equal split only when the beneficial interest is actually unequal. This isn’t a choice you can make arbitrarily to suit a tax year; it must be a statement of fact supported by evidence. We often find that couples have naturally unequal contributions, perhaps from an inheritance or a prior business sale, yet they remain tethered to the 50/50 default because they haven’t formalised their actual shares.

Strategic Tax Planning with Form 17

If you own savings in unequal shares, such as a 90/10 split, you can declare this to HMRC using Form 17. This allows the partner with the lower marginal tax rate to be taxed on the larger portion of the interest, potentially saving the household significant sums. However, this declaration must be accompanied by a “Declaration of Trust” or similar evidence that confirms the unequal ownership. It’s a binary choice; you cannot use Form 17 to declare any split other than the actual beneficial interest held.

Timing is a critical factor in this process. You must submit Form 17 to HMRC within 60 days of signing the declaration of trust. If you miss this window, the declaration is invalid for tax purposes, and you’ll remain subject to the 50/50 default. We believe that professional verification of these documents is essential before submission, as HMRC’s scrutiny of these declarations has intensified alongside their increased data-sharing capabilities.

Non-Spousal Reallocation: The “Actual Share” Rule

The rules shift when joint accounts are held by unmarried partners, siblings, or friends. In these instances, the 50/50 default for spouses doesn’t apply. Instead, HMRC operates on the “Actual Share” principle. Tax is due based on the proportion of the funds each person provided. If one individual contributed 100% of the capital, they are typically liable for 100% of the tax on the interest, even if another name is on the account for administrative ease.

To avoid compliance challenges, we recommend maintaining meticulous records of contributions. If you’re an unmarried couple managing shared expenses, a clear paper trail of deposits and withdrawals serves as your primary defence during an investigation. Without this evidence, HMRC may default to an equal split, which might not be the most tax-efficient outcome for your specific circumstances.

HMRC Scrutiny: Avoiding Compliance Checks on Shared Savings

HMRC’s ability to monitor private financial arrangements has reached unprecedented levels of sophistication. In 2026, the “Connect” AI system serves as the central pillar of their enforcement strategy, cross-referencing data from UK financial institutions with individual tax filings in real-time. This automated oversight means that managing hmrc joint bank accounts savings tax is no longer just about calculating the right figures; it’s about ensuring those figures match the automated data stream HMRC receives. Discrepancies between bank-reported interest and your Self Assessment are now the primary trigger for compliance checks.

When the “Connect” system identifies interest income that hasn’t been declared, or identifies a 50/50 split that contradicts other financial data, it flags the account for human review. These flags often lead to “Simple Assessment” notices or more formal enquiries. For a detailed breakdown of current enforcement protocols and how to recognise a formal enquiry, our HMRC Tax Warning 2026 provides essential context on modern investigation triggers. We believe that proactive transparency is the only way to navigate this landscape without attracting unnecessary scrutiny.

Maintaining a Robust Audit Trail

A defensive tax position relies entirely on the quality of your documentation. If you’ve moved away from the default 50/50 split, you must be able to prove the source and ownership of the capital. We recommend maintaining a dedicated file for each joint holding that includes:

- Original bank statements showing the initial capital injection.

- Certified gift deeds or inheritance documentation if the funds originated from a third party.

- A clear record of “capital vs. interest” to ensure you aren’t accidentally reporting capital withdrawals as taxable income.

- Annual reconciliation reports that aggregate interest across all shared and sole accounts.

This level of detail is particularly important for high-calibre individuals whose accounts may see significant fluctuations. A well-prepared audit trail allows us to resolve most queries before they escalate into full-scale investigations.

Responding to an HMRC Enquiry

If HMRC queries your joint holdings, the response must be measured and evidence-led. Many taxpayers attempt to clarify beneficial ownership only after an enquiry has begun. While it’s possible to argue for an unequal split retrospectively, it’s significantly more difficult without a prior Form 17 or a formal Declaration of Trust. The risk of misreported savings isn’t just a higher tax bill; it can lead to penalties for “unintentional” tax evasion if HMRC deems you were careless in your reporting.

Professional representation is vital during these interactions. We act as the interface between you and the inspector, ensuring that all technical arguments regarding beneficial interest are presented with the necessary legal rigour. If you’ve received a notice of enquiry or wish to pre-emptively secure your filings, our team provides the discrete, high-level personal tax services required to protect your interests.

Strategic Partnership: How Davis & Co LLP Protects Your Wealth

Managing the intricacies of hmrc joint bank accounts savings tax is a technical requirement, yet for our clients, it represents just one facet of a comprehensive wealth management strategy. We believe that effective tax planning shouldn’t be a reactive response to HMRC’s automated systems. Instead, it’s a proactive, integrated process that aligns your shared assets with your long-term financial objectives. As Chartered Certified Accountants with a history of excellence since 1901, we provide the professional gravitas and deep-seated expertise required to navigate these complex interactions with confidence.

Our role as your strategic partner is to provide a level of analytical rigour that anticipates regulatory shifts before they impact your capital. While the technical defaults of the 50/50 rule or the limitations of the Personal Savings Allowance provide the framework, our expertise lies in the nuanced application of these laws. We move beyond simple compliance, focusing on the human and organisational impact of your financial structures to ensure your wealth is protected through every fiscal cycle.

Tailored Personal Tax Services

Our approach begins with a highly individualised assessment of your joint and sole savings structures. We don’t rely on generic templates; we examine the specific beneficial interest and legal titles of your holdings to ensure every filing is both accurate and tax-efficient. This precision is essential in an era of increased data-sharing, where even a minor discrepancy can trigger a compliance check. By providing meticulous oversight of your Self Assessment, we offer the quiet assurance that your affairs are managed with the highest level of discretion. Whether you hold domestic accounts or require sophisticated international tax planning for offshore joint holdings, our team ensures your global wealth remains secure and compliant.

Securing Your Financial Future

Effective management of savings interest is often the first step toward a more robust estate plan. We specialise in integrating your personal tax position with broader trust tax services and inheritance tax planning. This holistic view ensures that the way you hold your cash today doesn’t create unnecessary liabilities for your heirs tomorrow. For professionals with specific sector requirements, such as our dental tax specialist services, we provide industry-standard expertise that understands the unique cash flow and savings patterns of your practice. We position ourselves as a strategic partner dedicated to the long-term preservation of your capital.

The complexities of the 2026 tax landscape require a considered and steady hand. We invite you to consult with Davis & Co LLP for bespoke tax planning that reflects your individual needs and provides the peace of mind that comes from high-calibre professional representation.

Securing Your Shared Wealth Against Evolving Tax Standards

The 2026 tax landscape demands more than just awareness; it requires a commitment to technical precision. We’ve explored how the default 50/50 split can be realigned with beneficial interest to protect your Personal Savings Allowance. By formalising your actual ownership and maintaining a robust audit trail, you’ll move from a position of vulnerability to one of strategic advantage. Navigating the nuances of hmrc joint bank accounts savings tax doesn’t have to be a source of uncertainty when you have the right framework in place.

As Chartered Certified Accountants since 1901, we provide the steady, professional oversight needed to manage complex HMRC compliance and international tax matters. Our team acts as your strategic partner, ensuring your shared finances are integrated into a broader plan for wealth preservation. We’re here to provide the clarity and gravitas you need to manage your household’s assets effectively. Secure your personal tax position with Davis & Co LLP today and ensure your financial future remains stable and well-advised.

Frequently Asked Questions

Do I have to tell HMRC about my joint bank account?

You don’t need to notify HMRC simply for opening an account; however, you’re legally required to report any interest that exceeds your Personal Savings Allowance. UK financial institutions share data with the authorities automatically. If your share of the interest is taxable, it must be disclosed through your Self Assessment return or it may be collected via a change to your PAYE tax code.

Can I choose to have all interest taxed on my partner’s return?

You cannot simply elect to shift the tax liability for convenience or tax efficiency. HMRC assumes a 50/50 split for spouses and civil partners unless you provide evidence of unequal beneficial ownership. To change how hmrc joint bank accounts savings tax is applied, you must submit Form 17 alongside a formal Declaration of Trust that reflects the actual distribution of the capital.

What happens if we have different tax rates on a joint account?

Each partner is taxed on their share of the interest at their individual marginal rate. If one partner is a higher-rate taxpayer and the other is a basic-rate taxpayer, the higher earner will pay 40% tax on their half of the interest once their £500 PSA is exhausted. This often creates a higher total tax bill for the household than if the assets were held differently.

Is interest from a joint ISA taxed differently by HMRC?

ISAs are strictly individual products and cannot be held in joint names under current UK regulations. Any interest earned within your individual ISA remains tax-free and doesn’t count toward your Personal Savings Allowance. If you hold a “joint” savings account, it’s a standard bank account and the interest is fully taxable once allowances are exceeded.

How does HMRC know how much interest I have earned on a shared account?

HMRC utilises the “Connect” system to receive direct, automated data feeds from all UK banks and building societies. This data includes the total interest paid and the identities of all account holders. The system cross-references this information against your tax filings to identify omissions. Discrepancies often trigger automated “Simple Assessment” notices or more formal compliance enquiries.

What is the deadline for reporting joint savings interest on Self Assessment?

The reporting deadlines align with the standard Self Assessment calendar. For the 2026/27 tax year, you must submit a paper return by 31 October 2027 or an online return by 31 January 2028. Missing these dates can result in immediate penalties, even if the tax due on your savings interest is relatively modest.

Can HMRC check the bank accounts of both partners in a joint account?

Yes, HMRC possesses broad statutory powers to request information from financial institutions. If they open an investigation into one individual, the shared nature of a joint account provides them with full visibility of the funds and transactions for both parties. Maintaining clear records of who provided the capital is essential for resolving any queries regarding beneficial interest.