Could a significant reduction in your immediate tax liability be the most expensive strategic error of your career? For many dental practitioners facing personal income tax rates of 40% or 45%, the move toward a limited company structure feels like a natural progression. However, the tax implications of dental practice incorporation in 2026 are nuanced, requiring a balance between corporate efficiency and the protection of your long-term legacy. We understand the frustration of seeing practice growth eroded by high taxation, and we recognize the hesitation that comes with risking your NHS pension benefits.

In this guide, we provide a comprehensive analysis of the fiscal benefits, technical risks, and long-term financial impacts of moving your practice to a limited company. You’ll gain a clear understanding of the net tax benefit after considering the 25% Corporation Tax rate and the 18% Business Asset Disposal Relief rate effective from April 2026. We’ll also outline a roadmap for a compliant transition that ensures the preservation of your NHS contracts and pension eligibility, giving you the certainty required to lead your practice with confidence.

Key Takeaways

- Evaluate the efficiency of shifting from personal income tax rates of up to 45% to a corporate structure, utilizing Marginal Relief to optimize profits between £50,000 and £250,000.

- Navigate the complex tax implications of dental practice incorporation by understanding how goodwill valuation and Capital Gains Tax impact your practice’s immediate liquidity.

- Safeguard your NHS Pension Scheme eligibility by mastering the critical distinction between Practitioner and Officer status during the contractual transition.

- Develop a disciplined 12-month roadmap for incorporation that utilizes management accounts to monitor fiscal performance and ensure regulatory compliance.

- Transition your practice from a simple operational model to a sophisticated corporate entity, treating the move as a strategic valuation event rather than a basic tax adjustment.

The Evolving Landscape of Dental Practice Incorporation in 2026

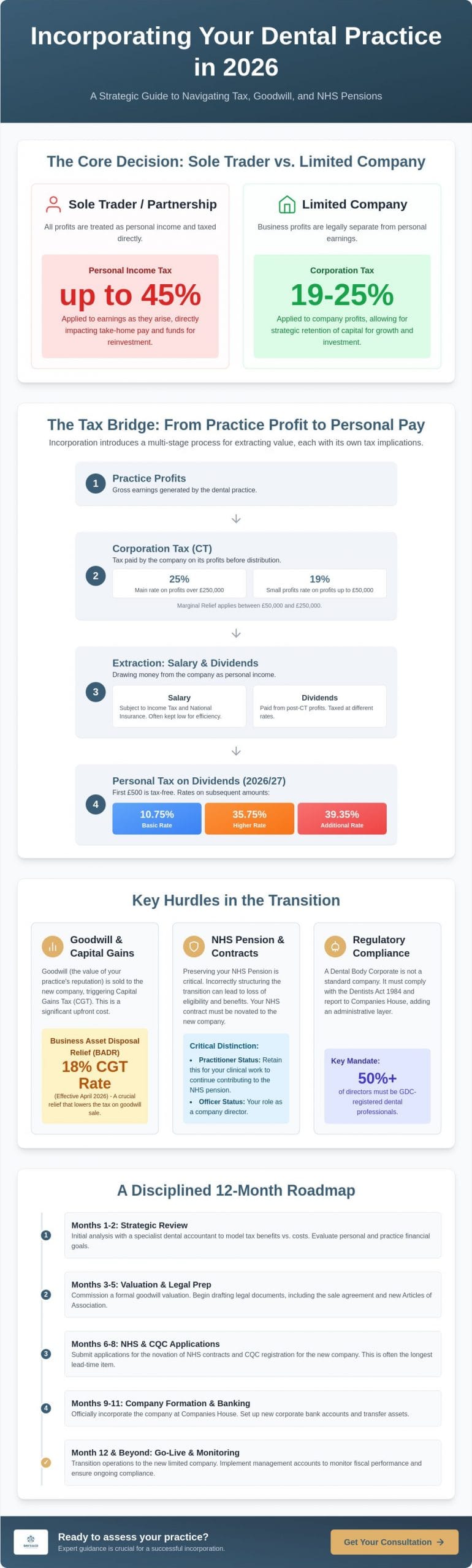

The transition from a sole trader or partnership to a Limited Company, often referred to as a “Body Corporate” in our sector, represents a fundamental shift in how dental professionals manage their commercial interests. In the 2026/27 tax year, this move is rarely about a single benefit. Instead, it’s a multi-faceted decision driven by a desire for structural clarity and fiscal resilience. While many focus solely on the potential for lower tax rates, the tax implications of dental practice incorporation encompass a broader spectrum of regulatory compliance and long-term asset protection. We see this as a strategic evolution rather than a mere change in paperwork.

To understand the foundation of this shift, one must grasp Corporate Tax Basics, which differentiate between personal earnings and company profits. This distinction is vital in an environment where the main rate of Corporation Tax stands at 25% for profits exceeding £250,000. For many high-earning principals, the gap between this and the 45% additional rate of personal income tax provides a compelling reason to review their current structure. However, the choice isn’t purely about the numbers on a balance sheet. It involves a sophisticated understanding of how a company acts as a separate legal entity, shielding you from certain personal liabilities while requiring a more disciplined approach to governance. We believe that choosing this path requires the guidance of a specialist dental tax accountant to ensure the transition doesn’t inadvertently trigger liabilities that outweigh the benefits.

Defining the Dental Body Corporate

Under the Dentists Act 1984, the legal framework for a Dental Body Corporate is strict. It’s not a standard private company. At least 50% of the directors must be GDC-registered professionals. This ensures clinical governance remains at the heart of the corporate structure even as the administrative burden shifts to Companies House. We help our clients manage this transition, ensuring that the Articles of Association reflect these specific professional requirements while maintaining the necessary distance between clinical risk and corporate stability.

Strategic Drivers for Incorporation in 2026

In 2026, practice profitability is under constant pressure from rising operational costs. The increased financial commitments associated with the minimum wage 2025 and 2026 rates mean that every pound saved in tax is vital for reinvestment. Operating through a company allows you to retain profits within the business at the 19% or 25% Corporation Tax rate, rather than paying higher personal tax on funds intended for practice upgrades. This strategic retention of capital is one of the most significant tax implications of dental practice incorporation, providing a buffer for growth that unincorporated practices simply cannot match.

Comparative Tax Analysis: Sole Trader vs. Limited Company

For a high-earning principal, the 45% additional rate on personal income often feels like a direct penalty on practice growth. In contrast, the corporate environment offers a more structured tiered approach. While a sole trader is taxed on all profits as they arise, a limited company allows for the separation of business earnings from personal drawdowns. The tax bridge is the multi-stage fiscal path that converts gross corporate earnings into personal take-home pay after accounting for corporation tax, employer obligations, and individual dividend liabilities. Understanding this bridge is essential when evaluating the tax implications of dental practice incorporation.

The 2026/27 dividend allowance remains at a modest £500, making the subsequent tax rates a critical factor in your planning. Basic rate taxpayers face a 10.75% charge on dividends, while higher and additional rate taxpayers are subject to 35.75% and 39.35% respectively. We find that many practitioners overlook the cumulative effect of these rates when they focus solely on the headline corporation tax figures. It’s vital to cross-reference these personal liabilities with the NHS contract and pension implications of incorporation, as any tax saving must be weighed against the potential impact on your long-term retirement benefits.

The Salary-Dividend Mix

We work with our clients to identify the “sweet spot” in profit extraction. This typically involves a modest salary that utilizes the personal allowance while keeping the individual below the threshold for higher National Insurance (NI) contributions. By distributing the remaining profit as dividends, we can often reduce the total NI burden for both the practice and the principal. This strategy requires a disciplined approach to timing, ensuring that dividends are only declared when the company has sufficient distributable reserves to remain compliant with the Companies Act.

Corporation Tax Thresholds in 2026

The 2026 regime utilizes a marginal relief system to bridge the gap between the 19% small profits rate and the 25% main rate. For practices with profits between £50,000 and £250,000, the effective tax rate climbs progressively. This means a multi-surgery practice with profits at the higher end of this scale will face a significantly different fiscal reality than a single-handed practitioner. We focus on managing this effective rate through the strategic use of legitimate business expenses and capital allowances. If you’re concerned about how these thresholds affect your specific profit margins, our dental tax specialist team can provide a bespoke projection. This level of granularity ensures that your transition is based on hard data rather than general assumptions.

Goodwill Valuation and Capital Gains Tax Implications

At the heart of any structural transition lies the valuation of goodwill. In a dental context, this represents the intangible value derived from your patient lists, the practice’s local reputation, and its strategic location. When you move to a corporate structure, you’re effectively selling this asset from yourself to your new company. The tax implications of dental practice incorporation are most visible here, as this transfer is treated as a disposal for Capital Gains Tax (CGT) purposes. It’s a pivotal moment that requires a precise market valuation to withstand HMRC scrutiny, as an overestimation can lead to significant penalties, while an underestimation leaves capital on the table.

The landscape for these transfers has shifted with the 2026 regulations. For qualifying disposals made from 6 April 2026, Business Asset Disposal Relief (BADR) provides a reduced CGT rate of 18% on the first £1 million of lifetime gains. This relief is essential for maintaining liquidity during the transition. We often see practitioners fall into the “double tax” trap, where they focus solely on the immediate CGT liability without considering that future growth within the company will be subject to Corporation Tax upon an eventual exit. Balancing the initial valuation with your long-term exit strategy is the only way to ensure the move remains fiscally sound over the next decade.

The Director’s Loan Account (DLA) Advantage

One of the most effective outcomes of selling goodwill to your company is the creation of a credit on your Director’s Loan Account. This represents a debt the company owes you personally. You can then draw tax-free income from the business as the company “repays” this loan from its post-tax profits. This mechanism provides a significant cash flow advantage, provided the original goodwill was transferred at a verifiable market value. We emphasize the necessity of an independent professional valuation to ensure this debt is considered legitimate by HMRC, protecting your ability to extract funds without triggering additional income tax liabilities.

Stamp Duty and Asset Transfer Risks

The transfer of physical assets requires equally careful handling. If your practice premises are included in the incorporation, Stamp Duty Land Tax (SDLT) implications must be calculated to avoid unexpected costs. Beyond the property, items such as dental chairs, specialized equipment, and stock must be formally transferred through a Sale and Purchase Agreement (SPA). This document acts as the legal cornerstone of the transition, clearly defining the price and terms of the transfer between you and the corporate entity. A well-drafted SPA ensures that capital allowances are preserved and that the separation between personal and corporate assets is legally robust, providing the intellectual rigour your practice deserves.

The NHS Pension and Contractual Hurdles

The most significant deterrent for many principals considering a structural change is the potential impact on their retirement legacy. Under current regulations, dental practitioners operating through a limited company are generally unable to contribute to the NHS Pension Scheme (NHSP). This restriction creates a fundamental tension between corporate tax efficiency and personal long-term security. Understanding these specific tax implications of dental practice incorporation is vital; the loss of pension growth can often outweigh the immediate corporation tax savings. The distinction between “Practitioner” status and “Officer” status is central to this issue. While a sole trader enjoys direct access as a practitioner, a company director is classified as an officer, a shift that can terminate NHSP eligibility unless specific, often complex, criteria are met.

We see many practitioners struggle with the realization that their pensionable earnings might be capped or eliminated upon incorporation. If you’re exploring the current tax advice uk landscape, you’ll find that the interplay between salary extraction and pensionable pay is a high-risk area. We focus on providing the intellectual rigour necessary to model these outcomes before any papers are signed. It’s not just about the tax you save today, but the wealth you preserve for the next thirty years.

Preserving NHS Pension Benefits

One potential, though increasingly scrutinized, route is seeking “Direction Body” status for the limited company. This allows the corporate entity to act as an employing authority, theoretically maintaining your access to the scheme. However, we must caution that this process is far from guaranteed and requires a high level of administrative compliance. There’s also the risk that a lower salary, taken to optimize your tax position, could negatively impact your CARE (Career Average Revalued Earnings) tiers. When NHSP access is no longer viable, we work with our clients to develop robust alternative private pension strategies that align with their new corporate structure and long-term goals.

Contractual Novation and CQC Compliance

The legal transfer of an NHS contract from an individual to a company is known as novation. This isn’t an automatic right. Integrated Care Boards (ICBs) often approach these requests with caution, sometimes using the opportunity to renegotiate terms or impose new conditions. We believe a successful novation requires a transparent, evidence-based proposal that demonstrates how the corporate structure benefits practice stability. Simultaneously, you must synchronize this with a change in your Care Quality Commission (CQC) registration. A failure to align the contract holder with the registered provider can lead to a breach of contract or a suspension of payments. Given the high stakes involved in these transitions, consulting a dental tax specialist is a prudent step to ensure your contractual and pension rights remain protected.

Implementation Strategy: A Framework for Dental Principals

Executing a structural transition requires a disciplined, chronological approach that spans approximately twelve months. This isn’t a mere administrative change; it’s a fundamental repositioning of your professional life. We initiate this process with a detailed feasibility study, culminating in a bespoke “Incorporation Report” that quantifies the specific tax implications of dental practice incorporation for your unique circumstances. This report acts as your strategic compass, ensuring that every decision, from the initial valuation to the final contract novation, is based on empirical data rather than optimistic projections. By utilizing our specialized dental tax services, you ensure that the transition is handled with the professional gravitas it deserves, mitigating risks before they manifest as liabilities.

A critical component of this roadmap is the integration of robust management accounts from the outset. These reports allow us to monitor the success of the transition in real time, verifying that the “tax bridge” between corporate profit and personal take-home pay is functioning as intended. We believe that visibility is the key to confidence. The typical implementation timeline follows a logical progression:

- Months 1-3: Feasibility analysis, NHS pension modeling, and preliminary goodwill assessment.

- Months 4-6: Formal valuation, legal drafting of the Sale and Purchase Agreement, and ICB/CQC notifications.

- Months 7-9: Formal company incorporation, opening of corporate banking facilities, and contract novation.

- Months 10-12: Finalization of the first corporate payroll and preparation for the dual tax filing system.

The Importance of Professional Valuation

HMRC maintains a high level of interest in goodwill transfers, particularly when they create significant credits on a Director’s Loan Account. “Back-of-the-envelope” calculations don’t just risk financial inaccuracy; they actively trigger HMRC scrutiny. Our role as your advisor is to provide a valuation that reflects the 2026 dental market with absolute precision. We defend these valuations with rigorous documentation, ensuring that the tax implications of dental practice incorporation remain a benefit rather than a point of contention with the authorities.

Ongoing Compliance and Governance

Once incorporated, your practice enters a more complex regulatory environment. You’ll transition from a single Self-Assessment return to a dual system of Corporate and Personal tax, alongside strict Companies House filing deadlines. This requires a shift in your internal governance. We provide the steady, deliberate oversight necessary to manage these statutory requirements, allowing you to focus on clinical excellence. A strategic partnership with a dental-specialist firm isn’t just an administrative convenience; it’s a safeguard for your practice’s long-term fiscal health.

Securing Your Practice’s Financial Future

Moving your practice to a corporate structure is a significant strategic shift that requires more than a simple tax calculation. It’s a decision that must balance the immediate benefits of corporate tax rates with the long-term preservation of your NHS pension and the accurate valuation of your practice’s goodwill. We’ve explored the necessity of a disciplined 12-month roadmap and the critical role of management accounts in maintaining fiscal clarity throughout this transition.

The tax implications of dental practice incorporation are profound; they influence everything from your personal liquidity to your eventual exit strategy. As Chartered Certified Accountants with niche dental expertise, we bring decades of experience in high-level tax planning and HMRC compliance to your side. Whether you’re managing a GDS contract or a private practice, our tailored solutions provide the security you need to lead with confidence.

Consult our specialist dental tax team for a bespoke feasibility report to ensure your move is both compliant and optimized. Your practice’s legacy is a significant achievement. Let’s work together to ensure it’s protected by the highest standard of professional advice.

Frequently Asked Questions

Will I definitely save money on tax by incorporating my dental practice in 2026?

Tax savings aren’t guaranteed and depend heavily on your practice’s profit levels and how you choose to extract funds. While the 19% small profits rate remains attractive, the 25% main rate for profits over £250,000 and the 35.75% higher rate dividend tax can erode benefits. We find that the most significant savings often come from retaining profits within the company for reinvestment rather than personal drawdowns.

How does incorporation affect my eligibility for the NHS Pension Scheme?

Most dental principals lose the ability to contribute to the NHS Pension Scheme upon incorporation. This happens because the scheme views company directors as “Officers” rather than “Practitioners,” a status change that typically terminates eligibility. Evaluating this specific impact is a vital part of understanding the total tax implications of dental practice incorporation, as the loss of pension growth can sometimes outweigh annual tax savings.

Can I still use the “Business Asset Disposal Relief” when I sell my goodwill to the company?

Yes, Business Asset Disposal Relief (BADR) remains available for qualifying goodwill transfers to your own company. From 6 April 2026, the applicable Capital Gains Tax rate for these disposals is 18%, subject to a £1 million lifetime limit. This relief is essential for creating a tax-efficient credit on your Director’s Loan Account, which allows for future tax-free withdrawals from the practice.

What happens to my existing NHS contract if I move to a limited company structure?

Your NHS contract doesn’t automatically transfer to your new company; it requires a formal process called novation. You must apply to your Integrated Care Board (ICB) for permission to move the contract from your name to the corporate entity. This process is complex and the ICB isn’t obligated to agree, so we recommend securing contractual certainty before finalizing your incorporation plans.

Do I need to inform the General Dental Council (GDC) if I incorporate?

You must ensure your new company complies with the “Body Corporate” requirements set out in the Dentists Act 1984. This includes the rule that at least 50% of the company’s directors must be GDC-registered professionals. While the GDC doesn’t “approve” the business move, the company itself must be registered and remain compliant with professional governance standards to avoid regulatory action.

How is the goodwill of a dental practice valued for tax purposes?

Goodwill is valued based on what a hypothetical third-party buyer would pay for the practice’s future earnings. This valuation considers your patient lists, the stability of your NHS contract, and the practice’s local reputation. HMRC expects a professional, evidence-based valuation; relying on informal estimates can lead to significant penalties and a reassessment of your Capital Gains Tax liability.

Is there a minimum profit threshold where incorporation becomes beneficial?

There’s no universal threshold, but incorporation typically becomes a serious consideration when annual profits exceed £50,000. However, the 2026 tax landscape, including the marginal relief between the 19% and 25% corporation tax rates, means the “break-even” point is now more variable. We model each case individually to ensure the administrative costs of a company don’t exceed the fiscal advantages.

What are the main administrative disadvantages of running a dental limited company?

The primary drawbacks include increased transparency and a higher administrative burden. You’ll need to file statutory accounts with Companies House, which are accessible to the public, and manage a dual tax system involving both corporate and personal returns. These requirements demand more disciplined bookkeeping and professional oversight than operating as a sole trader or in a traditional partnership.