When you acquire a dental practice, goodwill often accounts for 60% to 80% of the total purchase price. Despite this, many practitioners treat this intangible asset as a static figure on a balance sheet rather than a dynamic tax saving tool. It’s understandable if you find the shifting landscape of HMRC regulations regarding goodwill amortisation for dental practices unsettling. You’ve likely felt the frustration of trying to keep pace with the “black hole” period and the subsequent 2019 reintroduction of relief.

We’re here to provide the clarity required to ensure your 2026 tax strategy remains robust. By understanding the interaction between the Intangible Fixed Assets regime and your practice’s specific structure, you can turn a complex accounting requirement into a strategic advantage. This guide examines how to leverage the 6.5% fixed-rate relief and structure your next acquisition to protect your cash flow. We’ll examine the impact of incorporation and the precise steps needed to align your intellectual property valuation with current legislation.

Key Takeaways

- Define the distinction between personal and practice goodwill to ensure a precise baseline for your business valuation.

- Discover how to utilise the 6.5% fixed-rate relief under the IFA regime to maximise goodwill amortisation for dental practices acquired after April 2019.

- Learn to navigate the “Normalised EBITDA” approach to align your acquisition structure with your long-term tax and cash flow objectives.

- Understand the historical impact of the 2015-2019 “black hole” period and how to prepare for the 2026 changes to Business Asset Disposal Relief.

- Gain insights into why a specialist dental tax approach is essential for identifying and protecting qualifying intellectual property within the Intangible Fixed Assets regime.

Understanding Dental Goodwill: More Than Just a Reputation

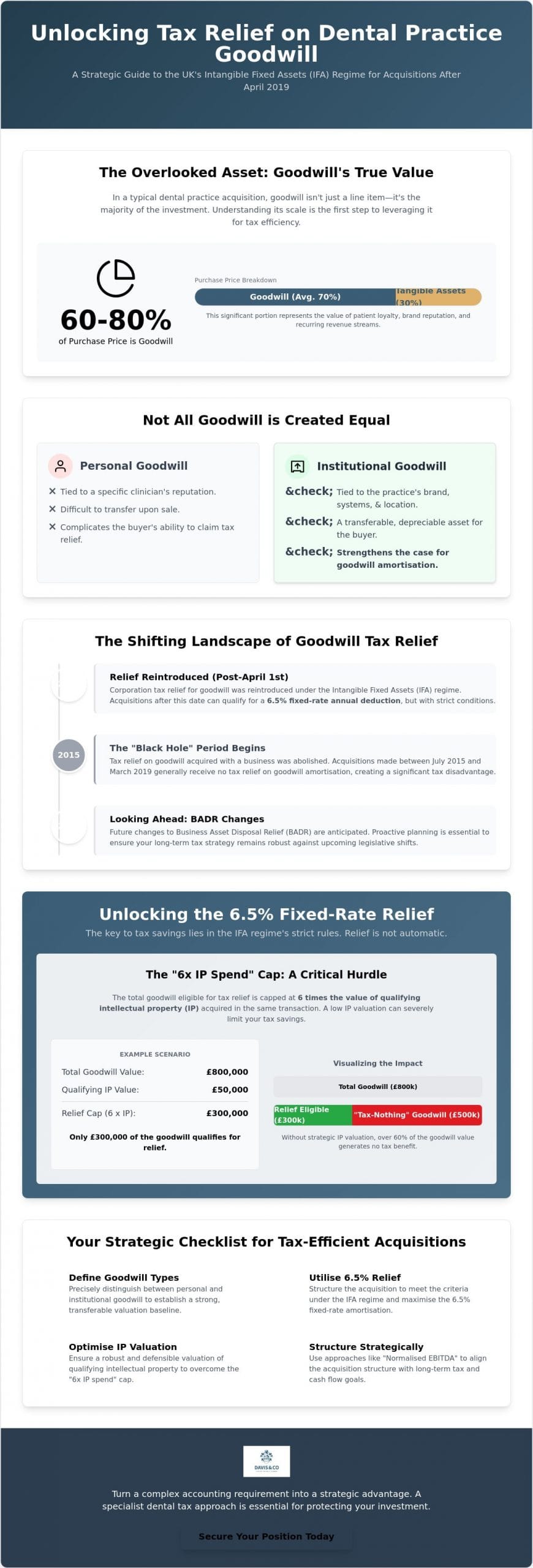

In the context of a dental practice acquisition, goodwill represents the premium paid for the business over and above the fair market value of its tangible assets, such as clinical equipment and surgery property. Within the UK dental sector, goodwill typically constitutes between 60% and 80% of the total purchase price. This high percentage reflects the intrinsic value of recurring revenue and patient loyalty. Understanding Dental Goodwill is fundamental for any practitioner, as it forms the basis for future tax relief claims.

The concept of transferable goodwill is particularly significant. It isn’t merely an abstract figure; it’s the primary driver for goodwill amortisation for dental practices. If the value is tied solely to the departing clinician, it has little worth to a buyer. However, if the value resides within the business structure itself, it becomes a depreciable asset that can provide substantial tax benefits under the right conditions.

The Components of Practice Value

A practice’s value is built upon several pillars that extend far beyond the physical chair. These include:

- Patient lists and recurring capitation contracts, such as Denplan or Practice Plan, which provide predictable revenue streams.

- A stable, well-trained clinical and administrative team that ensures operational continuity after the sale.

- Established internal systems and compliance protocols that reduce transition risks for the new owner.

- The strategic location and physical accessibility of the premises, which dictate local patient demographics.

Personal vs. Institutional Goodwill

HMRC closely examines the distinction between personal and institutional goodwill during practice sales. Personal goodwill stems from the specific reputation and clinical skill of an individual dentist. If patients visit the practice exclusively to see a specific clinician, that value is personal and often difficult to transfer. This can complicate the buyer’s ability to claim tax relief.

Institutional goodwill is tied to the practice’s brand, location, and systems. We often work with clients to institutionalise their goodwill well before a sale. This process involves transitioning patient loyalty from the individual to the practice brand. Doing so protects the valuation and strengthens the case for goodwill amortisation for dental practices. The more transferable the goodwill, the more tax-efficient the acquisition becomes for the new owner.

The UK Tax Framework for Goodwill Amortisation in 2026

The Intangible Fixed Assets (IFA) regime serves as the primary legislative framework governing how companies account for and claim relief on non-physical assets. It’s a complex area of tax law that treats goodwill as an asset for corporate tax purposes, allowing for a structured reduction in taxable profits. For practices operating as limited companies, this regime offers a pathway to recognise the gradual depreciation of the premium paid during an acquisition. Understanding the nuances of this framework is essential for maintaining a competitive fiscal position.

Since the 2019 reforms, the framework has moved toward a more targeted model of relief. Assets acquired after the 1 April 2019 rule stands as the definitive turning point for modern goodwill tax planning. Under current rules, eligible companies can claim a fixed-rate deduction of 6.5% per annum. However, this relief isn’t an automatic entitlement. It’s strictly contingent upon the acquisition of “qualifying intellectual property” as part of the same business purchase. This creates a direct legal link between the intangible value of your brand and the deductible goodwill amortisation for dental practices you can claim.

One of the most significant constraints within the IFA regime is the “6x IP spend” cap. This rule dictates that the total amount of goodwill eligible for relief cannot exceed six times the value of the qualifying IP acquired in the transaction. In a sector where goodwill often reaches seven figures, a low IP valuation can severely throttle your ability to claim relief. If your acquisition includes only minimal IP value, the majority of your goodwill may remain “tax-nothing” despite the post-2019 changes. As a dental tax specialist, we focus on ensuring these allocations are both defensible and strategically optimised during the due diligence phase.

Qualifying for the 6.5% Fixed-Rate Relief

To access this relief, the goodwill must be classified as a “relevant asset” acquired as part of a whole business purchase. It’s vital to note that this specific relief is a corporate benefit; sole traders and partnerships are excluded from claiming it. This distinction often serves as a primary motivator for practitioners considering incorporation. The relief applies only to “new” goodwill, meaning it must not have been held by a related party prior to the acquisition.

The Interplay with Intellectual Property (IP)

In a dental setting, qualifying IP typically includes registered trademarks, patient database software rights, or specific clinical patents. The value assigned to these items during the Purchase Price Allocation (PPA) process dictates the ceiling of your amortisation claim. We advise caution here; aggressive IP valuations designed solely to bypass the 6x cap are a common red flag for HMRC. A balanced approach that reflects the genuine commercial reality of the practice’s brand and systems is the most sustainable strategy.

Strategic Valuation and Its Impact on Amortisation Schedules

The valuation of a dental practice is the foundation upon which your entire tax-saving structure is built. We typically utilize a “Normalised EBITDA” approach, which adjusts earnings for non-recurring expenses and market-rate clinician salaries. This creates a realistic picture of the practice’s sustainable profit. Whether you employ the Market Approach, using industry-standard multiples, or the Income Approach via Discounted Cash Flow (DCF), the method you choose dictates the residual figure assigned to goodwill on your balance sheet.

A professional valuation provides more than just a price tag; it establishes a robust audit trail for HMRC. If the “residual” goodwill, the portion of the purchase price that cannot be attributed to tangible assets or specific intellectual property, is not supported by rigorous data, your claim for goodwill amortisation for dental practices may be vulnerable to challenge. We ensure that every calculation is backed by commercial reality to protect your long-term position and ensure compliance during potential audits.

EBITDA Multiples in the 2026 Dental Market

The 2026 market shows a clear divergence between private and NHS-heavy practices. Private clinics continue to command higher multiples, often driven by their scalable patient plans and cosmetic revenue. Conversely, NHS practices face tighter scrutiny due to contract stability concerns and inflationary pressures on delivery. Rising interest rates have introduced a level of caution, as the cost of debt service now weighs more heavily on a buyer’s return on investment.

“Add-backs” and “normalisation” are critical here. By adjusting for one-off refurbishments or personal expenses through the business, we can accurately reflect the practice’s true earning potential. This adjustment directly influences the final goodwill figure, and consequently, the total value available for future relief through goodwill amortisation for dental practices.

Purchase Price Allocation (PPA) Strategies

Effective tax planning requires a delicate balance during the PPA process. You must decide how to allocate the purchase price between tangible assets, which qualify for capital allowances, and intangible assets like goodwill. While tangible assets may offer a more immediate write-down through the Annual Investment Allowance, the 6.5% fixed-rate election for goodwill provides a steady, predictable reduction in taxable profit over several years.

Integrating these PPA decisions with your broader small business accountant strategy ensures that your practice’s growth isn’t hampered by inefficient tax structures. We look at the total lifecycle of your investment, ensuring that amortisation works in tandem with other relief mechanisms to optimize your overall cash flow. This holistic view is what separates a mere service provider from a strategic partner.

Navigating Pitfalls: The 2015-2019 “Black Hole” and 2026 BADR Changes

The historical context of your practice’s acquisition or incorporation defines your present tax liabilities. Between 8 July 2015 and 31 March 2019, practitioners entered what is often termed the “black hole” period. During these years, tax relief for goodwill was entirely abolished. If you acquired a practice or incorporated your business within this specific window, the goodwill sits on your balance sheet as a “tax-nothing,” offering no relief under the Intangible Fixed Assets regime. This historical legacy remains a significant hurdle for those seeking to optimise goodwill amortisation for dental practices today.

As we approach 2026, the focus shifts from historical acquisition traps to the tax implications of an exit. A major legislative change occurs on 6 April 2026, when the Business Asset Disposal Relief (BADR) rate increases from 14% to 18%. For practice owners planning a sale, this 4% jump represents a substantial reduction in net proceeds. When combined with the £1 million lifetime limit for BADR, the importance of precise timing and structural preparation becomes paramount. If your lifetime limit is already exhausted, gains on goodwill are typically taxed at the main Capital Gains Tax rate of 24% for higher-rate taxpayers.

The Incorporation Trap

Transferring goodwill from a sole trader or partnership to a limited company no longer yields the tax advantages it once did. HMRC’s “Related Party” rules are designed specifically to prevent artificial claims. You cannot simply sell goodwill to a company you control to trigger a new cycle of relief. If the goodwill was created or held by a related party before 2015, or during the black hole period, it remains ineligible for amortisation. We often explore strategic alternatives, such as retaining goodwill personally or utilising specific share structures, when traditional relief is unavailable.

Planning for a 2026 Exit

Timing your sale around the April 2026 transition requires a balanced view of market multiples and tax rates. While selling before the BADR increase to 18% may seem logical, you must also consider the “Capital Gains vs. Income” debate. Ensuring your tax advice in the UK accounts for these shifting rates is essential for protecting your final take-home value. A sale concluded on 5 April 2026 could be significantly more profitable than one completed just 24 hours later, provided the transaction is commercial and defensible.

The complexity of these rules means that generic accounting often fails to protect the clinician’s interests. To ensure your exit strategy is robust against these legislative shifts, contact our dental tax specialists for a comprehensive review of your practice’s tax position.

Implementation: How Specialist Dental Accountants Secure Your Position

The successful application of the Intangible Fixed Assets regime requires more than a basic understanding of tax law; it demands a meticulous approach to implementation. At Davis & Co LLP, we act as strategic partners during the acquisition and restructuring phases to ensure that every fiscal opportunity is captured. While the theory of goodwill amortisation for dental practices is straightforward, the execution often fails when handled by generic firms that lack sector-specific insight. A generalist may overlook the specific intellectual property requirements that unlock the 6.5% relief, leaving significant capital on the table.

Establishing a robust “Year 1” accounting setup is the most critical step in protecting your future claims. We ensure that your initial balance sheet entries are not only accurate but fully defensible against potential HMRC scrutiny. This proactive stance provides the predictability you need for long-term cash flow management. Our team integrates these amortisation strategies into your broader financial architecture, whether that involves international tax planning for complex portfolios or a focused personal wealth strategy for your eventual retirement.

Our Approach to Purchase Price Allocation

We perform a detailed analysis of your acquisition to identify every pound of qualifying intellectual property. This process involves liaising with specialist valuers to ensure the goodwill figure is grounded in commercial reality and is HMRC-robust. Our work doesn’t end at the point of sale; we provide ongoing monitoring of your amortisation schedules. This ensures that the tax relief remains consistent with your practice’s evolving operational needs and that your financial reporting remains beyond reproach.

The Davis & Co LLP Partnership

Working with us provides the understated confidence necessary to navigate even the most complex HMRC enquiries. We don’t just focus on annual compliance; we’re committed to the long-term growth and stability of your practice. Our role is to provide the intellectual rigour and professional discretion that high-calibre dental professionals expect from their advisors. We invite you to request a consultation with our dental tax specialists to discuss your specific practice valuation and explore the full potential of goodwill amortisation for dental practices within your business structure.

Securing Your Practice’s Fiscal Legacy

The landscape of practice ownership is increasingly defined by the precision of your tax planning. Successfully managing goodwill amortisation for dental practices requires a proactive approach to purchase price allocation and a deep understanding of the Intangible Fixed Assets regime. By aligning your intellectual property valuation with current HMRC standards, you transform a significant acquisition cost into a sustainable cash-flow advantage.

As the Business Asset Disposal Relief rate rises to 18% in April 2026, the cost of an unstructured exit becomes significantly higher. Professional guidance ensures you navigate these transitions with composed authority. As Chartered Certified Accountants with a history of success spanning over 120 years, we provide the specialist expertise required to accelerate your business growth while maintaining total compliance. We understand the nuances of dental practice tax and the rigorous requirements of modern valuation.

Consult our specialist dental tax advisors at Davis & Co LLP to discuss how our expertise in HMRC Intangible Fixed Asset regimes can protect your practice’s valuation. We look forward to partnering with you to secure a prosperous and tax-efficient future for your clinical practice.

Frequently Asked Questions

Can I still amortise goodwill if I buy a dental practice as a sole trader?

No, you cannot claim this relief as a sole trader. The Intangible Fixed Assets regime is a corporate tax benefit reserved exclusively for limited companies. If you operate as an unincorporated practitioner, goodwill is treated as a capital asset rather than a revenue-deductible expense. Many clinicians consider incorporation specifically to access these professional tax advantages.

What happens to my goodwill amortisation if I sell the practice within five years?

Selling your practice triggers a comparison between the sale proceeds and the asset’s tax-written-down value. If the sale price is higher, you’ll likely face a balancing charge, which effectively treats the previously claimed relief as taxable profit. This ensures you only benefit from the actual economic depreciation of the asset during your period of ownership.

Is the 6.5% fixed-rate relief mandatory, or can I choose a different rate?

The 6.5% rate is a fixed election available for relevant assets acquired after April 2019. While you can opt for an accounts-based approach if the asset has a reliably estimable useful life, the fixed-rate election provides greater predictability. Most practitioners prefer this method to avoid subjective debates with HMRC over the actual lifespan of their practice assets.

How does the 2026 BADR increase affect the value of my goodwill upon exit?

The scheduled increase from 14% to 18% in April 2026 reduces the net cash you retain from the sale of your practice goodwill. While it doesn’t change the gross market valuation, it significantly impacts your post-tax return. Strategic timing is essential to manage this transition, particularly if you’re approaching your £1 million lifetime limit for relief.

What constitutes “qualifying intellectual property” in a typical dental practice?

Qualifying intellectual property typically includes registered trademarks, clinical patents, or specific rights to patient database software. In a dental context, the brand name and established patient management systems are the most common examples. Identifying these assets is vital for unlocking goodwill amortisation for dental practices under current legislation.

Can I claim relief on goodwill if I purchased the practice from a family member?

Claims involving family members are usually restricted by “Related Party” rules. HMRC prevents taxpayers from creating artificial tax deductions through transactions between connected persons. If the goodwill was previously held by a relative or a company they control, it’s highly unlikely to qualify for the 6.5% fixed-rate relief regardless of the purchase price.

What is the “6x IP cap” and how does it practically limit my tax deductions?

The 6x IP cap limits the amount of goodwill eligible for tax relief to six times the value assigned to qualifying intellectual property in the same transaction. If you purchase a practice with £500,000 of goodwill but only £10,000 of IP, your eligible goodwill for relief is capped at £60,000. This makes precise IP valuation a critical component of your acquisition planning.

Should I revalue my practice goodwill if I am planning to incorporate in 2026?

Revaluing your goodwill is necessary to establish a fair market price for the transfer to your new company. This sets your Capital Gains Tax baseline for the transaction. However, you must remember that incorporating an existing business usually won’t trigger new goodwill amortisation for dental practices due to the strict related party restrictions governing these transfers.