A clean audit report isn’t a prize won during the final weeks of the financial year; it’s the inevitable result of twelve months of disciplined governance. We understand that for many UK directors, the process often brings a sense of unease. With the Financial Reporting Council’s new supervisory model having launched in April 2026, the margin for error has narrowed significantly. You likely recognise the pressure to present a flawless set of accounts to stakeholders while fearing the market volatility that follows a “limitation of scope” or a qualified report.

Avoiding a qualified audit opinion requires more than just tidy spreadsheets. It demands a proactive alignment with the revised ISA (UK) 240 and 570 standards issued in March 2026, which place greater emphasis on fraud risk and going concern assessments. This article provides a comprehensive framework to ensure your financial reporting meets these rigorous benchmarks. We’ll explore how to strengthen your internal controls and manage the transition to the new 2026 audit exemption thresholds, ensuring your business remains resilient and well-regarded by the market.

Key Takeaways

- Understand why an unmodified audit report serves as the essential benchmark for financial transparency and protects your firm’s credit rating.

- Identify the common reporting triggers and material thresholds that directors must monitor when avoiding a qualified audit opinion.

- Grasp the critical distinctions between qualified, adverse, and disclaimer reports to better understand the long-term implications for your company’s reputation.

- Master a five-step framework for strengthening internal controls and engaging with auditors early on complex or unusual transactions.

- See how bespoke assurance services provide the strategic clarity needed to satisfy stakeholders while maintaining a clean bill of health.

The Strategic Importance of an Unmodified Audit Opinion

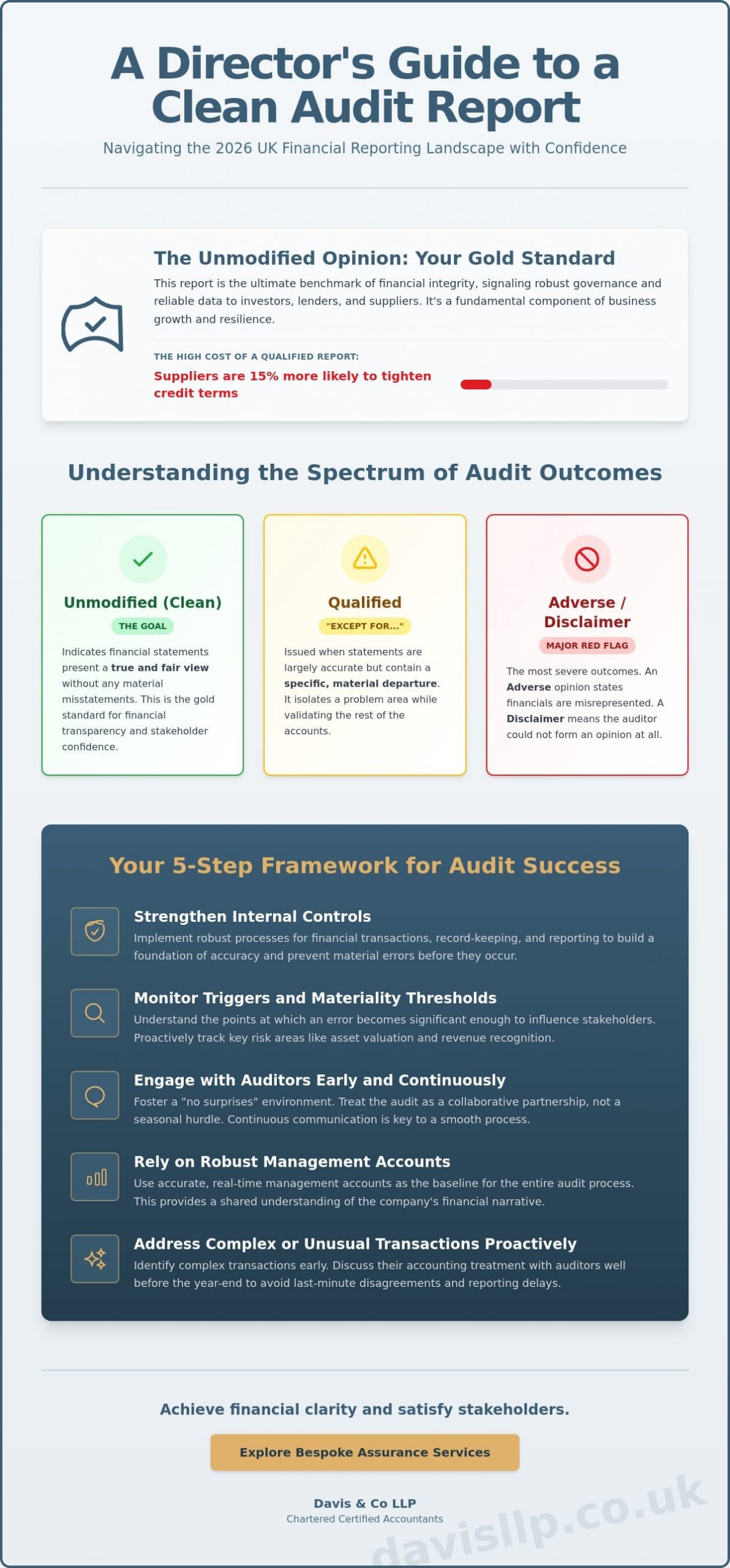

An unmodified opinion represents the gold standard of financial integrity in the UK corporate environment. It serves as a definitive statement from an independent professional that your financial statements present a true and fair view of the company’s position. For a director, achieving this outcome is a fundamental component of Business Growth Acceleration. It signals to the market that your internal governance is robust and your data is reliable. The structure and implications of the formal Auditor’s Report provide the primary lens through which external stakeholders assess your management’s competence. When a report is qualified, it suggests a breakdown in either record-keeping or transparency, which can have immediate commercial consequences.

The link between audit outcomes and business credit ratings is direct and often unforgiving. Credit reference agencies frequently downgrade firms that receive anything less than a clean bill of health, as a qualification represents an unquantified risk. This isn’t just a concern for public companies; private SMEs often face restricted access to trade credit insurance if their accounts are flagged. Avoiding a qualified audit opinion is, therefore, a pragmatic necessity for maintaining the liquidity required to fund daily operations and long-term expansion.

Reputational Risks and Capital Access

Lenders and investors view a qualified opinion as a significant red flag that triggers intensive due diligence. In the current 2026 financial climate, where the FRC has intensified its supervisory model, banks have become increasingly sensitive to “limitation of scope” caveats. A qualification can lead to a “valuation haircut” during merger or acquisition talks, as buyers discount the purchase price to compensate for the uncertainty in the balance sheet. Beyond capital, your position in the national supply chain depends on trust. Suppliers are 15% more likely to tighten credit terms or demand pro-forma payments if they perceive instability in your statutory filings.

The Auditor-Management Partnership

We view the audit process as a collaborative assurance model rather than a seasonal hurdle. The most successful directors foster a “no surprises” environment through continuous communication with their audit team. This partnership relies on the quality of underlying data. Relying on robust, real-time management accounts provides the baseline for audit success. By identifying complex transactions early and discussing their accounting treatment before the year-end, you move from a reactive stance to a position of strategic control. This proactive engagement ensures that when the final report is drafted, it reflects a shared understanding of the company’s financial narrative, effectively mitigating the risk of last-minute disagreements or reporting delays.

Common Triggers for a Qualified Audit Opinion

A qualified audit opinion is an “except for” report issued when financial statements are largely accurate but contain specific material departures from standards. This distinction is vital for directors to grasp. It signifies that, while the majority of the financial narrative is reliable, there’s a specific area where the auditor either disagrees with the management’s treatment or lacks the evidence to confirm the figures. Avoiding a qualified audit opinion requires a precise understanding of materiality. This threshold represents the point at which an error or omission becomes significant enough to influence the economic decisions of a stakeholder. Auditors don’t seek perfection in every penny; they seek assurance that no misstatement is large enough to distort the company’s true financial position.

When an auditor issues this type of report, they use the “except for” clause to isolate the problem. This allows the rest of the accounts to remain validated, which prevents a total loss of stakeholder confidence. However, the presence of even a single qualification can trigger restrictive covenants in loan agreements or complicate future equity raises. You can find detailed technical guidance on these Departures from Unqualified Opinions through international standards, which mirror the rigorous approach taken by UK regulators in 2026.

Disagreement with Accounting Treatments

Qualifications often arise from fundamental disagreements regarding asset valuation or revenue recognition. If a board insists on a valuation for a property or intellectual property that exceeds what the auditor considers “fair value” under UK GAAP or IFRS, a qualification is inevitable. Disputes also frequently occur over the adequacy of bad debt provisions or the timing of revenue on complex, multi-year contracts. These areas rely heavily on professional judgement. Directors must ensure their accounting estimates are supported by documented logic and market data to withstand auditor scrutiny. Our Audit and Assurance specialists often find that early dialogue on these estimates is the most effective way to reach a consensus before the final reporting deadline.

Limitation of Scope: The Evidence Gap

A “limitation of scope” occurs when the auditor is unable to perform the necessary procedures to verify a balance. This isn’t necessarily a sign of wrongdoing, but rather a gap in the available evidence. Common examples include the inability to attend a physical inventory count at a remote warehouse or a lack of access to the records of a newly acquired subsidiary. To remediate these gaps, directors should implement rigorous record-keeping protocols from the first day of the financial year. If documentation is missing, you must work with your advisors to find alternative evidence, such as third-party confirmations or subsequent cash testing, to satisfy the auditor’s requirements and prevent the issue from becoming “pervasive.”

Clean vs. Qualified vs. Adverse: Comparing Audit Outcomes

The audit report is a spectrum of assurance rather than a simple pass or fail grade. At the summit sits the unqualified opinion, confirming that your accounts present a true and fair view in all material respects. This is the outcome every director seeks to protect the firm’s reputation. However, when issues arise, the auditor must choose between several modified opinions based on the severity and reach of the findings. Avoiding a qualified audit opinion is often a matter of ensuring that any disagreements or evidence gaps remain isolated rather than systemic. If a problem is deemed “material but not pervasive,” a qualification is issued. If the issues are so fundamental that they render the entire set of accounts misleading, the report moves into the far more damaging territory of an adverse opinion.

An “Emphasis of Matter” paragraph occupies a unique space. It doesn’t constitute a qualification; instead, it draws the reader’s attention to a matter already appropriately disclosed in the accounts, such as a significant legal dispute or a major post-balance sheet event. While it doesn’t “taint” the audit, it acts as a signal to stakeholders that certain risks deserve closer inspection. Conversely, a “Disclaimer of Opinion” represents the ultimate failure of the audit process. This occurs when the auditor cannot obtain sufficient evidence to form any conclusion at all, often due to catastrophic record-keeping failures or severe limitations imposed by management.

A Comparison Framework for Directors

To evaluate the potential impact on your business, it’s helpful to view these outcomes through the lens of stakeholder reaction and reporting severity.

| Report Type | Level of Assurance | Likely Stakeholder Reaction |

|---|---|---|

| Unqualified | High (True and Fair) | Full confidence; standard credit terms maintained. |

| Qualified | Moderate (“Except for”) | Increased scrutiny; potential inquiry from lenders. |

| Adverse | None (Not True and Fair) | Severe alarm; likely breach of loan covenants. |

| Disclaimer | None (No Opinion) | Immediate loss of credibility; risk of regulatory action. |

The Going Concern Assessment

The March 2026 revisions to ISA (UK) 570 have placed the auditor’s assessment of a company’s viability under a microscope. Directors must now provide even more robust evidence of their ability to continue operating for at least twelve months from the date the financial statements are authorised. A “Material Uncertainty Related to Going Concern” disclosure is a specific type of warning that can appear even in an otherwise clean report. It doesn’t mean the company is insolvent, but it indicates that certain conditions exist that may cast significant doubt on its future.

You can mitigate this risk by demonstrating solvency through rigorous cash flow management. For audits of financial statements for periods beginning on or after 15 December 2026, the threshold for these assessments will be even higher. Proactive directors use detailed sensitivity analysis and stress-testing to show auditors that the business can withstand adverse economic shifts, effectively bridging the gap between a cautionary disclosure and a clean bill of health.

A Five-Step Strategy for Avoiding a Qualified Opinion

Securing an unmodified report is a year-round commitment to precision rather than a frantic exercise conducted in the weeks following your year-end. Management holds the primary responsibility for the preparation of financial statements; therefore, the board must take a lead role in avoiding a qualified audit opinion by fostering an environment of transparency. We recommend a structured five-step approach to ensure your board remains in control of the financial narrative:

- Early Engagement: Proactively flag complex or unusual transactions, such as a £2 million property acquisition or a new revenue-sharing agreement, as they occur during the year.

- Control Strengthening: Review your authorisation levels to ensure no single individual has end-to-end control over a significant financial cycle.

- Audit-Ready Files: Maintain a “permanent file” containing updated legal contracts, board minutes, and property title deeds to prevent delays.

- Prior-Year Remediation: Actively address the “management letter” points raised in the previous year’s audit to demonstrate a trajectory of improvement.

- Specialist Support: Engage external audit and assurance expertise to review technical disclosures and complex accounting treatments before the statutory auditors arrive.

Internal Controls and Documentation

A robust “control environment” is the most effective defence against a limitation of scope. Auditors are required to test the systems that produce your numbers; if those systems are weak, the volume of substantive testing increases, as does the risk of an unresolved discrepancy. Segregation of duties is essential. For instance, the person who authorises a supplier payment shouldn’t be the same person who reconciles the bank account. Implementing digital bookkeeping services can significantly reduce manual entry errors, which currently account for approximately 25% of all material misstatements in SME accounts. A clear, digital paper trail allows auditors to verify transactions with minimal friction, protecting you from evidence gaps.

Proactive Dispute Resolution

The most common cause of a qualified opinion is a late-stage disagreement over an accounting estimate. Whether it’s the valuation of work-in-progress or the impairment of goodwill, these areas rely on professional judgement. We suggest a “no surprises” policy where management presents its logic and supporting evidence for these estimates well in advance of the audit field work. If a technical dispute arises, seeking a “second opinion” or conducting a pre-audit health check can provide the clarity needed to adjust your position or strengthen your argument. Resolving these issues early in the cycle ensures the final reporting process remains a matter of routine rather than a source of boardroom anxiety.

If you are concerned about how the revised 2026 auditing standards might impact your upcoming filing, our team can provide a bespoke assurance review to identify and resolve potential triggers before they reach your statutory report.

Bespoke Assurance: The Davis & Co LLP Approach

At Davis & Co LLP, we believe the audit process should be a source of clarity rather than a period of annual uncertainty. Our philosophy of “quiet excellence” ensures that we provide a robust statutory or voluntary audit that stands up to the highest levels of professional scrutiny. We don’t view the audit as a mere regulatory hurdle; instead, we position it as a strategic tool for Business Growth Acceleration. By providing insights into operational efficiencies and risk management, we help directors look beyond the balance sheet to identify the underlying drivers of value within their organisations.

Avoiding a qualified audit opinion is especially complex for businesses with cross-border operations or intricate corporate structures. Our deep expertise in international tax planning allows us to support complex group audits where transfer pricing and overseas subsidiary valuations often present significant reporting risks. We work meticulously to ensure that every component of a group structure is aligned with current UK GAAP and IFRS requirements. This creates a seamless consolidation process that satisfies both local and international stakeholders, ensuring that your global footprint is matched by global reporting integrity.

Tailored Solutions for Complex Entities

We understand that a one-size-fits-all approach is insufficient for the nuanced needs of family offices or international groups. Our team provides specialised assurance for niche sectors, including our dedicated dental practice expertise, where the interpretation of associate contracts and practice valuations requires specific industry knowledge. By staying ahead of the Financial Reporting Council’s April 2026 supervisory model changes, we ensure your firm remains compliant with the most recent ISA (UK) standards. Our approach is characterized by a composed partnership; we provide the necessary professional distance while remaining accessible to your management team throughout the year.

Securing Your Financial Future

A clean audit opinion is more than a yearly requirement; it’s the foundation of your corporate legacy and a signal of your firm’s enduring stability. Whether you’re preparing for a future exit or seeking to strengthen your market position, the assurance of an unmodified report is indispensable in a volatile economic landscape. We invite you to take the next step in protecting your business’s reputation and ensuring your financial reporting remains beyond reproach. Our national team is available for a confidential consultation to discuss your specific audit and assurance needs.

Consult our audit and assurance specialists today to begin a collaborative partnership focused on your long-term success.

Strengthening Your Corporate Reputation and Future Growth

A clean audit report doesn’t happen by accident; it’s the result of a deliberate, year-round commitment to governance. The 2026 corporate landscape demands a higher level of transparency than ever before. With the FRC’s revised standards on fraud and going concern now in effect, the path to an unmodified report requires diligence rather than seasonal effort. You’ve seen how robust internal controls and early engagement with your auditors form the bedrock of a successful filing. By prioritising these strategic actions, you’re not just avoiding a qualified audit opinion; you’re actively protecting your firm’s credit rating and stakeholder trust.

As Chartered Certified Accountants since 1901, we bring a legacy of quiet excellence to every engagement. We specialise in complex international group assurance and provide the bespoke insights needed to turn compliance into a driver for business growth. Our approach is designed to provide you with the security of a professional expert while maintaining the collaborative partnership your board requires.

Secure your clean bill of health with Davis & Co LLP audit services

We look forward to helping you maintain the robust financial integrity that your business deserves.

Frequently Asked Questions

What is the difference between a clean and a qualified audit opinion?

A clean or unmodified opinion confirms that your financial statements present a true and fair view of the company’s position in all material respects. In contrast, a qualified opinion includes an “except for” statement. This indicates that while the majority of the report is reliable, there are specific material misstatements or evidence gaps that prevent a full endorsement. Directors should focus on avoiding a qualified audit opinion to maintain maximum stakeholder confidence and protect their firm’s creditworthiness.

Can a company survive a qualified audit opinion?

Companies can certainly survive a qualification, but they often face immediate commercial friction. Lenders may view the report as a breach of loan covenants, potentially leading to a 1% to 2% increase in interest rates or a reduction in credit limits. While not a terminal event, it requires a clear remediation plan to reassure suppliers and investors that the underlying business remains viable. The reputational recovery typically takes at least two years of subsequent clean reports to fully restore market trust.

How much does it cost to fix a qualified audit report?

The cost of rectifying the underlying issues depends entirely on the nature of the qualification, such as rebuilding accounting records or performing retrospective valuations. While we don’t provide fixed fees for these bespoke services, the indirect costs are often more significant. These include potential “valuation haircuts” during a sale or the increased cost of capital from lenders who now perceive the company as a higher risk due to the reporting caveat.

Does a qualified opinion always mean there is fraud?

A qualified opinion doesn’t automatically imply fraud. Most qualifications in the UK result from technical disagreements over accounting treatments or a “limitation of scope” where evidence is missing. However, under the revised ISA (UK) 240 standards issued in March 2026, auditors have enhanced responsibilities to report on fraud risks. A qualification due to a lack of evidence can sometimes lead stakeholders to question the integrity of the control environment, even if no fraud has occurred.

How can I change an auditor’s mind about a qualification?

You can’t simply “change an auditor’s mind” through persuasion; you must provide “sufficient appropriate evidence” to resolve their concerns. This typically involves producing the missing documentation or adjusting the financial statements to reflect the auditor’s preferred accounting treatment. Early engagement is the most effective strategy for avoiding a qualified audit opinion, as it allows time for these adjustments to be made before the final report is signed and filed at Companies House.

What happens if a subsidiary has poor records but the group is clean?

If a subsidiary’s records are poor, the group auditor must determine if the discrepancy is material to the consolidated financial statements. If the subsidiary accounts for more than 5% to 10% of group assets or turnover, its poor records could trigger a qualification for the entire group. Directors of parent companies must ensure that newly acquired or remote subsidiaries adhere to the same rigorous reporting standards as the head office to prevent a localized issue from tainting the group report.

Is an “Emphasis of Matter” the same as a qualification?

An “Emphasis of Matter” is not a qualification. It’s a paragraph used by auditors to draw attention to a matter that’s already correctly disclosed in the financial statements, such as a significant legal dispute or a major post-balance sheet event. While it doesn’t “taint” the audit opinion, it serves as a signal to readers that they should carefully consider the specific risks mentioned. It’s a tool for transparency that doesn’t suggest a failure in the accounting records themselves.

How long does a qualified opinion stay on a company’s record?

A qualified opinion remains on the public record at Companies House effectively indefinitely, as the accounts are part of the firm’s permanent filing history. While the immediate impact on credit ratings often diminishes after three years of subsequent clean reports, the qualification will always be visible to anyone conducting historical due diligence. This permanent record underscores why maintaining a clean audit bill of health is a critical component of a director’s professional legacy and the company’s long-term value.