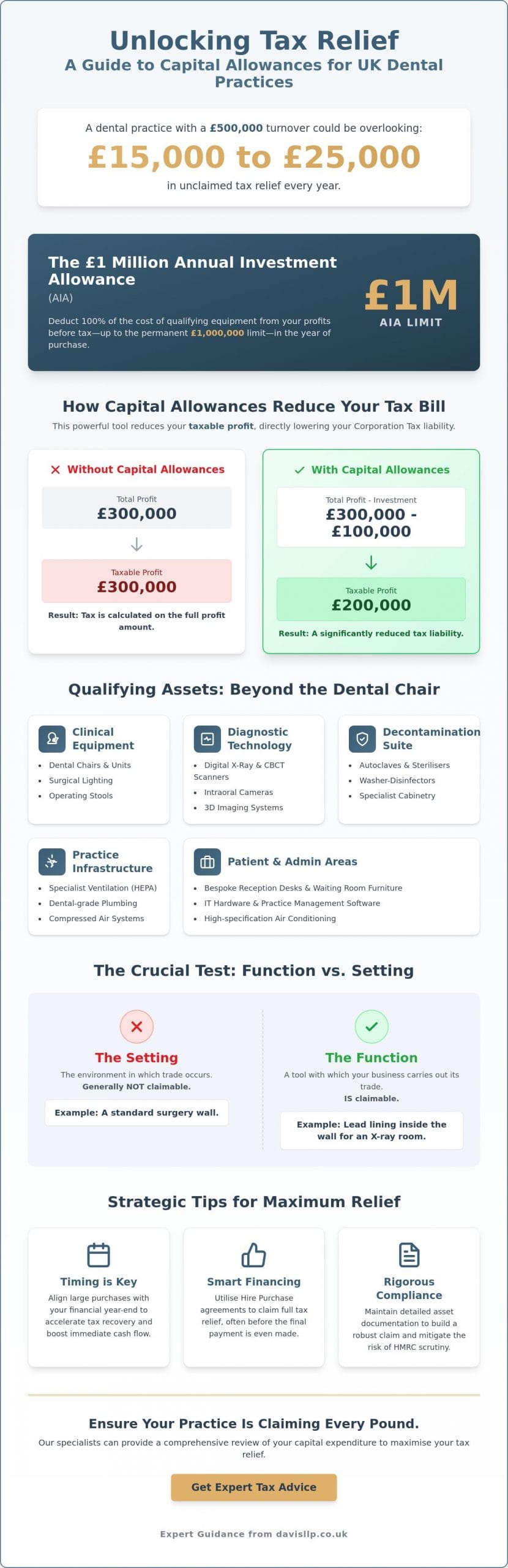

Did you know that a private dental practice with a £500,000 turnover could be overlooking between £15,000 and £25,000 in unclaimed tax relief? We understand that the high upfront costs of modern clinical technology, from 3D scanners to high-specification dental chairs, often place a significant burden on your practice’s liquidity. Mastering the nuances of capital allowances for dental equipment uk is no longer a secondary administrative task; it’s a vital component of your strategic financial management.

We recognize that the 25% Corporation Tax rate for profits exceeding £250,000 has introduced a new layer of complexity to your annual planning. This guide provides a sophisticated framework to help you manage these shifts, ensuring you claim every pound of relief you’re entitled to under the latest 2026 standards. We’ll examine how the permanent £1 million Annual Investment Allowance works alongside building alterations to reduce your taxable profits and secure the cash flow necessary for your next phase of expansion.

Key Takeaways

- Identify the specific clinical and diagnostic assets that transition from simple capital expenditure to powerful tax-saving instruments within your practice.

- Navigate the 2026 tax landscape by utilizing the £1 million Annual Investment Allowance to secure immediate relief on capital allowances for dental equipment uk.

- Align your investment timing with the practice financial year-end to accelerate tax recovery and enhance your immediate operational liquidity.

- Evaluate the strategic benefits of Hire Purchase agreements, which often allow for full tax claims to be realized before the final payment is made.

- Establish a rigorous compliance framework through detailed asset documentation and specialist guidance to mitigate the risk of HMRC scrutiny.

The Fundamentals of Capital Allowances for UK Dental Practices

In the technical sphere of UK tax law, accounting depreciation is not a tax-deductible expense. Instead, the government provides Capital Allowances as a statutory replacement. This mechanism allows your practice to deduct the cost of qualifying capital assets from your trading profits before tax is calculated. For a high-intensity clinical environment, understanding the distinction between revenue and capital expenditure is vital. Revenue expenditure covers day-to-day operational costs like dental consumables and staff wages, which are deducted in full during the year they occur. Capital expenditure involves long-term investments in assets that serve the business over several years, such as digital imaging systems or surgery refurbishments.

Dental practices are uniquely positioned to benefit from these claims due to their heavy reliance on sophisticated, high-value technology. While a standard office might only claim for computers and furniture, a dental surgery requires complex plumbing, specialized lighting, and pressurized air systems. These investments often represent a significant portion of a practice’s turnover. By correctly identifying capital allowances for dental equipment uk, we help practice owners preserve vital cash flow, particularly during major refurbishments where upfront costs can otherwise stifle growth.

The Mechanism of Tax Relief

It is a common misconception that capital allowances act as a direct “cash back” or tax credit. In reality, they function by reducing your “taxable profits.” If your practice earns £300,000 in profit but invests £100,000 in qualifying equipment, your tax liability is calculated on the remaining £200,000. This is particularly relevant for sole trader dental associates who must navigate the 2026 personal tax bands; reducing your taxable income can prevent you from slipping into a higher tax bracket or losing your personal allowance. Securing expert tax advice in the UK ensures these mechanisms are applied to your specific career stage, whether you’re an associate or a multi-site practice owner.

Plant and Machinery: The Core Category

To qualify for relief, an asset must generally fall under the “plant and machinery” category. This requires passing the “function test” rather than the “setting test.” In simple terms, the asset must be a tool with which your business carries out its trade, not merely the setting or environment in which the trade happens. While a standard wall is part of the “setting” and does not qualify, the lead lining within that wall for an X-ray room serves a functional clinical purpose and is therefore claimable. Establishing the “expected life” of these assets is equally important, as it determines the rate of writing-down allowances if you exceed your annual investment limits. Most clinical capital allowances for dental equipment uk fall into the main pool, though certain integral features of the building may be subject to different rates.

Qualifying Dental Assets: Beyond the Dental Chair

While the dental chair is the most visible investment in a surgery, it represents only a fraction of the assets that qualify for relief. A comprehensive claim for capital allowances for dental equipment uk extends into every corner of the practice. Clinical essentials like delivery units, surgical lighting, and operating stools are standard inclusions. However, diagnostic technology often carries a higher price tag and offers significant relief potential. This includes digital X-ray sets, CBCT scanners, and intraoral cameras. Even the decontamination suite, with its autoclaves, washer-disinfectors, and specialist cabinetry, forms a core part of your claimable capital expenditure.

Broadening the scope further, we look at the practice infrastructure. High-specification air conditioning and specialist ventilation (HEPA) systems aren’t just comfort features; they’re functional requirements for modern infection control. Similarly, dental-grade plumbing and compressed air systems qualify as integral features. Even patient-facing areas contribute. Bespoke reception desks, waiting room furniture, and the IT hardware required for practice management software are all valid assets. Following the UK government guidance on capital allowances helps ensure that these diverse items are correctly categorized to maximize your claim.

The “Hidden” Allowable Costs in Refurbishments

Refurbishment projects often contain hidden costs that generalist accountants might overlook. Specialist electrical wiring for X-ray equipment and dental units is a functional necessity, not just a building improvement. If you’ve had to install reinforced flooring to support heavy clinical machinery or partition walls with lead lining for radiation protection, these are qualifying capital expenditures. They serve a specific clinical function rather than just providing the setting for the business. If you’re planning a surgery update, our dental tax specialist team can help identify these embedded costs before the project begins.

Digital Transformation Assets

The shift toward digital dentistry introduces new categories of qualifying assets. CAD/CAM milling machines and 3D printing stations for in-house labs represent significant capital investments. Software licences are more nuanced; they typically qualify as capital expenditure if they provide an enduring benefit to the practice, whereas annual subscriptions might be treated as revenue costs. Don’t forget the server infrastructure and cybersecurity hardware necessary to protect sensitive patient data. These technological foundations are essential for a modern practice and are fully eligible for relief under the current 2026 rules.

The 2026 Tax Landscape: AIA, Full Expensing, and Business Structure

The fiscal environment for 2026 presents both challenges and strategic openings for the modern dental practice. Central to this is the Annual Investment Allowance (AIA), which remains a cornerstone of effective tax planning. With a permanent limit of £1 million, the AIA allows your practice to deduct the full cost of qualifying capital allowances for dental equipment uk from your profits in the year of purchase. This 100% immediate relief is a powerful tool for maintaining liquidity while upgrading clinical technology. It’s particularly effective for sole traders and partnerships who don’t have access to the full expensing regimes reserved for incorporated entities.

For practices operating as limited companies, the landscape offers even greater flexibility. Full Expensing allows incorporated businesses to claim a 100% first-year allowance on new main rate plant and machinery. This means that even if you’ve already utilised your £1 million AIA on other projects, such as a major surgery refurbishment, you can still achieve full relief on new equipment like CBCT scanners or dental chairs. Additionally, a 50% first-year allowance is available for “special rate” assets, including integral features like lighting and heating systems. These mechanisms are vital when navigating the 25% main rate of Corporation Tax; a well-timed claim can often reduce your taxable profits enough to benefit from the 19% small profits rate or marginal relief.

Incorporation as a Strategic Choice

Choosing to incorporate your practice is a significant structural pivot that unlocks the full benefits of the 2026 expensing rules. While the tax savings on new assets are substantial, we must carefully balance these gains against the potential loss of NHS pension benefits for those with significant health service contracts. We believe this decision shouldn’t be made in isolation. Engaging a strategic small business accountant allows us to model these outcomes precisely, ensuring your business structure supports both your immediate tax efficiency and your long-term retirement goals.

Writing Down Allowances (WDA)

When an investment doesn’t qualify for immediate 100% relief, we manage the remaining value through Writing Down Allowances. Assets are generally split into two categories: the Main Pool, which attracts an 18% annual deduction, and the Special Rate Pool, which receives 6%. Most clinical capital allowances for dental equipment uk sit in the main pool, while integral building features fall into the special rate. We also monitor balancing charges closely; if you sell or trade-in old equipment for a price higher than its remaining tax value, a charge may arise. Proactive management of these pools ensures that the “tail” of your capital allowances continues to provide tax benefits throughout the lifecycle of your equipment.

Financial Strategy: Timing Purchases and Financing Models

The effectiveness of your tax planning depends heavily on the synchronisation of your investment cycle with your financial year-end. By strategically timing the acquisition of new clinical technology, you can significantly accelerate the tax relief available. For many practices, reinvesting surplus profits into new equipment just before the year-end is a proven method to reduce the immediate tax bill. However, it’s vital to remember the “delivery and installation” rule; an asset is generally only eligible for capital allowances for dental equipment uk once the obligation to pay becomes unconditional, which usually coincides with the equipment being brought into use.

The choice between financing models also dictates the timing and scale of your relief. Hire Purchase (HP) agreements are particularly advantageous for dental professionals. Under an HP contract, HMRC treats the practice as the owner of the asset from the moment it’s brought into use, allowing you to claim the full Annual Investment Allowance on the total purchase price immediately. This is true even though the actual cash payments are spread over several years. In contrast, operating leases often fail to qualify for capital allowances because the legal ownership remains with the lessor. In those cases, you’d only receive tax relief on the monthly rental payments as a revenue expense, which lacks the immediate impact of a front-loaded capital claim.

The Year-End Reinvestment Strategy

Accelerating a purchase by even a few days can move your tax relief forward by an entire year. We often work with clients to forecast their annual profits to determine if an immediate claim is optimal or if deferring the investment might yield better results in a future period where higher tax rates might apply. It’s a delicate balance. While the “Super-deduction” of previous years has concluded, the permanent 100% AIA and Full Expensing for limited companies provide a stable foundation for these multi-year forecasts. If you’re unsure how your current financing affects your eligibility, our dental tax specialist team can review your agreements to ensure they’re structured for maximum efficiency.

VAT and Capital Allowances Interaction

For practices that are VAT-exempt or partially exempt, the calculation of qualifying costs requires precision. If your practice cannot reclaim the VAT on a new digital scanner, that non-reclaimable VAT is added to the capital cost of the asset for your allowance claim. This effectively increases the relief you receive on the total “gross” investment. When using Hire Purchase, remember that VAT is typically due upfront on the full purchase price, whereas the interest elements are treated as a separate revenue expense. For large-scale dental property projects exceeding £250,000, the “capital goods scheme” threshold may apply, requiring adjustments to your VAT recovery over a ten-year period.

Navigating Compliance and Specialist Dental Tax Advice

While the fiscal benefits of claiming tax relief are substantial, they must be balanced with a rigorous approach to compliance. HMRC’s increased focus on corporate tax filings means that surface-level claims are no longer sufficient. We believe that every claim should be supported by detailed asset logs and a clear justification of use that explains the clinical necessity of the expenditure. This level of detail is where the distinction between a generalist accountant and a specialist dental tax advisor becomes most apparent. A generalist might overlook the nuances of dental-grade infrastructure, whereas our team at Davis & Co LLP understands how to categorise complex clinical assets correctly.

One of the most effective ways to improve your practice’s financial position is through a retrospective review. It’s common for practices to have significant unclaimed allowances from previous years, particularly following a change in ownership or a major surgery refurbishment. We work with our clients to identify these missed opportunities, often recovering thousands of pounds in tax relief that can be reinvested into the business. The Davis & Co LLP approach is to treat these claims as part of a multi-year growth strategy rather than a one-off tax filing. This ensures your capital investment plan remains aligned with your broader commercial goals.

The Importance of Intellectual Rigour in Claims

Success in complex tax matters requires more than just following a checklist. We apply intellectual rigour to every claim, moving beyond standard asset lists to defend bespoke clinical installations. When building alterations are involved, we document the specific clinical requirements, such as radiation shielding or specialist plumbing, to satisfy HMRC’s function test. We also ensure that any structural changes remain compliant with GDC regulatory requirements for bodies corporate. This thoroughness provides the security and peace of mind necessary for a professional practice to invest with confidence.

Next Steps: Securing Your Practice Finances

Securing your practice’s financial future begins with choosing the right partner. Knowing how to find a chartered accountant who understands the dental industry’s unique capital needs is a strategic advantage. Our process starts with a comprehensive Davis & Co LLP capital allowance audit of your existing practice, where we scrutinise both current and past investments. We also collaborate directly with your clinical equipment suppliers to ensure that invoicing is transparent and tax-compliant from the outset. By establishing these robust foundations, we help you maximise your relief on capital allowances for dental equipment uk while maintaining absolute compliance with current 2026 standards.

Securing Your Practice’s Financial Future for 2026 and Beyond

The 2026 fiscal landscape offers a unique opportunity for dental practices to transform their tax liabilities into clinical growth. By aligning your investment cycle with the £1 million Annual Investment Allowance and the benefits of Full Expensing, you can significantly reduce taxable profits and improve liquidity. We’ve explored how the right business structure and precise timing are essential for maximising capital allowances for dental equipment uk, ensuring that your practice remains both competitive and compliant in an evolving market.

Managing these complexities requires more than a generalist approach; it demands the intellectual rigour of a dedicated strategic partner. As Chartered Certified Accountants since 1901, we offer niche expertise in dental tax and practice growth. We specialise in international and complex UK tax planning, providing the discretion and precision your professional matters deserve. We invite you to Book a Specialist Dental Tax Consultation with Davis & Co LLP to evaluate your current position. We look forward to helping you secure a stable and prosperous future for your practice.

Frequently Asked Questions

What is the maximum I can claim for dental equipment in 2026?

The maximum immediate claim is £1 million per year through the Annual Investment Allowance (AIA). This allows you to deduct 100% of qualifying expenditure on clinical technology from your taxable profits in the year of purchase. If your investment exceeds this £1 million threshold, you can still claim relief through writing-down allowances at either 18% or 6% annually, depending on the asset’s specific classification.

Can I claim capital allowances on a second-hand dental chair?

You can absolutely claim capital allowances on second-hand equipment through the AIA. It’s a common misconception that tax relief is restricted to brand-new items. While the “Full Expensing” regime is reserved for new assets purchased by limited companies, the AIA remains a flexible and powerful tool for practices acquiring pre-owned chairs, delivery units, or diagnostic sets from other providers.

Do building alterations like lead lining for X-rays qualify for tax relief?

Lead lining and other clinical alterations are eligible for relief because they serve a functional purpose necessary for dental radiography. These structural changes move beyond the “setting” of the business and qualify as plant and machinery. This category also includes specialised plumbing, reinforced flooring designed to support heavy surgery units, and bespoke ventilation systems required for modern infection control standards.

How does “Full Expensing” differ from the Annual Investment Allowance for dentists?

The AIA provides a 100% deduction on up to £1 million of spending for all business structures, including sole traders and partnerships. Full Expensing is an uncapped 100% relief available exclusively to limited companies for new main-rate assets. For incorporated practices, Full Expensing is a strategic choice when the £1 million AIA limit has already been reached on other capital projects.

What happens to my capital allowances if I sell my dental practice?

Selling your practice triggers a “balancing event” for tax purposes. If the sale price allocated to the equipment is higher than its remaining tax value in your pools, a balancing charge arises, which is added to your taxable profits. We believe that the proper allocation of the sale price within the purchase agreement is vital to managing this potential tax liability effectively.

Can dental associates claim capital allowances on their own portable equipment?

Dental associates are entitled to claim capital allowances for dental equipment uk that they purchase personally for their work. If you invest in your own loupes, surgical motors, or specialised handpieces, these are treated as capital assets of your individual trade. This relief directly reduces the profits subject to your personal income tax and Class 4 National Insurance contributions.

Is it better to lease or buy dental equipment from a tax perspective?

Outright purchase or Hire Purchase is often more tax-efficient for immediate relief as these methods allow you to claim the full AIA in the year the equipment is brought into use. Operating leases, while beneficial for cash flow, typically only allow you to deduct monthly rentals as revenue expenses. This effectively defers the tax benefit over the entire term of the lease.

How far back can I go to claim missed capital allowances on my surgery?

You can often identify and claim for assets purchased several years ago, provided you still own and use them in the practice today. While there are strict limits on amending previous tax returns, you can frequently bring the “unclaimed” value of old assets into your current tax computation. This retrospective approach is a core part of how we identify hidden value in existing surgeries.