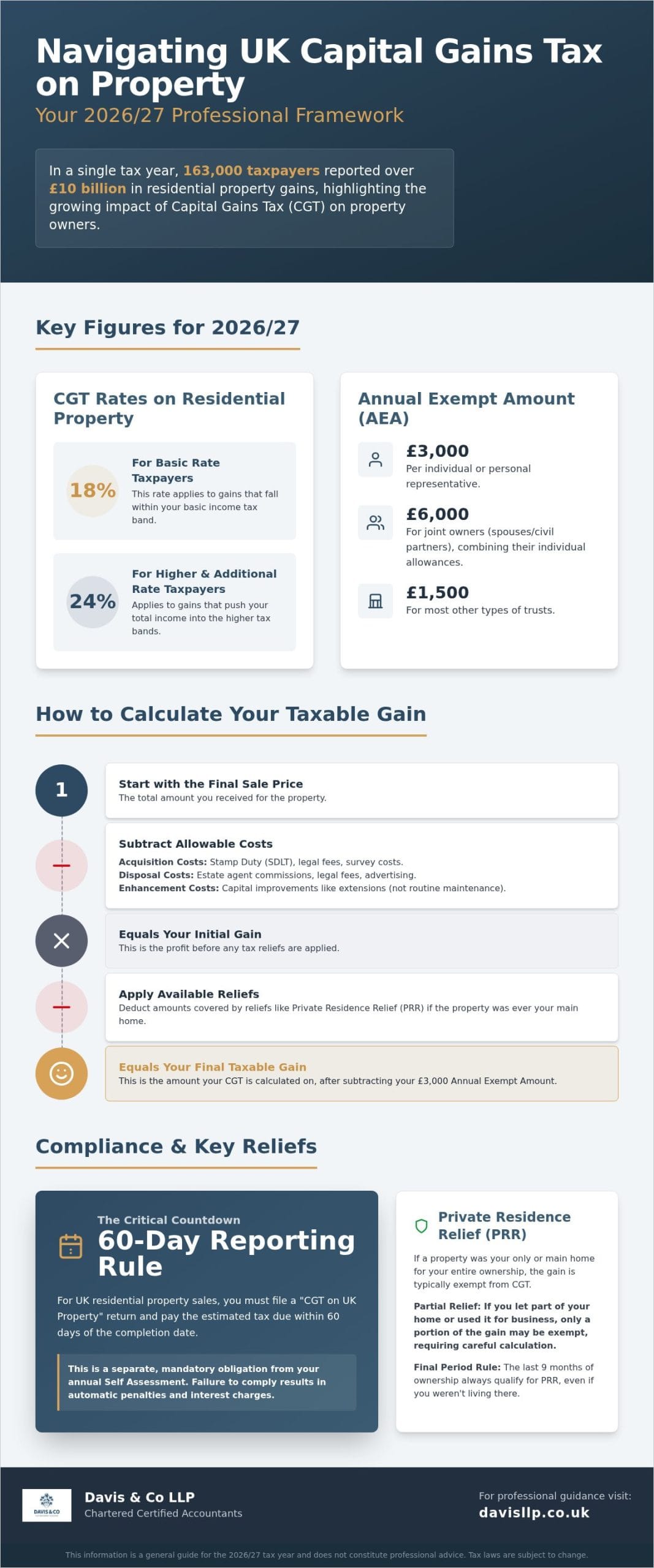

In the 2024 to 2025 tax year, 163,000 taxpayers filed a capital gains tax on property uk return, reporting more than £10 billion in residential gains. This record high demonstrates how a shrinking Annual Exempt Amount, now set at just £3,000 for the 2026/27 period, has brought a wider range of property owners into the scope of HMRC. For many, the prospect of surrendering up to 24% of their investment growth is a source of understandable concern.

We recognize that the complexity of the current tax regime often leads to unnecessary stress. The 60-day deadline for reporting and payment is unforgiving; the distinction between capital improvements and routine maintenance remains a frequent point of confusion. You deserve a clear strategy that prioritizes both compliance and the preservation of your wealth. Our collective experience suggests that while tax is inevitable, the amount you pay is often a variable that can be managed through diligent planning and professional oversight.

This guide offers a professional framework to help you calculate your liability and maximize the use of available reliefs. We will detail the specific 2026/27 rates, clarify which renovation costs qualify as allowable expenses, and provide a step by step approach to meeting your reporting obligations. By the end of this article, you’ll have the insights needed to approach your property disposal with composure and strategic foresight.

Key Takeaways

- Master the precise formula for calculating your taxable gain, including which legal fees, estate agent commissions, and acquisition costs qualify as allowable expenses.

- Discover how to maximize Private Residence Relief (PRR) and utilize the “Final Period of Ownership” rule to protect your investment yields on former primary homes.

- Understand the critical operational differences between your standard Self Assessment and the mandatory 60-day reporting account for capital gains tax on property uk.

- Identify the strategic timing required to meet HMRC’s strict payment window and avoid the financial impact of non-compliance penalties and interest.

- Explore why a proactive approach to property accounting is essential for navigating complex HMRC investigations and ensuring long-term fiscal stability.

Understanding Capital Gains Tax on UK Property in 2026

Understanding Capital Gains Tax begins with a clear definition: it’s not a tax on the total amount of money you receive, but rather on the profit or “gain” realized when you dispose of an asset. For property owners, this gain is the difference between what you paid for the property and the price at which you sold it, adjusted for allowable costs. As of the 2026/27 tax year, capital gains tax on property uk remains a significant consideration for investors and second-home owners alike.

The current rate structure distinguishes between your total taxable income and the size of your gain. Basic rate taxpayers are subject to an 18% rate on residential property gains, while higher and additional rate taxpayers face a 24% charge. While residential property historically carried higher rates than other assets, legislative changes have aligned the rates for non-residential property, such as commercial premises and land, with these residential figures. This creates a uniform tax environment for most property disposals, though the reporting requirements for residential sales remain uniquely stringent.

We often find that the most pressing administrative challenge for any seller is the 60-day reporting and payment window. HMRC requires that a “CGT on UK Property” return be filed and the estimated tax paid within 60 days of the completion date. This is a separate obligation from your annual Self Assessment return. Failure to meet this deadline often results in immediate penalties and accruing interest, making proactive preparation essential before the sale even concludes.

Chargeable Assets vs. Exemptions

Most property that isn’t your primary home is considered a chargeable asset. This includes buy-to-let investments, holiday homes, and business premises. However, Private Residence Relief (PRR) remains the cornerstone of property tax planning. If a property has been your only or main home throughout your entire period of ownership, you typically won’t pay any tax on the sale. Complexity arises when a property has served multiple purposes. If you’ve let out part of your home or used a specific area exclusively for business, you may only be entitled to partial relief, requiring a precise calculation of the chargeable portion of the gain.

The 2026 Annual Exempt Amount

The Annual Exempt Amount (AEA) has undergone significant reductions in recent years, stabilizing at £3,000 for the 2026/27 tax year. This tax-free allowance is available to individuals and personal representatives, while trustees for disabled people also receive this full amount. For other types of trusts, the allowance is generally halved to £1,500. Strategic asset positioning is often beneficial here; for instance, properties held in joint names by spouses or civil partners allow both individuals to apply their £3,000 allowance against the gain, effectively creating a £6,000 tax-free threshold for the disposal.

Calculating Your Taxable Gain: Allowable Expenses and Enhancements

Arriving at an accurate figure for capital gains tax on property uk requires a meticulous review of your financial records. The fundamental calculation is straightforward: your gross gain is the sale price minus the purchase price and allowable costs. However, the nuance lies in defining what HMRC classifies as allowable. Miscalculating these figures can lead to either an overpayment of tax or, conversely, an underpayment that invites scrutiny and potential penalties.

Allowable acquisition costs typically include Stamp Duty Land Tax (SDLT), survey fees, and legal charges incurred during the initial purchase. When disposing of the asset, you can also subtract estate agent commissions, legal fees, and advertising costs. These incidental expenses are vital for reducing your taxable exposure. While you can find the official Capital Gains Tax rates on government portals, the application of these rates depends entirely on the precision of your cost-base analysis. If you’re unsure how to categorize specific historical expenditures, our team at Davis & Co LLP can provide a comprehensive review of your records to ensure every legitimate deduction is captured.

A frequent point of contention involves the distinction between capital improvements and day to day maintenance. Maintenance costs, such as painting or repairing a leaky roof, are generally considered revenue expenses and cannot be deducted from your capital gain. Instead, these are often offset against rental income. Capital improvements, however, must add value to the property or significantly prolong its life to be deductible against the gain.

Capital Improvements: What HMRC Accepts

HMRC accepts costs for significant structural changes that enhance the property’s value. Examples include loft conversions, extensions, or the installation of a first time central heating system. It’s vital to distinguish these from like-for-like replacements. Replacing old wooden window frames with modern double glazing of a similar standard is often viewed as a repair. However, if the work involves a significant upgrade that changes the property’s character, it may qualify. We recommend maintaining a comprehensive capital expenditure log, supported by invoices and contracts, throughout your period of ownership.

Rebasing for Long-Term Ownership

For properties held for several decades, the 1982 rebasing rule is essential. If you acquired a property before 31 March 1982, you can use its market value on that date as your base cost rather than the original purchase price. Similarly, non-residents disposing of UK residential property can often use the market value as of 5 April 2015 to calculate their gain. This rebasing ensures you aren’t taxed on gains that accrued before the relevant legislation applied to you. Obtaining a professional, retrospective valuation is often necessary to establish an accurate and defensible base cost for HMRC.

Strategic Reliefs for Landlords and International Investors

Minimizing the impact of capital gains tax on property uk often relies on the strategic application of statutory reliefs. These are not merely administrative checkboxes but sophisticated tools that, when applied correctly, preserve significant portions of an investor’s equity. We believe that a proactive approach to these reliefs is essential, as eligibility often depends on decisions made years before a disposal occurs.

Private Residence Relief (PRR) remains the primary shield for homeowners. Even if you’ve transitioned a former home into a rental investment, the final 9 months of ownership are generally treated as tax-free, provided the property was once your main residence. This “Final Period of Ownership” rule allows for a transitional period without penalizing the seller for the time it takes to secure a buyer. However, it’s vital to recognize that Lettings Relief has been fundamentally restricted. Previously a generous allowance for landlords, it now only applies in cases of shared occupancy where the owner resided in the property alongside the tenant. For most traditional buy-to-let investors, this relief is no longer a viable option for reducing liability.

For those operating across borders, international tax planning is indispensable. Non-residents are liable for UK tax on gains from both residential and commercial property, a requirement that often creates a dual reporting obligation. While double taxation treaties usually prevent paying tax twice, the administrative burden remains high. Compliance with The 60-Day Reporting Rule is mandatory for non-residents regardless of whether a tax liability exists, necessitating a disciplined approach to documentation.

Non-Resident Capital Gains Tax (NRCGT)

The UK’s approach to non-resident capital gains tax on property uk encompasses all types of land and buildings. The interaction between UK legislation and your local country of residence tax laws requires a high-calibre advisor to navigate correctly. For instance, a gain might be calculated differently in the UK versus a jurisdiction like the US or France, potentially leading to timing mismatches for tax credits. Utilizing specialized international tax services ensures that these cross-border complexities don’t erode your investment returns.

Business Asset Disposal Relief (BADR)

Business Asset Disposal Relief (BADR) offers a reduced tax rate on qualifying gains up to a lifetime limit of £1 million. While many associate this with selling a company, it can apply to property used within a trade. It’s important to note that for the 2026/27 tax year, the rate for gains qualifying for BADR is 18%, a significant shift from previous years. Furnished Holiday Lets (FHLs) historically qualified for these benefits, but the 2026 outlook requires careful monitoring as legislative shifts continue to target these specific tax advantages. Strategic pitfalls often arise when properties are held within a company structure or when the “business use” of the asset isn’t clearly defined for the duration of ownership.

The 60-Day Reporting Rule: Compliance and Strategic Timing

Meeting the administrative requirements for capital gains tax on property uk is often more time sensitive than the sale itself. Since October 2021, the window to report a disposal and pay the estimated tax has been fixed at 60 days from the date of completion. This isn’t a mere suggestion; it’s a rigid statutory deadline. We often observe that taxpayers confuse this requirement with their annual Self Assessment. In reality, you must create a dedicated “Capital Gains Tax on UK Property” account to settle the liability long before your year end tax return is even due.

Strategic timing plays a pivotal role in managing your liquidity. If a sale completes in late March, the gain falls into the current tax year, requiring payment within the 60-day window. However, delaying completion until after April 6 moves the disposal into the following tax year. While the 60-day rule still applies for the initial payment, the final reconciliation on your Self Assessment return is pushed back by an entire year. This shift can significantly alter your cash flow and determine which year’s Annual Exempt Amount you utilize. If you’re planning a disposal near the end of the fiscal year, our property accounting services can help you model the most tax efficient completion date.

HMRC applies interest and penalties with little hesitation for late submissions. Even if there’s no tax to pay because of reliefs, certain non-residents must still file a return. The financial impact of a late filing penalty, combined with interest on the unpaid tax, can quickly erode the profits from your sale. Precision in your initial estimate is vital to avoid these unnecessary costs.

Offsetting Losses and Annual Planning

You can reduce your property tax bill by offsetting capital losses incurred from other assets, such as the sale of shares or other investments. If your total losses exceed your gains in a single year, you can carry the remaining balance forward to offset against future property disposals indefinitely. The £3,000 annual exempt amount is a “use it or lose it” allowance that cannot be carried over to subsequent tax years, making it essential to utilize it fully within the current period.

Preparing for the HMRC Digital Return

The digital return requires exhaustive documentation, including original purchase dates, a breakdown of acquisition costs, and the final disposal value. Gathering these records while the sale is in progress, rather than after completion, is the only reliable way to meet the 60-day deadline. Many sellers find that the complexity of multi-asset portfolios or historical improvements requires expert tax advice in the UK to ensure the return is both accurate and defensible under HMRC scrutiny.

The Role of a Strategic Property Accountant

Effective management of capital gains tax on property uk requires more than just numerical accuracy; it demands a proactive approach that anticipates legislative shifts and individual circumstances. We believe that the role of a strategic advisor is to move beyond simple compliance. While calculating the gain is a necessary step, the true value lies in the preceding months and years of planning. At Davis & Co LLP, we provide the technical precision and professional gravitas required to manage high-value disposals with composure. When dealing with the 24% higher rate tax or complex relief structures, the involvement of a Chartered Accountant offers a vital layer of protection against HMRC investigations, ensuring that every deduction is both legitimate and defensible.

A reactive approach often leads to missed opportunities for relief or errors in the 60-day reporting window. By contrast, a partnership based on foresight allows us to prepare the necessary documentation long before a sale reaches completion. This meticulous preparation is what distinguishes a routine filing from a robust tax strategy. We focus on the organizational and individual impact of your property assets, ensuring that your financial decisions align with your broader objectives for growth and stability.

Beyond the Calculation: Holistic Tax Management

A property sale shouldn’t be viewed in isolation. To truly optimize your position, it is essential to integrate property disposals into your broader personal tax plan. This holistic view is particularly important when considering the tax implications of transferring property into a limited company, a process that requires careful navigation of both capital gains tax and Stamp Duty Land Tax. For clients with commercial portfolios, our small business accountants provide the specialized oversight needed to manage corporate property assets while maintaining business growth acceleration and cash flow efficiency.

Securing Your Legacy with Davis & Co LLP

Our firm is dedicated to intergenerational wealth preservation. A long-term partnership allows us to maintain a detailed capital expenditure log over the years, making the eventual reporting of capital gains tax on property uk seamless and accurate. This historical perspective is invaluable when establishing a defensible base cost for properties held for decades. We ensure your reporting is robust enough to withstand the most rigorous HMRC scrutiny, providing you with the peace of mind that your legacy is secure. We recommend scheduling a strategic review with our team before you list your property for sale, allowing us to identify the most efficient path forward for your specific circumstances.

Securing Your Property Investment Yields for the Future

Managing the complexities of capital gains tax on property uk requires a blend of technical precision and proactive timing. The foundation of a successful disposal lies in the meticulous documentation of allowable costs and the strategic application of statutory reliefs. By addressing the 60-day reporting window with foresight rather than urgency, you can avoid the financial friction of penalties and maintain the integrity of your investment portfolio.

At Davis & Co LLP, we’ve served as Chartered Certified Accountants since 1901, providing discreet and authoritative advice to high-net-worth individuals. Our specialization in property accounting and international tax allows us to navigate the most intricate cross-border challenges with composed expertise. We position ourselves as your strategic partner, ensuring that every disposal is optimized for both immediate compliance and long-term wealth preservation.

Before you commit to a transaction, it’s essential to model the potential impact on your broader financial landscape. Consult our Property Tax Specialists for a Strategic Disposal Review to ensure your next move is as tax-efficient as possible. We’re here to help you move forward with confidence and clarity.

Frequently Asked Questions

Do I pay Capital Gains Tax on my main home in the UK?

You generally don’t pay tax on your main home if it qualifies for Private Residence Relief (PRR). This relief applies provided the property has been your only or main residence throughout your ownership. However, you might face a liability if you’ve used part of the home exclusively for business, let out a portion of it, or if the grounds exceed 0.5 hectares.

What are the Capital Gains Tax rates for residential property in 2026?

For the 2026/27 tax year, the rates are 18% for basic rate taxpayers and 24% for those in the higher or additional rate bands. These specific percentages apply to the gain realized on residential assets after deducting your annual allowance. Understanding the capital gains tax on property uk rates is essential for accurate cash flow modeling before you finalize a disposal.

How long do I have to report a property sale to HMRC?

You must report the sale and pay the estimated tax within 60 days of the completion date. This deadline is strict and separate from your annual Self Assessment obligations. Failing to meet this window often triggers immediate penalties and interest charges; we recommend preparing your documentation well in advance of the sale to ensure compliance.

Can I deduct the cost of a new kitchen from my Capital Gains Tax bill?

You can only deduct the cost of a new kitchen if it represents a capital improvement rather than a routine repair. If you’re replacing a functional kitchen with a similar standard, HMRC typically views this as maintenance. However, if the work involves structural changes or a significant upgrade that increases the property’s value, it may qualify as an allowable enhancement.

What happens if I sell a UK property while living abroad?

Non-residents are liable for tax on all UK property disposals and must file a return within 60 days, regardless of whether a gain is realized. You can often use the April 2015 rebasing rule to calculate your gain from that date forward. This ensures you aren’t taxed on growth that occurred before the current non-resident legislation was introduced.

Is there an annual tax-free allowance for Capital Gains in 2026?

The Annual Exempt Amount (AEA) for individuals in the 2026/27 tax year is £3,000. This tax-free allowance can’t be carried forward to future years, so it’s a “use it or lose it” benefit. For properties held in joint names, such as by spouses, you can effectively combine your allowances to shield up to £6,000 of the gain from capital gains tax on property uk.

Can I offset a loss on a property sale against other income?

No, you cannot offset a capital loss from a property sale against your general employment or self-employment income. Capital losses can only be used to reduce taxable gains from other assets, such as shares or additional properties. If your losses exceed your gains in a single year, you can carry them forward to offset against future capital gains indefinitely.

Do I need to report a sale if no tax is due?

UK residents don’t usually need to report the sale of a main residence if the disposal is fully covered by Private Residence Relief. However, if you’re a non-resident, you must report the sale of any UK land or property within 60 days even if there’s no tax to pay. Residents must also report disposals of second homes if the total proceeds exceed four times the annual allowance.