In 2026, the success of a property disposal is no longer defined by the headline tax rate, but by the surgical precision of your ‘allowable expenditure’ records and the speed of your reporting. We understand that the reduced £3,000 annual exempt amount feels restrictive, especially when paired with the stringent 60-day window for reporting and payment. Managing capital gains tax on second property uk 2026 requires more than just an awareness of the 18% and 24% rates; it demands a proactive approach to documentation and a clear-eyed understanding of HMRC’s evolving expectations.

You’re right to feel concerned about the complexity of identifying every deductible capital improvement or the risk of late-filing penalties. Our aim is to provide you with the clarity needed to navigate these technicalities with confidence. We’ll outline a definitive timeline for compliance, demonstrate how to calculate your potential liability accurately, and explore the strategic reliefs that can legally reduce your final bill. By the end of this guide, you’ll have a robust framework to ensure your property disposal is both compliant and tax-efficient.

Key Takeaways

- Determine how your total taxable income dictates your placement within the 18% or 24% residential tax brackets for the 2026/27 year.

- Differentiate between deductible capital improvements and routine maintenance to ensure you accurately offset your final gain.

- Maintain compliance by mastering the 60-day window for reporting and paying capital gains tax on second property uk 2026.

- Uncover the strategic benefits of integrating individual property sales into a comprehensive trust and inheritance tax framework.

- Recognize how joint ownership and the £3,000 annual exempt amount can be leveraged to minimize the overall tax burden on your portfolio.

Understanding Capital Gains Tax on UK Residential Property in 2026

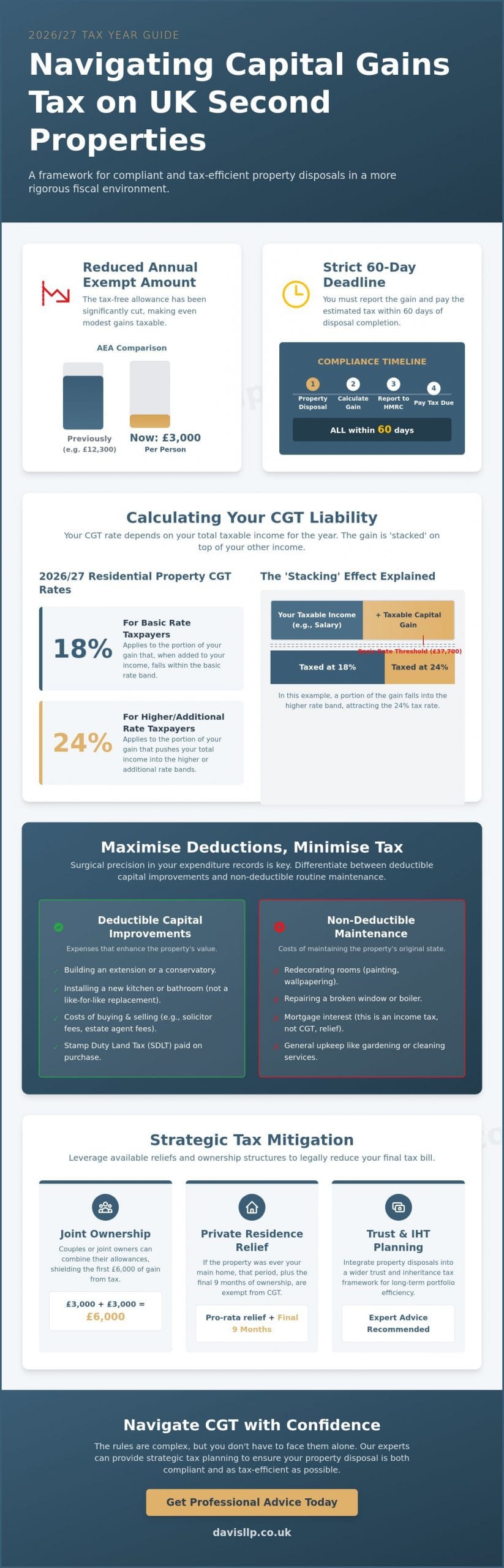

At its core, Capital Gains Tax (CGT) is a levy on the profit realized when you dispose of an asset that has increased in value. It’s the ‘gain’ you make, rather than the total amount you receive, that HMRC seeks to tax. For those managing a portfolio, the 2026/27 tax year introduces a more rigorous fiscal environment. The historical framework of Capital Gains Tax in the United Kingdom has evolved to create a clear distinction between residential property and other assets, such as shares or commercial buildings. While other assets may attract lower rates, residential disposals are subject to 18% for basic rate taxpayers and 24% for those in the higher or additional rate bands.

The 2026 landscape is particularly notable for the reduced Annual Exempt Amount, which now stands at just £3,000 per person. This reduction means that even modest gains on a capital gains tax on second property uk 2026 disposal will likely result in a taxable event. We’ve observed that this shift places a greater emphasis on meticulous record-keeping. Small-scale investors can no longer rely on a generous tax-free allowance to buffer their gains; instead, every pound of profit above the £3,000 threshold must be accounted for and reported within the mandatory 60-day window.

The Scope of Chargeable Residential Assets

HMRC maintains a broad definition of what constitutes a ‘second property’. This category includes buy-to-let investments, holiday homes, and inherited properties that haven’t served as your primary residence. When you inherit a property, the ‘cost’ for CGT purposes is typically the market value at the date of the previous owner’s death, known as the probate value. If the property’s value increases between that date and the eventual sale, CGT applies to that specific uplift. It’s also vital to recognize that properties held in trust are subject to specific 2026 regulations, where trustees generally face a flat 24% rate on any gains made upon disposal.

Private Residence Relief (PRR) and its Limitations

Private Residence Relief remains the most significant tool for reducing liability, but its application to second properties is often partial. If you lived in the property as your main home for a portion of your ownership, we can help you calculate a pro-rata relief for those years. In 2026, the ‘final period’ exemption remains at 9 months, allowing you to claim relief for the last three quarters of ownership regardless of whether you occupied the property during that time. However, letting relief is now highly restricted. It’s generally only available to those who shared the occupancy of their home with a tenant, making it largely irrelevant for traditional buy-to-let disposals.

Calculating Your Liability: 2026 CGT Rates and Thresholds

Precise calculation of your liability requires a granular understanding of how HMRC categorizes your total annual income. For the 2026/27 tax year, the residential property rates remain distinct from other asset classes, fixed at 18% for basic rate taxpayers and 24% for those in the higher or additional rate bands. These Capital Gains Tax rates and allowances are applied after you’ve utilized your £3,000 Annual Exempt Amount (AEA). For couples who jointly own a property, this allowance can be combined to shield £6,000 of the total gain from taxation, provided the ownership structure is correctly documented prior to disposal.

The calculation isn’t a simple flat-rate assessment. Instead, it’s a “stacking” exercise. Your taxable capital gain is added to your other taxable income for the year, such as salary, dividends, or rental profits. If the combined figure exceeds the basic rate threshold of £37,700, the portion of the gain that falls above this limit is taxed at the higher 24% rate. This interaction makes the timing of a sale critical. A significant gain on a capital gains tax on second property uk 2026 can easily push a basic rate earner into the higher bracket, substantially increasing the tax burden on a single transaction.

Income Tax Interaction and the ‘Banding’ Effect

One effective method to mitigate this “banding” risk is the strategic use of pension contributions. By making a grossed-up contribution to a registered pension scheme, you effectively extend your basic rate band. This can keep a larger portion of your property gain within the 18% bracket rather than the 24% tier. It’s a sophisticated technique that requires careful timing within the same tax year as the disposal. We often assist clients in identifying these opportunities to ensure their broader financial goals align with their immediate tax obligations.

The NRCGT Regime for International Owners

International owners face a unique set of challenges under the Non-Resident Capital Gains Tax (NRCGT) rules. If you’re a non-UK resident selling UK residential interests, you’re generally only taxed on the gain made since April 2015. This “rebasing” rule ensures that any growth in value prior to that date isn’t captured by the UK tax net. However, the reporting requirements are strict; you must notify HMRC of the disposal within 60 days, even if no tax is due or you’ve made a loss. For those with complex cross-border interests, our international tax planning services provide the necessary oversight to manage these obligations seamlessly. If you’re unsure how your residency status impacts your disposal, a consultation with our personal tax services team can provide the tailored clarity you require.

Mitigation Strategies: Reducing Your 2026 CGT Bill

Reducing your liability for capital gains tax on second property uk 2026 begins with a granular review of your acquisition and disposal costs. Every pound spent during the purchase or sale process serves as a legitimate deduction from your gross gain. This includes Stamp Duty Land Tax paid at acquisition, legal fees for the conveyance, and estate agent commissions upon disposal. For owners of mixed-use assets, such as a residential flat situated above a commercial unit, the calculation becomes more nuanced. In these instances, we must apportion the gain between the residential and commercial components. This precision prevents the inadvertent application of the higher 24% residential rate to the entirety of a diversified asset, ensuring you only pay what’s strictly necessary on the residential portion.

Another vital tool in your strategic arsenal is the ability to offset capital losses. If you’ve realized losses on other assets, such as a portfolio of shares or a commercial building, these can be deducted from your residential property gain in the same tax year. You can also carry forward unused losses from previous years to shield your current profits. Navigating the official guidance on Tax when you sell property reveals that these deductions aren’t automatic. They require proactive reporting to HMRC to be valid, even if the loss results in no tax being due for the period.

Capital Improvements vs. Revenue Repairs

Distinguishing between capital expenditure and revenue repairs is a frequent point of contention with HMRC. A capital improvement is an enhancement that adds value to a property rather than merely restoring it to its previous condition. For example, replacing a dilapidated roof with identical materials is generally viewed as a repair, whereas adding an extension or installing a modern central heating system where none existed before constitutes a capital improvement. For 2026 compliance, you must retain all invoices, contracts, and proof of payment. Without this documentary evidence, HMRC may disallow these deductions, significantly inflating your taxable gain.

Joint Ownership and Gifting Strategies

The 2026 reduction of the Annual Exempt Amount to £3,000 makes joint ownership strategies more compelling. Transfers between spouses or civil partners occur on a ‘no gain, no loss’ basis, allowing you to move a portion of the property’s equity to a partner who may be in a lower income tax bracket. This maneuver effectively doubles the available tax-free allowance to £6,000 and can help keep the remaining gain within the 18% basic rate band. However, exercise caution when gifting property to children. Such transfers are treated as disposals at market value for CGT purposes and may also trigger Stamp Duty implications if a mortgage is attached to the title.

The 60-Day Rule: HMRC Reporting and Payment Deadlines

Compliance in 2026 is anchored by the 60-day reporting and payment window. This mandatory timeframe begins on the date of completion, not the date of exchange. You must submit a ‘tax on account’ return and pay the estimated liability within this period. Failure to meet this deadline triggers immediate penalties, starting at £100, with further charges and interest accruing as the delay persists. While the annual Self Assessment remains necessary for final reconciliation, this mid-year reporting ensures HMRC receives funds closer to the point of disposal. When calculating capital gains tax on second property uk 2026, the speed of your administrative response is as vital as the accuracy of your figures.

You don’t need to file a 60-day return if the disposal is covered entirely by Private Residence Relief or if the gain falls below your remaining £3,000 annual exempt amount. However, if any tax is due, the obligation is absolute. Timing your disposal requires a strategic view of the calendar. A sale completed on April 1st requires payment by May 31st. A sale completed on April 7th moves the reporting obligation into a new tax year’s administrative cycle, though the 60-day rule remains constant. This choice can significantly impact your short-term cash flow management.

The Reporting Process: A Step-by-Step Checklist

The process requires a dedicated ‘Capital Gains Tax on UK Property’ account, which is separate from your standard Government Gateway login. You’ll need to provide an estimate of your total taxable income for the year to determine whether the 18% or 24% rate applies. Because the tax year is often still in progress, this calculation is technically an estimate. If your final year-end income is lower than predicted, or if subsequent capital losses occur, we can help you reclaim any overpaid tax through your standard Self Assessment return.

Common Pitfalls in the 60-Day Window

A frequent source of confusion is the distinction between exchange and completion. For tax purposes, the disposal date is the date of exchange, which determines the tax year the gain falls into. However, the 60-day countdown for reporting only begins at completion. This nuance is critical for sales occurring near the April 5th threshold. Delays often arise from incomplete cost data or late valuations from solicitors, making early preparation essential. Utilizing expert tax advice in the UK ensures these technical distinctions are managed correctly, protecting you from avoidable HMRC scrutiny. For a bespoke analysis of your disposal timeline, consider a consultation with our property accounting specialists.

Strategic Tax Planning with Davis & Co LLP

Effective management of capital gains tax on second property uk 2026 transcends the mere fulfillment of reporting deadlines. While the 60-day rule provides a rigid framework for compliance, our approach focuses on the broader fiscal narrative of your portfolio. We view each disposal not as an isolated event, but as a pivotal moment within your wider financial trajectory. Our dual-location expertise, with offices in both London and Harpenden, allows us to provide this high-calibre oversight to a diverse national client base. We offer the discretion and professional gravitas required when handling sensitive commercial and personal matters, ensuring that your wealth is protected through meticulous analytical thought.

For high-net-worth individuals, the interaction between property disposals and other tax heads is often complex. A sale doesn’t just trigger a CGT liability; it alters the composition of your estate for Inheritance Tax purposes and may impact existing trust structures. We specialize in integrating these disposals into a cohesive strategy that prioritizes long-term stability. By aligning your property accounting with your broader trust and estate planning, we ensure that every transaction serves your ultimate objectives. This level of precision is essential in an environment where the margin for error has been narrowed by reduced allowances and increased HMRC scrutiny.

Tailored Property Accounting for Investors

Managing a portfolio with multiple residential and commercial interests requires a specialized level of oversight. We provide the clarity needed for complex “Mixed-Use” disposals, where apportioning gains correctly is the difference between a standard tax bill and an overpayment. For those operating through corporate structures, our strategic small business accountant services offer a pathway to sustainable growth. We ensure that your property company’s accounting remains robust, allowing you to focus on acquisition and development while we manage the technicalities of compliance and cash flow.

Securing Your Financial Future

The 2026 tax landscape demands a partner who acts as a strategic advisor rather than a mere service provider. Professional advice is your most effective safeguard against the risks of late reporting or inaccurate calculations. We pride ourselves on building composed partnerships with our clients, offering the secure, well-advised distance of an expert while remaining deeply committed to your success. As you manage the complexities of capital gains tax on second property uk 2026, our team stands ready to provide the intellectual rigour your portfolio deserves. We invite you to consult with Davis & Co LLP for your property tax planning to ensure your next disposal is handled with the precision it requires.

Optimising Your Property Disposal for a New Fiscal Era

The 2026 tax landscape requires a shift from reactive reporting to proactive strategy. As we’ve explored, the reduced £3,000 allowance and the mandatory 60-day window leave little room for administrative oversight. Success now depends on the meticulous identification of allowable expenditure and the strategic timing of your disposal to align with your broader income tax position. Managing capital gains tax on second property uk 2026 is no longer a simple year-end task; it’s a sophisticated exercise in compliance and portfolio preservation.

At Davis & Co LLP, we’ve served as trusted advisors to high-net-worth individuals and property investors since 1901. Our chartered certified accountants specialise in property accounting and international tax, providing the bespoke, partner-led service required for complex tax matters. We invite you to secure your property disposal strategy with Davis & Co LLP. By partnering with us, you gain the clarity and confidence to move forward, knowing your interests are managed with the highest degree of professional gravitas. Your portfolio’s future is secure when built on a foundation of expert insight and steady guidance.

Frequently Asked Questions

Do I pay Capital Gains Tax if I inherit a second property and sell it immediately?

You generally only pay tax on the increase in value from the date of death to the date of sale. If you sell the property immediately at its probate value, there is typically no gain to tax. However, if the market value rises during the period you hold the asset, you must account for this uplift. It’s vital to obtain a professional valuation at the time of inheritance to establish an accurate ‘cost’ for HMRC purposes.

Can I offset the cost of a new kitchen against my Capital Gains Tax bill in 2026?

You can deduct the cost of a new kitchen only if it represents a capital improvement rather than a revenue repair. Replacing damaged units with a similar standard is considered a repair and isn’t deductible for CGT. Conversely, upgrading a basic kitchen to a premium finish or expanding the layout adds measurable value to the asset. You must keep all invoices and contracts to substantiate these claims during a disposal involving capital gains tax on second property uk 2026.

What is the 60-day rule for reporting property sales to HMRC?

The 60-day rule requires you to report and pay an estimated ‘tax on account’ within 60 days of the sale’s completion. This is a mandatory requirement for UK residential property disposals where tax is due. You’ll need a digital UK Property Account to submit the return and make the payment. This process is distinct from your annual Self Assessment, which serves as a final reconciliation of your tax position at the end of the year.

Is there any way to avoid Capital Gains Tax on a second home legally?

Legally reducing or eliminating your bill involves utilizing Private Residence Relief, offsetting capital losses, or transferring ownership to a spouse. If you lived in the property as your main home at any point, you may qualify for partial relief for those periods of occupation. Offsetting losses from other assets, such as shares or commercial units, can also lower the taxable gain. These strategies require careful documentation to ensure they meet HMRC’s strict eligibility criteria.

How does the 2026 Annual Exempt Amount affect joint property owners?

Joint owners each receive a personal £3,000 Annual Exempt Amount for the 2026/27 tax year. This means a couple owning a property together can shield £6,000 of the total profit from taxation. It’s a significant consideration when managing capital gains tax on second property uk 2026, as it effectively doubles the tax-free threshold. We recommend ensuring that ownership percentages are correctly registered and documented well in advance of any planned disposal.

What happens if I miss the 60-day deadline for my property disposal report?

Missing the deadline triggers an automatic £100 late filing penalty from HMRC. If the delay extends beyond three months, additional daily penalties or a percentage of the tax due may be charged. Interest also accrues on any unpaid tax from the 61st day after completion. Prompt action is essential to mitigate these costs, as HMRC’s systems are increasingly automated in identifying late property reports and issuing associated fines.

Do I need to report a property sale if I have made a loss?

You aren’t required to submit a 60-day report if the sale results in a capital loss rather than a profit. However, it’s often strategically beneficial to report the loss through your annual Self Assessment return. Doing so allows you to carry the loss forward to offset against future gains, potentially reducing your tax burden in later years. Precise record-keeping of acquisition costs and disposal fees remains vital even when no profit is realized.

Can I use my ISA or pension contributions to reduce my CGT liability?

While you cannot pay property CGT directly from these accounts, pension contributions can lower your overall taxable income. By increasing your pension contributions, you may effectively pull your total income back into the basic rate band of £37,700. This can reduce the applicable CGT rate on your property sale from 24% to 18%. ISAs provide tax-free growth for other assets but don’t offer a direct mechanism to offset residential property gains.