Is your current share option plan a genuine incentive for your key talent, or is it a ticking tax liability waiting for a due diligence audit? For high-growth businesses, the recent expansion of the 2026 rules means more companies than ever can access these benefits, yet the complexity of maintaining compliance has never been higher. Seeking expert enterprise management incentives scheme advice is no longer just about meeting HMRC criteria; it’s about ensuring your most valuable assets feel truly invested in the firm’s long-term trajectory.

We understand that the fear of a valuation dispute or the risk of “dry tax” liabilities can make even the most ambitious founders hesitant. You’ve worked hard to build a culture of excellence. You deserve a reward structure that reflects that without creating unnecessary administrative friction. This guide will show you how to manage the 2026 eligibility changes, including the increased £120 million gross asset limit and the 500-employee threshold. We’ll provide a clear roadmap for implementation, from securing HMRC valuation to aligning your options with a future exit, ensuring your team remains motivated and your business remains audit-ready.

Key Takeaways

- Learn how to leverage EMI as a sophisticated instrument for securing high-calibre leadership within the competitive 2026 talent market.

- Gain clarity on the expanded 2026 eligibility thresholds, including the £120 million gross asset limit, to ensure your business is positioned for expert enterprise management incentives scheme advice.

- Understand the technical nuances between Actual Market Value and Unrestricted Market Value to mitigate the risk of HMRC valuation disputes.

- Master the design of precise performance conditions and exercise triggers that align individual rewards with your firm’s long-term commercial milestones.

- Explore how a compliant EMI structure integrates with international tax planning to facilitate a frictionless due diligence process during a future corporate exit.

The Strategic Value of Enterprise Management Incentives in 2026

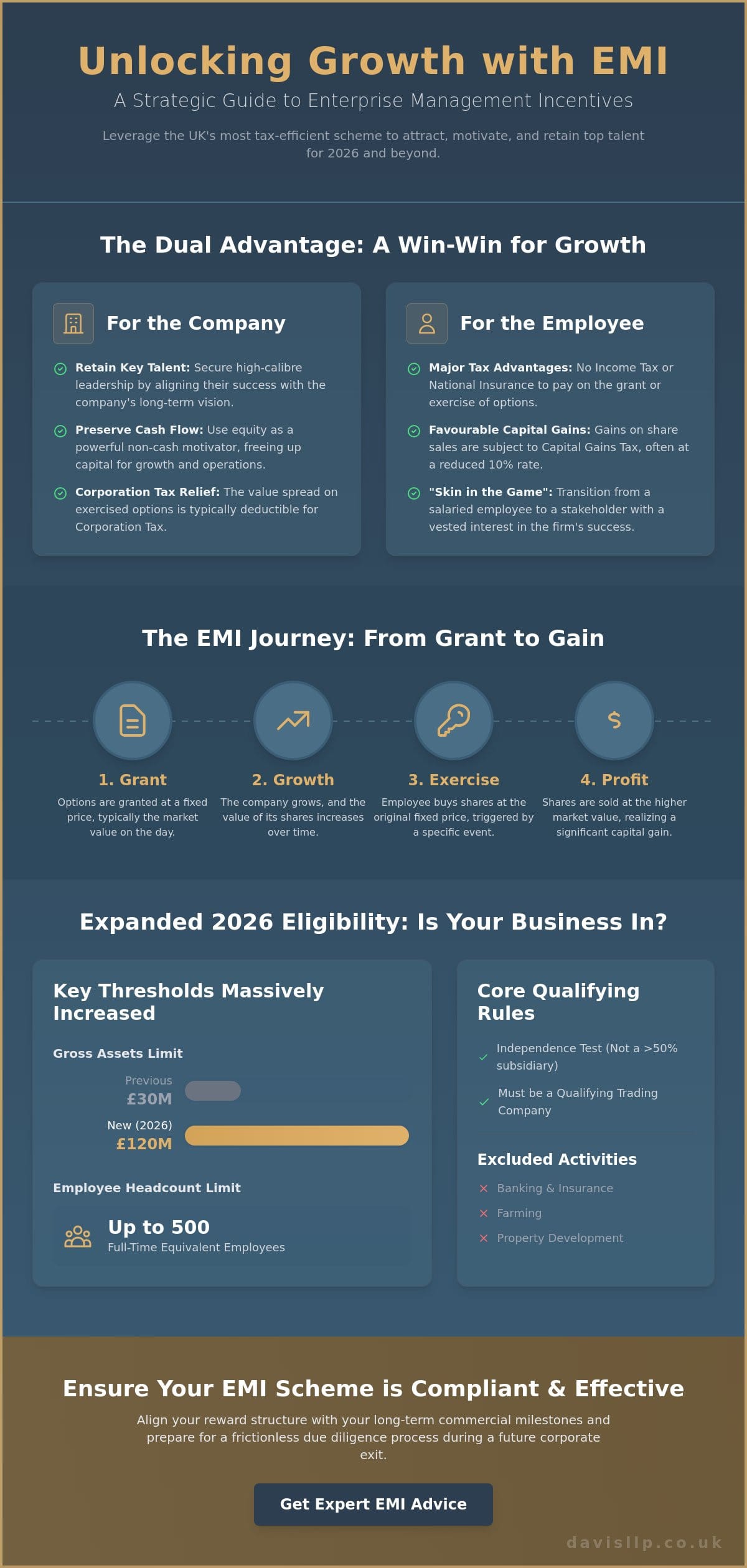

Enterprise Management Incentives (EMI) represent the most tax-efficient mechanism available to UK businesses for rewarding and retaining high-calibre personnel. While the underlying concept is a specialized form of Employee Stock Option, the specific legislative framework surrounding EMI makes it uniquely potent for high-growth enterprises. In 2026, with the UK maintaining its position as the third-largest global destination for venture capital, the ability to offer meaningful equity is no longer optional; it’s a strategic necessity for those looking to scale.

We find that the most impactful enterprise management incentives scheme advice centres on the alignment of interests. For companies competing within the UK’s ecosystem of over 11,000 high-growth startups, matching the high base salaries of established corporations isn’t always feasible or desirable. EMI allows you to preserve vital cash flow by using equity as a non-cash motivator that carries significant upside potential. This shift in compensation structure moves an employee’s mindset from that of a salaried worker to a stakeholder with genuine “skin in the game,” ensuring their personal success is inextricably linked to the firm’s valuation.

How EMI Options Function in Practice

The process begins with the “grant,” where an employee is given the right to acquire shares at a later date. The “exercise” occurs when the employee actually buys those shares, usually triggered by a specific event like a company sale or the passage of time. The cornerstone of the scheme’s value is the fixed exercise price, which is typically set at the market value of the shares on the day of the grant. As the company grows, the gap between this fixed price and the eventual exit value creates the employee’s profit. This creates a powerful psychological anchor, as key management can see the tangible results of their contributions reflected in the growing value of their options.

Primary Tax Advantages for Companies and Employees

The tax benefits of an EMI scheme are twofold, providing relief for both the individual and the organization. For the employee, there’s generally no Income Tax or National Insurance to pay when the options are granted or exercised, provided the exercise price matches the market value at the time of the grant. When the shares are eventually sold, the gains are subject to Capital Gains Tax, often at a reduced rate of 10% through Business Asset Disposal Relief. From the company’s perspective, the “spread”—the difference between the market value at exercise and the price the employee pays—is usually deductible for Corporation Tax purposes. Securing expert enterprise management incentives scheme advice ensures these calculations are handled with the precision required to satisfy HMRC’s rigorous standards.

Navigating the 2026 EMI Eligibility Criteria and New Limits

The expansion of the EMI framework in April 2026 has fundamentally altered the landscape for medium-sized enterprises. Previously, many firms found themselves outgrowing the scheme just as they reached a critical scale. Now, the gross assets limit has been raised to £120 million, a substantial increase from the previous £30 million threshold. Similarly, the employee headcount cap has moved to 500 full-time equivalents. These changes ensure that the scheme remains a viable tool for businesses well into their mid-market journey.

When seeking enterprise management incentives scheme advice, it’s vital to address the “independence” test early in the planning process. HMRC requires that the company granting the options is not a 51% subsidiary of another entity. If your business is part of a group, the qualifying rules apply to the group in its entirety. Additionally, the company must be a qualifying trading company. This means it must exist for the purpose of carrying on a trade with a view to profit, rather than purely for investment or non-commercial activities. For a granular look at the statutory requirements, the GOV.UK EMI Scheme Rules provide the baseline for compliance.

Understanding Excluded Activities in a Modern Context

Certain sectors remain excluded from the EMI regime to prevent tax advantages from being used in areas HMRC deems “low risk” for growth or already well-supported. These include banking, farming, and property development. However, we often see tech-enabled platforms operating within these sectors that may still qualify if their primary activity is the provision of technology rather than the excluded trade itself. This distinction is subtle but critical for fintech or proptech firms aiming to attract senior talent. We recommend a thorough review of your revenue streams to confirm that your core operations don’t fall foul of these definitions.

Employee Participation Requirements

Eligibility isn’t limited to the company; the individual participants must also meet strict criteria. An employee must work at least 25 hours per week or 75% of their total working time for the company. Individuals holding a “material interest”—defined as more than 30% of the ordinary share capital—are ineligible. Selecting the right participants is a strategic exercise in business growth acceleration, as the goal is to reward those who directly influence the firm’s valuation. By focusing on key management and high-potential contributors, you ensure the equity pool is utilized to its maximum effect.

Valuation Strategies and HMRC Compliance

Securing a robust valuation is the most technically demanding phase of implementing an EMI scheme. HMRC requires two distinct figures: the Actual Market Value (AMV) and the Unrestricted Market Value (UMV). The AMV represents the value of the shares taking into account any restrictions, such as the inability to sell them freely, and is used to set the exercise price. Conversely, the UMV assumes no such restrictions exist. This higher figure is critical because it determines how much of an individual’s £250,000 three-year limit is being utilized. Failing to distinguish between these values accurately can lead to unexpected tax charges for employees upon exercise, undermining the scheme’s primary purpose.

Scale-ups often face unique hurdles depending on their growth stage. Early-stage firms might struggle to justify a low valuation shortly after a high-priced funding round, while later-stage companies must navigate the complexities of a more crowded cap table. Once a valuation is agreed upon with HMRC, a 90-day window opens. All options must be granted within this timeframe. If this window is missed, the agreement expires, and the process must begin anew. This strict timeline requires synchronized efforts between your board, your advisors, and your administrative team to ensure no participant is left behind. For a deeper look at the strategic nuances of these rules, this Complete Guide to EMI offers an excellent foundation for understanding the broader regulatory context.

The HMRC Valuation Agreement Process

The formal route to agreement involves submitting a VAL231 form to HMRC’s Shares and Assets Valuation (SAV) team. This submission isn’t merely a disclosure; it’s a negotiation. We often advocate for significant discounts on the AMV, sometimes ranging from 60% to 90%, based on minority interest holdings and a lack of marketability. Precise enterprise management incentives scheme advice is essential here to ensure the proposed discount is defensible. Maintaining a meticulous record of this agreed valuation is also vital for future due diligence, as any potential acquirer will scrutinize these records to ensure no latent tax liabilities exist.

Ongoing Compliance and Disqualifying Events

An EMI scheme isn’t a static arrangement; it requires active monitoring to remain compliant. Certain “disqualifying events” can jeopardize the tax-favoured status of the options. These include the company being acquired, a change in the nature of the trade, or an employee no longer meeting the working time requirements. If such an event occurs, employees usually have only 90 days to exercise their options to retain the tax advantages. Additionally, companies must fulfill annual reporting obligations to HMRC. We ensure that these filings are integrated into your broader audit and assurance processes, providing peace of mind that the scheme remains in good standing year after year.

Implementation: Designing Performance Conditions and Exercise Triggers

The transition from theoretical tax planning to a live incentive structure requires a methodical approach. Implementation isn’t merely an administrative exercise; it’s the moment your commercial objectives are codified into legally binding agreements. High-quality enterprise management incentives scheme advice ensures that the triggers for share acquisition align perfectly with your long-term vision for the firm. We focus on creating a structure that rewards genuine contribution while protecting the company’s capital integrity.

The process typically follows five critical stages:

- Stage 1: Defining the commercial objectives. You must decide whether the options are “exit-only,” meaning they can only be exercised upon a company sale, or based on time or performance milestones.

- Stage 2: Drafting the EMI Option Agreement. This document must contain precise legal definitions regarding vesting schedules and exercise rights.

- Stage 3: Securing the HMRC valuation. As discussed previously, this agreement must be in place before the formal grant to ensure tax certainty.

- Stage 4: Formal board approval. The directors must pass a resolution to grant the options and issue the formal certificates to participants.

- Stage 5: Online notification. You must notify HMRC of the grant within the 92-day statutory limit to maintain the scheme’s tax-advantaged status.

Exit-Only vs. Milestone-Based Schemes

For founders with a clear five to seven-year horizon for a trade sale, “exit-only” schemes are often the most straightforward choice. They prevent the cap table from becoming cluttered with minority shareholders before a liquidity event. However, if your goal is business growth acceleration, milestone-based triggers can be more effective. These link equity rewards to specific KPIs, such as recurring revenue targets or product development phases. It’s also essential to define “good leaver” and “bad leaver” provisions clearly. This ensures that if a key individual departs under amicable circumstances, they may retain some benefit, whereas those who leave under a cloud forfeit their unvested options.

Communicating the Scheme to Employees

A scheme’s value is only realized if your team understands it. We recommend providing an “Option Summary” alongside the legal agreement. This document should explain the potential financial upside in plain English without making definitive guarantees. Transparency regarding tax obligations is equally important. While EMI is highly tax-efficient, employees must understand that Capital Gains Tax will apply upon the eventual sale of their shares. Clear communication fosters trust and ensures the scheme acts as a genuine retention tool rather than a source of future confusion. If you require bespoke documentation or a review of your current vesting schedules, our team provides comprehensive company secretarial services to manage the administrative burden of your share schemes.

Integrated Advice: Aligning EMI with Long-Term Growth

EMI schemes shouldn’t exist in a vacuum. To be truly effective, they must be integrated into a comprehensive financial strategy that considers both the company’s trajectory and the founders’ personal goals. For businesses with global ambitions, this integration often involves international tax planning to ensure that UK-based equity incentives complement the tax structures of foreign branches or parent entities. This holistic view prevents the fragmentation of corporate interests and ensures that your incentive structure remains robust across different jurisdictions.

A significant portion of the value in securing professional enterprise management incentives scheme advice lies in preparing for an eventual exit. During a corporate sale, the buyer’s legal and financial teams will scrutinize every aspect of your share scheme. Clean, well-documented EMI records are vital to avoid price chips or indemnity claims during due diligence. We ensure that every grant, valuation, and notification is recorded with the precision required to withstand such intense examination. This level of preparation is a hallmark of expert tax advice in the UK, where the focus remains on the long-term protection of shareholder value.

Many growth-focused firms rely on small business accountants who possess a deep understanding of equity incentives. It’s not enough to manage the monthly payroll; your advisors must understand how equity distribution impacts your balance sheet and your talent retention. By aligning these different financial workstreams, you create a stable environment where growth is both sustainable and tax-efficient. We believe that the most successful schemes are those where the accountant and the founder work in a composed partnership to drive the business forward.

The Davis & Co LLP Approach to EMI

Our methodology moves beyond mere compliance. We provide the strategic foresight necessary to ensure that equity is distributed in a way that truly drives performance. We work closely with founders to define meaningful triggers that reflect the actual commercial milestones of the business. Throughout this collaborative process, we maintain the highest levels of discretion and precision, particularly when managing sensitive shareholding data. We position ourselves as a strategic partner, projecting a persona that is both traditional in its values and contemporary in its application.

Next Steps for Your Business

If you’re considering implementing a scheme, the first step is a feasibility study to confirm your company’s eligibility under the 2026 rules. We then review your existing share structures to identify any potential conflicts that could hinder a smooth implementation. Finally, we recommend securing a professional consultation to begin the formal valuation process with HMRC. Taking these steps early ensures that your enterprise management incentives scheme advice is tailored to your specific needs, providing a clear roadmap for rewarding the people who make your success possible.

Transforming Your Key Talent into Strategic Stakeholders

The 2026 updates to the EMI framework provide a unique opportunity for high-growth firms to solidify their competitive advantage. By navigating the increased £120 million asset and 500-employee thresholds with precision, you can transform your share option plan into a powerful engine for retention and performance. Success hinges on a clear roadmap that balances HMRC compliance with your specific commercial milestones. Securing professional enterprise management incentives scheme advice ensures your structure remains robust during future due diligence and aligns perfectly with your exit strategy.

At Davis & Co LLP, we’ve been helping businesses thrive as Chartered Certified Accountants since 1901. Our team specializes in growth acceleration and international tax planning, providing comprehensive support that spans from the initial valuation negotiation to the final HMRC notification. When you secure strategic EMI scheme advice from Davis & Co LLP, you gain a partner dedicated to the long-term integrity of your corporate structure. We’re ready to help you turn your key talent into dedicated stakeholders who are truly invested in your firm’s success.

Frequently Asked Questions

What are the asset and employee limits for EMI in 2026?

To qualify for the scheme, your company’s gross assets must not exceed £120 million and you must have fewer than 500 full-time equivalent employees. These limits were increased from £30 million and 250 employees respectively in April 2026. This expansion allows larger, high-growth firms to access the scheme’s significant tax benefits while remaining compliant with HMRC’s updated thresholds.

Can a company in a ‘non-qualifying’ sector still use EMI?

Generally, companies primarily engaged in excluded activities such as banking, farming, or property development are ineligible. However, if your firm provides technology or specialized services to these sectors without carrying out the excluded trade itself, you might still qualify. Seeking professional enterprise management incentives scheme advice is vital here to analyze your revenue streams and confirm your trading status with HMRC.

How long does it take to get an EMI valuation agreed with HMRC?

It typically takes between two and four weeks to receive a formal response from HMRC’s Shares and Assets Valuation team. This timeframe can vary depending on the complexity of your company’s capital structure and the detail provided in your VAL231 submission. Once the valuation is agreed, you have a 90-day window to formally grant the options to your selected employees.

What happens to EMI options if an employee leaves the company?

The outcome depends on the “good leaver” and “bad leaver” provisions defined in your specific EMI Option Agreement. Usually, leaving the company is a disqualifying event, which triggers a 90-day window for the employee to exercise their vested options. If they don’t exercise within this period, they lose the associated tax advantages, and the options may lapse according to your scheme’s rules.

Is there a limit on the value of shares an individual can hold under EMI?

An individual can hold unexercised EMI options with a total value of up to £250,000 at the time of the grant. This limit is calculated using the Unrestricted Market Value (UMV) and applies over a three-year rolling period. Furthermore, the total value of all unexercised EMI options granted by a single company cannot exceed £6 million under the 2026 regulations.

Does the company need to be a ‘small’ company to qualify for EMI?

No, the term “small” is relative; the 2026 rules are designed to support substantial mid-market enterprises. With the headcount limit now at 500 employees and gross assets capped at £120 million, the scheme is accessible to many established firms that have moved beyond the startup phase. It’s a strategic tool for any qualifying business aiming for rapid growth and talent retention.

What is a ‘disqualifying event’ for an EMI scheme?

A disqualifying event is a change that ends the tax-favoured status of the options, such as the company being acquired or a participant no longer meeting the working time requirement. When such an event occurs, the employee must exercise their options within 90 days to retain the tax benefits. If exercise happens after this window, the uplift in value from the date of the event is subject to Income Tax.

Can EMI options be granted over existing shares or only new issues?

EMI options can be granted over either newly issued shares or existing shares held by a shareholder or an Employee Benefit Trust. Most companies prefer to use new issues as it doesn’t require an immediate cash outlay to purchase shares from current holders. We help you manage the resulting dilution on your cap table to ensure the interests of founders and investors remain balanced.