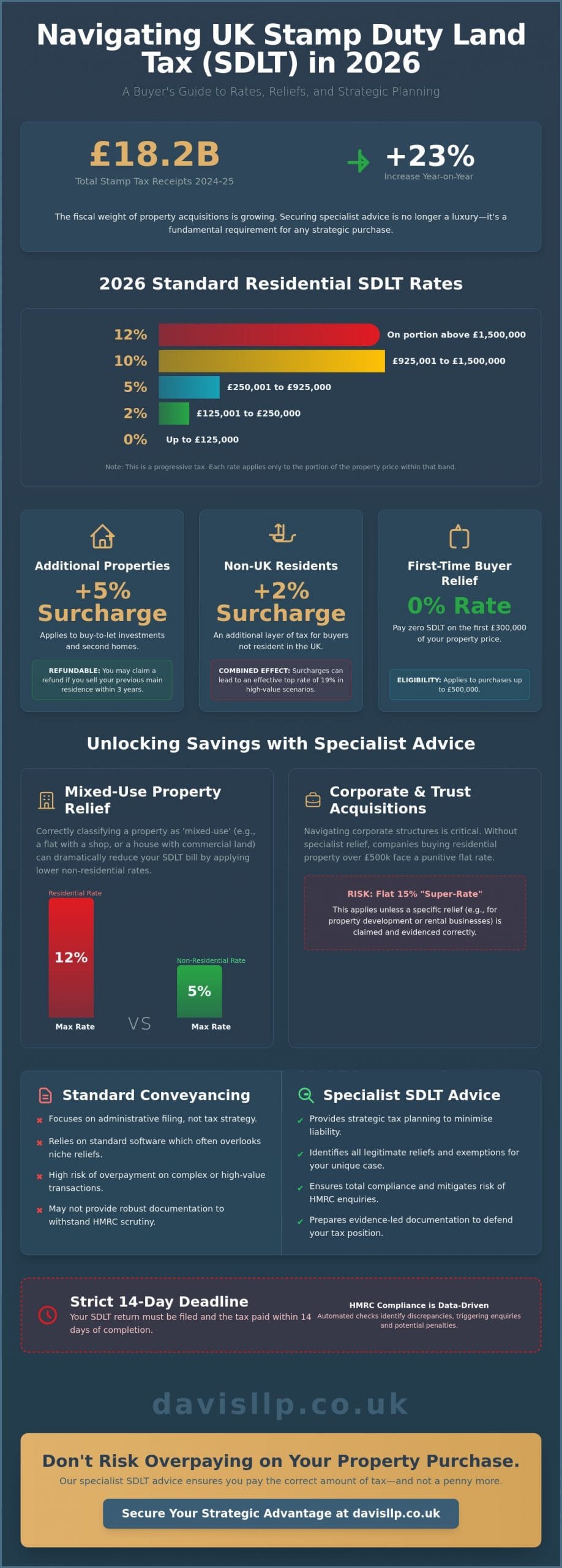

Total stamp tax receipts reached £18.205 billion in the 2024-2025 financial year, a 23% increase that underscores the growing fiscal weight of property acquisitions. For many, the transition to the rate structure that took effect in April 2025 has turned what was once a simple calculation into a significant financial risk. Securing specialist stamp duty land tax advice for buyers is no longer a luxury for the cautious; it’s a fundamental requirement for any strategic property acquisition in 2026.

You likely feel that the current thresholds, where the 0% band ends at just £125,000 for standard purchases, leave very little room for error. It’s natural to worry about overpaying due to a misclassification or facing a stressful HMRC enquiry years after you’ve settled into a new home. We’ll show you how to address these complexities with precision, ensuring you claim every applicable relief while maintaining total compliance. This guide provides a detailed breakdown of the 2026 residential rates, explores the nuances of first-time buyer and non-resident surcharges, and outlines a structured approach to strategic tax planning.

Key Takeaways

- Identify the 2026 threshold adjustments and learn why standard automated software often overlooks legitimate niche reliefs.

- Understand the critical distinction between administrative conveyancing and the specialist stamp duty land tax advice for buyers required for complex acquisitions.

- Gain insights into HMRC’s data-driven compliance checks and the specific statutory windows for amending returns or securing overpayment refunds.

- Discover how bespoke property accounting and personal tax planning can protect your interests in high-value or international transactions.

- Learn how to maintain robust, evidence-led documentation to satisfy rigorous HMRC standards and prevent the risk of discovery assessments.

Navigating the SDLT Landscape in 2026

Stamp Duty Land Tax (SDLT) is a self-assessed transfer tax payable to HMRC on the acquisition of land and property in England and Northern Ireland. While many view it as a mere administrative checkbox, the History of Stamp Duty Land Tax reveals its evolution into a sophisticated fiscal instrument with significant financial implications. Following the reversal of temporary measures on 1 April 2025, the 2026 landscape requires a more rigorous approach to calculation. Understanding the distinction between residential, non-residential, and mixed-use land classifications is vital, as the “effective rate” of tax often differs significantly from the headline bands. Professional stamp duty land tax advice for buyers ensures these nuances are addressed before the 14-day filing deadline.

Current 2026 Residential Rates and Thresholds

The current thresholds reflect a return to traditional levels following the sunsetting of previous incentives. For standard residential purchases, the 0% band now applies only to the first £125,000 of the purchase price. This is a marked shift from the £250,000 threshold that supported the market in early 2025. Portions between £125,001 and £250,000 attract a 2% rate, while the portion from £250,001 to £925,000 is taxed at 5%. High-value acquisitions face steeper progression, with rates reaching 10% and 12% for portions exceeding £925,000 and £1.5 million respectively. First-time buyers still benefit from relief on properties up to £500,000, though the 0% threshold for this group has reduced to £300,000.

The Surcharge Regime: Additional Properties and Non-UK Residents

The surcharge regime adds layers of complexity for investors and international clients. Acquisitions of additional residential properties, such as buy-to-let investments or holiday homes, trigger a 5% surcharge on top of standard rates. Additionally, non-UK residents are subject to a 2% surcharge, which can lead to an effective top rate of 19% in specific high-value scenarios. We often assist clients in navigating the strategic timing of property disposals. If you replace your main residence within three years of paying the higher rate, you may be eligible for a refund of the 5% surcharge. This coordination between your property accounting and personal tax planning is essential to prevent unnecessary capital erosion during the acquisition process.

Maximising Legitimate Reliefs and Exemptions

Identifying applicable reliefs is often the difference between a viable acquisition and a prohibitive one. Many buyers inadvertently overpay because standard reporting processes fail to account for the specific characteristics of a property or the buyer’s unique circumstances. In 2026, where residential portions above £1.5 million attract a 12% charge, the stakes for precision are high. Seeking professional expert tax advice in the UK allows you to look beyond the basic headline rates and explore legitimate avenues for mitigation.

Compliance remains the cornerstone of any tax strategy. HMRC’s Official government SDLT guidance provides the baseline, but applying it to complex scenarios requires a robust, evidence-based approach. Whether you’re navigating the complexities of charitable exemptions or probate transfers, your claim must be defensible. Providing a clear trail of documentation is essential to satisfy HMRC’s increasingly sophisticated automated checks. If you’re unsure about your eligibility for specific exemptions, our personal tax services can provide the necessary clarity before you commit to a purchase.

Mixed-Use Properties and Non-Residential Rates

Classifying a property as “mixed-use” can result in substantial savings, as the top rate for non-residential land is only 5%. This classification extends beyond traditional shop-and-flat arrangements. It often involves a nuanced analysis of “gardens and grounds,” particularly for rural estates where land might be used for commercial grazing or third-party access. We’ve seen numerous disputes where HMRC challenges these classifications; therefore, having detailed property accounting records and professional surveys is vital to secure the lower rate. Securing tailored stamp duty land tax advice for buyers before the transaction completes is the most effective way to manage these risks.

Corporate and Trust-Based Acquisitions

Corporate buyers face a distinct set of challenges, including a 15% “super-rate” for residential properties valued over £500,000. This rate applies unless specific reliefs, such as those for property development or rental businesses, are correctly claimed. For global investors, international tax planning is indispensable to ensure that the interaction between UK SDLT and overseas tax regimes doesn’t create an unnecessary fiscal burden. The structure of the holding entity must be carefully considered to avoid unintended surcharges that could erode the long-term yield of your property portfolio.

Why Specialist Tax Advice Surpasses Standard Conveyancing

A common misconception in property acquisition is that the legal transfer of title and the assessment of tax liability are the same process. They aren’t. While a solicitor is essential for ensuring a secure legal title, their primary focus remains the conveyancing process. The fiscal implications of the purchase, however, require a different analytical lens. Professional stamp duty land tax advice for buyers focuses on the nuanced interpretation of tax law rather than the administrative filing of a return. This distinction is critical because the responsibility for the accuracy of an SDLT return rests with the buyer, not the person who files it.

Many law firms rely on automated software to calculate SDLT. These systems are designed for high-volume, standard transactions and often lack the sophistication to identify “grey areas” or niche reliefs. When a transaction involves complex ownership structures, mixed-use land, or multiple dwellings, software often defaults to the highest residential rate. This conservative approach protects the law firm’s professional indemnity but can lead to significant overpayments for the buyer. We position the chartered accountant as the strategic lead in these transactions, ensuring that tax analysis precedes the legal completion.

The Limitation of Conveyancing Software

Standard transactions are becoming increasingly rare as property usage and ownership structures evolve. Automated calculators struggle with properties that don’t fit a narrow definition of “residential.” For instance, dwellings that are uninhabitable at the point of completion or estates with significant non-residential elements require a manual expert review. A second opinion from a tax specialist often reveals that what was initially flagged as a standard residential purchase actually qualifies for a lower rate. This manual intervention is the only way to ensure precision in an environment where HMRC’s scrutiny is intensifying.

Collaborative Partnership in Property Acquisition

For commercial and corporate buyers, a property acquisition is rarely an isolated event. It’s a component of a larger fiscal strategy. We bridge the technical gap by integrating our SDLT analysis with our small business accountant services. This collaborative approach ensures that the SDLT return aligns with your broader corporate tax position and long-term cash flow management. A professional tax report also carries significant weight with lenders. It demonstrates a level of due diligence that reinforces the stability of your investment and provides peace of mind that your compliance is beyond reproach.

Managing Compliance and HMRC Scrutiny

HMRC’s oversight has evolved into a data-driven operation. By cross-referencing Land Registry records with individual tax returns, the Revenue can identify discrepancies with surgical precision. This shift makes “aggressive” tax avoidance schemes particularly dangerous, as they often rely on technical loopholes that lack commercial substance. For those seeking professional stamp duty land tax advice for buyers, the priority must be on defensive compliance and the creation of a robust audit trail. A well-documented file, prepared at the point of acquisition, is your most effective shield against future challenges.

The statutory windows for managing your return are strict. You generally have 12 months from the filing date to amend a return or claim a refund for overpaid tax. However, discovery assessments allow HMRC to look back much further if they suspect a loss of tax was brought about carelessly or deliberately. Maintaining records for at least six years isn’t just a recommendation; it’s a fundamental part of a sound property accounting strategy. If you’re concerned about your current standing, our personal tax services can provide a comprehensive review of your historical filings.

Preventing and Navigating HMRC Enquiries

Certain triggers frequently lead to an HMRC tax warning or a formal “Check of a Tax Return” letter. These include claiming multiple dwellings relief on properties that don’t meet the strict criteria or applying non-residential rates to land that HMRC considers part of a garden. Responding to these enquiries requires a measured, technical approach. Professional representation ensures that the dialogue remains focused on the relevant legislation and prevents the escalation of penalties. We act as your strategic partner, managing the correspondence to reach a resolution that protects your financial interests.

The SDLT Reclaim Process

Reclaiming overpaid tax is a structured process with specific criteria. The most common scenario involves the “replacement of main residence” rule. If you buy a new home before selling your previous one, you’ll pay the higher rate surcharge upfront. You then have a three-year window to sell the original property and claim a refund of that surcharge. This reclaim must be submitted within 12 months of the sale. Precision in these timelines is vital. We provide the expert stamp duty land tax advice for buyers needed to navigate these windows, ensuring that your capital is returned promptly and without unnecessary administrative friction.

Bespoke Property Tax Solutions with Davis & Co LLP

Our approach to providing stamp duty land tax advice for buyers is rooted in the belief that every acquisition is a significant milestone in a client’s fiscal history. We don’t view SDLT as an isolated cost but as a critical component of your broader property accounting and personal tax framework. By aligning our analysis with your long-term objectives, we ensure that your transaction is structured to support both immediate cash flow management and future growth. This holistic perspective is what distinguishes a strategic partnership from a mere service provision.

For clients with global interests, we bridge the complex gap between international tax planning and the specificities of UK property law. Our history of professional gravitas and discretion makes us the preferred choice for high-value and complex transactions that require more than a standard assessment. We provide the intellectual rigour necessary to navigate the 2026 regulatory environment, offering a sense of security that comes from deep-seated expertise rather than marketing hyperbole. The result is a seamless integration of tax efficiency and regulatory compliance.

A Strategic Partner for Property Investors

We offer tailored advice for specialized sectors, including dental professionals who require a deep understanding of how property acquisitions interact with their unique business structures. Managing the tax lifecycle of a property involves more than just the initial purchase. It requires a considered view of the transition from acquisition to eventual disposal. We stay at the forefront of the 2026 regulatory updates, ensuring that your portfolio remains compliant and efficient as the fiscal environment evolves. Our commitment is to provide a steady, dependable constant in a volatile market.

Initiating Your Strategic Tax Review

To initiate your strategic tax review, please prepare your draft heads of terms and any proposed ownership structure documents. Our property tax team will then conduct a thorough analysis to produce a definitive SDLT liability report. Precision is our priority. This measured process allows you to proceed with your transaction with understated confidence. Obtaining professional stamp duty land tax advice for buyers that accounts for every detail of your specific transaction is the first step toward long-term fiscal stability. We’re here to act as your strategic partner, providing the expert oversight necessary to secure your financial interests.

Securing Your Property Interests with Precision

Success in the 2026 property market depends on a disciplined approach to fiscal obligations. By moving beyond basic calculations and focusing on the nuanced application of reliefs, you ensure that your acquisition remains a sound investment. We emphasize that tax precision is not merely about compliance; it’s about the strategic preservation of your capital. Maintaining a clear, evidence-based audit trail allows you to proceed with the confidence that your interests are fully protected against future scrutiny.

As Chartered Certified Accountants since 1901, we offer a level of reliability that only a century of practice can provide. We are specialists in international and property tax planning, with a proven track record in managing complex HMRC compliance. When you seek stamp duty land tax advice for buyers, you deserve a partner who understands the high-calibre requirements of your portfolio. Consult Davis & Co LLP for bespoke Stamp Duty Land Tax advice to bring professional gravitas to your next transaction. We’re here to ensure your property journey is both secure and well-advised.

Frequently Asked Questions

What are the Stamp Duty rates for 2026?

Standard residential rates in 2026 apply progressively: 0% for the first £125,000; 2% on the portion between £125,001 and £250,000; and 5% on the band from £250,001 to £925,000. Higher portions attract 10% up to £1.5 million, with a top rate of 12% for any amount exceeding that threshold. These rates have remained consistent since the threshold changes on 1 April 2025.

Can I claim a Stamp Duty refund if I sell my previous home later?

You’re eligible for a refund of the 5% higher rate surcharge if you sell your previous main residence within 36 months of purchasing your new home. The reclaim must be submitted to HMRC within 12 months of the sale date of the previous property. We often manage these reclaims as part of our property accounting services to ensure timelines are strictly met and capital is recovered efficiently.

Is there a difference between SDLT for individuals and limited companies?

Limited companies are generally subject to the 5% higher rate surcharge on all residential acquisitions, even for their first purchase. Furthermore, a 15% flat rate applies to corporate purchases over £500,000 unless the property is used for a qualifying business purpose, such as property development or a rental business. Professional stamp duty land tax advice for buyers is essential here to identify and claim these specific corporate reliefs.

Do first-time buyers still get Stamp Duty relief in 2026?

First-time buyers benefit from a 0% rate on the first £300,000 of a purchase, provided the total property price doesn’t exceed £500,000. For the portion between £300,001 and £500,000, a 5% rate applies. If the property price exceeds the £500,000 cap, the relief is entirely withdrawn, and the transaction is taxed at standard residential rates instead.

What counts as a “mixed-use” property for SDLT purposes?

A mixed-use property is one that incorporates both residential and non-residential elements, such as a doctor’s surgery with a flat above or a rural estate with land used for commercial purposes. These acquisitions are taxed at non-residential rates, which are capped at 5%. Classifying a property correctly requires a detailed review of the land’s usage to ensure the classification is defensible under HMRC scrutiny.

How long do I have to pay Stamp Duty after completing a purchase?

You must file your return and pay the tax due within 14 days of the effective transaction date, which is typically the date of completion. This is a strict statutory deadline; missing it results in automatic fixed penalties and accruing interest. We recommend preparing your tax analysis well in advance of completion to ensure the filing is both accurate and punctual.

Can I appeal an HMRC decision regarding my Stamp Duty relief claim?

You have the right to appeal an HMRC assessment or decision through a statutory review or by taking the matter to the First-tier Tribunal. It’s vital to present a robust, evidence-led case that addresses the technical points raised by the Revenue. Our team provides the expert stamp duty land tax advice for buyers needed to navigate these disputes and reach a resolution that protects your financial position.

Is Stamp Duty payable on the VAT element of a commercial property purchase?

SDLT is calculated on the total consideration for the property, which includes any VAT charged on the purchase price. In commercial transactions where the seller has opted to tax the property, the 20% VAT adds a significant layer to the taxable base. This interaction can substantially increase your total acquisition cost, making it necessary to factor the VAT element into your initial cash flow management plans.