While the 2024 Autumn Budget increased the Stamp Duty surcharge to 5%, the question for 2026 isn’t whether property investment is dead, but rather how its structure must evolve to remain sustainable. You’ve likely felt the weight of Section 24 and the narrowing margins that come with shifting interest rates. It’s a common concern that the traditional route to securing a buy to let mortgage is no longer the straightforward path to passive income it once was. We recognise that the landscape has shifted from simple asset acquisition to a complex exercise in fiscal strategy.

This guide provides a comprehensive look at how these financial instruments function in the current climate and the critical tax implications you must understand to maintain a profitable portfolio. We’ll explore the framework for choosing between personal and limited company ownership, ensuring your decisions are grounded in commercial reality. By the end of this analysis, you’ll have the clarity required to organise your investments with confidence and precision.

Key Takeaways

- Understand the fundamental mechanics of a buy to let mortgage to ensure your investment strategy aligns with both rental yield requirements and long-term capital growth.

- Discern the critical differences in affordability assessments, specifically how lenders utilise Interest Coverage Ratios (ICR) to stress-test your application.

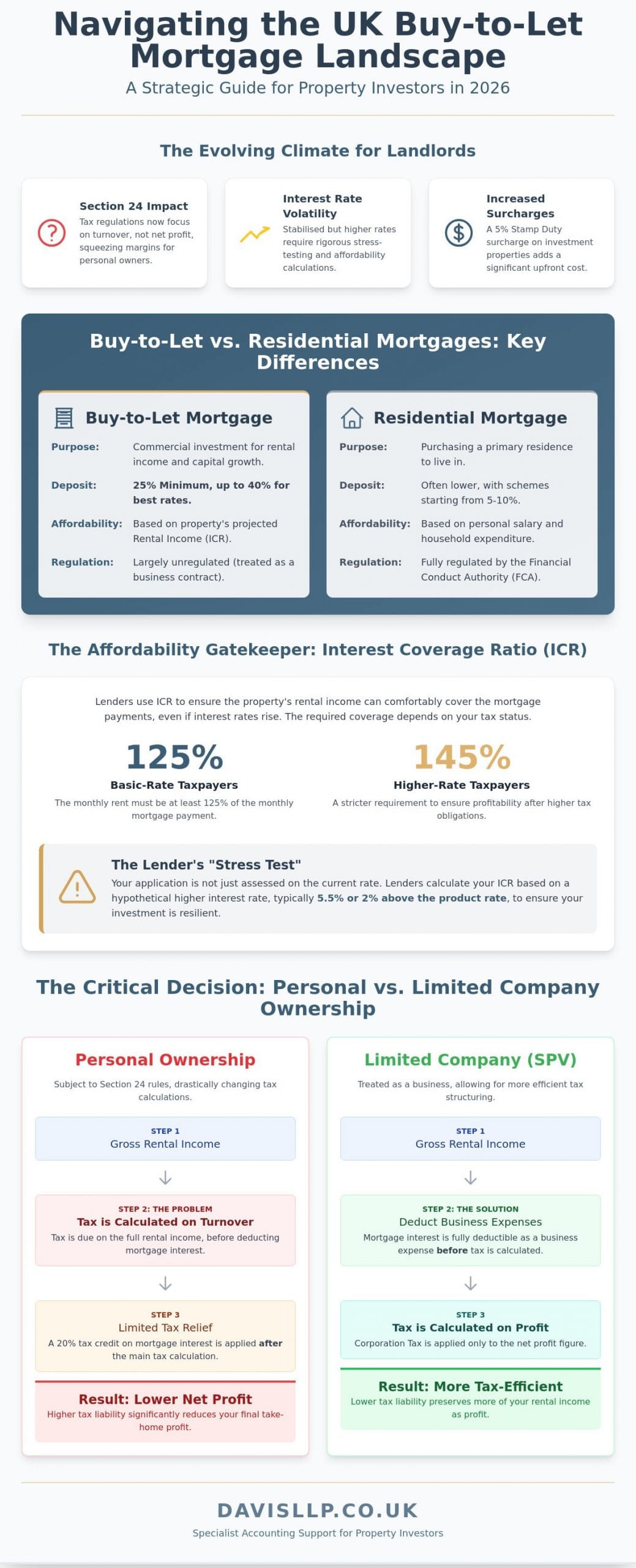

- Prepare for the fiscal realities of Section 24 by understanding how current regulations tax turnover rather than net profit.

- Compare the commercial implications of personal ownership against Special Purpose Vehicle (SPV) structures to identify the most tax-efficient path for your 2026 portfolio.

- Learn how bespoke accounting support can provide the strategic foresight necessary to preserve capital and facilitate future property acquisitions.

Understanding the Fundamentals of Buy-to-Let Mortgages in 2026

A buy to let mortgage is a bespoke financial instrument specifically structured for individuals or corporate entities purchasing property as a commercial venture rather than a primary residence. Unlike standard residential loans, these products are assessed primarily on the property’s ability to generate monthly income. We view these arrangements as strategic partnerships between the lender and the investor, where the focus shifts from personal affordability to the commercial viability of the asset.

The core intent behind securing a buy to let mortgage in 2026 is the pursuit of a dual-return strategy: consistent rental yield and long-term capital growth. While the market underwent significant shifts following the interest rate volatility of 2023 and 2024, the current climate is one of stabilised maturity. Industry data from the Hamptons Lettings Index indicates that UK rental growth is maintaining a steady 3.8% annual trajectory in 2026. This provides a predictable environment for investors who prioritise wealth preservation and steady cash flow over speculative gains.

We must distinguish between the two primary regulatory categories of these loans. Most investment-led transactions are “unregulated” because they’re treated as business contracts. However, “consumer” buy-to-let mortgages, which often apply when a borrower lets a property previously lived in by themselves or a family member, fall under the protective remit of the Financial Conduct Authority (FCA). Identifying which category your transaction falls into is a critical first step in our advisory process.

Who is a Buy-to-Let Mortgage For?

Lenders typically require a minimum personal income of £25,000 per annum, though some specialist providers for experienced portfolio investors may waive this. Most institutions set a maximum age limit of 85 at the end of the mortgage term. Lenders view these loans as higher risk than residential borrowing because they’re susceptible to “void periods” where no tenant is present. Consequently, a minimum deposit of 25% is usually the baseline for securing competitive rates in the 2026 market.

The Legal and Regulatory Landscape

The Prudential Regulation Authority (PRA) enforces rigorous stress-testing to ensure landlords can withstand potential rate rises. In 2026, lenders often require an Interest Cover Ratio (ICR) of 145% for higher-rate taxpayers, calculated at a stressed interest rate of 5.5% or more. Compliance also involves adhering to the Renters’ Rights Act 2024 and meeting strict Energy Performance Certificate (EPC) standards. We provide the intellectual rigour necessary to navigate these statutory obligations, ensuring your portfolio remains both compliant and commercially sound.

Key Differences: How Buy-to-Let Mortgages Work Compared to Residential Loans

A buy to let mortgage functions on a fundamentally different risk profile than a standard residential loan. While a homeowner’s application prioritises personal salary and household expenditure, the commercial viability of the property takes precedence in a professional investment assessment. Lenders view these as business transactions. Consequently, the entry requirements are more stringent. You will typically need a minimum deposit of 25%, though the most competitive interest rates often require 40% equity to mitigate lender risk against market fluctuations.

Affordability and the Interest Coverage Ratio (ICR)

Lenders evaluate affordability through the Interest Coverage Ratio (ICR). This metric determines if the projected rental income can comfortably service the debt while accounting for maintenance, tax, and periods of vacancy. For basic-rate taxpayers, lenders generally expect a 125% cover. However, since the 2017 tax reforms, higher-rate taxpayers usually face a more rigorous 145% requirement. This higher threshold ensures the landlord remains profitable after paying tax on the gross income.

Lenders don’t just look at the current interest rate; they apply a “stress test” to your application. This often involves calculating affordability at a hypothetical rate of 5.5% or 2% above the product rate. If the property’s rent cannot meet the ICR at this elevated level, the loan amount will be capped. To improve your ICR and secure the necessary funding, you might consider:

- Increasing the initial capital contribution to reduce the loan-to-value (LTV) ratio.

- Opting for a five-year fixed-rate product, as some lenders apply more lenient stress tests to longer-term fixes.

- Purchasing through a limited company structure, which may allow for a 125% ICR regardless of your personal tax bracket.

Interest-Only vs. Repayment Mortgages

The vast majority of professional landlords choose interest-only payment structures. This strategy prioritises monthly cash flow, as you only pay the interest charges and don’t reduce the original loan balance. It’s a pragmatic approach for those looking to build a portfolio, as the surplus income can be diverted toward the deposit for a subsequent acquisition. It also provides a cleaner set of accounts for tax purposes.

However, an interest-only buy to let mortgage carries the inherent risk that the capital must be repaid in full at the end of the term. Most investors plan to sell the property to settle the debt, though this relies on the property’s value increasing or remaining stable over twenty-five years. Repayment mortgages are less common but suit those who wish to own the asset outright for retirement income. We frequently advise clients on how to align these financing choices with their wider commercial and private wealth objectives to ensure the chosen structure remains robust across a long-term horizon.

The Tax Reality: Interest Relief and the Section 24 Impact

The legislative shift introduced between April 2017 and April 2020 fundamentally restructured the fiscal obligations of private landlords. Under Section 24 of the Finance (No. 2) Act 2015, individual investors can no longer deduct mortgage interest or other finance costs from their rental income before calculating their tax liability. You’re now taxed on the gross turnover of your property portfolio. While a 20% tax credit is applied to your finance costs, this mechanism often fails to offset the increased tax burden for those in higher brackets. This transition means that for many, the buy to let mortgage is no longer the straightforward tax-efficient vehicle it once was.

Calculating Your True Tax Liability

The impact of Section 24 is most visible when rental turnover pushes a landlord into a higher tax bracket. Consider a landlord earning £45,000 from a salary and £20,000 in rent, with £10,000 in mortgage interest. Previously, the taxable profit was £10,000. Now, the full £20,000 is added to the salary, creating a total income of £65,000. This moves £14,730 of income into the 40% bracket for the 2024/25 tax year, as the higher-rate threshold sits at £50,270. The 20% tax credit doesn’t fully compensate for this jump, creating a “hidden” tax hike. We recommend meticulous bookkeeping to track all allowable expenses, such as letting agent fees, insurance, and utility bills, to mitigate this artificial inflation of taxable income.

Common Misconceptions About BTL Deductions

Distinguishing between revenue expenditure and capital improvement is vital for statutory compliance. Repairs, such as fixing a leaking roof or repainting between tenancies, are deductible from rental income. However, adding an extension or installing a significantly upgraded kitchen is a capital improvement. These costs aren’t deductible from annual income; instead, they offset Capital Gains Tax upon the eventual sale of the property. The 10% Wear and Tear Allowance was abolished on 6 April 2016, replaced by the Replacement of Domestic Items Relief. This allows you to claim for the actual cost of replacing furnishings like sofas or appliances, provided they’re for the sole use of tenants. Securing professional tax advice before finalising a buy to let mortgage deed is a pragmatic step to protect your long-term commercial objectives. The same principle applies across all property-related commercial ventures — just as specialist restaurant accountants protect hospitality margins through bespoke sector knowledge, property investors benefit most from advisors who understand the specific fiscal landscape of their asset class. This need for sector-specific expertise extends to other high-earning professionals too; for instance, dentist accountants near me searches often reveal how professionals in regulated industries require the same depth of bespoke financial guidance to avoid costly miscalculations in their tax liabilities.

Strategic Structuring: Personal Ownership vs. Limited Company BTLs

The movement toward Special Purpose Vehicles (SPVs) has fundamentally altered how investors approach the market. According to data from Companies House, over 50,000 new property companies were incorporated in 2023, a trend that has solidified as we move through 2026. This shift isn’t merely a trend; it’s a calculated response to the evolving tax environment. Individual landlords face the full weight of personal income tax rates, which reach 45% for additional-rate payers. In contrast, corporate structures benefit from Corporation Tax rates, currently set at 19% for profits below £50,000 and 25% for those exceeding £250,000.

The Benefits of Incorporating Your Property Portfolio

Choosing a corporate structure often hinges on the ability to deduct 100% of mortgage interest payments from rental income before tax is calculated. For many higher-rate taxpayers, this remains the primary driver for seeking a buy to let mortgage through an SPV. We’ve seen how this mechanism protects margins that would otherwise be eroded by the Section 24 restrictions, which limit personal tax relief to a 20% credit. Beyond immediate tax efficiency, companies offer a robust framework for succession planning. Shares can be transferred to family members over time, which often proves a more pragmatic approach to managing future inheritance tax liabilities. Reinvesting profits within the company also avoids the immediate personal tax hit, allowing for faster portfolio growth.

The Drawbacks and Costs of Limited Companies

The corporate route isn’t a universal solution. Lenders often view limited companies as higher risk, which results in higher interest rates and more substantial arrangement fees compared to personal products. You’ll also need to account for the administrative burden. This includes the cost of annual accounts, corporate tax filings, and legal secretarial duties. There is also the “double taxation” challenge. Once the company pays its tax, you’ll likely face personal tax on any dividends or salary you draw. With the dividend allowance remaining at £500, extracting cash requires a bespoke strategy to remain cost-effective. Additionally, both individuals and companies must pay the 5% Stamp Duty Land Tax surcharge on additional properties, a rate increased in the October 2024 budget.

Understanding which structure aligns with your long-term goals is essential for sustainable growth. Our team provides the bespoke legal and strategic advice required to navigate these complex decisions.

Optimising Your Property Portfolio with Specialist Accounting Support

Managing a property portfolio in 2026 demands more than basic bookkeeping. The transition from holding a single asset to overseeing a complex collection of interests requires a shift from passive oversight to active commercial strategy. Davis & Co LLP provides the technical rigour and discreet advisory services necessary to ensure your investments remain both profitable and compliant within a tightening regulatory framework. We act as a strategic partner, helping you look beyond the immediate rental yield to the long-term health of your entire estate.

Bespoke Solutions for Modern Landlords

Generic, off-the-shelf accounting software often lacks the nuance required for sophisticated property structures. With the full implementation of Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA) in April 2026 for landlords with qualifying income over £50,000, precision is no longer optional. We focus on real-time cash flow management and growth acceleration. Our team ensures HMRC compliance through robust audit and assurance processes, protecting you from the risks of unexpected enquiries. Securing a competitive buy to let mortgage is merely the starting point; the real value lies in how that debt is structured against your total tax liability.

Strategic tax planning serves as the foundation for capital preservation. We assist clients in navigating the complexities of interest relief restrictions and Capital Gains Tax obligations. For non-resident landlords, we manage the specific requirements of the Non-Resident Landlord Scheme (NRLS), ensuring that international tax treaties are applied correctly to avoid double taxation. Our approach integrates your property holdings into a wider wealth management strategy, considering:

- The use of Limited Company structures or Special Purpose Vehicles (SPVs) to optimise corporation tax rates.

- Inheritance Tax planning to facilitate the smooth transfer of property assets to future generations.

- Strategic re-leveraging of existing equity to fund a new buy to let mortgage for portfolio expansion.

- Detailed analysis of allowable expenses to ensure no legitimate deduction is overlooked.

Taking the Next Step in Your Investment Journey

Success in the UK property market is rarely the result of chance. It’s the product of calculated decisions and professional partnership. We invite you to book a consultation for a comprehensive property tax review. This session allows us to examine your current holdings and identify untapped efficiencies that could improve your net position. A partnership with a Chartered Certified Accountant provides the stability required to navigate volatile markets with confidence. Contact Davis & Co LLP today to secure your financial future and refine your investment trajectory through quiet excellence and proven expertise.

Securing Your Property Portfolio’s Future in 2026

The landscape for property investment continues to evolve, particularly as the long-standing implications of Section 24 of the Finance Act 2015 define the boundaries of profitability. Success in the current market requires a precise approach to structuring, whether you’re navigating the complexities of personal ownership or transitioning to a limited company model. Selecting the right buy to let mortgage is no longer simply a matter of finding the lowest interest rate. It’s about how that debt interacts with your broader tax liabilities and commercial objectives.

At Davis LLP, we provide the steady guidance needed to manage these variables. As Chartered Certified Accountants with over 120 years of expertise, we specialise in property accounting and international tax planning. We don’t offer generic templates; we deliver bespoke advice tailored to your unique circumstances. Our role is to ensure your portfolio remains resilient against regulatory shifts while maintaining the clarity you need to make informed decisions. If you’re evaluating your advisory options, understanding how to find a chartered accountant who specialises in property and tax strategy is an essential first step toward securing the right professional partnership.

Discuss your property tax strategy with our specialist accountants and secure the professional oversight your investments deserve.

With the right structural foundations in place, your property business is well-positioned to thrive for years to come.

Frequently Asked Questions

Can I get a buy-to-let mortgage as a first-time buyer?

Yes, you can secure a buy to let mortgage as a first-time buyer, though your choice of lenders is significantly reduced. Data indicates that approximately 80% of UK lenders require applicants to own their primary residence before approving an investment loan. You’ll likely face more stringent criteria, such as a minimum age requirement of 25. Lenders also look for a minimum personal income of £25,000 to mitigate the perceived risk.

How much deposit do I really need for a buy-to-let property in 2026?

You typically require a minimum deposit of 25% for a buy-to-let property in 2026. While some niche lenders offer products at 20% loan-to-value, these carry much higher interest rates that can erode your profit margins. A 40% deposit remains the industry standard for accessing the most competitive rates. This larger capital buffer protects your investment against potential house price fluctuations or periods of vacancy.

Is it better to buy a rental property in my own name or a limited company?

The choice between personal ownership and a limited company depends on your current tax bracket and future investment goals. Since the full implementation of Section 24 in April 2020, individual landlords can’t deduct mortgage interest from rental income before tax is calculated. Holding property within a limited company allows you to treat interest as a business expense. This structure is often more efficient for higher-rate taxpayers who plan to build a portfolio.

What is the “stress test” and how does it affect my borrowing power?

A stress test is a calculation used by lenders to ensure your rental income covers mortgage costs even if interest rates increase. Most providers require an Interest Coverage Ratio (ICR) of 125% for basic-rate taxpayers or 145% for those in higher tax brackets. They usually test this against a nominal interest rate of 5.5% or 6%. This assessment determines your maximum borrowing capacity based on the property’s monthly rental yield.

How much Stamp Duty will I pay on a buy-to-let property?

You’ll pay a 3% surcharge on top of standard Stamp Duty Land Tax (SDLT) rates when purchasing an additional residential property in England. For a property valued at £300,000, the total SDLT bill currently reaches £11,500. This includes the standard residential portion and the additional property levy. It’s a significant upfront cost that we advise clients to calculate carefully before committing to a purchase.

Can I move into my buy-to-let property if my circumstances change?

You can’t move into your buy-to-let property without first obtaining formal written consent from your mortgage lender. Most buy-to-let agreements are unregulated contracts that strictly prohibit owner-occupation. Moving in without authorisation is a breach of your mortgage conditions and can lead to the loan being called in. You’ll typically need to switch to a regulated residential mortgage, which involves a full assessment of your personal affordability.

What happens to my buy-to-let mortgage when the interest-only term ends?

You must repay the original capital sum in full when the interest-only term of your buy to let mortgage expires. Most investors plan to meet this obligation by selling the property or by refinancing the debt with a new loan. If the property’s value has fallen below the original purchase price, you’ll need to provide the difference from your own funds. We recommend reviewing your exit strategy at least five years before the term ends.

Are buy-to-let mortgage interest payments still tax-deductible?

Mortgage interest payments aren’t fully tax-deductible for individual landlords under current UK tax law. Since 2020, you receive a tax credit instead, which is capped at 20% of your mortgage interest payments. This change often increases the tax liability for higher-rate taxpayers because the credit doesn’t always cover the full tax due on the income. Limited companies are exempt from this specific rule and can still deduct interest as a business expense.