Is the steady growth of your turnover quietly creating a liability that could compromise your firm’s stability? For many UK directors, approaching the £90,000 vat threshold, a figure maintained for the 2024 to 2026 period, feels less like a commercial victory and more like an impending encounter with HMRC’s penalty regime. You’ve likely spent years refining your pricing; the prospect of an overnight 20% increase for your clients is understandably daunting.

We understand the pressure of balancing expansion with the complexities of statutory tax law. This guide provides the strategic framework you need to master the rolling 12-month calculation, a nuanced metric that contributed to a significant volume of late-registration penalties throughout the 2023/24 tax year. We’ll outline a bespoke approach for 2026 that protects your profit margins while ensuring total compliance peace of mind. We’ll examine the precise registration triggers you must monitor, effective turnover tracking methods, and pragmatic ways to transition your business model without sacrificing your hard-earned market position.

Key Takeaways

- Understand the current statutory requirements for the £90,000 vat threshold and how this consumption tax affects your commercial operations.

- Learn the precise methodology for calculating taxable turnover, ensuring your compliance is based accurately on gross income rather than net profit.

- Evaluate the strategic merits of voluntary registration to determine if becoming a VAT-registered entity aligns with your broader commercial objectives.

- Identify the procedural risks associated with late registration and the critical role of the VAT1 form in maintaining a transparent relationship with HMRC.

- Discover how bespoke VAT solutions can provide the clarity and foresight required to manage complex tax obligations with quiet excellence.

The VAT Threshold in 2026: Core Principles and Figures

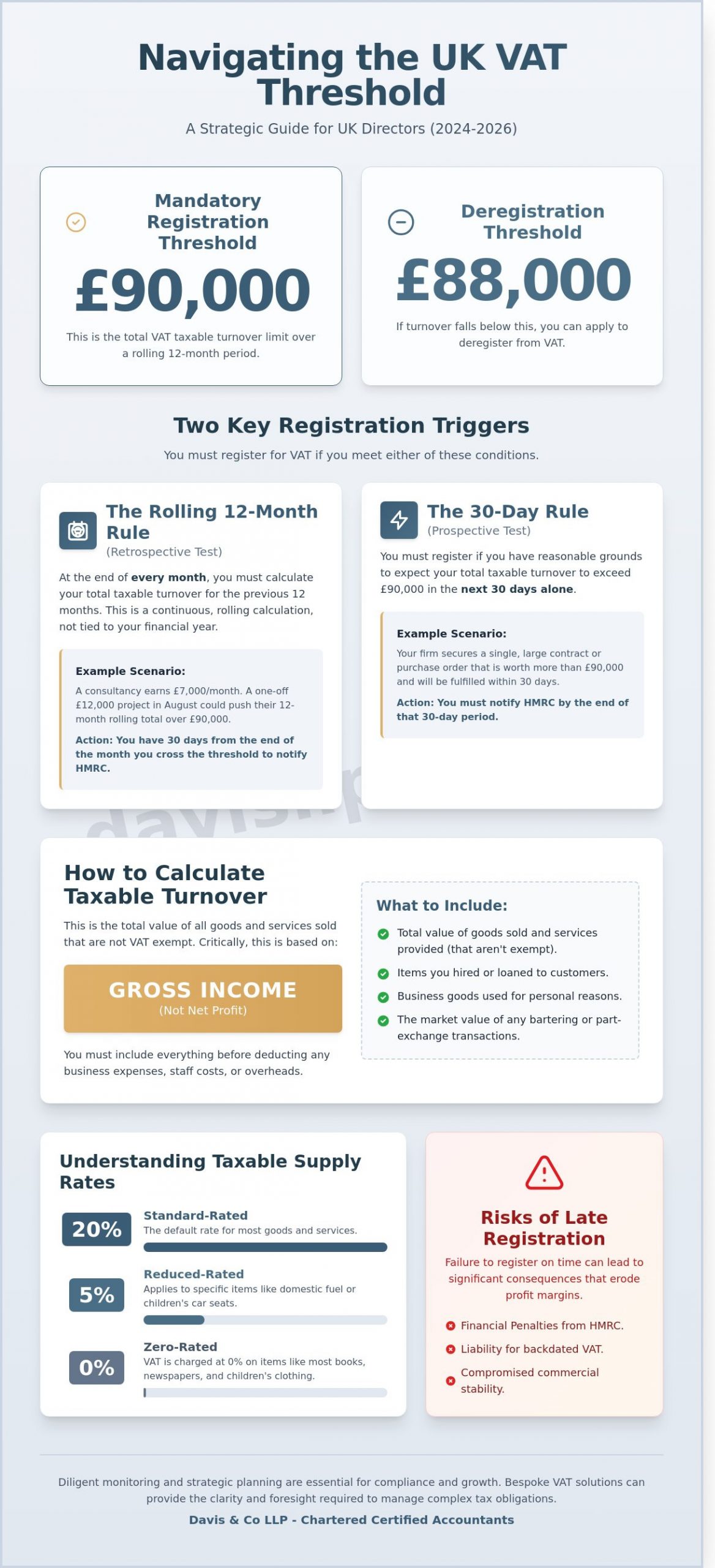

As we advise our commercial clients, maintaining a precise understanding of statutory obligations is fundamental to long-term fiscal stability. The UK Value-Added Tax (VAT) acts as a consumption tax, collected by businesses on behalf of the government. For the 2026 period, the mandatory vat threshold remains fixed at £90,000. This figure represents the specific point of taxable turnover where registration becomes a legal necessity. VAT is essentially a tax on the value added to goods and services at each stage of production and distribution, ensuring the tax burden falls on the final consumer while allowing businesses to recover tax paid on their own inputs.

We also distinguish this registration limit from the deregistration threshold of £88,000. This lower figure allows a small buffer to prevent businesses from constantly oscillating between registered and non-registered status due to minor fluctuations in monthly income. Registration is triggered by two primary mechanisms: the retrospective 12-month test and the prospective 30-day test. Both require diligent monitoring to ensure compliance with HMRC regulations.

The Rolling 12-Month Rule Explained

HMRC applies a retrospective test that often catches directors off guard. It’s a common misconception that the vat threshold aligns with the fixed financial year or the April tax calendar. Instead, you must calculate your cumulative turnover at the end of every single month for the previous 12 months. Monitoring this figure requires a diligent internal accounting process.

Consider a boutique consultancy earning £7,000 monthly. If they secure a £12,000 project in August 2026, their rolling total might suddenly breach the £90,000 limit. You have 30 days from the end of the month in which you crossed the limit to notify the authorities. We recommend a month-end review of your trailing turnover to ensure you don’t inadvertently breach the limit without a strategic plan in place.

Prospective Registration: The 30-Day Rule

The prospective trigger requires a forward-looking assessment of your commercial activity. You’re required to register if you expect your total taxable turnover to exceed £90,000 in the next 30 days alone. This scenario typically arises when a firm secures a substantial one-off contract or a major purchase order from a new client. It’s a strict statutory obligation.

You must inform HMRC by the end of that 30-day period. Failing to act promptly results in backdated tax liabilities and potential financial penalties, which can significantly erode your profit margins. This prospective rule is designed to capture high-growth events immediately. We provide bespoke guidance to ensure your reporting remains accurate and timely during these periods of rapid expansion.

Accurately Calculating Your VAT Taxable Turnover

Determining whether your business has crossed the vat threshold involves more than a cursory glance at your bank balance. Taxable turnover refers to the total value of all goods and services sold that aren’t exempt from VAT. We must emphasize that this figure represents gross income before any business expenses, staff costs, or overheads are deducted. If your business conducts bartering transactions or utilizes business assets for private purposes, the open market value of these items must be integrated into your calculations. Precise record-keeping is a necessity; a single overlooked invoice can lead to accidental non-compliance.

You should regularly consult the official VAT threshold figures to ensure your rolling 12-month total remains within legal bounds, currently set at £90,000 as of 1 April 2024. This calculation isn’t based on your fixed financial year. Instead, it operates on a rolling 12-month basis, meaning you must evaluate your position at the end of every month. HMRC’s 2023 tax gap report highlighted that small errors in turnover reporting contribute to a significant portion of the £32 billion in uncollected tax, making intellectual rigour in your bookkeeping essential for risk mitigation.

Taxable vs. Exempt Supplies

Your turnover calculation depends on the precise classification of your supplies. Most goods and services fall into three taxable categories:

- Standard-rated (20%): The default rate for most commercial activities.

- Reduced-rated (5%): Applied to specific items like domestic fuel or children’s car seats.

- Zero-rated (0%): Includes most books, newspapers, and children’s clothing.

It’s a common misconception that zero-rated sales are excluded from your calculations. While no VAT is charged to the customer, these sales contribute 100% of their value toward your vat threshold limit. Conversely, exempt items, such as specific insurance products or education services, are excluded entirely from this specific calculation. Misidentifying a zero-rated item as an exempt one can lead to an unexpected and costly registration requirement.

Special Considerations for Professional Sectors

Professional practices often face complexities with mixed income streams. For instance, a dental practice might offer exempt healthcare alongside standard-rated cosmetic treatments, requiring a meticulous partial exemption calculation. It’s also vital to distinguish between disbursements, where you pay a third party on a client’s behalf, and recharges, which are part of your own service delivery. Misclassifying a recharge as a disbursement can artificially deflate your reported turnover and invite unwanted scrutiny. Our team provides bespoke advisory services to help you navigate these technical distinctions, ensuring your commercial objectives remain aligned with statutory requirements.

Strategic Analysis: Voluntary vs. Mandatory Registration

Deciding whether to register before hitting the vat threshold requires a cold, commercial assessment of your client base. For many, the transition isn’t a simple administrative hurdle but a fundamental shift in profitability. We often observe the “VAT trap” in the B2C sector, where a business with £89,000 in turnover and a 30% margin faces a sharp decline in net profit the moment they cross the £90,000 limit. If your customers are private individuals, you’ll likely absorb the 20% tax to remain competitive. This results in an immediate 16.6% reduction in your take-home revenue.

The calculation changes for B2B models. Registration signals a level of business maturity. It suggests your turnover exceeds the current £90,000 vat threshold or that you’re positioning for significant growth. It removes the “small business” stigma when you’re pitching for contracts with larger corporate entities. Since these clients can reclaim the VAT themselves, your 20% price increase is cost-neutral to them. We view early registration as a bespoke strategy for firms aiming to establish a professional gravitas early in their lifecycle. Working with a proactive small business accountant can help you model the precise impact of registration on your margins before making this strategic commitment.

The Benefits of Voluntary Registration

You can reclaim VAT on most goods purchased for business use up to four years before your registration date. For services, this window is six months. We find this particularly advantageous for startups with high initial capital expenditure on equipment or IT infrastructure. If your business deals in zero-rated items, such as books or children’s clothing, you’ll likely receive regular repayments from HMRC. This provides a consistent boost to your liquid capital that unregistered competitors cannot access.

Choosing the Right VAT Accounting Scheme

The Flat Rate Scheme allows businesses with a turnover under £150,000 to pay a fixed percentage to HMRC, simplifying your bookkeeping. For example, an IT consultant might pay 14.5%, retaining the difference between that and the 20% charged. Cash Accounting is vital for businesses with turnover up to £1.35 million. It ensures you only pay VAT once the customer has paid your invoice. This prevents the “dry” tax bill where you owe HMRC funds you haven’t yet collected. For those seeking reduced administration, the Annual Accounting Scheme allows for a single return per year.

Compliance and the Risks of Late Registration

Identifying that your turnover has exceeded the vat threshold is merely the first step in a precise statutory process. You must notify HMRC within 30 days of the end of the month in which your taxable turnover went over the £90,000 limit. This notification is conducted through the submission of a VAT1 form. Failure to act within this window triggers an ‘Effective Date of Registration’ that HMRC backdates to the first day of the second month following the breach. We often find that clients are unprepared for the liability this creates; you’re responsible for VAT on all sales made from that date, regardless of whether you’ve collected it from your customers.

The financial implications of a delay are structured under a strict penalty regime. HMRC calculates ‘failure to notify’ penalties based on a percentage of the ‘potential lost revenue’. These charges range from 5% for non-deliberate delays to 100% for cases where the omission is deemed deliberate and concealed. Because you must account for VAT on sales made between the trigger date and the formal registration, the sudden tax burden can erode your profit margins. We assist businesses in calculating these backdated liabilities to prevent unexpected cash flow disruptions.

Applying for a Registration Exception

If a breach of the vat threshold is purely temporary, you may apply for a registration exception. You’ll need to provide robust evidence proving your taxable turnover won’t exceed the £88,000 deregistration limit in the subsequent 12 months. This requires a formal written application to HMRC, typically supported by data such as the termination of a specific contract or the conclusion of a one-off project. We provide bespoke guidance to ensure these applications meet the rigorous evidentiary standards required by the VAT Registration Service.

Ongoing VAT Management and Digital Records

Compliance remains a continuous obligation following your initial registration. Under Making Tax Digital (MTD) regulations mandated for all VAT-registered entities since April 2022, you must maintain functional compatible software. This digital link ensures that your records remain immutable and reduces the risk of transcription errors. Our team highlights the necessity of professional oversight for quarterly returns to maintain accuracy and mitigate the risk of HMRC audits. We offer bespoke VAT advisory services to ensure your commercial objectives align with your statutory obligations.

Bespoke VAT Solutions with Davis & Co LLP

Managing the complexities of the UK tax system requires more than simple bookkeeping; it demands a partnership built on foresight. At Davis & Co LLP, we act as strategic advisors to ensure your transition into the 2026 tax year is seamless. We understand that approaching the vat threshold creates specific pressures on cash flow and pricing structures. Our firm provides the quiet excellence needed to handle these transitions. We integrate VAT planning with your corporation and personal tax liabilities to ensure your total tax exposure remains optimised. By utilising tailored management accounts, we identify potential threshold breaches up to six months before they occur, giving you the time to adjust your commercial strategy.

Our firm treats your financial health as a single, cohesive entity. We don’t view VAT in isolation. Instead, we examine how registration affects your overall profitability and your personal tax position as a director or owner. This holistic method ensures that decisions made today won’t create unforeseen liabilities in other areas of your business. We provide the steady, measured guidance required to maintain stability in a volatile regulatory environment.

Expert VAT Compliance Services

Our approach to VAT registration and quarterly returns is defined by precision. We manage the statutory requirements with a level of rigour that reduces the risk of HMRC enquiries. If a dispute arises, our team handles all communications with the Revenue, drawing on decades of experience in dispute resolution. This professional assurance allows directors to focus on core operations, knowing their compliance is secure. In 2024, our intervention in HMRC audits helped 92% of our clients resolve queries without additional penalties. We offer a reliable buffer between your business and the complexities of tax law.

Strategic Growth and Tax Planning

Scaling a business beyond the current £90,000 vat threshold requires careful financial modelling. We assist clients in evaluating the impact of VAT on their margins before the requirement becomes mandatory. Choosing the right accounting scheme, such as the Flat Rate Scheme or Cash Accounting, can save a mid-sized firm approximately £3,000 to £5,000 annually depending on their sector. We provide the pragmatic advice necessary to select the most tax-efficient path for your specific circumstances. Our goal is to ensure your growth is sustainable and your tax strategy is robust.

Securing Your Business Position for 2026

Managing your position relative to the vat threshold requires a blend of rigorous calculation and long-term foresight. By 2026, the distinction between mandatory and voluntary registration will remain a critical decision point for growing enterprises. Precision in tracking your 12-month rolling turnover ensures you remain compliant with HMRC regulations while avoiding the financial burden of late registration penalties. At Davis & Co LLP, we draw upon over 120 years of heritage as Chartered Certified Accountants to provide the clarity your business deserves. Our team offers specialist expertise in complex sectors including international trade and dental tax; we ensure your strategy is both robust and tax-efficient.

We’re here to transform statutory obligations into a structured path for growth. Whether you’re approaching the limit or planning a voluntary registration to reclaim input tax, a measured approach is essential. Secure your business’s future with bespoke VAT advice from Davis & Co LLP. It’s a privilege to help you navigate these complexities with total peace of mind.

Frequently Asked Questions

Is the VAT threshold based on my profit or my total sales?

Your VAT obligations are determined by your total taxable turnover, not your net profit. This figure represents the total value of all goods and services sold that aren’t exempt from tax. If your rolling 12-month turnover exceeds the £90,000 vat threshold, you must register with HMRC. We advise clients to monitor gross receipts monthly to ensure statutory compliance remains a priority regardless of business overheads or final margins.

What happens if I go over the VAT threshold temporarily for one month?

You can apply for a registration exception if you can prove to HMRC that your breach of the limit is temporary. You’ll need to demonstrate that your taxable turnover won’t exceed the £88,000 deregistration limit in the upcoming 11 months. This request needs to be submitted in writing. If HMRC doesn’t grant the exception, you’re required to register within 30 days of the month you exceeded the limit.

Can I register for VAT even if my turnover is below £90,000?

You’re permitted to register for VAT voluntarily even if your turnover remains below the £90,000 vat threshold. This strategic move allows your business to reclaim VAT on commercial purchases and professional expenses. It’s often beneficial for firms dealing primarily with VAT-registered clients who can recover the tax themselves. We’ve seen businesses improve their perceived market standing by adopting this approach, though it requires rigorous record-keeping under Making Tax Digital rules.

Does the VAT threshold apply to overseas sales or exports?

Exported goods and services are generally zero-rated but still count toward your total taxable turnover. You must include these figures when calculating if you’ve reached the mandatory registration limit. While you won’t charge VAT to overseas customers, the turnover contributes to your statutory requirement to register. Accurate documentation of the place of supply is essential to ensure you’re following the 2023 updated HMRC guidance on international trade.

How do I calculate my turnover if I have multiple separate businesses?

HMRC treats separate entities as a single business for VAT purposes if they share significant financial, economic, and organisational links. If two businesses you control are effectively one operation, their turnovers are combined to determine if they meet the £90,000 limit. This prevents disaggregation, where a business is split to avoid registration. We recommend a formal review of your corporate structure to ensure each entity maintains the three distinct pillars of independence required by law.

What are the penalties if I register for VAT later than I should have?

Penalties for late registration are calculated as a percentage of the VAT due from the date you should’ve registered. These failure to notify charges range from 5% if you’re less than 9 months late to 15% if you exceed 18 months. HMRC also charges interest on any unpaid tax from the effective date of registration. It’s vital to act quickly; voluntary disclosure often results in more lenient treatment than if HMRC discovers the omission during an audit.

Do I need to include zero-rated items in my VAT threshold calculation?

You must include all zero-rated sales in your calculation, though you exclude items that are officially exempt. Common zero-rated goods like children’s clothing or most books contribute to your taxable turnover total. In contrast, exempt services such as insurance or specific financial dealings don’t count toward the threshold. Confusing these two categories is a common error that leads to 20% of late registration cases we manage for new commercial clients.

Is the VAT threshold the same for all types of business structures?

The registration limit remains identical whether you operate as a sole trader, a partnership, or a limited company. HMRC applies the same £90,000 requirement across all legal structures. If you’re a sole trader with two separate trades, you must combine their turnover because the individual, not the business name, is the taxable person. We ensure our clients understand that their legal vehicle doesn’t grant any specific relief regarding these statutory turnover limits.