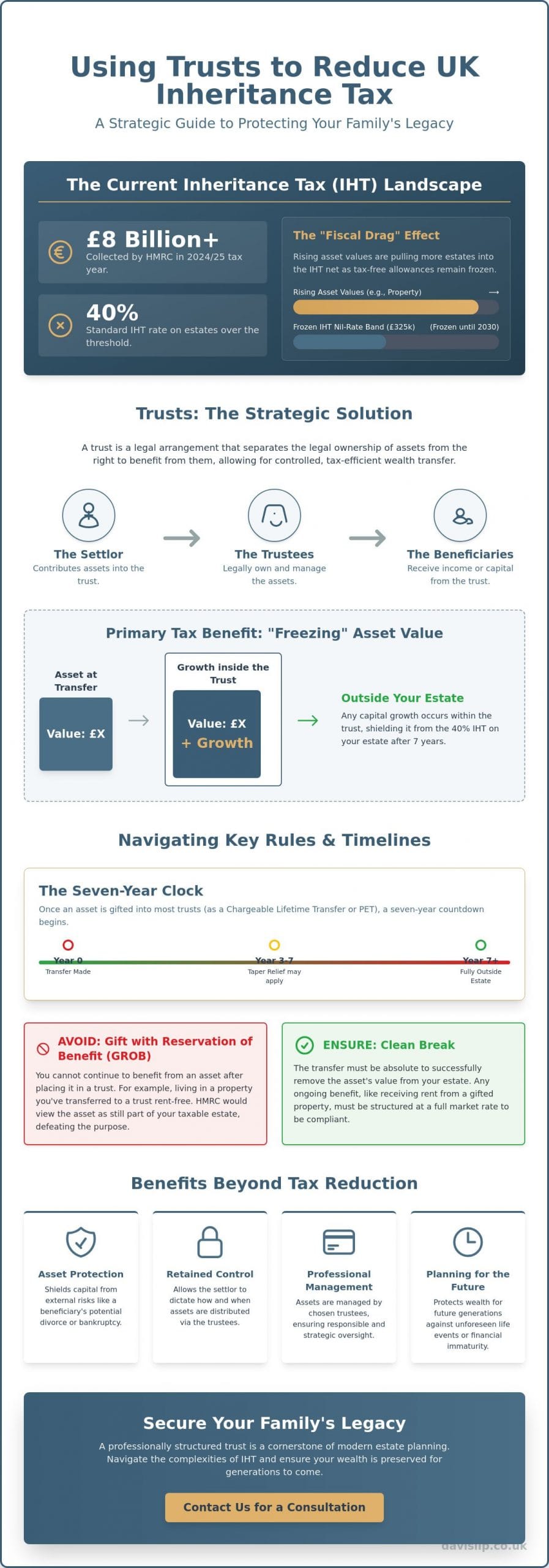

With HMRC collecting over £8 billion in Inheritance Tax during the 2024/25 tax year, more families are exploring the benefits of using trusts to reduce inheritance tax uk as property values rise while allowances remain frozen until 2030. It’s understandable to feel a sense of frustration when assets you’ve worked a lifetime to build face such significant depletion. You want to ensure your legacy reaches your children rather than being absorbed by the state, yet the fear of losing control over your hard-earned capital often makes the decision to gift assets feel premature or risky.

This guide demonstrates how professionally structured trusts provide a sophisticated middle ground, allowing you to mitigate your tax liability while retaining the necessary oversight of your family’s financial future. We will examine the strategic implementation of various trust structures, the impact of the 2026 APR and BPR caps, and how to maintain professional peace of mind in an increasingly complex regulatory environment.

Key Takeaways

- Evaluate why traditional gifting often falls short for high-value estates and how trusts provide a more resilient solution against the 40% IHT threshold.

- Master the technical relationship between settlors, trustees, and beneficiaries when using trusts to reduce inheritance tax uk to ensure professional estate structuring.

- Compare various trust frameworks to determine the optimal balance between immediate asset removal and the level of control you wish to maintain.

- Prepare for long-term fiscal responsibilities by understanding the mechanics of HMRC’s 10-year anniversary charges and capital distribution exit fees.

- Explore how to align your trust strategy with a wider personal tax plan, including the potential advantages of Family Investment Companies.

The Inheritance Tax Landscape in 2026: Why Trusts Matter

The UK tax system currently imposes a 40% charge on the value of estates exceeding the available thresholds. For many families, this represents a significant erosion of wealth that took generations to accumulate. For a foundational UK Inheritance Tax overview, it’s clear how these rates remain a constant pressure on wealth preservation. While traditional gifting remains a common strategy, it often lacks the nuance required for complex estates or those where the donor wishes to maintain some level of influence. This is where using trusts to reduce inheritance tax uk becomes a vital component of a modern estate plan. Unlike an outright gift, a trust allows for a controlled transition of wealth, ensuring that assets are managed according to your specific intentions rather than being subject to the immediate whims of beneficiaries.

The fiscal environment in 2026 is defined by a shift toward tighter restrictions on reliefs. The introduction of the £2.5 million cap on Agricultural Property Relief (APR) and Business Property Relief (BPR) means that even business owners who previously felt secure must now reconsider their positions. Reactive planning is no longer a viable strategy. By categorising transfers as either exempt or Potentially Exempt Transfers (PETs), we can begin to map out a timeline that respects the seven-year rule while utilising trust structures to house assets outside the taxable estate. The strategic advantage of using trusts to reduce inheritance tax uk lies in the ability to remove value from the estate without surrendering the governance of those assets.

The Nil-Rate Band and the “Fiscal Drag” Effect

The standard Nil-Rate Band has remained at £325,000 since 2009. With this threshold frozen until April 2030, a phenomenon known as fiscal drag is pulling more families into the IHT net every year. When you combine this with the Residence Nil-Rate Band of £175,000, a couple may have a £1 million allowance, yet this is quickly eclipsed by rising asset values. Persistent property price growth consistently outpaces these stagnant tax threshold adjustments, making the 40% liability a reality for an increasing percentage of the population. It’s estimated that the number of estates paying IHT will rise to 8% once pensions are brought into the scope of the tax in 2027.

Trusts as a Solution for Asset Protection

Beyond the immediate tax benefits, trusts offer a layer of security that simple gifting cannot match. By moving assets out of your legal ownership while retaining the beneficial intent for your heirs, you create a protective barrier. This structure shields capital from external risks such as a beneficiary’s divorce, potential bankruptcy, or simple financial immaturity. There’s a profound psychological benefit in knowing your legacy is professionally managed and protected from the volatility of life’s unpredictable events. This level of discretion and security ensures that your family’s wealth remains a resource for future generations rather than a source of immediate complication.

The Mechanics of Trusts: How They Reduce Tax Liability

At its core, a trust is a formal legal arrangement that separates the legal ownership of assets from the right to benefit from them. This relationship involves three distinct parties: the settlor, who contributes the assets; the trustees, who manage the fund with professional discretion; and the beneficiaries, who are entitled to receive the income or capital. By using trusts to reduce inheritance tax uk, you effectively move the legal title of your wealth into a protected structure. One of the primary strategic advantages of this shift is the ability to “freeze” the value of an asset for tax purposes. Once an asset is transferred, any subsequent capital growth occurs within the trust, remaining outside your personal estate and therefore beyond the reach of the 40% IHT rate upon your death.

A critical consideration in this process is the Gift with Reservation of Benefit (GROB) rules. To successfully remove an asset from your estate, you cannot continue to enjoy the benefit of that asset after it has been placed in trust. For example, transferring a property into a trust while continuing to reside there without paying a market rent would likely cause HMRC to view the asset as still part of your taxable estate. Precision in these arrangements is paramount to ensure the tax benefits are realised as intended. Our trust tax services provide the technical oversight necessary to navigate these complex boundaries while maintaining your long-term legacy goals.

The Seven-Year Clock: PETs vs. CLT

The tax treatment of a transfer depends heavily on the type of trust selected. Most transfers into discretionary trusts are classified as Chargeable Lifetime Transfers (CLT). If the value of the transfer exceeds your available £325,000 Nil-Rate Band, an immediate lifetime tax charge of 20% applies. This contrasts with Potentially Exempt Transfers (PETs), typically associated with Bare Trusts or direct gifts, which carry no immediate charge but require the settlor to survive for seven years. Taper relief reduces the inheritance tax rate on a sliding scale if the donor survives between three and seven years after making the gift. Understanding this distinction is vital, as a CLT, despite the potential 20% entry charge, can often be more tax-efficient for high-growth assets than waiting for a PET to expire.

Relevant Property Trusts and the IHT Net

Most modern discretionary trusts fall under the “Relevant Property” regime, a specific tax framework designed to capture value within trusts over time. According to the Official HMRC guidance on trusts, these structures are subject to periodic charges every ten years and exit charges when capital is distributed. Bare Trusts are a notable exception to this regime; they’re treated as if the beneficiary owns the assets directly, which simplifies the tax position but offers less control for the settlor. Managing the balance between these immediate charges and the long-term reduction of your estate requires a nuanced approach that considers both your current liquidity and the projected growth of your family’s wealth.

Strategic Comparison: Selecting the Right Trust Structure

Choosing the correct framework is a matter of balancing immediate tax efficiency with the level of influence you wish to retain over the capital. While using trusts to reduce inheritance tax uk is a common objective, the legal structure you select dictates your long-term flexibility and governance. A Bare Trust offers simplicity and the rapid removal of assets from your estate, but it leaves the settlor with no control once the beneficiary reaches adulthood. Conversely, more complex arrangements provide the oversight required to manage substantial wealth across generations, ensuring that distributions align with your specific values and the evolving needs of your heirs. This decision should always be viewed as part of a wider personal tax services strategy to ensure all elements of your financial life work in harmony.

Bare Trusts: Simplicity and Immediate Efficiency

Bare Trusts are fundamentally different from other structures because the assets are treated as belonging directly to the beneficiary for tax purposes. These transfers are classified as Potentially Exempt Transfers (PETs), meaning they fall entirely out of the settlor’s estate after seven years without any immediate entry charges. However, the trustees have no discretion; once a beneficiary reaches age 18 (or 16 in Scotland), they have an absolute right to the capital. This makes them ideal for targeted goals, such as grandparents funding a grandchild’s university education or assisting a first-time buyer with a property deposit, where the risk of the beneficiary mismanaging the funds is considered low.

Discretionary Trusts: The Ultimate Governance Tool

For families with more complex requirements, a Discretionary Trust offers unparalleled flexibility. Here, the trustees have the power to decide when, how, and to whom distributions are made. This is particularly useful for protecting a family business or a specialised professional practice, such as a dental practice, where immediate distribution to heirs might not be appropriate. The primary trade-off is the fiscal cost. using trusts to reduce inheritance tax uk via this route often involves a 20% Chargeable Lifetime Transfer (CLT) tax on any value exceeding the £325,000 Nil-Rate Band. Despite this entry charge, the ability to protect assets from a beneficiary’s potential divorce or creditors often justifies the initial expense.

Flexible Life Interest Trusts

These structures are often the cornerstone of estate planning for married couples. A Life Interest Trust allows a surviving spouse to receive the income from the trust assets for the remainder of their life, while the underlying capital is preserved for the children. This is a strategic tool for those in second marriages, as it prevents “sideways disinheritance” where assets might otherwise pass to a new spouse’s family. When structured as an Immediate Post-Death Interest (IPDI), these trusts benefit from specific IHT treatments that can simplify the transition of wealth while ensuring the security of the surviving partner.

Navigating HMRC Compliance: 10-Year Charges and Exit Fees

Maintaining a trust requires a meticulous approach to regulatory obligations. While using trusts to reduce inheritance tax uk offers clear long-term benefits, the trade-off involves adhering to HMRC’s specific charging regime for “relevant property.” This framework ensures that wealth held within trusts doesn’t escape taxation indefinitely. Professional accounting is indispensable here; submitting accurate Trust Tax Returns and managing HMRC reporting prevents the accumulation of penalties that can otherwise erode the trust’s value. For those with international interests, “excluded property” trusts remain a cornerstone of international tax planning, allowing non-UK assets to remain outside the scope of UK IHT when structured correctly.

Compliance isn’t merely about paying the correct amount; it’s about the timing and accuracy of your disclosures. One of the most common pitfalls for settlors is failing to register their arrangement with the HMRC Trust Registration Service (TRS). This digital record is now a mandatory requirement for nearly all UK express trusts, regardless of whether they have a tax liability. Neglecting this step can lead to significant administrative friction and financial penalties, particularly as HMRC continues to tighten its oversight in 2026.

The 6% Periodic Charge: A Strategic Perspective

A 6% charge every 10 years might initially seem like an additional burden. Yet, from a strategic perspective, paying a maximum of 6% on the value exceeding the £325,000 Nil-Rate Band every decade is often far more efficient than the 40% charge that would otherwise apply upon death. Valuation of trust assets for these anniversary reports must be precise, reflecting the market value on the day of the ten-year milestone. For assets that have been held for less than the full ten-year cycle, HMRC applies a proportionate charge logic based on the number of quarters the property was held within the trust. Similarly, “Exit Charges” are calculated when capital is distributed to beneficiaries between these ten-year anniversaries.

The Trust Registration Service (TRS) Requirements

The TRS has become a mandatory pillar of trust management. Almost all UK trusts must register to comply with anti-money laundering regulations, and the 2026 compliance environment leaves no room for oversight. Deadlines are strict, and the penalties for non-compliance are increasingly robust. Ensuring your structure remains fully compliant requires a deep understanding of evolving legislation. Our Expert Tax Advice in the UK provides the necessary roadmap for navigating these regulatory hurdles with confidence. To secure your legacy against these compliance risks, we invite you to explore our dedicated Trust Tax Services for comprehensive reporting support.

Effective estate management requires looking beyond a single tax. While using trusts to reduce inheritance tax uk is a powerful lever, it must be synchronised with your Income Tax and Capital Gains Tax positions to avoid unintended fiscal consequences. For certain high-net-worth individuals, a Family Investment Company (FIC) might serve as a more flexible alternative or a complementary vehicle, offering diverse ways to manage corporate profits while planning for succession. We view these structures as part of a unified personal tax services strategy, ensuring that every financial decision reinforces your overall objective of wealth preservation.

The transition from a theoretical understanding of estate planning to the implementation of a bespoke trust deed requires a high level of analytical rigour. It’s not simply about tax mitigation; it’s about creating a governance framework that survives for generations. Davis & Co LLP provides the professional gravitas and technical expertise needed to navigate these sensitive matters. Our collaborative approach ensures that your legacy is not only tax-efficient but also aligned with your family’s long-term values and operational realities.

Trusts for Business Owners and Dental Specialists

For those operating within specialised sectors, such as dental professionals or private business owners, the stakes are particularly high. Using trusts to reduce inheritance tax uk allows you to hold shares in a private limited company or a dental practice while maintaining essential governance. It’s vital to ensure that Business Relief (BR) is preserved; poor structuring could inadvertently disqualify assets from this relief, especially given the £2.5 million cap introduced in April 2026. This complexity underscores the importance of finding a Chartered Accountant who possesses a deep understanding of your specific industry requirements. Our role as a dental tax specialist ensures that your professional practice is protected from unnecessary fiscal erosion while remaining fully compliant with HMRC’s latest standards.

The Importance of Regular Professional Review

A trust is not a static instrument. It’s a living arrangement that needs to adapt as your family and the law evolve. Your “expression of wish” letter, which guides trustees in their decision-making, must be updated regularly to reflect your current family dynamics and intentions. We also monitor the shifting legislative horizon, including HMRC’s evolving stance on anti-avoidance measures and the upcoming 2027 changes to pension tax treatment. By developing a long-term partnership with our firm, you ensure that your multi-generational wealth preservation strategy remains robust. Moving from a general plan to a customized solution is the most effective way to secure professional peace of mind. We invite you to explore our trust tax services to begin this transition.

Securing Your Family Legacy for the Next Generation

The strategic implementation of trust structures is no longer reserved for the ultra-wealthy; it’s a necessary step for any family whose assets exceed the frozen nil-rate thresholds. By using trusts to reduce inheritance tax uk, you can effectively freeze the value of your estate and protect your capital from external risks like divorce or bankruptcy. We’ve explored how these vehicles provide the governance required to manage complex assets while ensuring that your heirs are well-provided for according to your specific wishes.

As Chartered Certified Accountants established since 1901, we bring over a century of professional gravitas to every engagement. Our deep-seated expertise in international and trust tax, combined with a specialized focus on dental professional tax planning, ensures that your estate is handled with the highest level of precision and discretion. Consult Davis & Co LLP for bespoke Trust and Inheritance Tax planning to transition from theoretical understanding to a robust, actionable strategy. We look forward to partnering with you to secure your financial future.

Frequently Asked Questions

Can I still access my money if I put it into a trust for IHT purposes?

You generally cannot retain access to the capital or income if you are using trusts to reduce inheritance tax uk effectively. Retaining a benefit would likely trigger the “Gift with Reservation of Benefit” rules, which cause HMRC to treat the assets as if they were still part of your taxable estate. For a trust to be successful in mitigating IHT, the transfer must be a genuine gift where you no longer have a legal or beneficial interest in the property.

How much does it cost to set up and maintain a trust in the UK?

The costs associated with trusts vary significantly based on the complexity of the assets involved and the specific governance requirements of the deed. Professional fees usually cover the initial strategic design, the legal drafting of the trust documents, and the mandatory registration with the HMRC Trust Registration Service. Ongoing maintenance includes the preparation of annual Trust Tax Returns and periodic valuations to ensure compliance with the ten-year charging regime.

Is there a limit to how much I can put into a trust to avoid Inheritance Tax?

There is no legal limit on the total value you can place into a trust, but there are clear fiscal thresholds to consider. Transfers into most modern trusts that exceed your available £325,000 Nil-Rate Band will trigger an immediate Chargeable Lifetime Transfer tax of 20%. While there’s no ceiling, the immediate tax cost must be balanced against the long-term 40% saving on your death estate and the protection of future asset growth.

What happens to the trust if the person who set it up dies within seven years?

If the settlor dies within seven years of making a transfer, the value of that gift is usually brought back into the estate for Inheritance Tax purposes. Taper relief may apply if the settlor survives for at least three years, gradually reducing the tax rate on the gift. This rule underscores why proactive estate planning is more effective than reactive measures taken later in life, as it allows the seven-year clock to expire fully.

Do I still need a Will if I have already set up a trust?

A Will remains a vital component of a professional estate plan even if you have established a trust. Most individuals possess assets that aren’t suitable for trust ownership, such as personal effects, vehicles, or specific bank accounts. A Will acts as a comprehensive safety net, ensuring these residual assets are distributed according to your intentions and allowing you to formally appoint executors and guardians for minor children.

Can a trust be used to reduce tax on international assets held by UK residents?

Trusts are a cornerstone of international tax planning, particularly through the use of “excluded property” structures. If a settlor is non-UK domiciled at the time the trust is created, assets situated outside the UK may be held in a way that keeps them permanently outside the scope of UK Inheritance Tax. This requires precise structuring to navigate the complex interaction between UK domestic law and international tax treaties.

What are the main differences between a Bare Trust and a Discretionary Trust?

The primary distinction involves the level of control and the timing of the beneficiary’s rights. In a Bare Trust, the beneficiary has an absolute right to the assets and income once they reach the age of 18. A Discretionary Trust provides much greater flexibility, as the trustees have the power to decide when and how much each beneficiary receives. This makes the discretionary model a more robust governance tool when using trusts to reduce inheritance tax uk for larger or more complex family estates.