With UK SME loan approval rates hovering at approximately 44%, the difference between a secured facility and a rejection letter often rests on the desk of your accountant rather than the strength of your sales pitch. You’ve likely felt the mounting pressure of high-street criteria or the underlying anxiety that comes with personal guarantee requests. Understanding how to prepare financial statements for a business loan is no longer just a compliance task; it’s a strategic necessity in a market where gross lending has reached £68 billion, yet scrutiny remains at an all-time high.

We’ll show you how to master the forensic requirements and strategic positioning needed to secure high-level funding with favourable terms. This guide provides a clear roadmap for your financial preparation, from aligning with the latest FRS 102 amendments on revenue recognition to managing the tax implications of new debt. We’ll explore why your management accounts now carry more weight than your business plan and how to present a resilient fiscal narrative that satisfies even the most cautious credit committee.

Key Takeaways

- Understand why modern underwriters prioritize forensic quantitative analysis over traditional qualitative pitches to quantify commercial risk.

- Learn how to prepare financial statements for a business loan by focusing on management accounts that demonstrate real-time fiscal discipline.

- Evaluate the tax-deductibility of interest and the implications of the Corporate Interest Restriction to ensure your debt structure remains efficient.

- Discover how to construct a bank-ready funding dossier featuring stress-tested cash flow forecasts that prove repayment capacity.

- Leverage the role of audit and assurance to provide third-party validation, significantly increasing lender confidence in your application.

The 2026 UK Business Lending Landscape: Navigating Bank Appetite

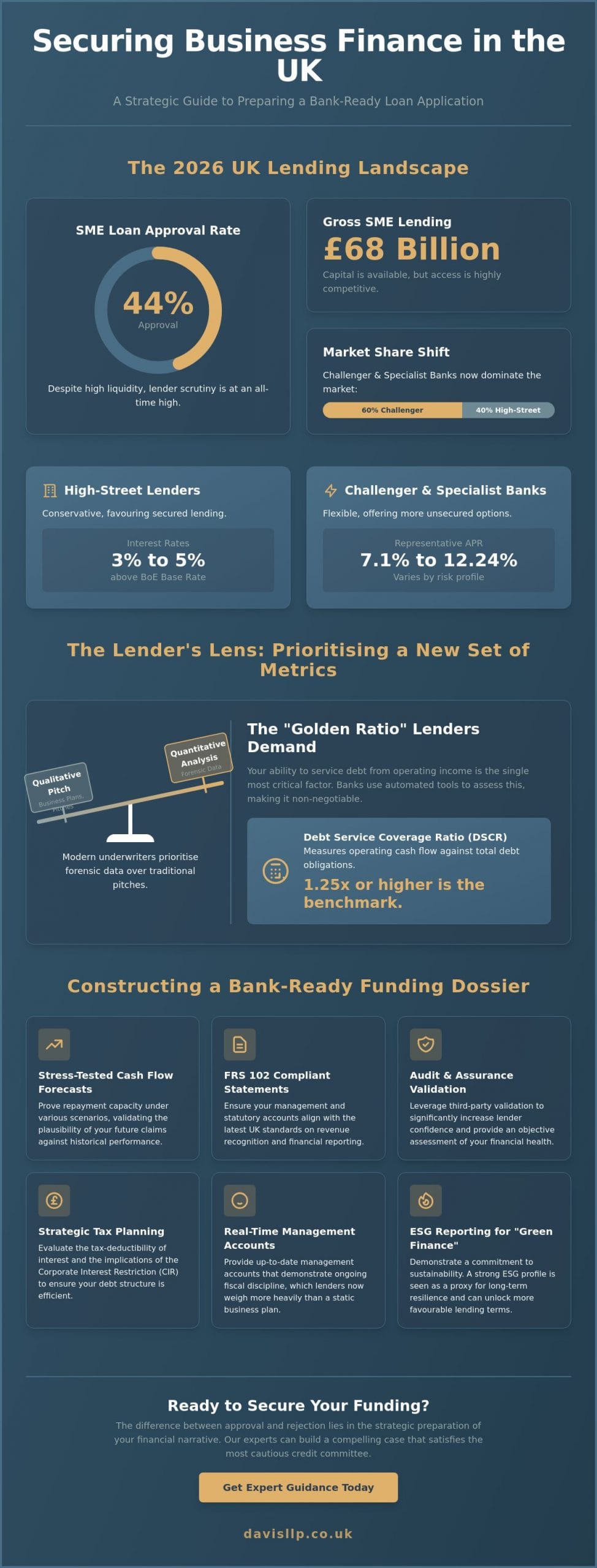

The UK commercial lending environment in 2026 is defined by a paradox of high liquidity and stringent caution. While gross SME lending reached £68 billion last year, the approval rate remains a modest 44%. This suggests that while capital is available, the criteria for access have tightened significantly. High-street institutions have largely retreated to a more conservative posture, often favouring secured lending at 3% to 5% above the Bank of England base rate. Conversely, challenger and specialist banks have captured 60% of the market by offering more flexible, albeit often more expensive, unsecured options with representative APRs between 7.1% and 12.24%.

Understanding how to prepare financial statements for a business loan is the first step in bridging this gap between your capital needs and a lender’s risk appetite. The government’s Open Finance Roadmap, published by the FCA in Spring 2026, has begun to streamline how data is shared, but it’s also increased the transparency requirements for every applicant. You’ll need to demonstrate not just profit, but a sophisticated understanding of your cash flow resilience. The British Business Bank has seen its financial capacity increased to £25.6 billion, largely to support the evolved Growth Guarantee Scheme. This scheme remains a vital lifeline for businesses that might otherwise fall into the credit gap, provided they can build their application around core financial statements that reflect the new FRS 102 standards.

Traditional Term Loans vs. Revolving Credit Facilities

Deciding between a fixed-term loan and a revolving credit facility requires a deep dive into your operational cycle. Term loans remain the preferred choice for significant asset acquisitions, where repayment schedules can be aligned with the asset’s useful life. For businesses managing seasonal cash flow volatility, revolving credit provides a safety net, though it demands rigorous daily management. We’ve found that a blended approach often offers the best balance of long-term stability and short-term flexibility, allowing you to scale without over-leveraging your balance sheet.

The Rise of ESG-Linked Lending Criteria

Sustainability is no longer a peripheral concern for UK lenders. By 2026, banks have integrated environmental, social, and governance (ESG) metrics directly into their risk assessments. Documenting your environmental impact can lead to “Green Finance” opportunities, which often feature lower margins for compliant firms. Lenders view a strong ESG profile as a proxy for long-term operational resilience and forward-thinking management. If you can demonstrate a clear commitment to sustainability within your reporting, you’re likely to secure more favourable terms in a competitive market.

The Lender’s Lens: How Banks Quantify Your Business Risk

Commercial lending has moved beyond the era of the persuasive business pitch. In 2026, bank underwriters rely on automated forensic tools that strip away marketing hyperbole to reveal the clinical reality of your balance sheet. Understanding how to prepare financial statements for a business loan requires adopting this “Lender’s Lens,” where every entry is viewed through the prism of risk mitigation and repayment certainty. Adhering to the UK government guidance on financial statements ensures your baseline compliance, but lenders look for a narrative that extends beyond basic filing requirements. They want to see that your fiscal discipline is a permanent fixture of your operations, not a temporary adjustment for a funding round.

While your future projections are necessary to explain the loan’s purpose, a lender’s decision is anchored in your historical performance. They use the past three years of trading to validate the plausibility of your future claims. If your revenue has grown at 5% annually, a projection of 30% growth following a capital injection will be met with healthy skepticism unless the underlying data supports such a leap. Underwriters also evaluate the management team’s experience, looking for a track record of navigating sector-specific challenges. They’re looking for proof that you’ve managed debt responsibly before and that your business possesses the operational maturity to handle increased leverage.

Critical Financial Ratios Banks Scrutinise

- Debt Service Coverage Ratio (DSCR): This is the “golden ratio” for lenders. It measures your operating cash flow against your total debt obligations. Most UK banks look for a DSCR of 1.25x or higher, indicating you have a 25% buffer after meeting all repayments.

- EBITDA Margins: Banks value consistency over aggressive, unproven spikes in profit. A stable EBITDA margin suggests your business has strong pricing power and effective cost controls.

- Liquidity Ratios: The current ratio, which compares your current assets to current liabilities, demonstrates whether you can weather short-term economic shocks without defaulting on your commitments.

The Importance of Accurate Management Accounts

Statutory accounts are often too historical to be useful for a modern credit decision; by the time they’re filed, they can be 18 months out of date. This is why management accounts have become the primary document for bank underwriters. They provide a real-time snapshot of your current trading position, including up-to-date debtors, creditors, and cash reserves. Engaging a small business accountant who understands these institutional expectations is often the catalyst for a successful offer. Avoid the temptation of “window dressing” your financials by delaying supplier payments or accelerating invoices just before an application. Forensic auditors easily spot these patterns, and they can terminally damage the trust required for a long-term banking partnership. Our team at Davis & Co LLP focuses on maintaining this high standard of reporting to ensure your business remains perpetually bank-ready.

Strategic Debt Structuring and UK Tax Efficiency

Securing capital is rarely just about the immediate cash injection; it’s about optimizing the long-term cost of that capital through the lens of UK fiscal policy. For established businesses, debt often represents a more efficient tool for growth than equity because interest payments are generally a tax-deductible expense. With the main rate of Corporation Tax at 25% for companies with profits exceeding £250,000, the “tax shield” provided by debt can significantly reduce the effective cost of borrowing. When we advise on how to prepare financial statements for a business loan, we ensure that these tax advantages are clearly modeled to show a realistic post-tax cost of capital.

Larger borrowing requirements must account for the Corporate Interest Restriction (CIR) rules. Currently, the UK applies a de minimis threshold of £2 million in net interest expense per annum. If your interest costs exceed this limit, the deductibility of that interest may be restricted to a percentage of your tax-EBITDA. Understanding these thresholds is essential during the preparation phase to ensure your debt servicing doesn’t lead to an unexpected tax burden. By aligning your repayment schedule with your projected taxable profits, you can maintain a balance between aggressive growth and fiscal stability.

Debt vs. Equity: A Strategic Comparison

Retaining total control of your business is perhaps the most compelling argument for choosing debt over equity. While surrendering a 20% stake might feel “free” in terms of cash flow, the long-term cost of giving away future upside and decision-making power is often far higher than a bank’s interest margin. Bank funding remains a primary tool for growth acceleration because it allows owners to leverage existing assets without diluting their ownership. We focus on structuring these loans to protect personal wealth by negotiating terms that limit the scope of personal guarantees, ensuring that the corporate entity remains the primary obligor wherever possible.

International Considerations for Cross-Border Funding

Securing funding for international expansion introduces a layer of complexity regarding withholding tax on cross-border interest payments. If your UK business is borrowing from or lending to overseas entities, you must navigate the relevant double taxation treaties to avoid paying tax on the same interest twice. This is where international tax planning becomes an integral part of your borrowing strategy. We help our clients structure their global debt to ensure compliance with both HMRC and foreign jurisdictions, ensuring that the capital you raise is deployed as efficiently as possible across your entire organizational footprint.

Constructing a Bank-Ready Funding Dossier

Securing high-level funding requires more than a standard business plan; it demands a structured “Funding Dossier” that provides a clinical narrative of your company’s stability. While earlier sections explored the “Lender’s Lens,” the practical application of knowing how to prepare financial statements for a business loan lies in the hierarchy of evidence you present. A modern underwriter expects a cohesive folder containing three years of certified accounts, current management accounts, and aged debtor and creditor ledgers. This evidentiary weight transforms your application from a request for capital into a professional investment proposition.

The presence of an independent audit can be the deciding factor for larger facilities. By engaging in voluntary Audit and Assurance, you provide third-party validation that significantly reduces the bank’s perceived risk. It signals that your internal controls are robust and your figures are beyond reproach. This level of transparency is particularly vital in 2026, as lenders navigate a fragile economic environment and prioritize borrowers who demonstrate absolute financial integrity.

The Forensic Cash Flow Forecast

Banks often reject applications because of overly optimistic “hockey stick” growth projections that lack historical grounding. Your dossier must include a forensic cash flow forecast that features three distinct scenarios: Best Case, Expected, and Worst Case. These projections should be stress-tested against potential interest rate fluctuations and supply chain disruptions. We recommend seeking expert tax advice to ensure your forecasts accurately account for all future liabilities, including VAT payments and Corporation Tax. A forecast that mirrors your historical margins while prudently factoring in new debt servicing costs is far more persuasive than an unproven vision of rapid expansion.

Mitigating Risks and Asset Security

Every loan application involves a discussion on security, typically involving fixed and floating charges over your business assets. A fixed charge applies to specific, identifiable assets like property or machinery, while a floating charge covers dynamic assets such as stock and raw materials. Directors often feel a natural anxiety regarding personal guarantees. You can often limit the scope of these guarantees by presenting a stronger dossier or by utilizing key person insurance and professional indemnity cover as alternative forms of risk mitigation. By proactively addressing how you will protect the lender’s capital, you position yourself as a strategic partner. Our team at Davis & Co LLP can assist you in assembling this bank-ready dossier to ensure your application stands up to the most rigorous forensic scrutiny.

The Role of Strategic Advisory in Securing Capital

The journey to securing capital isn’t a solitary endeavour. While we’ve discussed the technicalities of how to prepare financial statements for a business loan, the final hurdle often involves a face-to-face defence of those figures. A chartered accountant serves as more than a compiler of data; they’re your primary strategist in the bank interview. They help translate raw ledger entries into a narrative of operational excellence. This transition from technical data to strategic storytelling is what convinces a credit committee that your business isn’t just a safe bet, but a high-calibre partner.

Building lender trust requires what we call the “Auditor’s Advantage.” When you provide third-party assurance through our Audit and Assurance services, you’re offering a level of transparency that few SMEs can match. Lenders recognize that audited figures have undergone rigorous verification, which often leads to quicker approvals and more favourable interest margins. Once the offer is on the table, your advisor’s role shifts toward post-funding compliance. Maintaining the financial covenants set by your lender is essential to prevent a technical default, ensuring the longevity and stability of your credit facility.

From Compliance to Capital Readiness

We bridge the gap between basic bookkeeping and bank-standard reporting by focusing on the specific metrics that matter to modern underwriters. Our team conducts a comprehensive Pre-Lending Audit to identify potential financial red flags before they reach a lender’s desk. Whether it’s refining your Management Accounts or restructuring debt to improve your debt service coverage, we ensure you enter negotiations with professional gravitas. This preparation allows us to advocate for better terms, potentially saving your business significant sums in interest costs over the life of the loan. Our approach at Davis & Co LLP is designed to ensure you don’t just meet the criteria but exceed the bank’s expectations.

Long-term Growth Management

Securing the capital is only the beginning. The true measure of success lies in how that capital is deployed to maximize ROI. We work with you on Cash Flow Management to ensure that debt servicing never stifles your day-to-day operations. By monitoring your performance against the forensic forecasts we’ve built, we help you maintain the agility needed to capitalize on new opportunities as they arise. If you’re ready to move from planning to execution, we invite you to contact our partners at Davis & Co LLP for a comprehensive capital readiness review. We’ll ensure your business is positioned for the strategic growth it deserves.

Positioning Your Enterprise for Sustainable Growth

Successfully accessing commercial capital in 2026 requires a shift from traditional business planning to forensic financial storytelling. We’ve explored how the modern lender prioritizes real-time management accounts over historical statutory filings; we also examined why understanding the tax-deductibility of interest is vital for maintaining your margins. By assembling a robust funding dossier and stress-testing your cash flow forecasts, you transform a standard application into a strategic investment proposal. Learning how to prepare financial statements for a business loan is ultimately about demonstrating absolute fiscal discipline and long-term resilience.

As Chartered Certified Accountants since 1901, our team at Davis & Co LLP specializes in business growth acceleration and sophisticated cash flow management. Whether you require expertise in complex international tax planning or niche dental tax services, we provide the professional gravitas needed to negotiate favourable lending terms. We invite you to consult Davis & Co LLP for a strategic capital readiness review to ensure your next funding round is a success. With the right preparation and a steady partnership, the capital you need to scale is within reach.

Frequently Asked Questions

What is the most common reason UK banks reject business loan applications?

Insufficient debt service coverage and inadequate cash flow visibility are the primary drivers of rejection. Banks need to see that your business generates enough surplus cash to meet repayments comfortably after all operating expenses and tax liabilities are settled. If your management accounts show volatile margins or high debtor days, an underwriter will likely view the proposal as too high-risk for a standard facility.

How much can my business realistically borrow based on my EBITDA?

Most UK lenders will facilitate borrowing between 2.5 and 4 times your annual EBITDA, though this varies by sector and asset quality. The calculation is ultimately tethered to your Debt Service Coverage Ratio (DSCR). If your EBITDA is £100,000, a bank typically expects your total annual debt obligations to stay below £80,000 to maintain a healthy 1.25x safety buffer.

Do I always need to provide a personal guarantee for a business bank loan?

Personal guarantees are standard for most unsecured SME loans, but they aren’t always a mandatory requirement for well-capitalized firms with significant assets. If your business can offer a fixed charge on property or machinery, you may be able to negotiate the removal or limitation of a personal guarantee. It’s often a matter of the strength of the security package you present during negotiations.

How far back do banks look at financial statements for funding?

Lenders generally require the last three years of statutory accounts alongside your most recent management accounts. Understanding how to prepare financial statements for a business loan involves ensuring these documents show a consistent or improving trend in profitability. For businesses trading for less than three years, banks will place much heavier weight on forensic cash flow forecasts and the directors’ previous sector experience.

What is the difference between a secured and an unsecured business loan?

A secured loan is backed by a specific asset, such as commercial property, and typically offers lower interest rates of 3% to 5% above the Bank of England base rate. An unsecured loan relies on your business’s creditworthiness and often requires a personal guarantee. In 2026, unsecured representative APRs from high-street banks range from 7.1% to 12.24%, reflecting the higher risk taken by the lender.

How does my personal credit score affect my business’s ability to secure funding?

For SMEs and dental practices, your personal credit score remains a significant factor in the bank’s decision-making process. Lenders view a director’s personal financial conduct as a proxy for how they’ll manage corporate debt. Even if the business is profitable, a history of personal defaults or high credit utilization can lead to less favourable terms or an outright rejection of the application.

Can I get a bank loan to buy another business or dental practice?

Yes, acquisition finance is a standard product for businesses looking to expand through merger or purchase. If you’re a dental professional, using a dental tax specialist to prepare your application is essential, as lenders evaluate healthcare practices based on specific patient-retention metrics and NHS contract stability. These loans are often structured as term loans aligned with the expected return on investment of the acquisition.

How long does the business bank loan application process take in 2026?

The timeline for a business loan in 2026 depends heavily on the type of lender you choose. Digital challenger banks can often provide a decision and funds within 48 hours because of Open Finance integrations. Traditional high-street banks typically require four to eight weeks for a full forensic review and credit committee approval, particularly for larger, more complex secured facilities.