The very structure you build to grow your private practice could be the silent architect of your NHS pension’s decline. For many healthcare professionals, the transition into dual-stream work brings a sense of professional freedom, yet it often introduces a level of financial complexity that’s difficult to manage alone. We understand that accounting for private vs nhs income isn’t just about balancing two sets of books; it’s about protecting a lifetime of public service benefits while capitalising on your commercial potential.

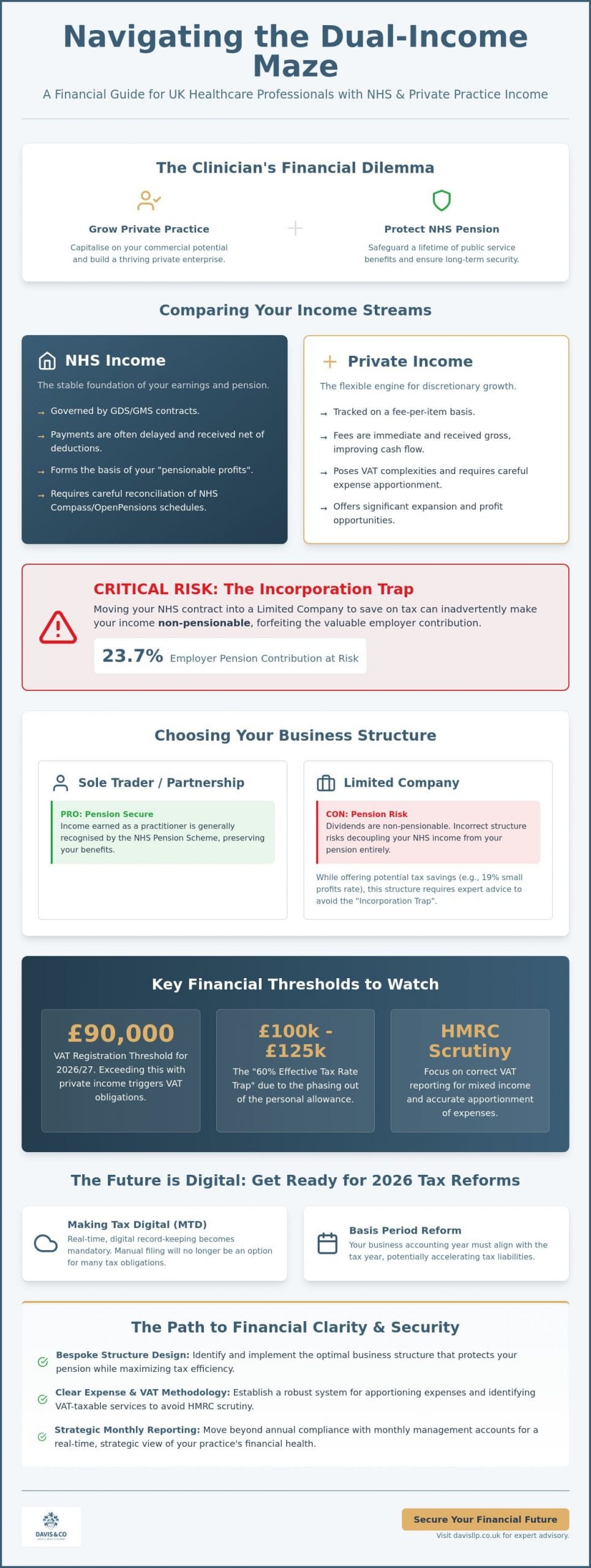

You’re likely concerned about the risk of breaking the link to your NHS pension through incorrect incorporation or facing HMRC scrutiny regarding mixed-income VAT. It’s a valid worry, especially with the VAT registration threshold set at £90,000 for the 2026/27 tax year and the effective 60% tax rate trap for income between £100,000 and £125,140. We’ll help you master these complexities to ensure your business remains tax-efficient and your 23.7% employer pension contributions stay secure. In this guide, we’ll explore how to design a bespoke structure that provides clear visibility of your profitability and keeps your long-term security intact.

Key Takeaways

- Identify the structural risks that could inadvertently decouple your private earnings from your NHS pension benefits.

- Navigate the nuances of accounting for private vs nhs income to ensure both streams are reported accurately while maximising your overall tax efficiency.

- Assess how the 2026 Corporation Tax rates influence the choice between remaining a sole trader or operating as a limited company for your private work.

- Establish a clear methodology for apportioning expenses and identifying VAT-taxable services within your private practice to avoid HMRC scrutiny.

- Move beyond annual compliance by using monthly management accounts to gain a strategic view of your practice’s growth and financial stability.

The Dual Income Landscape: Understanding NHS and Private Streams

The modern clinical career often occupies a hybrid space. While the foundational UK Private Healthcare System offers significant expansion opportunities, the integration of these earnings with state funded work creates a unique set of administrative challenges. Effectively accounting for private vs nhs income requires more than just separate bank accounts; it demands a deep understanding of how two fundamentally different financial ecosystems interact. We see this not merely as a bookkeeping task, but as a strategic exercise in balancing public service commitments with private enterprise.

NHS income is typically governed by GDS or GMS contracts, which dictate strict parameters for how funds are received and reported. These payments are often delayed, arriving as a net figure after various levies and pension contributions have been stripped away. In contrast, private fees are immediate and gross, usually tracked through practice management software on a fee per item basis. This creates a disparity in cash flow timing that can obscure your actual financial position if not managed with precision. We encourage our clients to view this as a strategic division: the NHS stream provides the reliable stability of a baseline, while the private stream serves as the engine for discretionary growth.

Reconciling NHS Schedules and Private Software

Mapping data from NHS Compass or OpenPensions into your primary accounting software is a frequent point of friction. The primary pitfall is the time lag; work completed in one month might not appear on a schedule until several weeks later. These schedules also contain deductions for items like clinical waste or local levies that don’t always align with the gross figures recorded in your clinical software. Without careful reconciliation, these discrepancies lead to an overestimation of your true profitability and potential errors in your personal tax filings.

The 2026 Regulatory Environment

The arrival of Making Tax Digital (MTD) represents a significant shift for clinicians with multiple income sources. By 2026, the requirement for real time digital record keeping becomes paramount, as manual filing is no longer permitted for VAT and the scope for income tax continues to expand. Practitioners must align their reporting periods to meet these new digital standards, ensuring that every transaction, whether from a private patient or an NHS contract, is captured accurately.

The 2026 basis period reform forces medical professionals to align their accounting year with the tax year, potentially accelerating tax liabilities during the transition period. This makes it essential to maintain a clear, digital audit trail that separates the two streams while providing a consolidated view of your total tax exposure. Our role is to ensure these two streams coexist without compromising your compliance or your sanity.

The NHS Pension Dilemma: Why Business Structure is Critical

The choice of business structure is perhaps the most consequential decision a clinician will make regarding their long-term wealth. While the expansion of a private practice offers immediate financial rewards, the vehicle you choose to house that income can have profound implications for your retirement security. Effective accounting for private vs nhs income requires a nuanced understanding of “pensionable profits”—the specific portion of your earnings that the NHS Pension Scheme (NHPS) recognises for contributions. Misjudging this boundary doesn’t just lead to tax inefficiencies; it can fundamentally compromise your eligibility for one of the UK’s most robust pension frameworks.

A common pitfall we observe is the “Incorporation Trap.” Many practitioners are drawn to the limited company model to benefit from the 19% small profits rate or to manage the marginal relief bracket for profits between £50,001 and £250,000. However, the NHPS generally only recognises income earned as a practitioner in a sole trader or partnership capacity. If you move your NHS contract into a limited company, you risk rendering that income non-pensionable. Because dividends are currently non-pensionable, a dividend-heavy extraction strategy might offer short-term corporation tax savings but will forfeit the 23.7% employer contribution that defines the NHPS’s value. Balancing these interests requires the kind of personal tax services that look beyond the current tax year toward a decades-long horizon.

Adhering to the professional standards outlined in the GMC Good Medical Practice guidance involves maintaining integrity in all financial dealings. This includes ensuring your business structure doesn’t inadvertently obscure your professional obligations or your pension entitlements. We believe that a well-considered structure should act as a bridge between your clinical duties and your commercial ambitions, rather than a barrier to either.

Associates vs. Principals: Pension Accounting Nuances

The calculation of superannuation contributions differs significantly between associates and practice owners. Associates typically pay contributions based on a fixed percentage of their gross NHS earnings, whereas principals must account for their share of the practice’s net pensionable profit. With tiered member contribution rates reaching 12.5% for those earning over £67,669, understanding your “Total Pensionable Pay” is essential for managing your annual allowance and avoiding unexpected tax charges in a high-income 2026 environment.

The Certificate of Pensionable Profits

The annual reconciliation process is where many accounting errors take root. The Certificate of Pensionable Profits must be meticulously prepared to ensure the figures align perfectly with your self-assessment tax return. Understating these profits can lead to a shortfall in your future retirement benefits, while overstating them results in unnecessary present-day costs. Securing expert tax advice in the UK ensures this certificate is a true reflection of your dual-stream earnings, protecting your pension link without overpaying on contributions.

Sole Trader vs. Limited Company: Choosing Your Vehicle

The decision to operate as a sole trader, within a partnership, or through a limited company is a pivotal moment in a clinician’s career. For those managing a mixed portfolio, the 2026 Corporation Tax framework adds a layer of complexity to this choice. While the small profits rate of 19% remains attractive for companies with profits under £50,000, the main rate of 25% for those exceeding £250,000 requires careful modeling. Accounting for private vs nhs income effectively often means looking past a one size fits all solution to find a structure that respects both your clinical reality and your fiscal goals.

We frequently advise on a “hybrid” or dual structure. This involves maintaining your status as a sole trader for NHS contract work to preserve your pension link, while silo-ing your private fee income within a limited company. This approach can be highly effective, but it’s not always available to everyone. Some GDS or GMS contracts explicitly forbid the transfer of the contract to a corporate entity, making this distinction a contractual necessity rather than just a tax preference. Understanding these legal boundaries is the first step in building a secure financial foundation.

When Incorporation Makes Financial Sense

The “tipping point” for incorporation usually occurs when private fee income exceeds your immediate lifestyle needs. By retaining profits within a company, you avoid the higher and additional income tax rates of 40% and 45% on that surplus. This capital can then be deployed for business growth acceleration, such as investing in high tech dental scanners or clinical equipment, where the company benefits from capital allowances. A corporate structure also offers refined family tax planning opportunities through shareholdings, provided these arrangements are commercially justified and reflect genuine contribution.

The Risks of the Hybrid Structure

Operating a hybrid model introduces a higher degree of administrative rigour. You must manage inter-company transactions with precision to ensure that the personal and corporate entities remain distinct. HMRC maintains a keen interest in “Personal Service Companies” and the application of IR35 rules within medical settings. It’s vital to ensure that costs, such as practice overheads or staff time, are accurately apportioned between your NHS and private work. Failing to do so risks double taxation or unwanted scrutiny. Our approach focuses on creating clear visibility of profitability for both streams, ensuring that your cash flow management remains robust across both entities.

VAT and Expense Apportionment: Navigating Hidden Risks

While the majority of clinical work remains exempt from VAT, the expansion of private services into aesthetic or wellbeing categories introduces a significant regulatory hurdle. Accounting for private vs nhs income requires a precise distinction between medical care, which aims to protect or restore health, and purely cosmetic procedures, which attract the standard 20% VAT rate. With the VAT registration threshold set at £90,000 for the 2026/27 tax year, many practitioners find themselves approaching this limit through their private fee income alone, even if their total turnover is much higher.

HMRC has identified mixed-income practices as a priority area for inspections in 2026. Their focus often centres on the Partial Exemption method, a calculation that determines the proportion of input VAT you can reclaim on business expenses. If your practice generates both exempt NHS income and taxable private fees, you aren’t permitted to simply reclaim all VAT on your overheads. Instead, you must apply a rigorous apportionment to ensure you aren’t over-claiming, a process that demands a high level of analytical detail. Precise accounting for private vs nhs income is the only reliable way to safeguard your practice against the financial penalties of an incorrect VAT return.

Apportioning Overheads Correctly

Developing a robust formula for splitting rent, rates, and utilities between your two income streams is essential for compliance. This isn’t merely a matter of floor space; it requires documenting staff time with clinical precision. For instance, a receptionist’s hours must be split based on the volume of NHS versus private patient interactions. Relying on “reasonable apportionment” is no longer sufficient; a modern small business accountant will insist on evidence-backed data to withstand a potential audit. If you are concerned about your current exposure, our VAT compliance specialists can perform a thorough review of your apportionment methods.

Capital Allowances on Shared Equipment

The 2026 Full Expensing rules offer a powerful incentive for medical partnerships to invest in clinical technology. When equipment is used for both NHS and private patients, you can still maximise tax relief, provided the usage is correctly documented. A £50,000 investment in clinical technology can be fully deducted from your taxable profits in the year of purchase under these rules, provided the equipment qualifies as new and unused plant or machinery. This immediate relief significantly improves cash flow, allowing for further reinvestment in your practice’s growth. We help you navigate these rules to ensure every pound spent on technology works as hard as possible for your clinical and commercial success.

The Davis & Co Approach: Strategic Advisory for Clinicians

Our approach at Davis & Co is built on the premise that accounting for private vs nhs income shouldn’t be a retrospective exercise confined to a year end filing. We believe that true financial control comes from proactive, monthly management accounts that provide clinical directors with real time visibility of their performance. By the time the tax year concludes, our clients already understand their liabilities and have implemented the necessary strategies to mitigate them. We act as a strategic partner, helping you scale your private practice while ensuring your NHS legacy remains protected and your pension entitlements stay secure.

The complexity of the NHS BSA and its specific terminology requires more than generalist knowledge. Engaging a chartered accountant who understands the nuances of superannuation and contract types is essential for maintaining the integrity of your dual stream income. We bridge the gap between clinical operations and sophisticated financial management, allowing you to focus on patient care while we manage the intricate details of your commercial growth. For practitioners with cross border interests or expat status, we integrate international tax planning into your broader business structure, addressing a common gap in the advice typically offered to high earning UK clinicians.

Wealth Preservation and Trust Tax

Protecting the wealth generated through your private practice is a long term commitment. We utilise Trusts to safeguard assets for the next generation, ensuring that your hard work translates into lasting security. This includes comprehensive Inheritance Tax planning for healthcare professionals who hold significant property portfolios or practice assets. By coordinating your personal tax return with your practice accounts, we provide a level of transparency that ensures your total wealth is managed cohesively rather than in isolation.

Next Steps: Securing Your Financial Future

The first step toward achieving financial efficiency is a specialist dental or medical tax review. Our onboarding process begins with a comprehensive audit of your current income split and business structure, identifying immediate opportunities for tax savings and pension protection. We don’t just look at the numbers; we examine the underlying contracts and professional goals that drive them. If you’re ready to move beyond basic compliance and embrace a strategic approach to your finances, speak to our specialist dental tax team today to begin your audit.

Securing Your Professional Legacy and Commercial Growth

Managing a dual-stream career requires more than just administrative diligence; it demands a strategic alignment of your clinical commitments and commercial ambitions. We’ve explored how the right business structure protects your NHS pension link while providing the flexibility to scale your private practice. By mastering the nuances of accounting for private vs nhs income, you ensure that every patient interaction, whether state-funded or private, contributes to a cohesive financial future. Precise VAT apportionment and proactive management accounts are the tools that allow this balance to exist without compromising your long-term security.

As dental tax specialists and Chartered Certified Accountants with a history dating back to 1901, we bring a level of professional gravitas and niche expertise that’s essential for navigating the complexities of the NHS BSA. Our national UK coverage ensures that we’re positioned to support your practice’s growth wherever you’re located. To move beyond year-end compliance toward a partnership based on quiet excellence, Consult Davis & Co LLP for Specialist Dental and Medical Tax Advice. Your professional journey deserves a financial foundation as robust as the care you provide.

Frequently Asked Questions

Can I pay my NHS income directly into my limited company bank account?

You cannot pay NHS income into a limited company bank account if the underlying contract is held in your personal name. Most GDS and GMS contracts are non-corporate; therefore, the funds must be received by the individual or partnership named on the contract. Diverting these payments into a corporate entity without a formal contract novation risks breaking your link to the NHS pension and creating significant tax complications.

Does earning private income reduce my NHS pension benefits?

Private earnings do not reduce the value of the benefits you’ve already earned, but they can increase the cost of your ongoing contributions. High private income may push your total earnings into a higher tiered contribution bracket, which currently reaches 12.5% for pay over £67,669. Furthermore, substantial private growth can trigger Annual Allowance tax charges if your total pension growth exceeds the statutory limits for the year.

What is the VAT threshold for private cosmetic treatments in 2026?

The VAT registration threshold for the 2026/27 tax year is £90,000. This threshold applies specifically to your taxable turnover, which includes cosmetic procedures and other services that don’t qualify as exempt medical care. You must monitor your rolling twelve-month turnover carefully; if your private cosmetic fees exceed this limit, you’re legally required to register for VAT and apply the 20% rate to those services.

How do I apportion practice expenses between NHS and private work for HMRC?

You must use a fair and reasonable methodology to split shared costs, such as rent, utilities, and staff wages. Common techniques involve apportioning expenses based on surgery hours, floor space, or a percentage of total turnover. Maintaining detailed records is essential for accurate accounting for private vs nhs income, as it ensures you only reclaim the correct proportion of input VAT on your practice overheads.

Is it better to be a sole trader or a limited company for a mixed-income dentist?

The ideal structure depends on your specific ratio of NHS to private work and your retirement objectives. While a limited company can offer tax advantages for private fees, it’s generally unsuitable for NHS income because dividends are non-pensionable. Many practitioners find that a hybrid approach provides the most efficiency, allowing them to protect their NHS pension while managing their private practice growth through a corporate vehicle.

What happens to my NHS pension if I stop doing NHS work but keep my private practice?

Stopping NHS work makes you a deferred member of the NHS Pension Scheme. Your accrued benefits remain in the scheme and are adjusted for inflation, but you’ll no longer receive the 23.7% employer contributions. Before making this transition, it’s vital to ensure your private practice generates enough profit to fund an alternative retirement strategy that matches the security and value of the public sector scheme.

How does the 2026 basis period reform affect my tax payments on private income?

The 2026 basis period reform mandates that all self-employed clinicians report their profits based on the tax year ending April 5th. This change removes the flexibility of choosing a different accounting year-end and may lead to a transitional tax spike as overlapping profits are brought into charge. Aligning your accounting for private vs nhs income with the tax year is now a mandatory requirement for all practitioners.

Can a specialist accountant help me with an HMRC investigation into my medical practice?

A specialist accountant provides critical defence during an HMRC investigation by managing technical queries and ensuring your apportionment methods are legally defensible. Our Audit and Assurance services focus on protecting your practice from the stress of an inquiry while justifying your historical tax positions. We act as your professional advocate, ensuring that all clinical and commercial nuances are correctly presented to the tax authorities.