What if the primary value of your estate plan isn’t the legal document itself, but the specific tax architecture you build around it? For high-net-worth individuals and business owners, choosing the right type of trust for tax planning has become a sophisticated balancing act between maintaining long-term control and achieving genuine fiscal efficiency. We understand that the “Relevant Property” tax regime often feels like an impenetrable maze, particularly as strict Trust Registration Service compliance deadlines add a layer of administrative pressure. You’ve worked hard to build your wealth; it’s only natural to feel hesitant about structures that might seem to diminish your influence over your assets while seeking to protect them.

This guide provides a professional analysis of modern UK trust structures designed to help you navigate these complexities with composed confidence. We’ll outline how to minimise Inheritance Tax and Capital Gains Tax exposure while ensuring your succession plan remains legally robust and fully compliant with the 2026 regulatory landscape. We’ll examine the specific frameworks available to help you select a trust type that aligns with your family’s multi-generational goals and secures your legacy for the years ahead.

Key Takeaways

- Understand how trusts act as a cornerstone for UK Inheritance Tax mitigation by effectively separating legal and beneficial ownership of your assets.

- Learn the critical criteria for choosing the right type of trust for tax planning, comparing the flexibility of discretionary structures against the absolute entitlement of bare trusts.

- Navigate the 2026 Trust Registration Service (TRS) landscape to ensure your arrangements remain compliant within the mandatory 90-day registration window.

- Discover how to manage the “Relevant Property” regime, including strategic approaches to the 20% entry charge and periodic 10-year anniversary charges.

- Follow a structured framework for defining trust objectives and appointing professional trustees to maintain the long-term integrity of your estate.

The Strategic Role of Trust Funds in UK Wealth Management

A trust is a fiduciary arrangement that establishes a clear distinction between legal and beneficial ownership. In this structure, one party, known as the settlor, transfers assets to another, the trustee, to be managed for the benefit of a third party, the beneficiary. This separation is the engine behind sophisticated wealth management. When we assist clients in choosing the right type of trust for tax planning, we aren’t merely drafting a legal document; we’re creating a bespoke framework to protect capital from unnecessary erosion.

Historically, trusts have served as the cornerstone of UK inheritance tax (IHT) mitigation. By moving assets into a trust, a settlor can effectively remove those assets from their personal estate, provided they survive the gift by seven years and don’t retain a benefit. Beyond tax, these structures offer robust asset protection. They act as a shield, safeguarding family wealth from potential matrimonial claims, business insolvency, or the risks associated with spendthrift heirs. As we look toward the 2026 fiscal environment, trusts have evolved to meet rigorous HMRC transparency standards. While the reporting requirements are more stringent than in previous decades, the core benefits of control and protection remain unmatched for those with significant UK interests.

Beyond the Myth: Strategic Applications for Modern Estates

There’s a common misconception that trusts are reserved exclusively for the ultra-wealthy. In practice, they’re highly effective tools for any business owner or family with assets exceeding the £325,000 nil-rate band. We often use these structures to manage corporate succession, allowing private company shares to be held in a way that protects the business’s operational integrity while providing for the next generation. Trusts also facilitate structured education funding. They allow grandparents to gift capital for a grandchild’s schooling while ensuring the funds aren’t accessible for other purposes until the beneficiary reaches a certain maturity. This level of multi-generational gifting is central to the UK trust taxation principles that govern modern estate planning.

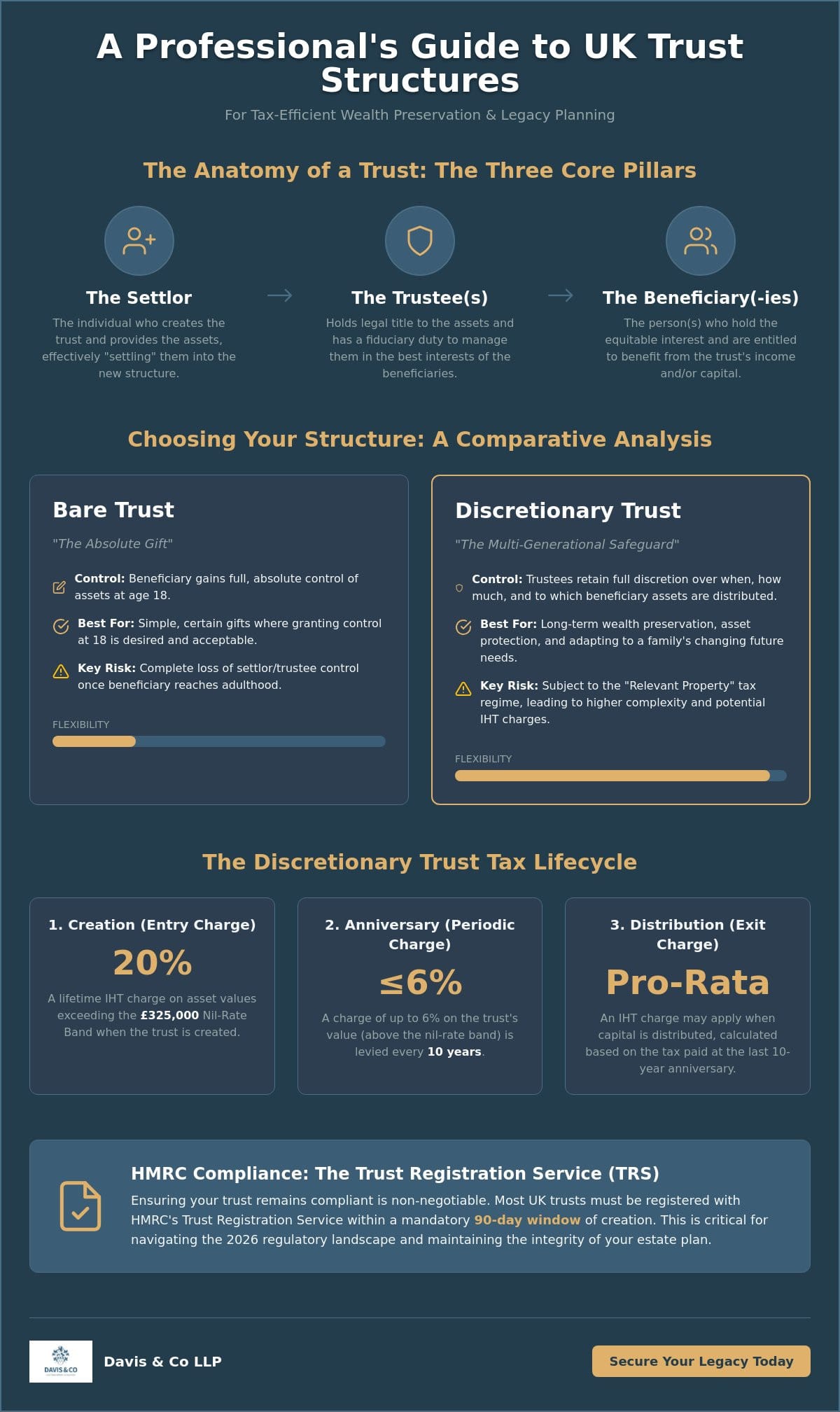

The Core Pillars: Settlors, Trustees, and Beneficiaries

Success depends on understanding the three core roles within any trust. The settlor is the individual who creates the trust and provides the assets. Their primary challenge is the “divestment” of legal control, which is necessary for the trust to be recognized by HMRC as a valid tax-planning vehicle. The trustees hold the legal title and carry the weight of a heavy fiduciary duty; they must act in the best interests of the beneficiaries at all times. While many families appoint “lay trustees” like friends or relatives, the complexity of 2026 compliance often makes professional oversight a necessity. Finally, the beneficiaries hold the equitable interest. Whether they’re entitled to the trust’s income, its capital, or both, their rights must be carefully balanced to ensure the settlor’s original intent is preserved. Choosing the right type of trust for tax planning requires a deep understanding of how these three roles will interact over several decades.

Evaluating UK Trust Structures: Bare vs. Discretionary vs. Interest in Possession

Selecting the appropriate vehicle requires a nuanced understanding of how control and tax liability intersect. Bare trusts represent the simplest form; they function as an “absolute gift” where the beneficiary has an immediate right to the trust property. While this model is administratively light, it carries a significant risk. Once the beneficiary reaches 18, they gain full legal control over the assets. For many parents and grandparents, this lack of deferred control makes bare trusts less appealing for substantial capital transfers. In these cases, choosing the right type of trust for tax planning involves looking beyond simplicity toward more robust protection.

Discretionary trusts offer a different path by providing the trustees with the power to decide the timing and amount of any distributions. A Discretionary Trust is the most flexible vehicle for long-term multi-generational wealth preservation. This flexibility is invaluable, as it allows the family to respond to changing circumstances, such as a beneficiary’s career success or personal struggles. Interest in Possession (IIP) trusts, often called “Life Interest” trusts, provide a middle ground. They grant a specific beneficiary, the “life tenant,” a right to the trust income for their lifetime, while the underlying capital is preserved for the “remaindermen.” This structure is frequently employed in second marriage scenarios. It ensures a surviving spouse is supported while guaranteeing that the family estate eventually passes to children from a first marriage.

Matching Structure to Family Dynamics

Family protection is often as important as tax mitigation. Discretionary trusts are frequently preferred for protecting assets from a beneficiary’s potential insolvency or matrimonial claims. Because the beneficiary has no absolute right to the capital, the assets are generally shielded from third-party creditors. When choosing the right type of trust for tax planning, we also consider settlor-interested trusts. These arise if the settlor, or their spouse, can benefit from the trust assets. HMRC’s anti-avoidance rules are particularly strict here; the settlor remains liable for income tax on the trust’s income, regardless of whether it’s distributed. Our trust tax services are designed to help you navigate these complex rules without falling into unintended tax traps.

Tax Differentiation Across Trust Vehicles

Tax treatment varies significantly between these vehicles. In a discretionary trust, income tax is generally charged at the trust rate of 45% for non-dividend income, though beneficiaries may claim a tax credit upon distribution. Crucially, discretionary trusts often benefit from Capital Gains Tax (CGT) hold-over relief. This allows the gain to be deferred when assets are settled into the trust, a major advantage for business owners. This contrasts with bare trusts, where the beneficiary is personally liable for tax on income and gains as they arise. Regardless of the chosen structure, compliance is mandatory. Trustees must ensure the arrangement is recorded with the HMRC Trust Registration Service (TRS) to avoid penalties. For a deeper dive into how these thresholds impact your specific bracket, you may find our guide on expert tax advice in the UK helpful.

The Step-by-Step Process of Setting Up a Trust Fund

Establishing a trust is a deliberate, multi-stage process that transforms a settlor’s strategic intent into a legally binding reality. While the previous sections explored the “why” and “which,” this section focuses on the practical “how.” Crucially, choosing the right type of trust for tax planning serves as the foundation for this entire sequence, as the specific structure dictates the legal and administrative requirements that follow. The process typically unfolds through five distinct phases:

- Phase 1: Defining the Trust Objective. We begin by identifying the specific goal, whether it’s mitigating a potential IHT liability or protecting a family business. This involves selecting the asset class for settlement, such as cash, property, or private shares.

- Phase 2: Appointing Trustees. Selection is critical. While family members are often chosen, the complexity of 2026 compliance makes professional oversight a necessity to ensure fiduciary duties are met and HMRC deadlines are respected.

- Phase 3: Drafting the Trust Deed. This legal document establishes the rules of the trust. HMRC recognizes several Types of UK trusts, and the deed must be tailored to the specific tax treatment of the chosen vehicle.

- Phase 4: The Settlement. This is the formal legal transfer of assets into the trust’s name. It’s the moment the settlor divests themselves of legal ownership.

- Phase 5: Registration. Most new trusts must be registered with the Trust Registration Service (TRS) within 90 days of becoming liable for tax.

The Importance of a Bespoke Trust Deed

Generic templates often fail to address the nuanced requirements of a complex family estate or corporate structure. A bespoke trust deed allows for the inclusion of specific clauses regarding investment powers and the potential exclusion of certain beneficiaries. We also recommend drafting a “Letter of Wishes.” While this document isn’t legally binding, it provides essential guidance to trustees on how the settlor intends the trust to operate in practice, especially regarding the timing of distributions to younger generations.

Asset Transfer Nuances: Property, Cash, and Shares

The tax implications of “settling” an asset vary significantly by asset class. Transferring UK property into a trust may trigger Stamp Duty Land Tax (SDLT) and immediate Capital Gains Tax (CGT) liabilities. Conversely, the strategic transfer of private company shares can often be managed more efficiently by utilizing Business Relief (BR) to reduce the IHT impact. For clients with more complex cross-border interests, our expertise in international tax planning ensures that non-UK assets are integrated into the structure without creating unintended tax friction. Choosing the right type of trust for tax planning requires a holistic view of these asset-specific rules to avoid costly entry charges.

HMRC Compliance and the Trust Registration Service (TRS)

While choosing the right type of trust for tax planning is a vital strategic first step, the long-term integrity of the arrangement depends on rigorous adherence to HMRC’s evolving compliance framework. In 2026, the Trust Registration Service (TRS) sits at the heart of this oversight. Transparency is no longer a choice; it’s a gateway requirement for almost all interactions with the UK tax system. Trustees now operate in a digital-first regulatory environment where Anti-Money Laundering (AML) obligations are strictly enforced. This means that even if a trust doesn’t currently have a tax liability, its existence and its beneficial ownership must likely be recorded on the national register to ensure full legal standing.

The administrative burden has shifted from occasional reporting to an ongoing requirement for accuracy. Trustees are legally responsible for updating the register within 90 days of any significant change, such as the appointment of a new trustee or a change in the defined class of beneficiaries. This level of scrutiny reflects a broader international move toward financial transparency, making professional record-keeping a non-negotiable aspect of wealth preservation.

TRS Deadlines and Penalty Avoidance

HMRC distinguishes between taxable and non-taxable trusts, yet the scope for registration has expanded significantly. Almost all “express” trusts created by a deed must now register, regardless of whether they currently hold a tax liability. Trustees have a strict 90-day window from the date of the trust’s creation to complete this process. For the 2026/27 tax year, the consequences of non-compliance are increasingly severe, with HMRC utilizing an automated penalty regime for late registrations. We view the 2026 HMRC stance on trust transparency as a mandatory pillar of modern estate management.

The Annual Trustee Compliance Cycle

Compliance is a continuous cycle rather than a one-off event. Trustees must prepare annual trust accounts and, where applicable, submit the SA900 Trust and Estate Tax Return to report income and capital gains. When distributions are made to beneficiaries, the issuance of R185 certificates is essential, as these documents allow beneficiaries to correctly report trust income on their personal tax returns. Beyond these filings, we recommend maintaining a formal “Minute Book.” This documents every strategic decision made by the trustees, providing a robust audit trail that justifies the trust’s management in the eyes of HMRC. If you’re concerned about meeting these rigorous standards, our Trust Tax Services can provide the professional oversight necessary to secure your family’s legacy.

Optimizing the Tax Efficiency of Your Trust Fund

While the initial legal structure provides the foundation, the true fiscal value of an estate plan is realized through the active management of its tax lifecycle. For those choosing the right type of trust for tax planning, most discretionary arrangements will fall under the “Relevant Property” regime. This framework imposes a 20% entry charge on lifetime transfers that exceed the current £325,000 Nil-Rate Band (NRB). It’s a significant threshold; exceeding it without a clear strategy can lead to immediate tax friction. However, these entry charges often act as a gateway to broader benefits, such as removing future growth from your personal estate and providing a robust shield against 40% death charges on the underlying capital.

Capital Gains Tax (CGT) management is equally vital. Under Section 260 of the TCGA 1992, many trusts benefit from “hold-over relief.” This allows a settlor to transfer assets into a trust without triggering an immediate CGT liability, effectively deferring the gain until the trustees eventually sell the asset or distribute it to a beneficiary. This deferral is a powerful tool for business owners settling private company shares, as it preserves capital that would otherwise be lost to immediate taxation. We find that integrating this relief into the broader succession plan is often the deciding factor when choosing the right type of trust for tax planning.

Strategic Management of the 10-Year Anniversary Charge

Discretionary trusts are subject to periodic charges every ten years, calculated at a maximum of 6% on the value exceeding the available Nil-Rate Band. Professional asset valuation is paramount as these deadlines approach. An inaccurate valuation can lead to overpayment or, conversely, HMRC penalties for under-reporting. Trustees must also plan for liquidity; if the trust holds illiquid assets like property or shares, there must be a strategy to meet the tax bill without forced sales. We also advise clients to be mindful of “related settlements.” If you create multiple trusts on the same day, they must share a single Nil-Rate Band, which can significantly increase the periodic tax burden.

Income and Capital Gains Tax Mitigation

Trustees have a £500 standard rate band where income is taxed at lower rates, but beyond this, the 45% trust rate generally applies. Efficiency often depends on the timing of distributions. Distributing income to beneficiaries in lower tax brackets can allow them to reclaim tax paid by the trust, effectively reducing the overall family tax leak. Conversely, accumulating income within the trust might be preferable for long-term capital growth despite the higher immediate rate. For bespoke calculations regarding your next periodic charge or to refine your distribution strategy, our trust tax services provide the technical precision required to maintain your trust’s efficiency over several generations.

Securing Your Multi-Generational Legacy

Trusts remain a vital component of UK wealth management, provided they’re underpinned by a rigorous compliance framework. The process of choosing the right type of trust for tax planning requires a careful evaluation of family dynamics, asset classes, and the specific tax regimes that apply in 2026. Whether you select a flexible discretionary structure or an interest in possession model, your focus must stay on balancing immediate tax efficiency with long-term control over your capital. It’s a complex task, but it doesn’t have to be a solitary one.

At Davis & Co LLP, our heritage as Chartered Certified Accountants dates back to 1901. We specialize in complex international and domestic trust tax planning, providing a partner-led service that prioritizes discretion and professional gravitas. We invite you to consult our Trust Tax Specialists for a bespoke wealth strategy to ensure your estate is both compliant and optimized for the future. Protecting your wealth is a journey, and with the right architectural support, you can secure a stable and prosperous legacy for the generations to come.

Frequently Asked Questions

How much does it cost to set up a trust fund in the UK in 2026?

The costs associated with establishing a trust depend heavily on the complexity of your estate and the specific asset classes being settled. Primary expenses typically include professional fees for drafting a bespoke Trust Deed and providing strategic tax advice. Ongoing costs may include annual accounting, tax return preparation, and professional trustee fees if you opt for external oversight to ensure long-term compliance.

Can I be a trustee of my own trust fund?

Yes, a settlor can serve as a trustee of the trust they’ve created. This allows you to retain a degree of involvement in the management of the assets. However, you must be mindful of settlor-interested tax rules; if you or your spouse can benefit from the trust, the income remains taxable as your own. We often recommend appointing at least one professional trustee to maintain impartial governance.

What is the main difference between a trust and a will?

A will is a static document that only takes effect upon your death, whereas a trust is a living arrangement that can manage assets during your lifetime and beyond. While a will must go through the public probate process, a trust offers immediate, private succession. Choosing the right type of trust for tax planning allows for more sophisticated control over how and when beneficiaries receive their inheritance.

How is a trust fund taxed on its investment income?

For the 2026/27 tax year, discretionary trusts pay a 45% rate on non-dividend income and 39.35% on dividend income after a £500 tax-free allowance. Interest in possession trusts are generally taxed at 20% for non-dividend income and 10.75% for dividends. Choosing the right type of trust for tax planning involves calculating which of these structures offers the most efficient path for your specific investment portfolio.

Can a trust fund be challenged or overturned in court?

Yes, trusts can be contested on grounds such as a lack of mental capacity at the time of creation, undue influence, or a failure to meet legal formalities. Creditors may also challenge a trust if they can prove it was established solely to shield assets from legitimate claims. Maintaining a robust audit trail and a clear Letter of Wishes is essential to defend the trust’s integrity against such challenges.

Do I need a separate bank account for a UK trust?

Yes, trustees have a strict fiduciary duty to keep trust assets entirely separate from their own personal finances. A dedicated trust bank account is a practical necessity for accurate record-keeping and transparent reporting to HMRC. It ensures that all income and capital transactions are clearly identifiable, which is a core requirement for fulfilling your obligations under the Trust Registration Service (TRS) and AML regulations.

How do I close or wind up a trust fund legally?

Winding up a trust involves the final distribution of all remaining assets to the beneficiaries as dictated by the Trust Deed. Before closure, trustees must ensure all outstanding tax liabilities, including any exit charges or final income tax returns, are fully settled with HMRC. The final step is to formally update the Trust Registration Service (TRS) to record that the trust has been terminated and no longer exists.

What happens to the trust assets if a trustee dies?

Trust assets are held legally by the trustees but don’t form part of a deceased trustee’s personal estate. If a trustee dies, the legal title to the assets typically passes to the surviving trustees, who continue to manage the trust. If the deceased was the sole trustee, the provisions in the Trust Deed or the deceased’s personal representatives will determine the appointment of a successor to ensure continuity of management.