Could a single administrative oversight in your SA900 filing jeopardize your standing as a trustee? With the 2026/27 tax year introducing a 39.35% dividend trust rate and a new £2.5m cap on Business Property Relief, the margin for error has never been thinner. We understand that managing multi-jurisdictional assets while maintaining meticulous records is a significant burden. Our trust tax return filing service is designed to alleviate this pressure, providing the technical precision required to satisfy HMRC’s increasingly rigorous standards.

You likely feel the weight of your fiduciary responsibilities, especially when faced with the £100 late filing penalty or the complexity of the £1,500 Capital Gains Tax annual exempt amount. This guide provides a clear path through the compliance landscape, offering expert guidance on the SA900 process and strategic insights to reduce tax liabilities safely. We’ll examine the critical deadlines for 2026 and how to ensure your reporting remains transparent and accurate for every beneficiary, giving you total peace of mind in an evolving regulatory environment.

Key Takeaways

- Understand how the 2026 reporting standards for the SA900 require more granular detail to protect your fiduciary standing and ensure full compliance.

- Identify the specific income and capital gains reporting duties that trustees must fulfill to mitigate the risk of significant HMRC penalties.

- Discover why engaging a professional trust tax return filing service is a critical step in managing the personal liability risks inherent in complex asset structures.

- Learn how to establish a robust audit trail and systematic record-keeping process that provides clarity for beneficiaries and tax authorities alike.

- Explore the strategic advantages of aligning trust compliance with broader international tax planning for a more cohesive and efficient financial framework.

Navigating Trust Tax Return Filing in 2026

The SA900 Trust and Estate Tax Return serves as the definitive compliance document for trustees in the United Kingdom. For the 2026 tax year, reporting requirements have moved toward a level of granularity that demands meticulous attention to detail. HMRC now requires a more comprehensive disclosure of trust assets and income streams to ensure total transparency across the board. Engaging a professional trust tax return filing service ensures these evolving complexities don’t lead to unintended non-compliance or fiduciary risk.

Trust structures vary significantly, from Discretionary Trusts to Interest in Possession arrangements, and each carries distinct tax implications under English trust law. Identifying the specific filing needs for your specific structure is the primary step toward effective stewardship. Central to this process is the “principal acting trustee,” who bears the ultimate responsibility for the accuracy of the submission. While all trustees share liability, this individual acts as the primary liaison with HMRC, managing data flow and ensuring all declarations are validated and submitted within the prescribed windows.

The Evolving Regulatory Landscape for Trustees

HMRC’s recent transparency initiatives have fundamentally altered how trust data is captured and cross-referenced. It’s no longer sufficient to report headline figures; trustees must now align their annual SA900 filings with the live data held on the Trust Registration Service (TRS). This alignment is particularly critical for those involved in international tax planning, where cross-border assets can complicate the reporting narrative. We focus on ensuring every disclosure is consistent, reflecting a cohesive strategy that stands up to scrutiny.

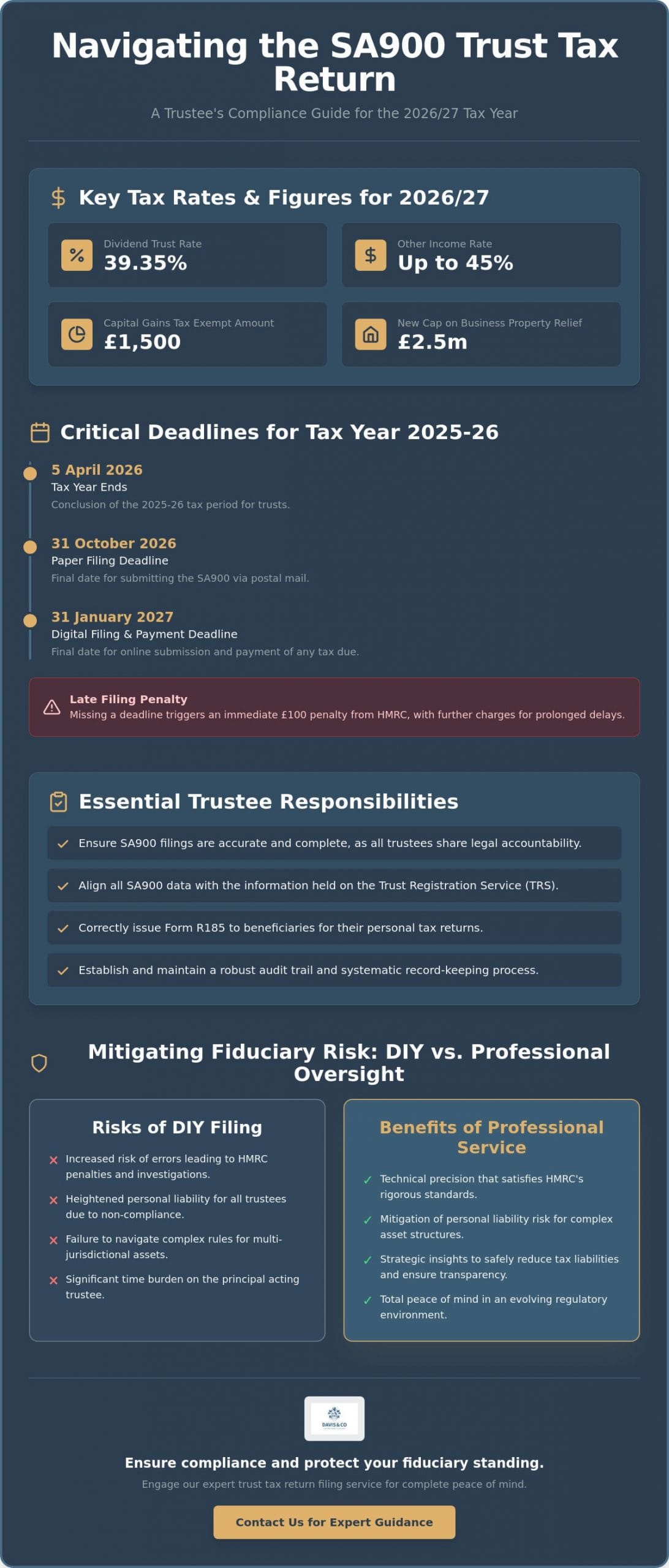

Critical Deadlines for the 2026 Tax Year

Precision in reporting is only valuable if it’s paired with timeliness. For the tax year ending 5 April 2026, the paper filing deadline for the SA900 is 31 October 2026. If you opt for digital submission, which requires HMRC-approved software, the deadline is 31 January 2027. This latter date also serves as the final cutoff for paying any tax liabilities. Missing these milestones triggers an immediate £100 penalty, with further charges accruing for prolonged delays. We help our clients manage these milestones with steady, measured precision.

Essential Trustee Responsibilities and the SA900 Framework

The fiduciary duty of a trustee extends far beyond the oversight of assets. It encompasses a strict legal obligation to ensure the SA900 Trust and Estate Tax Return accurately reflects the financial position of the trust. This responsibility is collective. While a lead trustee may be nominated for administrative correspondence, every individual on the board remains legally accountable for the integrity of the submission. Ensuring these filings are handled with technical precision is why many fiduciaries rely on a comprehensive trust tax return filing service to manage the burden of compliance.

Beyond the filing itself, trustees must manage the distribution of tax-paid income to beneficiaries. This requires the issuance of Form R185, which provides beneficiaries with the necessary data to complete their own personal tax returns. Mistakes in this chain of reporting can lead to significant friction and potential liability. It is essential that the trust’s accounting systems are robust enough to track these distributions against the tax already settled by the trust estate.

Reporting Income and Capital Gains

For the 2026/27 tax year, the fiscal landscape requires a nuanced understanding of varying rates. Dividend income within a trust is taxed at 39.35%, while other income can attract rates of up to 45%. Trustees must also navigate the complexities of Capital Gains Tax, where the annual exempt amount for trusts is £1,500. Whether dealing with rental profits or interest, each stream must be categorized correctly to avoid underpayment. When disposing of trust property, the applicable CGT rates of 18% or 28% must be applied based on the asset type. This requires a level of analytical rigour that generic software often fails to capture.

The Role of Supplementary Pages

The core SA900 form is frequently just the beginning of the compliance journey. Depending on the trust’s activities, supplementary pages such as the SA901 for trading income or the SA903 for UK property are essential. For trusts with a global footprint, foreign income pages are mandatory to disclose international assets and any applicable double taxation relief. The final stage involves the SA950 Trust and Estate Tax Calculation, which serves as the definitive summary of liabilities. Precision at this stage is vital for maintaining the trust’s financial standing. For those seeking to ensure every detail is meticulously addressed, our trust tax services provide the necessary technical oversight.

Professional Oversight vs. DIY: Mitigating Fiduciary Risk

While modern software has simplified the mechanics of data entry, it isn’t a substitute for the intellectual rigour required in fiduciary management. An official SA900 Trust and Estate Tax Return represents more than a series of filled boxes; it’s a legal declaration of a trustee’s stewardship. Software can validate that a field contains data, but it cannot determine if that data reflects a legally sound tax position. Relying solely on automation often leaves trustees exposed to personal liability for negligent or incorrect filings. Our trust tax return filing service bridges this gap, positioning Davis & Co LLP as a strategic partner in mitigating both your professional and personal risks.

Individual trustees are often surprised to learn that they can be held personally liable for the financial consequences of a mismanaged return. HMRC’s penalties for “failure to take reasonable care” can be substantial, and these costs are not always recoverable from the trust assets if the error is deemed negligent. By choosing professional oversight, you’re not just buying a service; you’re securing a robust defence of your fiduciary standing. We ensure that every submission is backed by deep-seated expertise and a thorough understanding of current legislation.

Identifying Strategic Tax Reliefs

Professional advisors look beyond the immediate return to manage the complex interaction between various tax types. When dealing with complex estates, specialized tax advice in the UK ensures that no available relief is overlooked. For example, discretionary trusts often benefit from “Expenses of Management” deductions, which can significantly reduce the tax burden on trust income. Automated systems rarely possess the nuance to apply these reliefs correctly across multi-jurisdictional assets, which can lead to overpayment or missed opportunities for the beneficiaries.

The Value of Professional Gravitas in HMRC Enquiries

HMRC’s approach to enforcement is increasingly sophisticated, yet a professionally prepared return often acts as a deterrent to unnecessary scrutiny. When a Chartered Accountant represents the trust, it signals a commitment to compliance and technical accuracy. This professional gravitas is invaluable if an enquiry does arise, as it ensures the trust’s position is defended with expert authority. Beyond the immediate filing, our involvement provides the security of professional indemnity, offering trustees a layer of protection that DIY software cannot provide. We don’t just file forms; we provide a steady, reliable constant in a volatile regulatory environment.

Strategic Record Keeping and Beneficiary Reporting

Effective trust administration relies on more than just the annual submission of an SA900; it requires a year-round commitment to meticulous documentation. We advocate for a systematic approach where every transaction, whether it’s a minor administrative expense or a major capital distribution, is recorded with its supporting evidence. This isn’t merely an administrative preference. It’s a necessity for maintaining a robust audit trail that justifies every trustee decision. HMRC mandates that trustees keep these records for at least six years from the end of the tax year they relate to. Failing to produce these upon request can lead to penalties and, more importantly, a breakdown in the trust’s legal defence during a formal enquiry.

Utilising a professional trust tax return filing service becomes significantly more efficient when a clear record-keeping framework is already in place. Clear documentation allows for the seamless transition from raw data to a completed return, ensuring that no deductible expenses are overlooked. This level of preparation reflects the quiet excellence required of a high-calibre fiduciary, providing a stable foundation for all future reporting and audits.

Best Practices for Annual Trust Record Management

Success in record management starts with the rigorous categorisation of all financial documents. Trustees should maintain separate files for dividend vouchers, bank statements, and detailed investment reports. We’ve found that digital record-keeping is increasingly essential for modern trust administration. It allows for instant retrieval and provides a secure, timestamped history of all trust activities. When these records are clear and well-organised, the annual filing process is simplified, often leading to a more cost-effective engagement with your professional advisors.

Issuing the R185: Transparency for Beneficiaries

A trustee’s reporting duty isn’t finished once the SA900 is submitted. You must also issue Form R185 (Trust) to every beneficiary who has received a distribution. This form is a critical document that details the beneficiary’s share of the trust’s income and the amount of tax the trust has already paid on their behalf. Beneficiaries rely on this information to claim tax credits or report income on their own personal returns. Timing is vital here. Issuing these statements promptly after the tax year ends ensures beneficiaries can meet their own filing deadlines without unnecessary stress. For “settlor-interested” trusts, additional complexities arise as the tax treatment often defaults back to the settlor, requiring even more precise reporting. For fiduciaries seeking to streamline these complex reporting chains, our bespoke trust tax services offer the technical precision and steady guidance necessary to protect all parties involved.

Bespoke Trust Tax Services from Davis & Co LLP

At Davis & Co LLP, we approach trust administration with a sense of quiet excellence. We understand that trustees aren’t simply looking for a vendor; they require a high-calibre advisor who can navigate the complexities of the 2026 tax landscape with discretion and poise. Our trust tax return filing service is built on this foundation of professional gravitas, ensuring that every SA900 submission is treated as a critical component of your broader fiduciary legacy. We don’t just process data. We apply intellectual rigour to ensure your trust’s financial narrative is accurate, compliant, and strategically sound.

The collaborative process we’ve developed ensures a seamless integration between our specialists and your board of trustees. We act as a steady constant, providing the reassurance needed to manage sensitive commercial and personal matters. By positioning ourselves as strategic partners, we help you navigate the volatile regulatory environment, allowing you to focus on the long-term objectives of the trust and its beneficiaries. This partnership is characterized by a composed authority that makes our clients feel secure and well-advised without sacrificing the necessary distance of a professional expert.

Our Comprehensive Approach to Trust Compliance

We manage the entire compliance lifecycle, from the initial Trust Registration Service (TRS) obligations to the final SA900 filing. Our team possesses deep-seated expertise in handling trusts with diverse asset classes, including complex property portfolios and international holdings. This breadth of experience is essential for maintaining long-term stability. We offer more than just administrative support; we provide the discreet, professional advice required to manage multi-jurisdictional family office requirements. Every disclosure is handled with the precision required in complex analytical thought, ensuring that your reporting remains transparent and beyond reproach.

Why Trustees Choose Davis & Co LLP

Our reputation as a strategic small business accountant is built on a history of success and a commitment to composed partnership. Trustees choose us because we offer a level of sophisticated analysis that automated tools simply cannot replicate. Whether you’re dealing with the 39.35% dividend trust rate or the nuances of the £2.5m cap on Business Property Relief introduced in April 2026, we provide the technical oversight necessary to protect your standing. We invite you to secure your fiduciary position through a professional consultation, ensuring your trust remains a dependable vehicle for future generations.

Securing Your Fiduciary Legacy in an Evolving Tax Landscape

As the 2026 tax year unfolds, the role of a trustee demands a sophisticated balance of administrative precision and strategic foresight. We’ve explored how the granular reporting requirements of the SA900 and the shifting landscape of international tax necessitate more than just basic data entry. By prioritizing meticulous record-keeping and ensuring clear, transparent reporting for beneficiaries, you fulfill your legal duties while protecting the trust’s long-term viability. It’s about more than simple compliance; it’s about the steady stewardship of family wealth across generations.

Our professional trust tax return filing service offers the technical oversight required to manage these responsibilities with absolute confidence. As Chartered Certified Accountants with a heritage dating back to 1901, we specialize in the nuances of international and complex trust tax, providing a bespoke service tailored to the unique needs of high-net-worth family offices. We invite you to secure your trust’s compliance with Davis & Co LLP and benefit from a partnership built on intellectual rigour and quiet excellence. We’re here to ensure your fiduciary standing remains secure in any regulatory environment.

Frequently Asked Questions

What is the SA900 form and who is responsible for filing it?

The SA900 is the definitive Trust and Estate Tax Return used to report all income and capital gains generated within a trust to HMRC. While a principal acting trustee is typically nominated to manage correspondence, the legal responsibility for the accuracy and timeliness of the filing remains collective across the entire board of trustees.

Do I need to register my trust with HMRC even if it has no tax liability?

Yes, almost all UK express trusts must register with the Trust Registration Service (TRS) regardless of whether they have a tax liability. This is a distinct transparency obligation from the annual SA900 filing. Trustees must ensure the TRS record is kept accurate to reflect any changes in beneficiaries or assets to remain compliant.

What are the penalties for late filing of a trust tax return in 2026?

HMRC imposes an immediate £100 penalty if you miss the filing deadlines, which are 31 October 2026 for paper returns and 31 January 2027 for digital submissions. If the return is more than three months late, additional daily penalties apply. Interest is also charged on any tax payments not settled by the January deadline.

Can I file a trust tax return myself using HMRC’s online tools?

HMRC does not provide a bespoke online portal for filing trust tax returns as it does for personal Self Assessment. To file digitally, you must use HMRC-approved commercial software. Trustees who do not wish to use third-party software are restricted to submitting a paper SA900 return by the earlier October deadline.

How does a professional filing service differ from using tax software?

A professional trust tax return filing service provides technical oversight and strategic risk management that software alone cannot offer. While software validates that fields are completed, our specialists apply intellectual rigour to identify management expense reliefs and ensure that complex, multi-jurisdictional assets are reported in a way that protects your fiduciary standing.

What information do I need to provide to my trust’s beneficiaries?

You’re required to provide each beneficiary with a completed Form R185 (Trust) detailing their share of the trust’s income. This form confirms the amount of tax already paid by the trust on that income. It’s an essential document for beneficiaries, as it allows them to correctly report the income on their personal tax returns.

Are there specific tax rules for trusts with international beneficiaries or assets?

Trusts with a global footprint face complex reporting requirements, including the completion of foreign income pages and the application of double taxation treaties. Specific residency tests for the trust itself must be conducted annually. These factors significantly increase the complexity of the SA900 and require a nuanced understanding of international tax planning.

How long should I keep records for a UK trust?

Trustees must maintain all financial records, including bank statements, investment reports, and expense vouchers, for at least six years after the end of the relevant tax year. This period ensures a robust audit trail is available if HMRC initiates an enquiry. Clear record-keeping is the foundation of a stable and defensible trust administration.