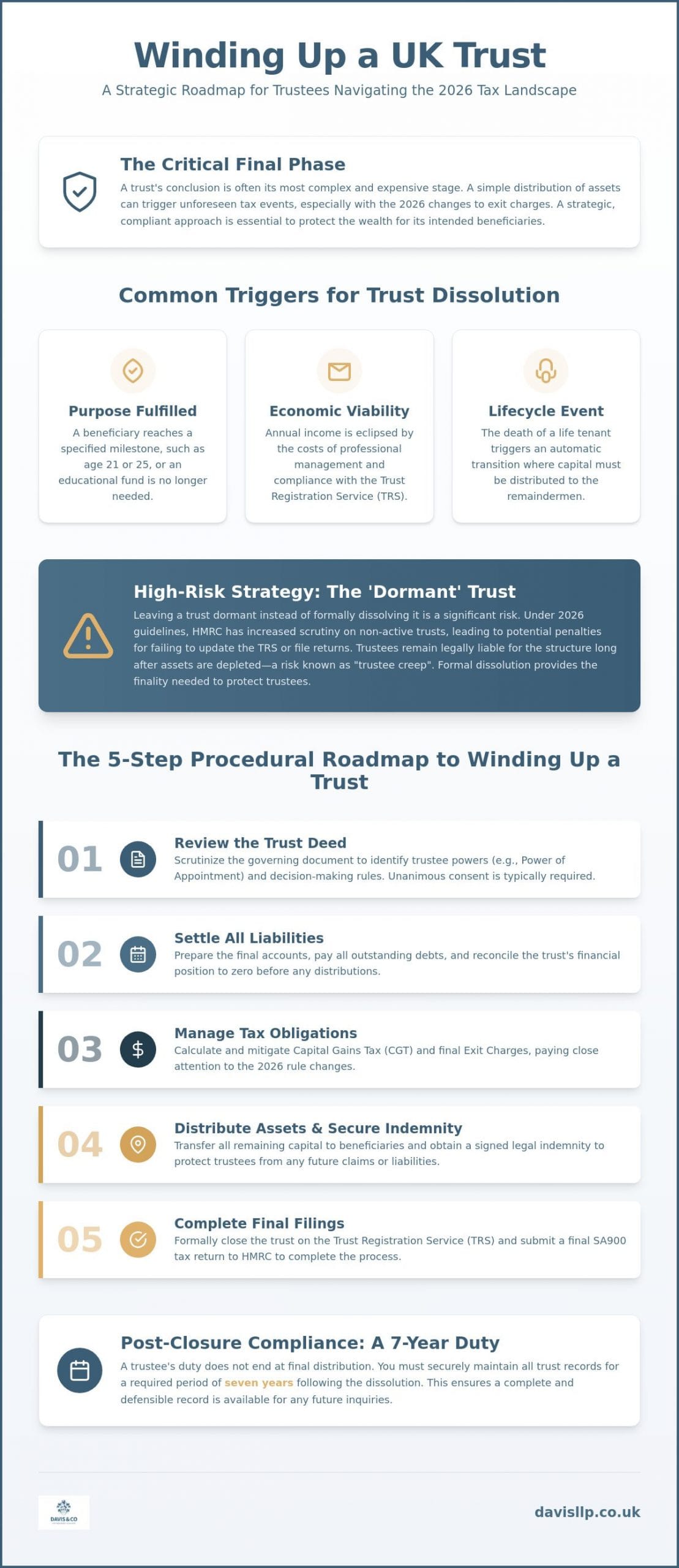

The most expensive phase of a trust’s lifecycle is often not its administration, but its conclusion. When considering how to dissolve a trust uk, many trustees discover too late that a simple distribution of assets can trigger a cascade of unforeseen tax events. With the 2026 changes to the calculation of exit charges now in effect, the margin for error has narrowed significantly. It’s a reality that requires both technical precision and a calm, strategic approach to ensure that the wealth you’ve protected remains intact for its intended recipients.

We understand that the prospect of navigating the Trust Registration Service (TRS) and negotiating potential beneficiary disputes can feel like an overwhelming administrative burden. This guide provides a professional roadmap for winding up a UK trust, focusing on the legal procedures and tax obligations essential for a clean exit in 2026. We’ll examine the specific steps required to minimise Capital Gains Tax liabilities, manage the latest HMRC compliance standards, and achieve a final distribution that respects both the letter of the law and the interests of your beneficiaries.

Key Takeaways

- Identify the legal triggers and governing principles, such as the Saunders v Vautier rule, that dictate a trust’s formal termination.

- Explore the strategic steps on how to dissolve a trust uk while managing the 2026 tax landscape to minimise exit charges and Capital Gains Tax.

- Master the administrative requirements for the Trust Registration Service to ensure a formal and compliant closure of the legal record.

- Implement a disciplined five-step roadmap to reconcile final accounts and settle all outstanding liabilities before the final distribution of capital.

- Secure your professional standing by maintaining accurate trust records for the required seven-year period following the dissolution.

Understanding Trust Dissolution: When the Lifecycle Reaches its Conclusion

Trust dissolution represents the final, formal stage of a trust’s existence. It’s the process by which trustees distribute the remaining capital and income to beneficiaries, effectively terminating the legal entity. While many view a trust as a permanent fixture, it’s governed by a specific lifecycle rooted in English trust law. Dissolving a trust isn’t merely a matter of emptying a bank account; it’s a structured legal exit that requires a clear understanding of the trust deed and current HMRC expectations. Whether a trust ends naturally by reaching its term or is proactively wound up for strategic reasons, the administrative precision required remains the same.

The decision on how to dissolve a trust uk often hinges on the Perpetuities and Accumulations Act 2009. For most trusts created after April 2010, the law sets a maximum lifespan of 125 years. This “perpetuity period” acts as a natural ceiling. However, waiting for a trust to expire by reaching this limit is rarely the most efficient path. In 2026, many trustees are finding that proactive winding up is a more viable strategy. Recent shifts in the tax landscape, specifically the changing treatment of Agricultural and Business Property Reliefs within exit charge calculations, have made the cost of maintaining certain structures higher than the benefit they provide.

Common Triggers for Winding Up a Trust

The most frequent catalyst for dissolution is the simple fulfilment of the trust’s original purpose. This often occurs when a beneficiary reaches a specific age milestone, such as 21 or 25, or when an educational fund is no longer required. Economic viability has also become a primary driver. If the annual income generated is eclipsed by the costs of professional management and the rigorous requirements of the Trust Registration Service (TRS), the trust has likely reached its logical conclusion. Additionally, the death of a life tenant often triggers an automatic transition where the capital must be distributed to remainders.

The Risk of Dormancy vs. Formal Dissolution

Choosing to leave a trust “dormant” rather than formally dissolving it’s a high-risk strategy that we advise against. Under the 2026 TRS guidelines, HMRC has increased scrutiny on non-active trusts. Failing to update the register or file the final SA900 tax return can lead to significant financial penalties. Beyond the regulatory risk, there’s the issue of “trustee creep.” This is a situation where trustees remain legally liable for a structure long after its assets have been depleted. A formal dissolution, backed by a deed of termination, provides the finality needed to protect trustees from future claims or unexpected compliance burdens.

The Legal Framework: Authority, Consent, and the Saunders v Vautier Rule

The trust deed serves as the constitutional foundation for any winding up process. Before taking any action, you must scrutinize this document to identify the specific powers granted to the trustees. In most cases, the authority to end the trust is found within the “Power of Appointment,” which allows trustees to distribute capital to beneficiaries. Understanding how to dissolve a trust uk requires a recognition that trustees must usually act with absolute unanimity. Unless the deed specifically allows for a majority decision, a single dissenting voice can halt the entire dissolution. This collective responsibility ensures that the interests of all parties are considered before the legal structure is dismantled.

Trustees should also prioritize the acquisition of legal indemnities. When you distribute the final assets, you’re essentially closing the door on the trust’s financial life. An indemnity from the beneficiaries protects you against future claims, ensuring that if an unexpected liability arises, the trustees aren’t personally responsible for the settlement. This is a standard but vital layer of protection that we integrate into our Trust Tax Services. It provides a sense of finality and security for those managing the exit.

Applying the Saunders v Vautier Rule in 2026

The rule in Saunders v Vautier remains a powerful tool for beneficiaries. It allows them to bypass the trust’s original terms and demand the distribution of assets, provided they are all of “full age” and “sound mind.” While the general age of majority is 18, many trust deeds specify 21 as the age of entitlement. In 2026, the specific wording of your deed still overrides general rules, meaning trustees must be cautious before agreeing to an early collapse. The rule also fails if there are “unascertained” beneficiaries, such as unborn grandchildren, who cannot yet give consent to the dissolution.

Discretionary vs. Bare Trusts: Different Exit Paths

The complexity of the exit path depends heavily on the trust structure. Bare trusts are the most straightforward. Since beneficiaries have an absolute right to both capital and income, the dissolution is often a matter of administrative transfer. Discretionary trusts are more involved. They require a formal “Deed of Appointment” to finalize the wind-up. This document records the trustees’ decision and provides a clear audit trail for HMRC regarding Trusts and taxes. Managing the “class of beneficiaries” in these cases is essential. You must ensure all potential claimants are accounted for to prevent legal challenges after the assets have been dispersed.

Navigating the Tax Landscape: Mitigating Exit Charges and CGT

Dissolving a trust is a significant tax event, often triggering the “Relevant Property Regime” which mandates periodic charges every ten years and exit charges whenever capital is distributed from discretionary structures. Determining how to dissolve a trust uk requires a meticulous review of the inheritance tax (IHT) framework. For 2026, the maximum IHT exit charge remains 6%, but the calculation has become more complex. New regulations now dictate that Agricultural Property Relief (APR) and Business Property Relief (BPR) are ignored when establishing the effective rate for exit charges. This change means that assets previously shielded may now contribute to a higher tax bill upon distribution.

Beyond inheritance tax, trustees must account for Capital Gains Tax (CGT). HMRC treats the transfer of assets to a beneficiary as a disposal at current market value. For the 2026-2027 tax year, the CGT rate for trustees is 24%, with a limited annual exempt amount of just £1,500. When trustees evaluate how to dissolve a trust uk, they must weigh these immediate costs against the long term benefits of winding up. Before finalizing any tax filings, ensure your records are accurate on the central portal to Register a trust as a trustee, as HMRC cross-references these details during the dissolution phase to ensure full compliance.

Mitigation Strategies: Hold-over Relief (Section 260)

Section 260 hold-over relief is perhaps the most vital tool for preserving capital during a wind-up. This relief allows the CGT liability to be deferred and effectively passed to the beneficiary, who takes on the trustees’ original base cost for the asset. It’s typically available when the distribution itself triggers an IHT charge, even if that charge is zero because the value falls within the £325,000 nil-rate band. By utilizing this strategy, trustees can avoid an immediate 24% tax hit, though the beneficiary will eventually face the tax when they sell the asset. It’s a sophisticated way to maintain the trust’s value during the transition.

Cross-Border and International Considerations

The tax landscape grows significantly more complex when dealing with non-UK resident beneficiaries. In 2026, distributions to individuals outside the UK may lead to immediate tax liabilities that cannot be deferred through standard UK reliefs. Managing offshore assets also requires rigorous reporting to avoid double taxation or penalties for non-disclosure. For those managing complex multi-jurisdictional structures, our guide to International Tax Planning offers specific insights into aligning your exit strategy with global tax obligations. We ensure that the human and organizational impact of these cross-border transfers is managed with the necessary discretion and expertise.

The 5-Step Procedural Roadmap to Winding Up a Trust

Executing a successful exit requires more than just a consensus among trustees; it demands a disciplined sequence of administrative actions. When we advise clients on how to dissolve a trust uk, we emphasize that the order of operations is as critical as the legal authority behind them. Skipping a step, particularly regarding debt reconciliation or tax filings, can leave trustees exposed to personal liability long after the assets have been distributed. This structured roadmap ensures that every regulatory and financial obligation is met with the necessary precision.

- Step 1: Review and Opinion. Re-examine the trust deed and obtain a formal legal or tax opinion to confirm the trustees’ powers and identify any potential “unascertained” beneficiaries.

- Step 2: Financial Reconciliation. Prepare final accounts and settle all outstanding liabilities. This includes professional fees, management expenses, and any lingering tax debts.

- Step 3: Legal Execution. Draft and execute the Deed of Appointment or the relevant legal instrument required to vest the assets in the beneficiaries.

- Step 4: Asset Transfer. Distribute the assets according to the deed while obtaining signed receipts and formal indemnities from every recipient.

- Step 5: Compliance Closure. File the final HMRC reports and formally close the record on the Trust Registration Service (TRS).

If you require assistance with the technicalities of these final filings, our specialists provide comprehensive Trust Tax Services to ensure your exit is both clean and compliant.

Preparing Final Accounts and Tax Returns

The final SA900 Trust and Estate tax return is the cornerstone of the dissolution process. It’s not enough to simply stop filing; you must actively notify HMRC that the trust has ceased to exist. For the 2026 tax year, record-keeping standards have shifted toward digital-first documentation. Trustees must ensure that “income” and “capital” distributions are accurately coded. This precision allows for the correct issuance of R185 tax certificates, which beneficiaries will need for their own personal tax reporting. Without these certificates, beneficiaries may struggle to justify the sudden influx of wealth to HMRC.

The Asset Distribution Phase

The logistics of the distribution phase vary depending on the asset class. While cash transfers are relatively straightforward, transferring property or private company shares requires a formal change of title at HM Land Registry or through a stock transfer form. We recommend recording the final decision in a formal Trustee Resolution. This document serves as a permanent record of the trustees’ intent and the valuation of assets at the point of exit. It’s the final piece of the puzzle in understanding how to dissolve a trust uk while maintaining an impeccable audit trail.

Strategic Post-Closure Compliance: TRS and Final Filings

Finality in trust administration is achieved only when the regulatory slate is wiped clean. While the physical distribution of assets marks the end of the trust’s practical utility, the legal entity persists in the eyes of HMRC until the Trust Registration Service (TRS) record is formally closed. Understanding how to dissolve a trust uk involves recognizing that an “active” status on the TRS, even for an empty trust, can trigger automated compliance flags. We ensure that this final administrative hurdle is cleared with the same level of discretion and precision applied to the earlier distribution phases. Closing the record isn’t a mere formality; it’s a distinct legal requirement that signals the end of the trustees’ reporting obligations.

Once the trust is terminated, trustees must maintain a robust archive. We advise that all trust documents, including the original deed, deeds of appointment, and final accounts, be retained for at least seven years after the date of dissolution. This period aligns with standard HMRC look-back windows and protects trustees should any historical tax queries arise. For those transitioning from trust structures to other forms of wealth management, our guide to Expert Tax Advice in the UK provides a broader perspective on long-term inheritance planning. Final communication with beneficiaries is equally vital. Providing them with a comprehensive summary of their distributions ensures they have the necessary data for their personal tax returns, preventing future disputes and ensuring all parties are aligned before the professional relationship is concluded.

Closing the TRS Record in 2026

To formally terminate the record, trustees or their authorized agents must log into the Government Gateway and declare the trust as “terminated.” This process requires the exact date of dissolution, which must match the date recorded on the final Deed of Appointment. A common error in the closing process is failing to reconcile the final tax return date with the TRS closure date, which can trigger HMRC queries. We recommend a final verification of all registered data to ensure the concluding “snapshot” of the trust is accurate, as this remains the permanent digital record of the entity’s existence.

The Role of Professional Advisors in Final Closure

The transition from active management to final dissolution is a high-stakes period where professional oversight is invaluable. At Davis & Co LLP, we guide our clients through each procedural nuance, providing the reassurance of a clean break. A professional sign-off or certificate of closure offers trustees peace of mind, confirming that all liabilities are settled and all regulatory filings are complete. If you are ready to conclude your trust’s lifecycle with confidence, speak with our Trust Tax specialists today to begin your winding-up process.

Securing a Compliant and Orderly Exit for Your Trust

Successfully winding up a trust is a multi-layered process that requires a meticulous alignment of legal authority, tax mitigation, and administrative finality. By prioritizing a formal deed of dissolution and strategically utilizing hold-over reliefs, you can protect the capital intended for your beneficiaries from unnecessary erosion. When determining how to dissolve a trust uk, the objective is always a clean break that leaves no lingering liabilities or unresolved reporting requirements for the trustees. It’s a significant undertaking that benefits from a steady, measured approach to compliance.

As Chartered Certified Accountants since 1901, we provide the deep-seated expertise necessary to navigate the most complex international and trust tax planning scenarios. Our discreet, partner-led service is specifically designed for family offices and individuals who require a sophisticated level of professional gravitas and intellectual rigour. Contact Davis & Co LLP for Expert Trust Dissolution Advice to ensure your final distribution is managed with absolute precision. We look forward to partnering with you to achieve a secure and compliant transition for your assets.

Frequently Asked Questions

How long does it typically take to dissolve a trust in the UK?

The dissolution process typically spans between six and twelve months. This timeframe is necessary to prepare final accounts, settle outstanding liabilities with HMRC, and execute the formal transfer of assets. If the trust holds complex or illiquid assets, such as private company shares or commercial property, the process may take longer to accommodate formal valuations and title registrations.

Can a trust be dissolved if one beneficiary disagrees?

Trustees can generally proceed with dissolution if they are exercising a discretionary power of appointment granted by the trust deed, even without unanimous beneficiary consent. However, if the termination is being driven by the beneficiaries themselves under the Saunders v Vautier rule, every beneficiary must be of full age and capacity and must agree to the dissolution. Disagreements in these circumstances can stall the process indefinitely.

What are the specific HMRC forms required to close a trust in 2026?

Trustees must submit a final SA900 Trust and Estate tax return to notify HMRC of the trust’s cessation. Additionally, an IHT100 form is required to report any inheritance tax exit charges due upon the distribution of capital. To ensure beneficiaries can correctly report their receipts, trustees must also issue R185 (Tax Income) or similar certificates. Accurate filing is a cornerstone of how to dissolve a trust uk while maintaining full compliance.

Is there a minimum asset value below which a trust should be dissolved?

There’s no statutory minimum value, but the decision is usually driven by economic viability. When the annual costs of professional fees, tax filings, and Trust Registration Service (TRS) compliance exceed the trust’s income or the benefit it provides to beneficiaries, dissolution becomes the logical choice. We often advise a review of trust viability if the administrative burden feels disproportionate to the capital protected.

Do I have to pay Capital Gains Tax when I close a trust?

Closing a trust usually triggers a Capital Gains Tax (CGT) event because the transfer of assets to beneficiaries is treated as a disposal at market value. For the 2026-2027 tax year, the trustee CGT rate is 24% on gains above the £1,500 annual exempt amount. However, many trustees avoid an immediate tax bill by utilizing Section 260 hold-over relief, which defers the gain until the beneficiary eventually sells the asset.

What happens to the Trust Registration Service (TRS) record once a trust is closed?

The TRS record must be formally updated to reflect that the trust has been terminated. This action provides a clear digital audit trail for HMRC and ensures that the trust is no longer flagged for annual compliance updates. While the record remains as a historical entry within the Government Gateway, marking it as closed effectively ends the trustees’ ongoing reporting obligations under the 2026 guidelines.

Can I dissolve a trust myself or do I need a solicitor and accountant?

While DIY dissolution is technically possible, it’s rarely advisable due to the significant personal liability trustees carry. Accountants and legal professionals provide the precision needed to calculate complex exit charges and draft the necessary indemnities. Given the high stakes of 2026 tax regulations, professional oversight ensures that the wind-up is final and that no lingering tax debts can be traced back to the trustees personally.

What is an exit charge, and how is it calculated in 2026?

An exit charge is an inheritance tax levy, capped at 6%, that applies when capital is distributed from a discretionary trust. In 2026, the calculation has become more stringent because Agricultural Property Relief (APR) and Business Property Relief (BPR) are now ignored when determining the effective rate of the charge. This change requires a more detailed analysis of the trust’s historical value to ensure the correct tax is paid. Mastering these calculations is essential for anyone learning how to dissolve a trust uk without incurring HMRC penalties.