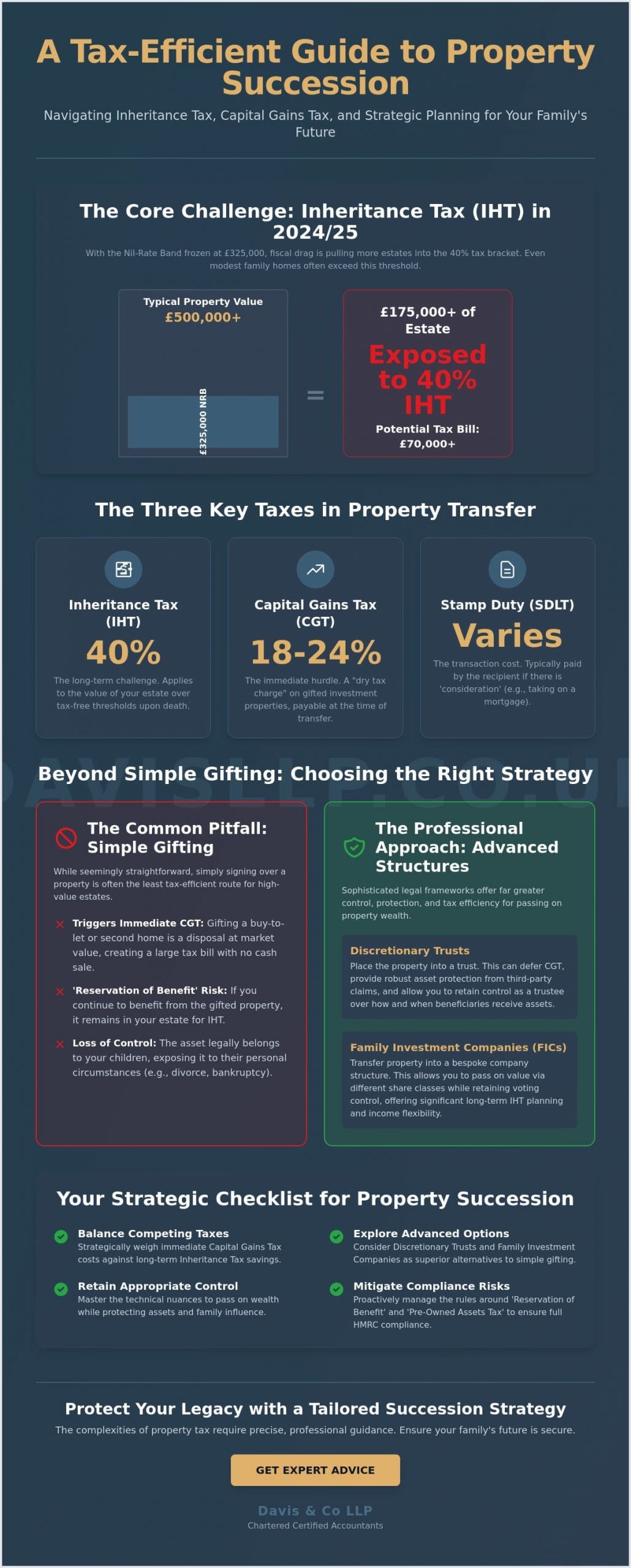

With the Inheritance Tax nil-rate band frozen at £325,000 until at least 2030, more than £8 billion was paid in IHT during the 2024/25 tax year. This persistent fiscal drag means that even modest family homes now frequently exceed tax-free thresholds, leaving many to wonder how to pass property to children tax efficiently without triggering a 40% charge on their estate. We recognise the apprehension that comes with such high stakes; you’ve spent a lifetime building your portfolio, and the prospect of double taxation through Capital Gains Tax and Inheritance Tax feels like an unnecessary penalty on your legacy.

This guide provides a clear roadmap to help you move beyond the uncertainty of the 7-year rule and the fear of losing control over your assets. You’ll discover the most effective legal frameworks and tax-planning strategies to transfer property wealth while minimising HMRC liabilities. We’ll explore the integration of the Residence Nil-Rate Band, the strategic use of Trust Tax Services, and the role of professional Property Accounting in protecting your family’s future. This overview ensures your succession plan is handled with the precision and discretion your legacy deserves.

Key Takeaways

- Balance immediate Capital Gains Tax disposals against long-term Inheritance Tax savings to ensure a seamless transition of property wealth.

- Explore the strategic advantages of Discretionary Trusts and Family Investment Companies as sophisticated alternatives to simple lifetime gifting.

- Master the technical nuances of how to pass property to children tax efficiently while retaining appropriate levels of control and asset protection.

- Recognise and mitigate the risks associated with ‘Reservation of Benefit’ rules and ‘Pre-Owned Assets Tax’ to maintain full HMRC compliance.

- Align your property succession with a comprehensive international tax planning framework to address the complexities of modern, globalised family estates.

Understanding the Strategic Landscape of Property Succession in 2026

Property succession in 2026 represents a sophisticated alignment of legal ownership and fiscal responsibility. It’s the process of transitioning real estate assets to the next generation while adhering to the stringent requirements of the UK tax system. Many property owners initially consider simple gifting as their primary route. However, for high-value estates, this approach is often the least efficient path. Gifting a buy-to-let property, for instance, is treated as a disposal at market value, which can trigger an immediate Capital Gains Tax bill even though no cash has changed hands. We view this transition not as a single transaction, but as a long-term wealth preservation move.

Effective planning moves beyond the transactional. It treats intergenerational wealth transfer as a professional discipline that balances three core objectives: tax mitigation, robust asset protection, and the maintenance of family influence over the portfolio’s future. Success requires a proactive strategy that addresses how to pass property to children tax efficiently without compromising the financial security of the parents. This involves a deep understanding of the legal landscape and the various tax triggers that occur during a transfer.

Why 2026 is a Pivotal Year for Estate Planning

The current fiscal environment has made property succession more challenging than in previous decades. With the Nil-Rate Band frozen at £325,000 until at least 2030, a phenomenon known as fiscal drag is pulling more estates into the 40% tax bracket. As property valuations continue to fluctuate, the gap between the frozen thresholds and actual market values widens. Understanding the UK Inheritance Tax rules is essential for any homeowner. Early intervention is particularly critical in a high-interest-rate environment, where the cost of refinancing or managing debt within a succession plan can significantly impact the net value passed to beneficiaries.

Identifying Your Primary Succession Goals

A strategic roadmap begins with a clear distinction between the family home and investment portfolios. Passing on a main residence involves specific reliefs, such as the Residence Nil-Rate Band, but it also carries the risk of “reservation of benefit” if parents intend to remain in the property. We often see clients struggling to balance their own need for long-term security with a child’s immediate requirement for a residence. Beyond the tax calculations, you must also evaluate the readiness of your beneficiaries. Managing a significant property asset requires a level of financial literacy that not every child possesses at the time of the transfer. Our approach focuses on the technicalities of how to pass property to children tax efficiently while ensuring the legal structure remains resilient against third-party claims.

The Interplay of UK Taxes: Navigating IHT, CGT, and SDLT

The strategic challenge of property succession lies in the friction between immediate and deferred tax liabilities. Many property owners focus exclusively on Inheritance Tax, yet the most significant hurdle often arrives the moment a gift is made. When you transfer a property that isn’t your primary residence, HMRC views this as a “dry tax charge.” You may owe a substantial amount in Capital Gains Tax despite receiving no cash from the transaction. Balancing these competing pressures requires a holistic view of your estate rather than treating each tax in isolation.

We often observe that the transition of a buy-to-let portfolio requires more than just a change in title deeds; it necessitates a comprehensive review of your Personal Tax Services to ensure the transfer doesn’t inadvertently create a liquidity crisis. A successful strategy must account for the immediate impact on your cash flow while securing the long-term tax-free status of the asset for your children.

Capital Gains Tax: The Immediate Hurdle

For the 2026/27 tax year, the Capital Gains Tax (CGT) rates for residential property are set at 18% for basic rate taxpayers and 24% for those in higher or additional bands. While Private Residence Relief (PRR) typically exempts your main home from these charges, any secondary property or investment asset is fully exposed. A market value disposal occurs when an asset is gifted or transferred at less than its full worth, requiring the donor to calculate Capital Gains Tax based on the property’s current open-market valuation rather than the actual price paid by the recipient. With the annual exempt amount limited to £3,000, even modest gains can lead to significant tax bills during the succession process.

Inheritance Tax and the Seven-Year Rule

While CGT represents an immediate cost, Inheritance Tax (IHT) remains a contingent liability. Most lifetime gifts of property are classified as Potentially Exempt Transfers (PETs). These assets only leave your estate entirely if you survive for seven years after the gift. According to Official IHT guidance, if death occurs between three and seven years, taper relief may reduce the tax rate on a sliding scale. Specifically, the 40% rate is reduced by 20% for each year beyond the third year of the gift. To manage the financial risk during this seven-year window, many families utilise “Gift Inter Vivos” insurance, which provides a payout to cover the potential IHT bill if the donor passes away prematurely.

Beyond these primary taxes, you must consider Stamp Duty Land Tax (SDLT). If a child takes over an existing mortgage as part of the transfer, the value of that debt is considered “consideration” and may trigger an SDLT charge based on standard residential rates. Additionally, if the property continues to generate rental yield, that income becomes the child’s liability. This shift in income can push a beneficiary into a higher tax bracket, making professional property accounting essential to preserve the net yield for the next generation.

Beyond Simple Gifting: Trusts vs. Family Investment Companies

While lifetime gifts are a traditional route for property succession, they often lack the control and protection required for substantial family estates. When dealing with high-value residences or multi-property portfolios, we look toward more sophisticated vehicles that separate legal title from beneficial enjoyment. These structures allow you to address the core challenge of how to pass property to children tax efficiently while shielding your legacy from external risks. The choice between a trust and a corporate structure depends heavily on the scale of your assets and the specific needs of your beneficiaries.

We believe that a well-structured succession plan should act as a fortress. It’s not just about the initial transfer; it’s about ensuring the property remains a family asset for decades. By utilising our Trust Tax Services or establishing a corporate vehicle, you can manage the timing of wealth distribution and protect your children from the complexities of direct ownership before they’re ready.

Using Trusts for Flexibility and Protection

Discretionary trusts offer a unique layer of security, ensuring that property remains within the family even in the event of a child’s future divorce or bankruptcy. Since the trustees maintain control over the assets, the property isn’t considered part of a child’s personal wealth for most third-party claims. Under the relevant property regime, these trusts are subject to periodic IHT charges every ten years, yet the trade-off is the ability to manage exactly when a child accesses the capital. Navigating the UK Inheritance Tax rules is vital here, as transfers into a discretionary trust may trigger an immediate 20% entry charge if the value exceeds your available nil-rate band. For simpler requirements, a Bare Trust might suffice, though it grants the child absolute rights to the asset at age 18.

The Rise of the Family Investment Company (FIC)

A Family Investment Company (FIC) has become a preferred corporate alternative for large property portfolios. By using multiple share classes, we can effectively separate voting rights from capital growth. Parents typically hold voting shares to maintain control over the company’s direction, while children hold “growth shares” that capture the future appreciation of the property. This is a masterclass in how to pass property to children tax efficiently, as the value of the children’s shares grows outside of the parents’ taxable estate. Within a FIC, rental income is subject to corporation tax rather than the higher personal income tax rates, allowing for more efficient reinvestment. Our Property Accounting experts note that while FICs involve higher administrative costs, the ability to deduct mortgage interest and business expenses often results in superior long-term tax savings. Transitioning existing properties into a FIC requires careful management of “incorporation relief” to avoid immediate Capital Gains Tax liabilities.

Avoiding the ‘Reservation of Benefit’ and Other Compliance Pitfalls

The technical elegance of a trust or a corporate structure is only as effective as its ongoing compliance. HMRC maintains a rigorous focus on the substance of property transfers, ensuring that a gift is genuine and that the donor has truly divested themselves of the asset’s benefits. If you retain any form of enjoyment or use of the property after the transfer, you risk falling into the “Gift with Reservation of Benefit” (GWRB) trap. This effectively nullifies the transfer for Inheritance Tax purposes, keeping the property’s full value within your taxable estate regardless of how many years have passed.

Beyond GWRB, the Pre-Owned Assets Tax (POAT) serves as a secondary line of defence for the revenue. POAT is an annual income tax charge levied on individuals who continue to benefit from an asset they previously owned or provided the funding for, even if they’ve successfully navigated the GWRB rules. This tax is calculated based on the “benefit” received, such as the rental value of the property you’re occupying. Avoiding these overlapping regimes requires meticulous planning and a clear understanding of how to pass property to children tax efficiently without triggering a perpetual tax leak.

Attempting to “sell” a property to a child at a significant undervalue often creates more problems than it solves. Such a transaction is viewed as a “gift into a settlement” or a “gift of value,” triggering the same Capital Gains Tax disposals discussed in earlier sections while potentially complicating the child’s future mortgage applications or legal standing. If you’re concerned about the long-term integrity of your estate, our Personal Tax Services can provide the necessary oversight to ensure your strategy remains compliant with evolving HMRC standards.

The Reality of Living in a Gifted Property

If you intend to remain in a property after gifting it to your children, you must pay a full market-rate rent to the new owners to avoid IHT inclusion. This isn’t a casual arrangement; it requires a formal, arm’s length rental agreement and regular evidence that the rent is being paid at current market levels. The administrative burden of documenting these payments is significant, as any shortfall could be interpreted as a retained benefit. In the context of GWRB compliance, full consideration is defined as the payment of a market-level rent that would reasonably be expected in an open-market transaction between unconnected parties.

Mitigating the Risk of Deliberate Deprivation of Assets

Local authorities possess broad powers to scrutinise property transfers when assessing an individual’s liability for long-term care home fees. If a transfer is deemed a “deliberate deprivation of assets,” the council can treat the property as if you still own it when calculating your contribution to care costs. Unlike the 7-year rule for Inheritance Tax, there’s no fixed statutory time limit for how far back a local authority can look. Strategic planning for care involves balancing your desire to protect the family home with the legal requirement to be transparent about your financial position. We focus on how to pass property to children tax efficiently by timing transfers when care needs aren’t foreseeable, ensuring the move is part of a broader, documented wealth preservation strategy rather than a reactive measure.

Implementing a Tailored Succession Strategy with Davis & Co LLP

Succession planning is rarely a static exercise. At Davis & Co LLP, we approach the question of how to pass property to children tax efficiently by situating it within your broader financial narrative. Our methodology transcends simple compliance; it involves a meticulous integration of your domestic assets into a wider international tax planning framework. This is essential for families whose interests or beneficiaries span multiple jurisdictions. We understand that the interplay between UK resident status and foreign property holdings requires a level of nuance that generic advice cannot provide.

Complex family dynamics often necessitate expert tax advice in the UK that balances technical precision with emotional intelligence. We provide coordinated modelling that accounts for Capital Gains Tax, Inheritance Tax, and potential corporation tax liabilities simultaneously. This multi-dimensional analysis ensures that a solution designed to mitigate IHT doesn’t inadvertently trigger an unmanageable CGT event. We maintain a steady, measured rhythm in our delivery, ensuring you feel secure and well-advised throughout the process.

The Davis & Co LLP Professional Partnership Model

Our relationship with clients is built on the principle of composed partnership. We move beyond transactional advice to act as a long-term strategic partner for your family’s estate. This involves working in tandem with legal professionals to ensure that deed transfers and trust documentation align perfectly with the tax structures we’ve designed. We conduct regular reviews to adapt your strategy to future legislative shifts in the UK. This proactive stance ensures your legacy remains protected against the volatility of the fiscal environment, providing a sense of stability in an often unpredictable market.

Next Steps for Your Family’s Wealth Preservation

Beginning the journey toward an efficient transfer starts with a comprehensive property portfolio audit. We require initial documentation including current valuations, acquisition costs, and details of any existing debt or ownership structures. From this foundation, we can establish a clear timeline for implementing trust or corporate structures. This process typically spans several months to ensure every detail is addressed with the necessary rigour. Determining how to pass property to children tax efficiently is a significant undertaking that requires the discretion and professional gravitas our firm is known for. We invite you to experience a partnership where quiet excellence and deep expertise are the standard for your family’s future.

Securing Your Family’s Real Estate Legacy

Transitioning property wealth in 2026 demands a shift from transactional gifting to long-term strategic alignment. We’ve examined the necessity of managing the immediate dry tax charges of Capital Gains Tax alongside the complexities of the seven-year Inheritance Tax window. By utilizing sophisticated vehicles such as Family Investment Companies or Discretionary Trusts, you can protect your assets from third-party claims while maintaining the family’s influence over the portfolio. Adhering to these regulations is the only way to ensure you understand how to pass property to children tax efficiently without compromising your own financial security.

As Chartered Certified Accountants with over 120 years of heritage, we specialise in international tax planning and bespoke trust tax services for high-net-worth property investors. Our approach is highly individualised. We invite you to request a strategic consultation with our personal tax specialists to begin modelling your tailored succession plan. With the right professional oversight, you can transform a complex fiscal challenge into a stable and enduring legacy for the next generation.

Frequently Asked Questions

Can I gift my house to my children and still live in it?

You can gift your home while remaining in residence, provided you pay a full market rent to your children. If you don’t pay rent, HMRC views this as a “Gift with Reservation of Benefit,” meaning the property remains part of your estate for Inheritance Tax purposes. This arrangement requires meticulous documentation to prove that the tenancy is handled on a strictly commercial basis.

What is the 7-year rule for gifting property in the UK?

The seven-year rule dictates that most property gifts are classified as Potentially Exempt Transfers. If you survive for seven years after making the gift, its value is entirely removed from your estate for Inheritance Tax calculations. This is a primary pillar of how to pass property to children tax efficiently, though it requires early intervention to ensure the timeline is met before any health changes occur.

Do children have to pay Stamp Duty on a gifted property?

Stamp Duty Land Tax is usually not payable on a property gifted for no monetary consideration. However, if your children take over an existing mortgage as part of the transfer, the value of that outstanding debt is treated as “consideration” by HMRC. If this debt exceeds the current 2026 Stamp Duty thresholds, a tax charge will apply based on standard residential rates.

Is it better to gift property now or leave it in a will?

The decision depends on whether you wish to prioritise Capital Gains Tax or Inheritance Tax mitigation. Gifting now starts the seven-year clock for IHT but often triggers an immediate CGT bill based on the property’s current market value. Leaving property in a will provides a “step-up” in base value for the beneficiaries, which can eliminate CGT on previous growth, but it exposes the asset to a 40% IHT charge.

How much Capital Gains Tax will I pay when gifting a second home?

From 6 April 2026, CGT rates on residential property are 18% for basic rate taxpayers and 24% for those in higher or additional rate bands. You’ll pay tax on the difference between your original purchase price and the market value at the date of the gift. The annual exempt amount for the 2026/27 tax year is £3,000, which offers very limited relief for high-value property gains.

Can I use a trust to pass property to my children tax-efficiently?

Trusts are an excellent vehicle for maintaining control while transitioning wealth to the next generation. We often use our Trust Tax Services to manage properties for younger children or to protect assets from external claims such as divorce. While they offer protection, trusts are subject to their own tax regime, including potential entry charges and periodic ten-year charges if the value exceeds your available nil-rate band.

What happens if I die within 7 years of gifting a property?

If death occurs within seven years, the gift’s value is brought back into your estate for Inheritance Tax purposes. Taper relief can reduce the tax due if you survive at least three years after the gift was made. The tax rate on the gift reduces on a sliding scale from 40% down to 8% by the sixth year, providing a partial benefit even if the full seven-year term isn’t reached.

How does the Residence Nil Rate Band work with property gifts?

The Residence Nil Rate Band provides an additional £175,000 allowance when passing a main residence to direct descendants. If you gift your home during your lifetime, you can still benefit from this allowance through “downsizing relief” provisions. This ensures you can still understand how to pass property to children tax efficiently without losing the tax-free threshold, which can reach £1 million for married couples.