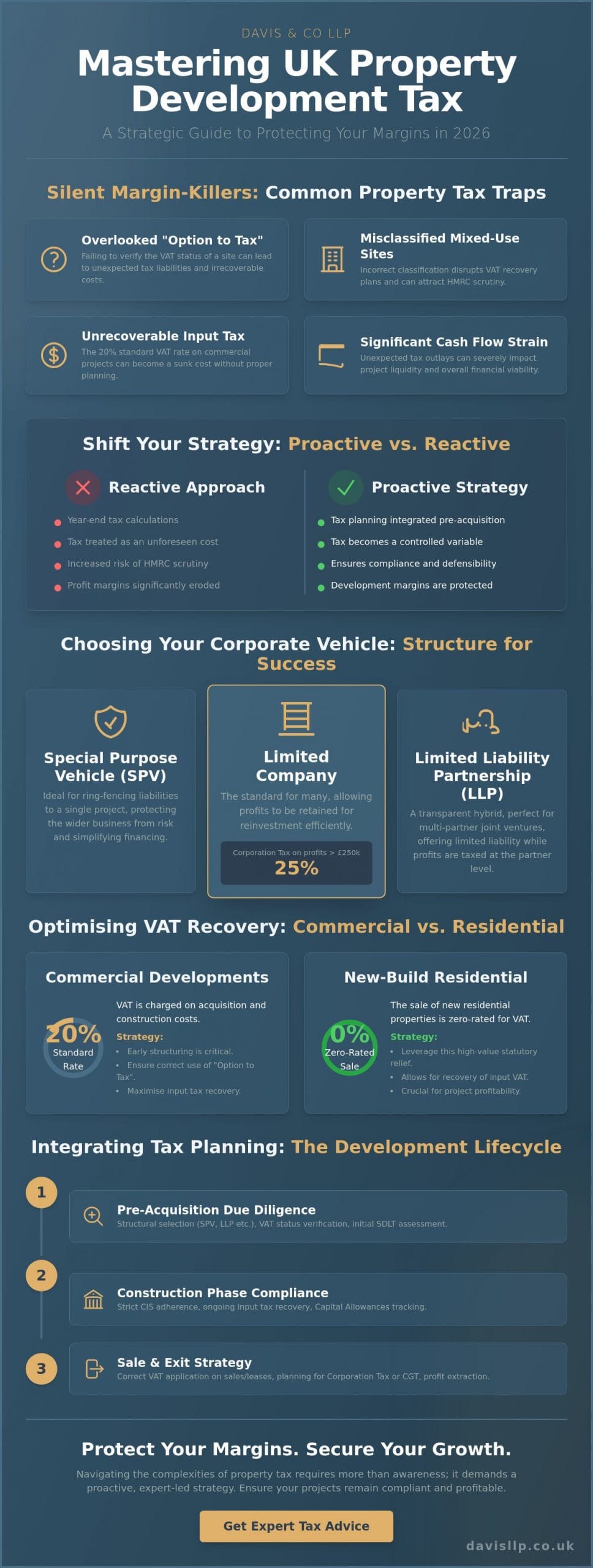

Could an overlooked “option to tax” or a misclassified mixed-use site be the silent margin-killer in your 2026 development pipeline? It’s a reality that property development is as much a feat of fiscal precision as it is of physical construction, yet even seasoned professionals find themselves ensnared by unexpected VAT “traps” during acquisitions. These oversights often lead to significant cash flow strain from unrecoverable input tax, particularly when navigating the 20% standard rate on commercial builds or the nuanced complexities of VAT on property transactions uk.

We believe that protecting your commercial viability requires more than just awareness; it demands a proactive strategy. This guide provides the clarity needed to master these transactional taxes, ensuring you can protect your development margins with quiet authority. We will examine how to optimize VAT recovery through the strategic use of Special Purpose Vehicles (SPVs) and identify high-value statutory reliefs, such as the zero-rate for new residential sales, to ensure your projects remain both compliant and profitable in this shifting regulatory landscape.

Key Takeaways

- Understand how to shift from reactive tax calculations to proactive planning that secures your development margins against rigorous HMRC scrutiny.

- Evaluate the strategic advantages of Special Purpose Vehicles (SPVs) and LLPs to ring-fence liabilities and optimize your corporate structure for long-term growth.

- Learn to identify high-value SDLT reliefs and ensure maximum recovery of VAT on property transactions uk by correctly navigating the 0% rating for new residential builds.

- Discover how to leverage statutory incentives like Land Remediation Relief and Capital Allowances to significantly reduce the net cost of commercial development.

- Master the integration of tax due diligence throughout the entire development life cycle, from pre-acquisition structural selection to construction phase compliance.

Navigating the UK Property Development Tax Landscape in 2026

Effective property development tax planning is far more than a year-end administrative exercise. In the current fiscal climate, it’s the proactive arrangement of VAT and Stamp Duty Land Tax (SDLT) liabilities to ensure that tax is a controlled variable rather than an unforeseen cost. As we move through 2026, HMRC has adopted a significantly more robust stance toward aggressive tax positions, placing a premium on transparency and commercial substance. For developers with high turnover, the accruals basis of accounting has become the operational standard, reflecting the need for precise financial reporting that aligns with the latest Making Tax Digital (MTD) mandates. Integrating professional tax advice before the site acquisition phase is no longer optional; it’s a fundamental requirement for protecting your development margins.

The complexity of UK Value-Added Tax (VAT) often creates friction during the early stages of a project. Failing to verify the VAT status of a site or the validity of an “option to tax” can lead to irrecoverable costs that immediately erode profitability. We see many developers struggling with the 20% standard rate on commercial acquisitions when early structuring could have mitigated the impact. Success in 2026 requires a steady, deliberate approach to VAT on property transactions uk, where every tax implication is mapped against the project’s long-term commercial viability.

The Distinction Between Trading and Investment

Determining whether a project falls under the scope of Corporation Tax on trading profits or Capital Gains Tax (CGT) requires a rigorous analysis of the “badges of trade.” HMRC scrutinizes the frequency of transactions, the methods of funding, and the nature of the asset to define the tax treatment. Your intent at the moment of acquisition dictates the entire VAT recovery trajectory; if the primary purpose is a quick resale, the project is viewed as a trading venture. For a 2026 HMRC audit, a clearly documented board minute or investment memorandum serves as the primary evidence that your “intent” aligns with your reported tax treatment, preventing costly reclassifications during the life of the development.

HMRC Compliance and the 2026 Regulatory Shift

Transparency requirements have intensified, particularly for developers utilizing international funding structures. HMRC now expects a granular level of detail regarding the source of funds and the ultimate beneficial ownership of development vehicles. Securing expert tax advice in the UK provides a necessary buffer against these compliance risks, ensuring that your reporting is both accurate and defensible. Furthermore, the Construction Industry Scheme (CIS) remains a cornerstone of project management; strict adherence to subcontractor verification and monthly filing is essential to avoid the heavy penalties that HMRC now applies with increasing frequency. In this environment, a disciplined approach to VAT on property transactions uk is the hallmark of a sophisticated development operation.

Corporate Structuring: SPVs, LLPs, and the Limited Company Debate

Selecting the appropriate corporate vehicle is a decision that dictates a project’s financial trajectory from the outset. Since the main rate of Corporation Tax reached 25% for companies with profits exceeding £250,000, developers must weigh this against the higher personal income tax bands. For many, it’s more efficient to retain profits within a corporate structure for reinvestment rather than extracting them as dividends. This choice becomes even more critical when navigating the complexities of VAT on property transactions uk, as the chosen entity must be correctly positioned to support full input tax recovery on construction and professional fees. Strategic profit extraction requires a balanced approach, utilizing a mix of salaries and dividends to manage personal tax liabilities while maintaining the company’s growth capital.

The decision between a limited company and a partnership often hinges on the specific needs of the investors. While companies are the standard, the Limited Liability Partnership (LLP) serves as a transparent hybrid solution for multi-partner joint ventures. It offers the protection of limited liability while allowing profits to be taxed at the individual partner level, which is particularly useful when partners have diverse tax profiles. Regardless of the entity, ensuring compliance with Stamp Duty Land Tax (SDLT) guidance is essential, especially when dealing with the 5% surcharge on additional residential properties or non-UK resident surcharges.

The Strategic Use of SPVs

Special Purpose Vehicles (SPVs) are the industry standard for ring-fencing project risk. Lenders typically prefer SPVs because they isolate the specific asset from the developer’s wider commercial liabilities, which often results in more favourable financing terms. For serial developers, a holding company architecture allows for the efficient management of multiple SPVs. There is also a distinct tax advantage in selling the shares of an SPV rather than the property itself, though this requires meticulous planning to ensure the VAT on property transactions uk remains fully optimized and that no “trapped” VAT issues arise for the buyer.

Group Structures and Loss Relief

A well-organized group structure provides the flexibility to utilize group relief, allowing you to offset losses in one development against profits in another. This is a vital tool for cash flow management across a diverse portfolio. For developers with cross-border interests, incorporating international tax planning ensures that global tax liabilities are managed without creating unnecessary friction with HMRC. It’s also imperative to maintain “arm’s length” transactions in all inter-company lending to satisfy transfer pricing regulations. If you’re managing complex multi-site operations, our team can provide the necessary oversight to ensure your group remains both compliant and tax-efficient.

Optimising Transactional Taxes: SDLT and VAT Recovery Strategies

Precision in transactional tax planning is the difference between a project that thrives and one that merely survives. While many investors view VAT on property transactions uk as a standard cost of doing business, it is actually a variable that can be optimized through meticulous structuring. Achieving a zero-rated status for the first grant of a major interest in new residential buildings allows for the full recovery of input tax on construction costs. This creates a significant cash flow advantage that is often lost in residential conversions, where unrecoverable VAT can become a silent drain on capital. We prioritize the identification of these recovery streams early, ensuring that the tax profile of the development supports its commercial objectives.

A frequent pitfall for developers is the “Option to Tax” trap. If a vendor has exercised their option to tax a commercial site, the purchase price increases by 20%. For a developer planning to build residential units for exempt letting, this VAT becomes an absolute cost that cannot be reclaimed from HMRC. Auditing the VAT status of land before the purchase is finalized is a non-negotiable step in our due diligence process. Similarly, navigating the 5% reduced rate for renovations of dwellings that have been empty for at least two years requires rigorous evidence; without it, contractors will default to the 20% standard rate, inflating project costs unnecessarily.

Mitigating SDLT Leakage

Stamp Duty Land Tax (SDLT) remains one of the most significant upfront costs in any acquisition. While formal Multiple Dwellings Relief has been abolished, identifying equivalent reliefs or utilizing mixed-use classifications remains a high-value strategy for 2026. By correctly identifying non-residential elements of a site, developers can often access lower commercial SDLT thresholds compared to the higher residential rates. It’s also vital to monitor “substantial performance,” as the tax liability is triggered the moment a buyer takes possession or pays a substantial part of the consideration, regardless of whether legal completion has occurred.

VAT Recovery and Construction Services

Contractors don’t always apply the correct VAT rates, often out of caution. It’s the developer’s responsibility to ensure that work on new builds is zero-rated and that qualifying conversions benefit from the 5% rate. For large-scale commercial assets, the Capital Goods Scheme requires monitoring of VAT recovery over a ten-year period, adjusting for changes in the building’s use. For those managing smaller portfolios, a small business accountant provides the necessary oversight to manage these complex cash flow requirements. Our approach ensures that every pound of input tax is accounted for, protecting your margins from avoidable leakage.

Maximising Development Incentives and Statutory Reliefs

While the diligent management of VAT on property transactions uk remains a priority for maintaining cash flow, the strategic application of statutory reliefs often dictates the ultimate profitability of a project. These incentives go beyond simple expense deductions; they’re designed to encourage the redevelopment of difficult sites and the adoption of innovative building techniques. By integrating these reliefs into your initial financial modeling, we ensure that your capital is deployed as efficiently as possible. We believe that a project’s fiscal design should be as robust as its structural engineering, particularly when navigating the 25% main rate of Corporation Tax.

Statutory reliefs like the Structures and Buildings Allowance (SBA) provide a steady 3% annual relief on qualifying construction costs for non-residential projects. Although this is a long-term play, it offers a predictable tax shield that enhances the commercial viability of commercial assets over their lifecycle. When combined with more immediate incentives, these allowances form a comprehensive strategy that protects your development margins from unnecessary erosion. Our approach focuses on identifying these opportunities during the pre-construction phase, ensuring that no qualifying expenditure is overlooked.

Land Remediation: Turning Liability into Relief

Brownfield sites often carry the burden of contamination or dereliction, yet they also offer some of the most significant tax opportunities. Land Remediation Relief provides a 150% tax deduction for companies tackling “blighted” land. Under the 2026 HMRC guidelines, this applies to costs incurred in treating soil contamination, removing asbestos, or clearing derelict structures that have been abandoned for decades. If your company spends £100,000 on qualifying remediation, it can deduct £150,000 from its taxable profits. For a developer paying the 25% main rate, this effectively reduces the net cost of the works by £37,500, often making the difference in the commercial viability of a complex site.

R&D and Capital Allowances

Innovation in construction is frequently overlooked as a source of tax relief. Research and Development (R&D) tax credits apply to any project that seeks to overcome technical uncertainties, such as developing new sustainable materials or integrating bespoke energy-efficient systems into complex builds. When combined with the 2026 rules for Full Expensing, which allow for an immediate 100% tax deduction on qualifying plant, machinery, and integral features, the impact on your balance sheet is substantial. We encourage a thorough review of the latest HMRC tax warnings to ensure your claims are robust and fully compliant with current standards. If you’re ready to enhance your project’s financial performance, our property accounting team can help you identify and claim the full range of statutory reliefs available to your development.

Integrating Tax Planning into the Development Life Cycle

Successful property development is a marathon of precision, requiring a tax strategy that evolves alongside the project. We view tax planning not as a series of isolated events, but as a continuous thread that runs from the initial site appraisal to the final exit. In the pre-acquisition phase, our focus is on rigorous due diligence and the verification of the VAT status of the land. This early intervention ensures that the chosen corporate structure is perfectly aligned with the project’s goals, preventing the “Option to Tax” traps that can derail a development’s feasibility before it even begins.

As the project moves into the construction phase, the emphasis shifts toward operational excellence and compliance. This involves the meticulous monitoring of the Construction Industry Scheme (CIS) and the real-time tracking of capital expenditure to ensure all statutory reliefs are captured. Managing VAT on property transactions uk during this period requires a steady hand to maintain cash flow and ensure that input tax recovery is maximized. A Chartered Accountant is essential for navigating these multi-year timelines, providing the intellectual rigour needed to manage complex analytical challenges across various tax years.

Exit Strategy and Capital Preservation

The exit phase represents the culmination of your strategic efforts, yet it’s often where the most significant tax liabilities arise. With the Business Asset Disposal Relief (BADR) rate having increased to 18% on 6 April 2026, the structure of your disposal requires careful consideration to preserve capital. We help you navigate the choice between “selling to reinvest” and “refinancing to hold,” analyzing the long-term impact on your portfolio’s liquidity. Managing the transition from trading profit to investment income is a delicate process, particularly when your objective is to build a sustainable, multi-generational property legacy.

The Value of Professional Partnership

While generic accounting software might suffice for simple operations, the complexities of high-value property development demand bespoke tax architecture. A proactive tax audit, conducted before HMRC initiates any formal investigation, provides a layer of security and demonstrates a commitment to fiscal integrity. At Davis & Co LLP, we position ourselves as your strategic partner, offering the individualized service delivery that has become our signature. Our approach ensures that your VAT on property transactions uk and wider tax liabilities are handled with the discretion and deep-seated expertise your commercial interests deserve.

Securing Your Development Legacy in 2026

Navigating the intricacies of VAT on property transactions uk requires a shift from reactive accounting to a proactive, lifecycle-based strategy. By establishing robust corporate structures like SPVs and identifying high-value statutory reliefs early in the acquisition phase, you protect your development margins from the friction of unrecoverable costs. We believe that fiscal precision is as vital to a project’s success as its physical construction, especially in an environment where HMRC scrutiny continues to intensify and regulatory requirements become more granular.

As Chartered Certified Accountants with over 120 years of expertise, our team specializes in property accounting and international tax planning. We offer a strategic partnership approach to HMRC compliance, ensuring that your portfolio is both resilient and tax-efficient across multi-year timelines. We invite you to consult our property tax specialists for a bespoke development strategy that aligns with your long-term commercial objectives. With the right advisory partner by your side, you can move forward with the confidence that your investments are secure and your vision is well-advised.

Frequently Asked Questions

Is property development considered a trade or an investment for tax purposes in 2026?

The classification depends on your intent and the frequency of your activities, analyzed through HMRC’s “badges of trade.” If you acquire a site with the primary purpose of a quick resale for profit, it’s generally treated as a trade subject to Corporation Tax. Conversely, holding property to generate long-term rental income is classified as an investment, where gains are subject to Capital Gains Tax at 24% for residential property.

Can I claim VAT back on a residential property development project?

You can reclaim VAT on a residential development if the project involves the first grant of a major interest in a new build, which is a zero-rated supply. However, if your strategy involves long-term residential letting, these supplies are usually exempt from VAT, meaning you can’t recover the input tax on construction costs. Managing VAT on property transactions uk requires identifying these recovery streams before the first brick is laid.

What is an SPV and why do property developers use them for transactions?

A Special Purpose Vehicle is a legal entity, typically a limited company, established for the sole purpose of a specific property project. Developers utilize them to ring-fence financial risks and liabilities, ensuring that a single project’s challenges don’t jeopardize their wider commercial portfolio. Lenders often mandate the use of SPVs to provide clear, isolated security for development finance, which can lead to more favourable borrowing terms.

How does Land Remediation Relief work for derelict sites in 2026?

This relief provides a 150% tax deduction for qualifying capital expenditure incurred while cleaning contaminated or derelict land. If your company spends £50,000 on asbestos removal or soil treatment, it can deduct £75,000 from its taxable profits. This incentive is a critical factor for brownfield developments, effectively reducing the net cost of remediation and making otherwise unviable sites commercially attractive for redevelopment in the 2026 fiscal landscape.

What are the VAT implications of the “Option to Tax” on commercial land?

The “Option to Tax” allows a landowner to charge VAT at the standard 20% rate on commercial land supplies that would otherwise be exempt. While this enables the owner to recover their own input tax, it increases the acquisition cost for buyers who can’t reclaim VAT, such as residential developers. We recommend a thorough audit of VAT on property transactions uk prior to acquisition to avoid unforeseen tax leakage on commercial sites.

Can I offset construction losses against my other personal income streams?

If your development activity is classified as a trade, you may be able to utilize “sideways loss relief” to offset trading losses against other personal income streams. However, if the project is considered a property investment, losses are generally restricted and can only be carried forward to offset future profits from the same property business. The distinction between these two classifications is a frequent point of contention during HMRC compliance reviews.

What is the Construction Industry Scheme (CIS) and when must I register?

The Construction Industry Scheme is a set of rules for making payments to subcontractors for construction work. You must register as a contractor if you pay subcontractors for such work, even if your primary business isn’t construction. This includes property developers who manage their own sites. Failure to verify subcontractors and file monthly returns results in significant penalties, making CIS compliance a cornerstone of modern, disciplined project management.

How has the 2026 budget affected VAT on property transactions?

The 2026 fiscal environment has been shaped by the increase in Business Asset Disposal Relief to 18%, effective from 6 April 2026. This change significantly impacts exit strategies for developers looking to sell their businesses or SPVs. While the main rate of Corporation Tax remains at 25% for profits exceeding £250,000, the budget maintained the 100% Full Expensing relief, providing a continuous incentive for capital investment in plant and machinery.