What if the most critical factor in your 2026 bank loan application isn’t your current profit, but the precision of your three-year volatility forecast? Many UK business owners feel the weight of increasingly stringent lending criteria and the pressure of interest rate volatility, particularly as the prime rate remains at 6.75%. You likely recognize that the traditional approach to borrowing has shifted; understanding how to secure business funding from banks now requires a level of financial transparency and strategic foresight that goes beyond basic bookkeeping.

We understand that preparing multi-year projections can feel like an exercise in complexity. This guide provides a comprehensive framework to help you optimize your creditworthiness and present a compelling case to your financial institution. We’ll explore how to align your growth objectives with current banking expectations to secure the capital required for sustainable expansion on favourable terms. From refining your internal management accounts to mastering the nuances of the 2026 lending environment, we’ll outline the steps necessary to turn a standard application into a successful funding round and a strengthened professional partnership.

Key Takeaways

- Understand the transition toward value-based lending models and how current UK base rates influence commercial margins in the 2026 environment.

- Learn how to secure business funding from banks by optimizing the ‘5 Cs’ of credit and taking proactive steps to strengthen your institutional credit profile.

- Identify the most appropriate funding structure for your specific requirements, comparing traditional term loans with revolving credit and asset-based lending facilities.

- Master the construction of a professional financial dossier, including the development of robust three-way forecasts and statutory audit and assurance reports.

- Develop a framework for post-funding debt management that focuses on covenant compliance and the strategic distinction between good and bad debt.

Navigating the 2026 Business Lending Landscape

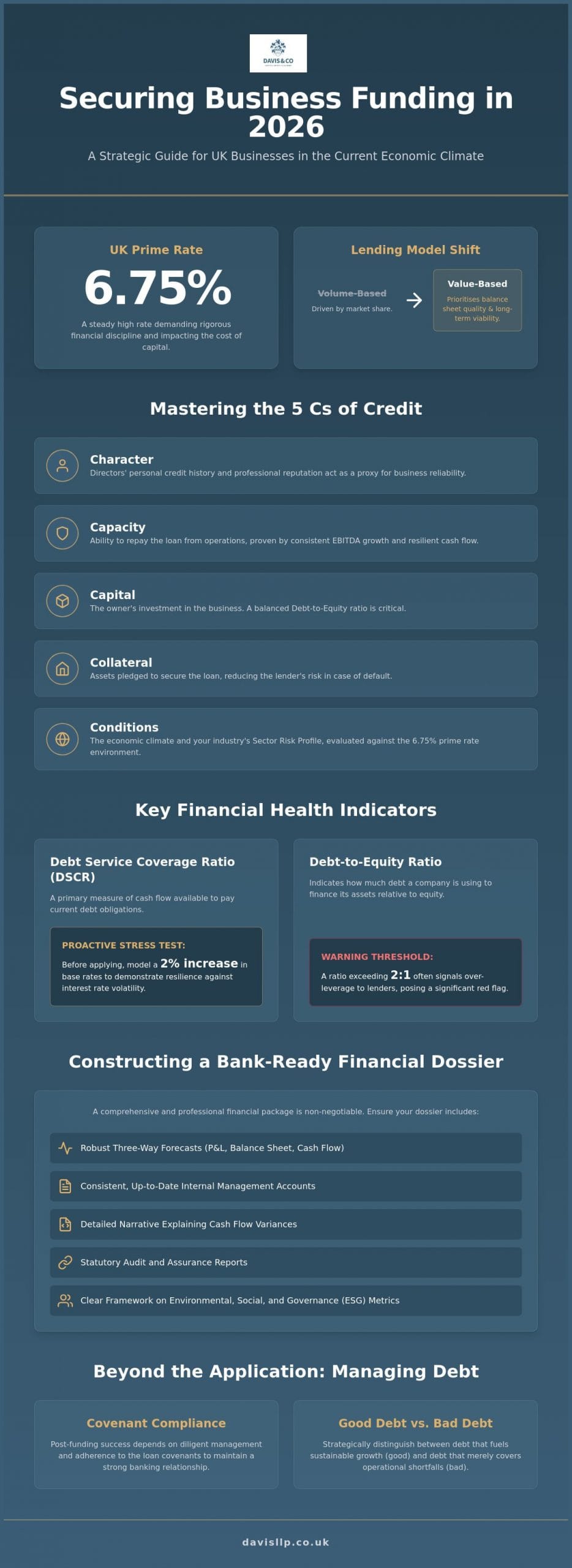

The economic environment of 2026 presents a unique set of challenges for UK business owners. With the prime rate holding steady at 6.75%, the cost of capital has reached a level that demands rigorous financial discipline. Banks have moved away from the volume-based lending of previous decades, where market share was the primary driver. Instead, they’ve adopted a value-based approach. This shift means lenders prioritise the quality of a business’s balance sheet and its long-term viability over sheer growth metrics. Gaining a deep understanding small business financing options is no longer just about finding a lender; it’s about positioning your firm as a low-risk, high-value asset in their portfolio.

Your industry’s “Sector Risk Profile” now carries significant weight in credit committee decisions. Banks categorise industries based on their sensitivity to current economic pressures, such as supply chain disruptions or shifting consumer behaviour. If your sector is flagged as high-risk, you’ll face tighter margins and more exhaustive scrutiny. We’ve observed that the most successful applicants secure funding well before a capital injection becomes an urgent necessity. Seeking terms while your cash reserves are healthy provides a strategic advantage, allowing you to negotiate from a position of strength rather than desperation. This foresight is a hallmark of effective how to secure business funding from banks in the current climate.

The Impact of Interest Rate Volatility on Debt Servicing

Banks in 2026 are focused intensely on your Debt Service Coverage Ratio (DSCR). In a high-rate environment, a ratio that was acceptable two years ago might now be considered marginal. You should stress test your own cash flow by modelling a 2% increase in base rates before submitting your application. This internal rigour ensures you can handle potential hikes. Deciding between fixed and variable rates requires a balanced view; while fixed rates offer certainty, they often come with higher upfront costs in a volatile market. It’s vital to ensure your how to secure business funding from banks strategy accounts for these fluctuations.

Bank Risk Appetite in 2026

Institutional risk appetite is now heavily influenced by Environmental, Social, and Governance (ESG) metrics. Tier 1 high-street banks are increasingly likely to reject applications from businesses that lack a clear sustainability framework. In contrast, specialist commercial lenders may offer more flexibility but often at a higher price point. Common red flags in 2026 include inconsistent management accounts and high levels of “hidden” debt, such as aggressive director loan accounts. Avoiding these triggers is essential for a smooth approval process and a long-term banking relationship.

The Fundamentals of Bank Creditworthiness

Understanding how to secure business funding from banks requires a mastery of the internal metrics lenders use to judge risk. While the broader economy sets the stage, your business’s individual creditworthiness is the script. Banks typically evaluate this through the ‘5 Cs’ of credit: Character, Capacity, Capital, Collateral, and Conditions. In 2026, the ‘Conditions’ element is particularly sensitive, as lenders assess how your specific operation withstands a 6.75% prime rate environment. They aren’t just looking at your past performance; they’re looking at your resilience against future shifts.

Optimising your business credit score is a continuous process that demands attention to detail. You should ensure all trade credit is reported accurately and that your Debt-to-Equity ratio remains balanced. A ratio exceeding 2:1 often signals to a bank that you’re over-leveraged, which can stall your application regardless of your turnover. Don’t overlook the personal credit of directors, either. For SMEs, the personal financial conduct of leadership is frequently viewed as a proxy for the business’s own reliability. Maintaining a clean personal credit history is often the deciding factor in securing competitive interest rates.

Capacity and Cash Flow Resilience

Capacity is your business’s ability to repay the loan from its primary operations. Lenders look for consistent EBITDA growth as a primary indicator of this health. If your business experiences ‘lumpy’ cash flow due to seasonal contracts or long project cycles, transparency is your best tool. We recommend providing a detailed narrative alongside your figures to explain these variances. Effective cash flow management is the cornerstone of proving repayment ability. It demonstrates that you have the foresight to navigate lean months without compromising your financial obligations.

Collateral and Security Structures

Collateral provides the bank with a secondary source of repayment, and there’s a clear hierarchy of security. Unencumbered freehold property remains the gold standard, followed by debentures over business assets and personal guarantees. Interestingly, 2026 has seen a rise in lenders accepting intellectual property and established digital assets as supplementary collateral, provided they’re independently valued. It’s also essential to understand the Enterprise Act’s impact on security rankings, particularly how it affects the distribution of assets. While UK standards are distinct, they share a logical rigour with international frameworks like SBA-guaranteed loan programs, which prioritise clarity in security. If you’re looking to scale, our team can assist with business growth acceleration strategies to ensure your balance sheet remains attractive to top-tier lenders.

Evaluating Debt Instruments: Selecting the Right Funding Structure

Choosing the correct financial instrument is as vital as the funding itself. While a term loan offers stability, a revolving credit facility provides the agility needed for fast-moving operations. In 2026, we’ve seen a notable increase in Asset-Based Lending (ABL), particularly for inventory-heavy businesses. This structure allows you to leverage the value of your stock or plant machinery, transforming static assets into liquid working capital. It’s a pragmatic solution for firms that possess significant physical value but require improved liquidity to fund expansion.

For those with significant property holdings, the choice between a commercial mortgage and a sale-and-leaseback arrangement is a strategic one. A mortgage builds equity over time, while sale-and-leaseback can instantly release capital for reinvestment without the burden of traditional debt. Similarly, invoice discounting and factoring have evolved. They’re no longer just “last resort” options but sophisticated tools for managing the gap between delivery and payment. When considering these varied paths, consulting a step-by-step guide to getting a business loan can help clarify which structure aligns with your specific growth trajectory.

Term Loans vs. Lines of Credit

A term loan is typically the superior choice for long-term capital expenditure, such as acquiring new premises or heavy machinery. It provides the certainty of a fixed repayment schedule, allowing for precise long-term budgeting. Conversely, a business line of credit is indispensable for managing short-term liquidity, such as seasonal VAT compliance cycles or temporary inventory surges. We always advise our clients to look beyond the headline APR. You must analyse the total cost of capital, including arrangement fees and non-utilisation charges, to understand the true effective interest rate. This level of detail is a prerequisite when learning how to secure business funding from banks that offer the most favourable terms.

Specialist Funding for Growth Sectors

The lending market has become increasingly segmented. Green Finance initiatives now offer tangible incentives, such as reduced margins for businesses that meet specific sustainability benchmarks. For tech-led firms, R&D-linked debt facilities allow for the capitalisation of future tax credits. We’ve also found that sector-specific expertise is a powerful lever. For instance, utilising specialist dental tax services or medical sector advisors can unlock niche lending products that high-street generalists might overlook. These tailored instruments often come with covenants that better reflect the operational realities of your industry. Navigating these options is a core part of how to secure business funding from banks in an era of hyper-specialisation.

Constructing a Bank-Ready Financial Dossier

A bank manager’s decision often rests on the clarity of the evidence presented. Your dossier should begin with three years of statutory audit and assurance reports to provide a baseline of historical reliability. History only tells half the story. A robust 3-way forecast, integrating your Profit and Loss, Balance Sheet, and Cash Flow, demonstrates that you understand the future mechanics of your business. This level of preparation is the definitive answer to how to secure business funding from banks in a competitive market.

Don’t leave financial anomalies to the lender’s imagination. A ‘Management Narrative’ that explains one-off capital expenditures or temporary margin dips prevents a credit officer from making negative assumptions. Supplement this with a directory of key contracts and professional asset valuations to ground your balance sheet in reality. Your executive summary should distill these hundreds of pages into a three-minute pitch. It must clearly state your capital requirement and your precise repayment strategy.

The Power of Management Accounts

While year-end accounts are a statutory necessity, they’re often too stale for a 2026 lending environment. Real-time management accounts are significantly more persuasive. They show that you’re monitoring your business today, not just reflecting on last year. By aligning your internal KPIs with the bank’s specific covenants, you demonstrate an unusual level of control over your operations. This requires that your underlying bookkeeping services are rigorous and capable of producing granular data on demand.

The Business Plan: Strategic Context for the Numbers

Your business plan must move beyond generic growth projections. It should articulate a specific ‘Use of Funds,’ detailing exactly how the capital will generate a return on investment. In a post-2025 economy, banks expect a sophisticated market analysis that acknowledges competitive positioning and potential headwinds. Identifying risks through a SWOT analysis isn’t a sign of weakness. It’s proof of a mature management team that has already planned for mitigation. Constructing this narrative is a vital component of how to secure business funding from banks, as it bridges the gap between raw data and strategic intent. If you require assistance in refining your financial presentation, we invite you to explore our management accounts and advisory services to ensure your application is beyond reproach.

Beyond the Application: Managing Debt for Sustainable Growth

Securing the facility is merely the first milestone; the true test of leadership lies in how that capital is deployed and managed. We believe it’s vital to distinguish between ‘good debt,’ which fuels revenue-generating assets and infrastructure, and ‘bad debt,’ which simply plugs operational inefficiencies. While our focus throughout this guide has been on how to secure business funding from banks, the long-term success of that funding depends on your ability to maintain the lender’s confidence after the funds have been drawn. This requires a shift in mindset from acquisition to stewardship.

Bank covenants are not just bureaucratic hurdles; they’re early warning systems designed to protect both the lender and the borrower. Monitoring these metrics, such as your leverage and liquidity ratios, requires a proactive rather than reactive stance. Technical defaults often occur not because a business is failing, but because management has lost sight of these contractual boundaries. If your operations span multiple jurisdictions, integrating your debt servicing into a broader international tax planning strategy is paramount. This ensures that interest payments are structured to be as tax-efficient as possible across your entire corporate footprint.

Tax Efficiency and Interest Deductibility

The UK’s corporate interest restriction rules can be complex, particularly for businesses with significant borrowing requirements. You must ensure that your interest payments remain deductible against your taxable profits, as exceeding these thresholds can unexpectedly increase your effective tax rate. This is where professional tax advice UK becomes indispensable. We also encourage our clients to review their funding structures periodically. As your credit profile strengthens and market conditions shift, refinancing can often unlock better terms or more flexible covenants, further reducing your total cost of capital.

Strategic Growth and Exit Planning

Well-managed bank debt can significantly enhance your enterprise value by demonstrating that the business is capable of servicing high-level institutional capital. It’s a balance of maintaining control while leveraging external resources to scale. By utilizing professional business growth acceleration, you ensure that every pound borrowed is directed toward high-impact initiatives that support your ultimate exit strategy. Whether you’re preparing for a future sale or seeking to dominate your niche, the strategic use of debt is a powerful tool. Understanding how to secure business funding from banks is only the beginning; the mastery of that debt is what truly drives sustainable growth.

Positioning Your Enterprise for Long-Term Success

Achieving a successful funding round in 2026 is a testament to a business’s operational maturity and strategic foresight. We’ve explored the necessity of aligning your internal management accounts with institutional expectations and the importance of selecting a debt structure that complements your specific growth trajectory. Ultimately, mastering how to secure business funding from banks is less about a single application and more about the ongoing discipline of financial transparency and risk mitigation.

As Chartered Certified Accountants with a legacy dating back to 1901, we provide the steady hand required to navigate these complex institutional landscapes. Our expertise in complex audit and assurance ensures your firm is bank-ready, while our specialization in international tax and growth acceleration helps you maximize the impact of every pound borrowed. We invite you to secure your strategic growth with Davis & Co LLP’s expert advisory services. With the right preparation and a committed professional partnership, your business is well-positioned to thrive in the years ahead.

Frequently Asked Questions

What is the most common reason bank loans are rejected in 2026?

The most common reason for rejection in 2026 is a failure to demonstrate cash flow resilience in a high-interest environment. With the prime rate at 6.75%, lenders are hyper-focused on your ability to service debt if rates rise even slightly. If your 3-way forecasts don’t account for these stress tests, banks will likely view your business as a high-risk prospect regardless of your historical turnover.

How much funding can my business realistically secure from a bank?

Most businesses can realistically secure funding equivalent to two to four times their sustainable annual EBITDA. This figure varies based on your sector’s risk profile and the quality of the security you can provide. For property-heavy businesses, the loan-to-value (LTV) ratio on your assets will often be the primary cap on your total borrowing capacity.

Do I always need to provide a personal guarantee for a business loan?

You will likely be required to provide a personal guarantee if your business lacks sufficient tangible assets to fully secure the facility. While some government-backed schemes or high-value debentures can reduce this requirement, banks in 2026 still view personal guarantees as a vital sign of a director’s commitment. It’s a standard feature of the SME lending landscape that ensures alignment between the business leadership and the financial institution.

How long does the bank funding application process typically take?

A typical bank funding application takes between four and twelve weeks from the initial submission to the final drawdown. This timeline is largely determined by the complexity of your business and the precision of your financial dossier. We’ve found that businesses focusing on how to secure business funding from banks through meticulous preparation can often expedite the process by reducing the need for additional queries from the credit committee.

Is it better to use a high-street bank or an alternative lender?

Choosing between a high-street bank and an alternative lender depends on your priority between cost and flexibility. High-street banks offer the most favourable interest rates and terms for businesses that meet their rigid criteria. Alternative lenders, while more expensive, provide a valuable service for firms that require rapid funding or have unique operational structures that don’t fit traditional models.

How do banks view businesses with international operations or tax structures?

Banks scrutinise international operations for jurisdictional risk and the complexity of cross-border tax arrangements. To secure approval, you must demonstrate a clear international tax planning strategy that shows your global revenue is stable and accessible for debt servicing. They prefer businesses that can prove their international footprint is a strength rather than a source of financial opacity.

Can I get a bank loan if my business has a poor credit history?

Securing a loan with a poor credit history is exceptionally difficult at Tier 1 institutions and usually requires a pivot to alternative lenders. These specialist providers may offer a path for how to secure business funding from banks or similar institutions, though they often demand higher interest rates or significant tangible collateral. We recommend focusing on repairing your credit score through consistent management accounts before approaching traditional lenders.

What financial ratios do bank managers look at most closely?

Bank managers look most closely at the Debt Service Coverage Ratio (DSCR) and the Debt-to-Equity ratio. A DSCR of 1.25x or higher is generally considered the baseline for safety in the 2026 lending climate. They also examine your current ratio to ensure you have sufficient liquidity to meet short-term obligations without disrupting your long-term growth plans.