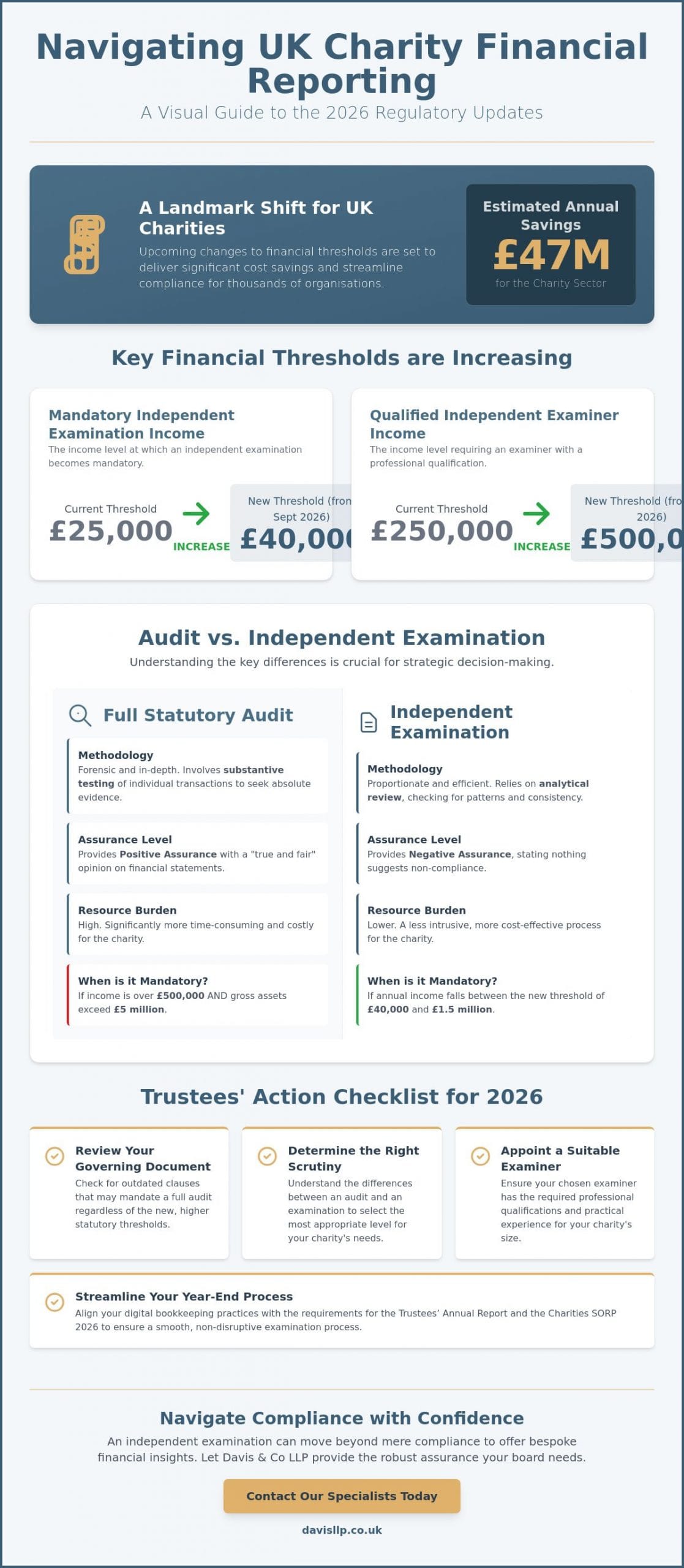

The UK government’s decision to raise financial thresholds for accounting periods ending on or after 30 September 2026 is expected to save the charity sector an estimated £47 million every year. This change means that more organisations can now benefit from an independent examination for charities, as the mandatory threshold for this level of scrutiny rises from £25,000 to £40,000. We understand that managing Charity Commission regulations can feel like a burden, particularly when the anxiety over personal liability and compliance costs weighs heavily on your board.

Our guide offers a professional overview of these regulatory changes, including the increase in the income threshold for a qualified independent examiner from £250,000 to £500,000. We’ll outline the strategic benefits of this bespoke assurance framework and how it provides quiet excellence for growing organisations. You’ll gain a clear understanding of the new three-tier reporting structure under the Charities SORP 2026 and how to ensure full compliance with CC31 guidance through a smooth, non-disruptive process.

Key Takeaways

- Understand the fundamental differences between substantive testing and analytical review to determine which level of scrutiny best serves your charity’s long-term objectives.

- Navigate the updated eligibility criteria to ensure your organisation benefits from a less intrusive independent examination for charities while maintaining statutory compliance.

- Identify the specific professional qualifications and practical experience required for an examiner to provide the robust assurance your board needs.

- Learn how to streamline your year-end process by aligning digital bookkeeping practices with the requirements of a sophisticated Trustees’ Annual Report.

- Discover how a tailored examination can move beyond mere compliance to offer bespoke financial insights, particularly for charities with complex or international structures.

Understanding the Independent Examination Framework for UK Charities

The Charities Act 2011 provides the statutory foundation for financial oversight in England and Wales. Within this framework, an independent examination for charities serves as a bespoke form of external scrutiny. It’s designed to provide a level of assurance that is proportionate to the size and complexity of the organisation. Unlike a full audit, which requires extensive substantive testing to provide a “true and fair” opinion, an independent examination focuses on a professional review of the accounts. It ensures the records are consistent with the underlying bookkeeping and that the accounts comply with relevant legal requirements.

While the Charity Commission often refers to this as a “light touch” process, it shouldn’t be mistaken for a superficial check. It’s a rigorous assessment that offers significant strategic value. For many growing organisations, this process acts as a bridge, offering the credibility needed to satisfy donors and grant makers without the intensive resource requirements of a full statutory audit. It provides a level of comfort to stakeholders that the charity’s resources are being managed responsibly and in accordance with its charitable objectives.

The Duty of Trustees in Financial Reporting

Trustees carry a significant responsibility to maintain financial transparency. This isn’t merely a matter of administrative preference; it’s a core fiduciary duty. Under the CC31 guidance, trustees must ensure that the charity’s financial statements are accurate and accessible. The 2026 regulatory updates, including the new Charities SORP which becomes mandatory for accounting periods beginning on or after 1 January 2026, introduce a tiered reporting structure that requires a more nuanced approach to governance. We believe that clear, transparent reporting is the most effective way to protect the charity’s reputation and mitigate the risk of personal liability for the board. It ensures that the story of the charity’s impact is backed by robust financial data.

When is an Independent Examination Mandatory?

The financial landscape for charities is shifting. For accounting periods ending on or after 30 September 2026, the income threshold for a mandatory independent examination for charities increases from £25,000 to £40,000. This change is part of a broader move toward proportionate regulation, estimated to save the sector £47 million annually. Organisations will generally require an examination if their annual income falls between £40,000 and £1.5 million.

However, an audit remains mandatory if a charity’s assets exceed £5 million and its income is over £500,000. It’s also vital to check your charity’s governing document. Some older constitutions may stipulate a full audit regardless of these statutory increases. We recommend that trustees review these documents early to ensure their chosen path of scrutiny remains legally sound and aligns with their strategic objectives.

Audit vs. Independent Examination: Key Differences and Strategic Choices

Deciding between a full statutory audit and an independent examination for charities is a matter of strategic resource management. While both provide external scrutiny, their methodologies differ fundamentally. An audit is a forensic exercise involving substantive testing, where the auditor seeks absolute evidence for individual transactions to provide a “true and fair” opinion on the financial statements. In contrast, an independent examination relies on an analytical review. The examiner looks for patterns, asks probing questions of the trustees, and ensures the accounts align with the charity’s records without necessarily verifying every single invoice.

The result of an examination is a “negative assurance” report. This statement confirms that nothing has come to the examiner’s attention to suggest the accounts are inaccurate or non-compliant. For many trustees, this level of scrutiny is more than sufficient to satisfy legal duties while significantly reducing the administrative and financial burden on the organisation. By opting for this more proportionate approach, charities can redirect the cost savings, which the DCMS estimates will reach £47 million across the sector by 2026, directly into their frontline services and business growth acceleration.

The Scope of an Independent Examiner’s Work

An examiner’s role is to provide a professional assessment of the charity’s financial health and reporting integrity. This involves a detailed review of internal control systems and a check for any unusual items or disclosures that might require further explanation. To maintain high levels of trust, examiners must adhere to strict professional standards for independent examiners. Their work ensures that the accounts don’t just balance, but also comply with the specific requirements of the Charities SORP 2026, which introduces significant changes to lease accounting and income recognition.

Choosing the Right Path for Your Charity

While the new £1.5 million income threshold for audits offers greater flexibility, trustees should consider the expectations of their wider stakeholder group. Major institutional funders or international donors sometimes require a full audit regardless of the statutory minimums. However, for most mid-sized organisations, the independent examination offers a pragmatic balance. It demonstrates financial integrity without the disruptive nature of a full audit.

Adopting the strategic small business accountant mindset allows trustees to view compliance as a tool for growth rather than a mere box-ticking exercise. We believe that choosing the right level of scrutiny is a vital part of a charity’s long-term financial strategy. If you’re unsure which path aligns with your 2026 objectives, our audit and assurance team can provide a tailored assessment of your specific requirements.

Qualifications and Eligibility: Appointing a Suitable Independent Examiner

Selecting the right individual to conduct an independent examination for charities is a decision that extends beyond mere statutory compliance. The law requires that an examiner is “independent,” a term that carries specific weight in a professional context. It implies a total absence of any connection to the charity that could be perceived as a conflict of interest. This includes not only the trustees themselves but also major donors, significant beneficiaries, or anyone involved in the day-to-day financial management of the organisation. True independence ensures that the scrutiny remains objective and the findings are beyond reproach.

The criteria for “requisite ability” also evolve as a charity grows. For accounting periods ending on or after 30 September 2026, the threshold at which a qualified independent examiner is mandatory will increase from £250,000 to £500,000. If your charity’s income exceeds this £500,000 mark but remains below the £1.5 million audit limit, you must appoint a member of a recognised professional body. This ensures the examiner possesses the technical expertise to navigate the complexities of the Charities SORP 2026 and provides the board with a higher degree of professional gravitas.

Recognised Professional Bodies for Examiners

Professional membership in bodies such as the ICAEW or ACCA serves as a hallmark of quality and reliability. These organisations require their members to adhere to strict ethical codes and maintain professional indemnity insurance, offering an essential safety net for trustees. In 2026, verifying the status of your proposed examiner is a vital step in your due diligence. It confirms that the individual is subject to regulatory oversight and possesses the practical experience necessary to handle sophisticated financial structures, including international interests or complex tax obligations.

Assessing Independence and Objectivity

It’s a common misconception that a charity’s regular bookkeeper can perform the examination. In reality, the examiner must be entirely separate from the preparation of the accounts they’re reviewing. This distinction is vital for maintaining the integrity of the process. When we work with clients, we ensure a clear separation of duties to protect the board from any accusations of partiality. Trustees should actively identify any personal or financial connections that might compromise an examiner’s objectivity, as even the appearance of a conflict can undermine the transparency of the final report.

Preparing for the Examination: A Best-Practice Checklist for 2026

Preparation for an independent examination for charities is a strategic undertaking that demands foresight. It’s not simply about gathering receipts; it’s about presenting a coherent narrative of your charity’s financial stewardship. With the Charities SORP 2026 becoming mandatory for periods starting on or after 1 January 2026, the transition to robust digital records is essential. Moving from physical vouchers to a cloud-based system allows for real-time reconciliations, which significantly streamlines the examiner’s review of your ledger and ensures that your data is current and accurate.

Your Trustees’ Annual Report is equally vital. It provides the necessary context for the financial data, explaining how your resources have been used to meet your charitable objectives. We’ve seen that a well-drafted report reduces the time an examiner spends on queries, as it pre-emptively addresses changes in income streams or significant expenditures. Particular attention must be paid to VAT compliance and Gift Aid claims. These areas are frequently scrutinised by regulators, and maintaining clear audit trails for these transactions is a hallmark of a well-governed organisation.

The Essential Document Pack

A successful examination relies on the quality and accessibility of your documentation. You should prepare a comprehensive pack that includes bank statements, investment reports, and full reconciliations for all accounts. It’s also vital to provide minutes from trustee meetings where significant financial decisions were made. If your organisation manages restricted funds, you must provide clear evidence that these monies were used strictly in accordance with the donor’s wishes. This level of transparency protects the board and reinforces the charity’s integrity in the eyes of the public and the Charity Commission.

Working with Your Examiner

We believe the relationship with your examiner should be a collaborative partnership. Setting clear expectations for communication at the start of the process prevents delays and ensures a smooth workflow. If the examiner identifies “matters of concern,” these should be viewed as opportunities to strengthen your internal controls rather than as criticisms of your management. This proactive approach ensures you meet the 10-month filing deadline for the Charity Commission with confidence and poise. If you require assistance in refining your financial systems before your next year-end, our charity accounting specialists are available to provide bespoke advice.

The Davis & Co LLP Approach: Bespoke Assurance for the Third Sector

At Davis & Co LLP, we view the independent examination for charities as more than a statutory hurdle. It’s an opportunity to provide trustees with the intellectual rigour and strategic clarity usually reserved for larger corporate entities. By applying our audit and assurance expertise to the examination process, we offer a level of scrutiny that goes beyond basic compliance. We focus on identifying operational efficiencies and ensuring that your financial reporting reflects the true impact of your organisation’s work. This commitment to quiet excellence ensures that your board can move forward with absolute confidence in its financial standing.

Specialist Expertise for Diverse Charities

Every organisation has its own nuances, whether it’s a medical research trust, an educational foundation, or a religious charity. We provide tailored solutions that respect these unique operational realities. For charities with international operations, the complexity increases significantly. Our deep understanding of international tax planning allows us to advise on cross-border funding and regulatory requirements with precision. We ensure that your global activities are reported accurately, mitigating risks and protecting your charity’s reputation across multiple jurisdictions.

Securing Your Charity’s Future

A proactive, year-round relationship with your examiner is the best way to avoid year-end surprises. We don’t believe in a “once-a-year” interaction. Instead, we act as a steady partner, providing dependable advice as your charity evolves. This approach is particularly valuable as the sector adapts to the tiered reporting structure of the Charities SORP 2026. By choosing a firm with a history of success in both the commercial and private client sectors, you signal to your stakeholders that you take your fiduciary duties seriously.

Transparency and stability are the foundations of long-term charitable impact. We invite you to contact our team to discuss how a bespoke independent examination for charities can support your strategic objectives for 2026 and beyond. We’ll provide a detailed proposal that addresses your specific needs, ensuring your organisation remains a trusted constant in an often volatile landscape.

Strengthening Your Charity’s Financial Governance for 2026

Navigating the transition to the new reporting thresholds and the Charities SORP 2026 requires a steady hand and a clear perspective. By understanding that an independent examination for charities is a strategic tool rather than a mere compliance burden, your board can focus its resources where they’re most effective. Whether you’re adapting to the increased £40,000 income threshold or managing the complexities of international funding, the right level of scrutiny provides the transparency your stakeholders expect.

As Chartered Certified Accountants with over 120 years of heritage, we bring a wealth of experience to the third sector. We specialise in providing tailored audit and assurance solutions for both national and international organisations, ensuring your financial reporting reflects the quiet excellence of your mission. We invite you to request a bespoke proposal for your charity’s independent examination to ensure your organisation remains resilient and well-advised. We look forward to supporting your continued success and impact in the years ahead.

Frequently Asked Questions

What is the income threshold for a charity independent examination in 2026?

For accounting periods ending on or after 30 September 2026, the mandatory threshold for an independent examination for charities increases to £40,000. This is a significant rise from the previous £25,000 limit. Charities with a gross income between £40,000 and £1.5 million will generally fall within this framework unless their asset value triggers a full statutory audit.

Can a volunteer or a member of the charity act as an independent examiner?

No, a member or regular volunteer cannot serve as your examiner. The Charity Commission requires the individual to be truly independent, meaning they must have no personal or financial connection that could influence their judgement. This ensures the scrutiny remains objective and maintains the professional gravitas required for statutory assurance. It’s vital that the examiner remains a neutral party to protect the integrity of the report.

How much does an independent examination for a charity typically cost?

Fees for an examination are determined by the complexity of the charity’s financial affairs rather than a fixed industry rate. The Department for Culture, Media and Sport (DCMS) estimates that the 2026 threshold increases will save the sector £47 million annually in compliance costs. This reflects the reality that an examination is a more proportionate and cost-effective alternative to a full audit for mid-sized organisations.

What happens if the independent examiner finds a serious problem?

If an examiner identifies a serious issue, they have a statutory obligation to report “matters of material significance” to the Charity Commission. This usually involves concerns regarding financial crime, significant governance failures, or risks to charitable assets. In most cases, the examiner will discuss these findings with the trustees first to allow for a bespoke solution or clarification before any formal report is submitted.

How long does the independent examination process usually take?

The process generally spans four to eight weeks from the receipt of all necessary documentation. This timeline depends heavily on the organisation of your digital records and the complexity of your restricted funds. Trustees must ensure the final report is submitted within 10 months of the financial year-end to remain compliant with statutory deadlines. Planning ahead is essential to avoid disruptive, last-minute rushes.

Does our charity need an audit if our income is below £1 million?

An audit may still be necessary even if your income is below the new £1.5 million limit. Under the 2026 regulations, an audit is mandatory if a charity’s assets exceed £5 million and its income is over £500,000. Additionally, your organisation’s governing document might specifically require a full audit regardless of these statutory minimums. We suggest reviewing your constitution regularly to ensure you’re following the correct path of scrutiny.

What is the difference between an independent examination and a financial review?

An independent examination for charities is a formal, legal requirement conducted according to specific directions from the Charity Commission. A financial review is typically an internal management exercise designed for strategic planning or cash flow management. While a review is useful for internal growth, it doesn’t provide the external assurance required for statutory filing. The examination offers a higher level of scrutiny that satisfies both donors and regulators.

How do we change our independent examiner if we are unhappy?

Trustees can usually change their examiner by passing a formal board resolution, provided this aligns with the charity’s constitution. It’s a straightforward administrative step, though it’s professional courtesy to inform the outgoing examiner in writing. We suggest a measured transition to ensure your new advisor has full access to historical records and context. This ensures your financial oversight remains a dependable constant during the change.