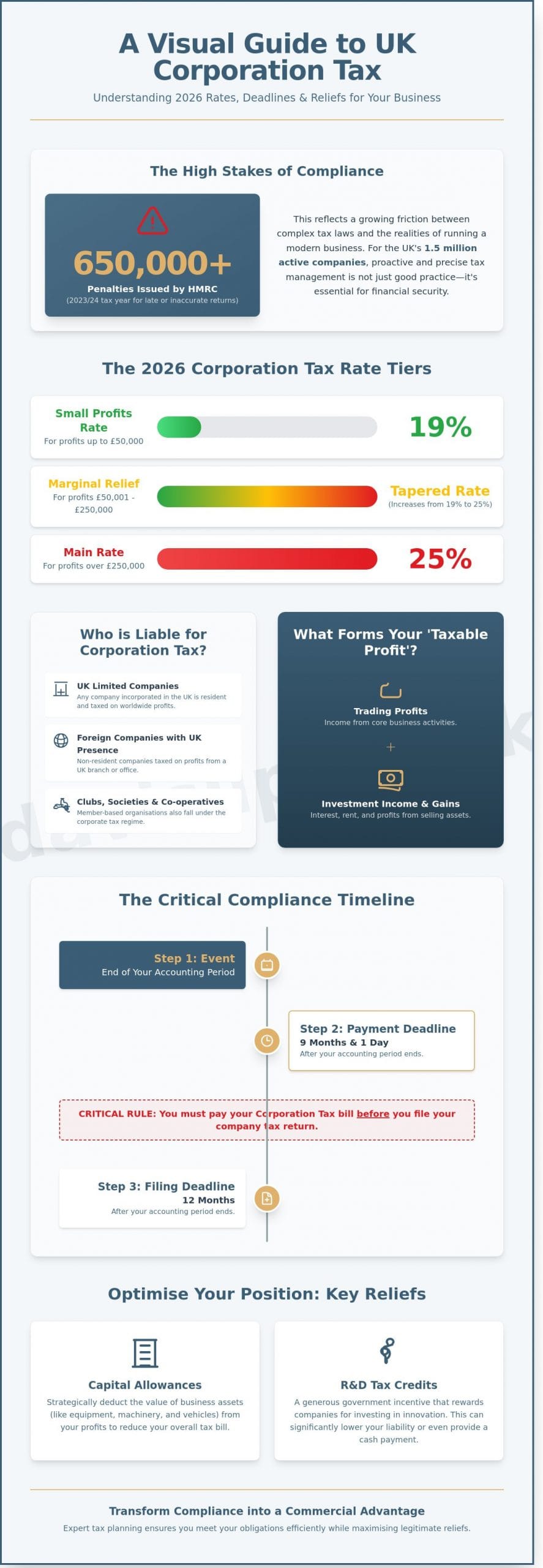

Did you know that during the 2023/24 tax year, HMRC issued more than 650,000 penalties to UK businesses for late or inaccurate company tax returns? This statistic reflects a growing friction between increasingly complex statutory requirements and the practical realities of running a modern firm. It’s a challenge we frequently address, as directors often feel the weight of ensuring every calculation is precise while fearing the financial impact of a missed deadline. You likely recognise that understanding exactly what is corporation tax is no longer a simple matter of applying a flat rate, especially with the nuances of marginal relief now affecting a significant portion of the UK’s 1.5 million active companies.

We’ve prepared this comprehensive guide to provide the professional gravitas and clarity your business requires to navigate the 2026 fiscal landscape. We’ll move beyond the basics to explore current rate structures, essential filing dates, and the bespoke reliefs that allow for legitimate tax optimisation. By the end of this article, you’ll have a clear, strategic perspective on your liabilities and the pragmatic steps needed to maintain a secure and efficient tax position.

Key Takeaways

- Gain a precise understanding of what is corporation tax and determine whether your entity, including foreign branches, is liable for this statutory levy.

- Navigate the 2026 dual-rate system by identifying how the £50,000 and £250,000 profit thresholds dictate your company’s specific tax percentage.

- Avoid common compliance pitfalls by mastering the critical ‘payment before filing’ rule and the statutory nine-month deadline following your accounting period.

- Discover how to optimise your fiscal position through strategic capital allowances and the latest 2026 Research and Development (R&D) tax credits.

- Learn how bespoke tax planning and international expertise can transform standard compliance into a strategic commercial advantage for your business.

Understanding Corporation Tax: A Definition for UK Limited Companies

Understanding what is corporation tax starts with recognising it as a statutory charge on the profits generated by corporate bodies and specific unincorporated associations. It’s a distinct fiscal obligation from the taxes paid by individuals or partnerships. Since the history of UK corporation tax began with its formal introduction in 1965, the system has evolved into a sophisticated framework that demands proactive management from every director.

We view this tax as a self-assessed liability. This means the responsibility rests entirely on your company to calculate, report, and settle its debts with HM Revenue & Customs (HMRC). There’s no invoice sent by the government; instead, you must maintain precise records to ensure your filings reflect the true financial position of the entity. Failure to manage this proactively often leads to avoidable penalties.

Who exactly is liable for Corporation Tax?

Liability isn’t restricted solely to private limited companies. While sole traders pay Income Tax on their business earnings, any incorporated entity falls under the corporate regime. This includes limited companies, foreign companies with a UK branch or office, and member-based organisations such as clubs, societies, and co-operatives.

The “resident” test determines the extent of your liability. Since 1988, UK law has dictated that any company incorporated in the UK is automatically resident here for tax purposes. These entities pay tax on their worldwide profits. Conversely, non-resident companies only pay the tax on profits specifically linked to a UK permanent establishment or UK property income. We provide bespoke advice to international clients to ensure these boundaries are clearly defined and compliant.

What constitutes ‘Taxable Profit’?

Taxable profit isn’t identical to the “profit before tax” figure seen in your annual accounts. It’s a refined value calculated after adjusting for non-deductible expenses and statutory capital allowances. To identify what is corporation tax based upon, we look at three primary income streams:

- Trading profits: The net income derived from your core business activities and service delivery.

- Investment income: This includes interest earned on corporate bank accounts or rental income from company-owned property.

- Chargeable gains: Profits realised from the sale of assets, such as land, buildings, or shares, that have appreciated in value.

On 1 April 2023, the UK transitioned to a tiered system. Companies with profits exceeding £250,000 now pay a main rate of 25%. Those with profits of £50,000 or less benefit from a small profits rate of 19%. For companies falling between these figures, a marginal relief system applies to ensure a smooth transition between the two rates. This structure requires a strategic approach to financial planning to ensure your business remains tax-efficient.

Calculating Your Liability: UK Rates and Thresholds for 2026

Understanding what is corporation tax requires a precise grasp of the current dual-rate structure. For the 2026 financial year, the UK continues to employ a system designed to distinguish between small enterprises and larger corporate entities. This approach ensures that tax burdens remain proportionate to a company’s financial performance while maintaining the UK’s competitive position among G7 nations.

The 2026 Rate Structure Explained

Profits exceeding £250,000 attract the Main Rate of 25%. This rate applies to the entirety of the company’s taxable profits once this upper limit is breached. Conversely, smaller entities with profits of £50,000 or less benefit from the Small Profits Rate, which remains fixed at 19%. This lower tier supports the growth of approximately 1.2 million small businesses across the UK, providing them with essential capital for reinvestment.

Businesses with profits between £50,000 and £250,000 pay an effective tax rate that increases gradually from 19% to 25% through the application of Marginal Relief. This relief acts as a tapered bridge, preventing a sudden tax “cliff edge” as profits grow. While calculating the specific figure is vital, ensuring you meet Corporation Tax payment deadlines is equally critical for statutory compliance. We’ve observed that 10% of businesses fail to account for the taper, resulting in avoidable cash flow strain.

The Impact of Associated Companies

HMRC defines an associated company as one that is controlled by the same person or group of persons. This definition extends beyond simple parent-subsidiary relationships to include companies under common individual control. It’s a vital distinction because the £50,000 and £250,000 thresholds are not applied per company; they’re divided by the total number of associated entities.

- Threshold Division: If you control two companies, the 19% threshold for each drops to £25,000.

- Strategic Control: Identifying “control” involves assessing share capital, voting power, or rights to assets during a winding-up.

- Compliance Risk: Miscounting associated companies is a frequent cause of HMRC enquiries.

This rule prevents businesses from artificially fragmenting operations to exploit lower tax rates. It’s a complex area where professional discretion is required. We find that many clients benefit from a review of their group structure to ensure it remains commercially pragmatic. Our team can provide bespoke tax planning advice to help you manage these thresholds effectively. Identifying these links early prevents the miscalculation of what is corporation tax for your specific business context.

The Compliance Timeline: Filing Obligations and Payment Deadlines

Directors often find the UK’s tax timeline counter-intuitive because of a specific procedural quirk. While most statutory filings follow the submission of a report, the payment for corporation tax is typically due before the tax return itself is filed. Understanding UK Corporation Tax overview requirements is essential to avoid HMRC’s automated penalty regime. For the majority of UK companies, the deadline to settle your tax liability is exactly nine months and one day after the end of your accounting period. However, the actual CT600 tax return isn’t due until 12 months after that same period ends. This three-month discrepancy often catches unadvised directors off guard, leading to avoidable interest charges on late payments.

The submission process is strictly digital. We ensure all filings utilize the CT600 form accompanied by accounts in iXBRL format. This technical standard allows HMRC’s systems to process financial data with precision. If a company misses the filing deadline by a single day, an immediate £100 penalty applies. Should the delay reach six months, HMRC levies an additional penalty equal to 10% of the unpaid tax. Maintaining meticulous, professional records isn’t just a matter of good practice; it’s a statutory safeguard against these escalating costs. Working with a proactive small business accountant who anticipates these deadlines rather than reacting to them can be the difference between seamless compliance and costly penalties.

Navigating the Accounting Period

Your financial year-end serves as the anchor for your entire tax calendar. While most firms operate on a standard 12-month cycle, specific scenarios like business start-ups or changes in year-end dates can result in a “long” accounting period. Since a single tax return cannot exceed 12 months, we manage these instances by preparing two separate returns to cover the extended timeframe. Aligning your tax year with your natural business cycle is a pragmatic choice that simplifies reporting and supports healthier cash flow management. Determining what is corporation tax liability accurately relies entirely on these defined periods.

Quarterly Instalment Payments (QIPs)

Larger corporate entities operate under a different, more demanding payment structure. Companies with taxable profits exceeding £1.5 million are classified as “large” and must pay their tax in four quarterly instalments. This profit threshold is divided by the number of associated companies under common control, which can pull smaller subsidiaries into the QIPs regime. For “very large” companies with profits exceeding £20 million, the first payment is due as early as two months and 13 days into the accounting period. HMRC applies a rigorous interest regime to any underpaid instalments, making bespoke financial forecasting a vital component of your commercial strategy.

Optimising Your Position: Essential Reliefs and Allowances

Understanding what is corporation tax represents only the first step in effective fiscal management. We believe that true commercial efficiency stems from the meticulous application of statutory reliefs. These mechanisms aren’t merely concessions; they’re strategic tools designed to incentivise reinvestment and innovation within the UK economy. By aligning your business activities with these incentives, you can protect your cash flow and support long-term growth objectives.

Capital Allowances and Full Expensing

The UK’s capital allowance regime underwent a significant shift following the 2023 Autumn Statement, which made ‘Full Expensing’ permanent. This allows companies to claim a 100% first-year allowance on qualifying new plant and machinery investments. For every £1 invested, your company can immediately deduct the full cost from its taxable profits. Smaller enterprises typically utilise the Annual Investment Allowance (AIA), which offers a 100% deduction on the first £1 million of qualifying expenditure. We find that many businesses fail to distinguish correctly between revenue expenses and capital items, which can lead to missed opportunities for immediate tax relief.

Loss Relief Strategies

Trading losses don’t need to be a permanent drain on your balance sheet. The current framework provides several pathways to recover value:

- Carry forward: You can carry losses forward indefinitely to offset future trading profits, effectively reducing what is corporation tax in subsequent years.

- Carry back: Losses can be carried back 12 months to offset profits from the previous period, often resulting in a welcome tax refund from HMRC.

- Group relief: If your business operates within a group where there’s 75% common ownership, profitable companies can absorb the losses of others to lower the collective tax burden.

Innovation and Intellectual Property

As we look toward 2026, the merged Research and Development (R&D) tax credit scheme remains a cornerstone of the UK’s innovation strategy. Companies can claim a credit worth 20% of qualifying expenditure, providing a direct boost to those developing new products or processes. For those holding qualifying intellectual property, the Patent Box regime is equally vital. It applies a reduced 10% rate of Corporation Tax to profits derived from patented inventions. Our team provides bespoke corporate tax advisory services to ensure your business remains compliant while maximising these sophisticated reliefs.

Strategic Tax Management: How Davis & Co LLP Supports Your Business

Davis & Co LLP views tax as a dynamic component of your commercial narrative. Compliance is our baseline. We focus on proactive, bespoke planning that anticipates legislative shifts rather than reacting to them. Since the main rate rose to 25% on 1 April 2023, the margin for error in financial planning has narrowed. Our international expertise helps firms scale across borders while managing the complexities of permanent establishment and double taxation treaties. We maintain a pragmatic relationship with HMRC, ensuring statutory reporting is precise and defensible. This reduces friction and allows your leadership team to focus on growth. Understanding what is corporation tax is simply the starting point for any director; managing its impact on your cash flow is where we provide value.

- Integrating tax strategy with long-term capital expenditure plans.

- Managing the transition between the 19% small profits rate and the 25% main rate.

- Advising on R&D tax credits and Patent Box claims to incentivise innovation.

- Coordinating statutory accounts with the CT600 filing to ensure total consistency.

Bespoke Solutions for Complex Structures

Family offices and multi-jurisdictional entities require a level of nuance that standard accounting firms often overlook. We tailor our advice to suit these intricate frameworks, ensuring that wealth is preserved and corporate obligations are met with total discretion. Our company secretarial services work in tandem with our tax team. This ensures that every board resolution or share transfer aligns perfectly with your tax filing requirements. We pride ourselves on a culture of quiet excellence, providing the professional gravitas necessary to handle sensitive commercial matters.

Next Steps for Your Corporate Tax Planning

Effective management begins long before the filing deadline. A pre-year-end tax review is essential. For companies with a 31 March year-end, conducting a review in January allows for the strategic timing of dividends, pension contributions, or asset purchases. Our dedicated advisors understand the specific pressures of your sector, whether you operate in legal services, technology, or real estate. To secure your firm’s financial future, you can initiate a consultation with our senior partners. We’ll examine your current structure and identify where a more refined approach to what is corporation tax can improve your bottom line. We’re here to act as your steady, dependable partner in an evolving regulatory environment.

Navigating Your 2026 Corporate Tax Obligations

Managing your limited company’s tax position in 2026 requires more than just a surface-level awareness of the 25% main rate. It demands a proactive approach to statutory filing cycles and a clear grasp of the small profits threshold. You’ve seen how identifying specific capital allowances and R&D reliefs can significantly protect your firm’s liquidity. While understanding what is corporation tax remains the fundamental starting point, the real value for your business lies in sophisticated, long-term strategic planning. It’s about ensuring your commercial objectives aren’t hindered by unforeseen liabilities.

Since 1901, Davis & Co LLP has provided understated, professional expertise to UK businesses navigating complex fiscal landscapes. We specialise in the intricate tax planning required for both domestic and international operations, ensuring every bespoke solution aligns with your specific needs. Our partners bring over a century of reliability and discretion to your financial affairs, helping you move beyond simple compliance toward genuine fiscal optimisation. We invite you to discover how our bespoke tax advisory can optimise your corporate position. With the right expert partnership, your business is well-placed to thrive throughout 2026 and beyond.

Frequently Asked Questions

When is the deadline for paying Corporation Tax in the UK?

You must pay your Corporation Tax within nine months and one day after the end of your company’s accounting period. For a financial year ending on 31 December, your payment is due by 1 October the following year. It’s vital to remember that the payment deadline is earlier than the filing deadline for your Company Tax Return, which is typically 12 months after your accounting period ends.

What is the current Corporation Tax rate for 2026?

The Corporation Tax rate for 2026 is scheduled to maintain the two-tier structure introduced in April 2023. Companies with taxable profits below £50,000 pay the small profits rate of 19%, while those exceeding £250,000 are subject to the main rate of 25%. A tapered relief system applies to businesses falling between these figures. Understanding what is corporation tax and its impact on your cash flow is vital for long-term fiscal planning.

Can I pay my Corporation Tax in instalments?

You can only pay in instalments if your company’s taxable profits exceed £1.5 million in a single accounting period. These Quarterly Instalment Payments require four payments throughout the year, typically starting six months and thirteen days into the period. For most small to medium enterprises with profits below this £1.5 million threshold, a single annual payment remains the standard statutory requirement for tax compliance.

How do I register my new company for Corporation Tax with HMRC?

You must register for Corporation Tax within three months of starting to do business, which includes buying, selling, or renting property. Most directors complete this process online via the HMRC portal alongside their initial Companies House registration. We suggest having your 10-digit Unique Taxpayer Reference (UTR) and company registration number ready to ensure the registration is processed without administrative delay or potential fines for late notification.

What happens if my company makes a loss instead of a profit?

If your company records a trading loss, you won’t pay Corporation Tax for that specific period. You can often use this loss to claim “loss relief” by carrying it back one year to offset against previous profits or carrying it forward to reduce future tax liabilities. For example, a £10,000 loss this year could potentially generate a tax refund if your company paid tax on £10,000 of profit in the preceding 12 months.

Is Corporation Tax paid on turnover or profit?

Corporation Tax is paid on your company’s annual taxable profit rather than its total turnover. You calculate this figure by taking your total revenue and subtracting allowable business expenses, such as staff wages and commercial insurance. Understanding what is corporation tax involves recognising that only the net earnings are subject to the levy. This ensures that the tax burden reflects the actual financial success of your business operations.

Do I need to pay Corporation Tax if my company is dormant?

You don’t need to pay Corporation Tax if your company is officially dormant for tax purposes. A company is considered dormant by HMRC if it hasn’t traded, received any income, or incurred significant expenses during the financial year. You’ll still need to inform HMRC of your dormant status to avoid receiving unnecessary tax returns. Maintaining accurate records is essential to prove the company has no taxable activities during this period.

What are the penalties for late Corporation Tax returns?

HMRC applies an immediate £100 penalty if your return is just one day late. This fine increases by another £100 if the return remains unfiled after three months. If your return is six months late, HMRC estimates your tax bill and adds a penalty equal to 10% of the unpaid tax. These charges double if you’re late for three consecutive accounting periods, making timely compliance a significant commercial priority for your firm.