In the current fiscal climate, a property development project’s success is determined in the boardroom long before the first spade hits the ground. We understand that unpredictable tax liabilities can quickly erode project liquidity, particularly when legislative volatility follows recent UK budgets. Effective property development tax planning is no longer just about compliance; it’s a fundamental pillar of risk management. You’ve likely felt the pressure of complex VAT recovery rules and the shifting sands of SDLT, making it difficult to forecast true net margins with the precision your stakeholders expect.

This guide provides the strategic clarity you need to protect your development margins through sophisticated corporate structuring and proactive tax mitigation. We’ll explore a clear framework for organizational design that accounts for the 25% corporation tax rate and the dividend tax increases taking effect in April 2026. You’ll discover how to maximize VAT and SDLT mitigation across various build types while building a robust exit strategy that preserves your capital. By the end, you’ll have a roadmap to transform tax from an unpredictable overhead into a managed strategic variable.

Key Takeaways

- Understand how recent legislative shifts necessitate a transition toward proactive property development tax planning as a primary tool for managing project liquidity.

- Explore the strategic use of Special Purpose Vehicles (SPVs) and holding companies to isolate commercial risks and optimize inter-company lending.

- Navigate the complexities of VAT recovery and SDLT surcharges to ensure your build’s profitability isn’t undermined by avoidable tax leakage.

- Discover how to unlock capital through Land Remediation Relief and enhanced capital allowances for qualifying plant and machinery.

- Design a sophisticated exit strategy that balances disposal timing with Capital Gains Tax mitigation to maximize your final returns.

The 2026 Landscape for Property Development Tax Planning

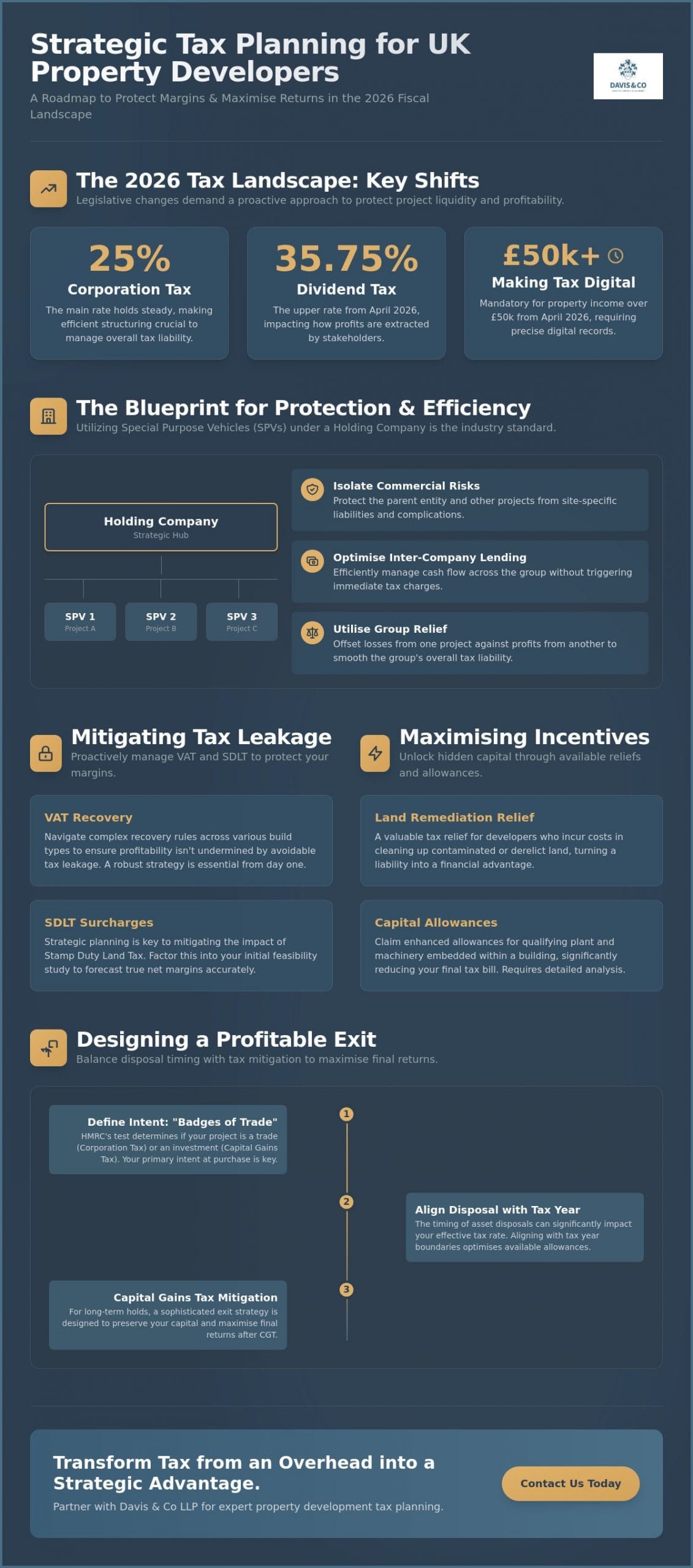

The fiscal environment for UK developers has undergone a significant transformation. We’ve seen the main rate of Corporation Tax hold steady at 25% while dividend tax rates climbed by 2% in April 2026, bringing the upper rate to 35.75%. These adjustments aren’t merely administrative hurdles; they’re variables that directly dictate whether a project remains liquid or becomes a liability. Effective property development tax planning now serves as a proactive risk-management tool. It allows us to anticipate cash flow requirements months before they impact the balance sheet. If you rely on reactive accounting, you’re essentially looking in the rearview mirror while navigating a volatile market. The recent budget shifts have tightened margins, making it vital to balance commercial agility with a defensive, compliant posture.

Waiting until the end of the financial year to assess your liabilities often leads to missed opportunities for relief. For instance, the transition to mandatory Making Tax Digital (MTD) for Income Tax in April 2026 for those with property income over £50,000 requires a level of digital precision that traditional spreadsheets can’t provide. We believe that a robust tax strategy should be integrated into the initial feasibility study of every site. This ensures that the tax burden is factored into the gross development value from the outset, preserving the intended profit margin against legislative volatility.

The Shift Toward Structural Sophistication

The “one project, one company” model has moved from a niche strategy to an industry standard for mid-market developers. Using Special Purpose Vehicles (SPVs) provides a clean break between developments, protecting the parent entity from project-specific liabilities. Navigating these complexities requires expert tax advice in the UK to ensure that inter-company loans and management fees are structured to withstand scrutiny. With the 2026 Corporation Tax thresholds in play, the timing of asset disposals can significantly impact your effective tax rate. We focus on aligning project milestones with tax year boundaries to optimize the use of available allowances and prevent unnecessary bracket creep.

Navigating HMRC Scrutiny in 2026

HMRC’s focus has sharpened, with a particular emphasis on identifying “red flags” in property accounts. These often include inconsistent treatment of professional fees or unsubstantiated claims for Land Remediation Relief. Robust documentation isn’t just a requirement; it’s your primary defense. Whether your exit strategy involves Capital Gains Tax on a long-term hold or Corporation Tax on a quick flip, the underlying paper trail must be impeccable. HMRC determines the distinction between property development trading and investment through the “badges of trade” test, focusing on the developer’s primary intent at the time of purchase and the degree of organization involved in the project.

Optimal Corporate Structuring for Multi-Site Developments

For developers managing multiple concurrent projects, the organizational blueprint is just as critical as the architectural one. Utilizing Special Purpose Vehicles (SPVs) allows for the isolation of project-specific risks, ensuring that a single site’s complications don’t jeopardize the entire portfolio’s stability. This structure is a cornerstone of sophisticated property development tax planning, as it provides a clean financial record for each project. It’s a disciplined approach. One that demands foresight. While the administrative burden of maintaining multiple entities is higher, the protection afforded to the developer’s core assets far outweighs the incremental cost of compliance. A central Holding Company serves as the strategic hub, facilitating inter-company lending and efficient cash flow management across the group.

The Holding Company and SPV Model

The primary advantage of a group structure lies in the ability to utilize Group Relief. This mechanism allows us to offset losses from a developing project against the taxable profits of a completed one, effectively smoothing the group’s overall tax liability. It’s particularly useful when navigating the 25% Corporation Tax rate. Moving funds between subsidiaries via inter-company loans can be achieved without triggering immediate tax charges, provided the transactions are documented at arm’s length. This structural sophistication is also relevant when identifying opportunities for Stamp Duty Land Tax relief, as certain corporate reorganizations may qualify for specific exemptions that preserve project liquidity during the acquisition phase.

International Capital and Overseas Investors

Cross-border investment into UK residential property requires a more nuanced approach to international tax planning. Non-resident developers must navigate the Non-Resident Capital Gains Tax (NRCGT) regime, which in 2026 continues to apply to both direct and indirect disposals of UK land. Reporting requirements are stringent, often necessitating filings within 30 days of completion. Structuring debt and equity correctly is vital to optimize cross-border efficiency, especially when considering the impact of withholding taxes on interest payments. We focus on ensuring that the funding mix respects thin capitalization rules while maximizing the deductibility of financing costs against UK profits. Refining your corporate structure isn’t a one-time task but an ongoing part of your Property Accounting cycle, ensuring your portfolio remains resilient against both commercial and fiscal pressures.

Directors and shareholders must also consider profit extraction with precision. With the upper dividend tax rate at 35.75% and the tax-free allowance capped at £500, the traditional “salary plus dividend” model requires careful recalibration. We often explore alternative methods, such as employer pension contributions or the strategic timing of bonuses, to ensure that the rewards of a successful development aren’t disproportionately eroded by personal tax liabilities. This holistic view of property development tax planning ensures that the wealth generated at the corporate level is preserved as it transitions to the individual.

Mitigating the Impact of SDLT and VAT on Margins

Transactional taxes represent the most immediate drain on a project’s liquidity. Unlike Corporation Tax, which is calculated on realized profits, Stamp Duty Land Tax (SDLT) and Value Added Tax (VAT) impact cash flow from the very beginning. Sophisticated property development tax planning requires a granular understanding of how these levies interact with different build types. In 2026, the additional property surcharge remains a significant factor, with rates for corporate purchases starting at 5% even for the lowest band. Failing to account for these surcharges during the acquisition phase can lead to a significant discrepancy in your initial capital requirements, often before the first contractor has been appointed.

We believe that managing these costs is not about evasion but about precise classification. The difference between a residential and non-residential rate can be the margin that makes a project viable. In a landscape of 25% Corporation Tax and rising construction costs, every percentage point of unrecoverable tax is a direct hit to your bottom line. We prioritize a proactive approach that integrates tax forecasting into the earliest stages of procurement and site assessment.

Strategic SDLT Planning

Large-scale land acquisitions in 2026 demand a rigorous analysis of classification. The distinction between purely residential and mixed-use land is pivotal. Mixed-use properties often benefit from non-residential SDLT rates, which are generally lower than the higher-rate residential bands that can reach as high as 17% for additional properties. We focus on identifying whether a site legitimately qualifies for this classification, as the savings on a multi-million-pound acquisition are substantial. Regarding the 2026 rules for SDLT refunds on uninhabitable properties, HMRC has tightened the criteria, requiring objective evidence that a dwelling is structurally unsuitable for occupation at the time of purchase to qualify for non-residential treatment.

VAT Optimisation for New Builds and Conversions

VAT recovery is the silent engine of development profitability. While the standard rate remains at 20%, the zero-rating of new residential construction allows developers to recover input tax on most professional fees and materials. However, mixed-use developments often fall into a VAT trap where input tax must be apportioned between taxable and exempt supplies. This complexity is why we advocate for the use of monthly returns to accelerate cash recovery. If your project involves converting a non-residential building into dwellings, you may benefit from the 5% reduced rate, provided the property has been empty for at least two years.

Structuring contracts with subcontractors is equally vital. Ensuring that the correct VAT rate is applied at the source prevents the developer from being taxed on capital gains or income that is artificially inflated by unrecoverable VAT. Misapplying a zero-rate to a conversion project can lead to significant penalties, making the distinction between renovation and reconstruction a critical legal boundary. We recommend a thorough review of all procurement routes to ensure that maximum recoverability is baked into the project’s financial DNA from the outset.

Maximising Incentives: Capital Allowances and Remediation Relief

While previous sections focused on defensive structuring and managing transactional costs, sophisticated property development tax planning also involves the pursuit of available incentives. These reliefs aren’t just bonuses; they’re essential for the viability of complex sites, particularly in urban regeneration. We’ve seen many developers overlook these incentives, viewing them as administrative burdens rather than the margin-boosters they truly are. In a fiscal year where the main Corporation Tax rate is 25%, failing to utilize these statutory reliefs is a significant oversight that directly impacts your project’s internal rate of return.

The 2026 landscape introduces new complexities for capital expenditure. While the Annual Investment Allowance (AIA) continues to offer 100% relief on up to £1 million of qualifying expenditure, the main rate of Writing Down Allowance (WDA) was reduced from 18% to 14% in April 2026. However, a new 40% First-Year Allowance for new and unused main-rate plant and machinery became available on January 1, 2026. Navigating these shifting rates requires a disciplined approach to procurement and asset classification.

Land Remediation Relief (LRR)

Land Remediation Relief remains one of the most effective tools for developers tackling brownfield sites. Companies can claim a corporation tax deduction of 150% of the qualifying expenditure on remediating contaminated land. This includes the removal of asbestos, radon, and even Japanese knotweed. For projects that are currently loss-making, there’s the option to surrender the loss for a payable tax credit of 16%. This provides a vital cash injection during the capital-intensive early stages of a development. We find that LRR often makes the difference in the feasibility of urban sites that would otherwise be commercially unviable due to high clean-up costs.

Capital Allowances on Fixtures and Fittings

Identifying qualifying expenditure within the “plant and machinery” category is paramount, especially in the common areas of residential blocks or commercial units. Integral features, such as electrical systems, lifts, and cooling systems, often represent a significant portion of the build cost. Since April 2026, the 14% WDA rate makes it even more important to identify every pound of qualifying expenditure early. We believe a specialist capital allowances survey is essential for high-value developments to ensure that no relief is left on the table. Precise documentation of these “integral features” allows for more aggressive, yet compliant, depreciation strategies that protect your project’s Cash Flow Management throughout the construction cycle.

Innovation in sustainable construction also opens doors to R&D tax credits. If your project utilizes novel modular methods or proprietary sustainable materials to solve specific technical challenges, a portion of those staff and material costs may be eligible for relief. This is a highly specialized area where the distinction between “standard practice” and “technical advancement” is key. Integrating these incentives into your overall property development tax planning ensures that you’re not just building structures, but also building a more tax-efficient business model for the long term.

Strategic Exit Planning and Capital Gains Optimisation

The conclusion of a development project shouldn’t be the point where you begin considering your exit strategy. In our experience, the most successful developers integrate their disposal plans into their initial property development tax planning framework. Whether you intend to sell the completed units immediately or retain them as part of a long-term rental portfolio, the tax implications vary significantly. Since April 2026, the rate for Business Asset Disposal Relief (BADR) has increased to 18%, up from the previous 14%. For higher-rate taxpayers, the Capital Gains Tax (CGT) on residential property stands at 24%. These rates, combined with a modest £3,000 annual exempt amount, mean that the timing of your exit is a critical factor in preserving your final margins.

We often advise clients to look beyond the immediate sale. Strategic timing of disposals can help you stay within specific tax brackets or utilize losses from other areas of your business. If you’re operating through a corporate structure, the interaction between Corporation Tax on trading profits and the eventual extraction of funds requires a balanced approach to ensure you aren’t taxed twice on the same economic gain. This foresight is what separates a transactional developer from a strategic wealth builder.

Transitioning from Development to Investment

When a developer decides to retain a property for long-term yield, the asset moves from “trading stock” to “fixed assets.” This transition is a “deemed disposal” for tax purposes, meaning you’re treated as having sold the property to yourself at market value. Managing this valuation process is vital to minimize tax leakage. If the market value is significantly higher than the build cost, you may face an immediate tax charge without the liquidity of a sale to cover it. Utilizing professional property accounting services is essential here to manage long-term yields and ensure that the base cost for future capital gains is correctly established.

Inheritance Tax and Wealth Preservation

For many of our clients, property development is a vehicle for multi-generational wealth. Family Investment Companies (FICs) have become an increasingly popular alternative to traditional trusts for holding property portfolios. They allow for the structured transfer of value to the next generation while the founders maintain control over the management and investment strategy. This is particularly relevant given the 2026 changes to Inheritance Tax (IHT). From April 6, 2026, a new combined limit of £2.5 million applies to Business Property Relief (BPR) and Agricultural Property Relief (APR) per person. To qualify for Business Relief in 2026, a property business must demonstrate that its activities are predominantly trading rather than investment, typically requiring a high level of active development or management rather than passive rental collection.

By aligning your exit strategy with your wider estate planning, we can help ensure that the capital you’ve worked hard to build is protected for the future. A robust approach to property development tax planning doesn’t just end with a successful build; it concludes with a secure transition of assets that respects both your commercial goals and your personal legacy.

Securing Your Development Margins in a Volatile Market

The transition toward structural sophistication and proactive mitigation is no longer optional in the 2026 fiscal year. We’ve explored how a disciplined approach to property development tax planning can safeguard your margins against the 25% Corporation Tax rate and rising transactional costs. By utilizing Land Remediation Relief and optimizing VAT recovery on conversions, you transform potential liabilities into strategic advantages. It’s about more than just numbers; it’s about building a resilient commercial legacy through precise corporate structuring and informed exit timing.

As Chartered Certified Accountants since 1901, we bring a history of reliability and deep-seated expertise to every project. We specialize in international and property tax planning, offering a composed partnership approach to the most complex financial matters. Our goal is to ensure you feel secure and well-advised as you navigate the intricacies of the UK’s legislative volatility. Consult with our strategic tax advisors to optimise your next development. We look forward to helping you secure the long-term success of your portfolio.

Frequently Asked Questions

Is it better to develop property as a sole trader or a limited company in 2026?

Operating through a limited company is generally the more efficient choice for developers in 2026. While the main Corporation Tax rate is 25%, this remains lower than the 42% or 47% higher rates of income tax scheduled for 2027. A corporate structure also facilitates the use of Special Purpose Vehicles, which are essential for isolating risk and managing project-specific finance without exposing your personal assets or other portfolio holdings.

What is the “VAT 5% rule” for property conversions?

The 5% reduced rate applies to the renovation or conversion of residential properties that have been empty for at least two years. This incentive is particularly valuable when converting non-residential buildings into dwellings or changing the number of units within an existing residential structure. It allows developers to significantly reduce their unrecoverable VAT burden on qualifying labor and materials, directly improving the project’s bottom line.

Can I claim Land Remediation Relief on a residential development?

Yes, companies can claim Land Remediation Relief on residential projects, provided the land was acquired in a contaminated state. This allows for a 150% corporation tax deduction on qualifying expenditure for cleaning up the site, including the removal of asbestos and Japanese knotweed. If the development company is loss-making, it may also be possible to surrender the loss for a 16% payable tax credit to aid liquidity.

How do SPVs help with property development tax planning?

SPVs are a cornerstone of property development tax planning because they ringfence the financial and tax obligations of a single project. This isolation prevents a loss on one site from automatically jeopardizing the solvency of the wider group. Structuring each development within its own SPV also provides a cleaner path for an eventual exit, as it allows for the sale of the company’s shares rather than just the underlying asset.

What are the main SDLT reliefs available to property developers?

Developers often utilize the non-residential SDLT rates for mixed-use acquisitions, which can be significantly lower than the higher-rate residential bands. Another critical area involves claiming refunds for properties that were structurally uninhabitable at the time of purchase. While HMRC has tightened the criteria in 2026, objective evidence of significant structural defects can still justify a reclassification to the lower non-residential rates, preserving vital capital during the acquisition phase.

How does the 2026 Corporation Tax rate affect my development profits?

The 25% main rate of Corporation Tax applies to all profits over £250,000, which requires a more disciplined approach to expense management and relief claims. For developers with profits below £50,000, the 19% small profits rate still provides some protection. However, most mid-market developments will fall into the higher bracket, making it essential to maximize capital allowances and other statutory reliefs to protect the net internal rate of return.

Can I offset development losses against my other personal income?

If you are developing through a limited company, you cannot offset project losses against your personal income from other sources. The company’s losses are contained within the corporate structure, though they can be carried forward to offset future profits within the same company or utilized across a group via Group Relief. Sole traders may have more flexibility through sideways loss relief, but this is often subject to strict caps and commerciality tests.

What is the difference between property trading and property investing for tax purposes?

The distinction lies in your primary intent, which HMRC assesses using the “badges of trade” test. Property trading involves acquiring and developing land with the specific intention of selling it for a profit, which is taxed as income or corporate profit. Property investing involves holding an asset for long-term rental yield and capital appreciation, which falls under the Capital Gains Tax regime upon disposal. Each path requires a fundamentally different tax strategy.