Could the total abolition of the UK’s non-domicile regime on 6 April 2025 actually be the catalyst your international wealth strategy requires? Many high-net-worth individuals feel a justified sense of unease as the transition to a residence-based system approaches. We recognise the complexity you face when reporting foreign assets to HMRC, especially with the 2026 reporting requirements looming. Securing professional cross border tax advice shouldn’t be a source of stress; it’s a strategic necessity to prevent the 40% tax traps that often catch the unwary during periods of legislative shift.

We’re committed to ensuring your global footprint remains both compliant and tax-efficient. You’ll learn to master the complexities of international tax residency, leverage double taxation agreements effectively, and build a strategic plan for your wealth. This article provides a clear, bespoke roadmap for managing your global assets while meeting your pragmatic commercial objectives under the latest statutory frameworks.

Key Takeaways

- Understand how the evolving landscape of global transparency and 2026 legislative shifts demand a more sophisticated approach to international compliance.

- Master the application of the Statutory Residence Test to clarify your UK tax position and manage the nuances of automatic residency and sufficient ties.

- Utilise Double Taxation Agreements to safeguard your assets and secure specialist cross border tax advice regarding the hierarchy of international taxing rights.

- Explore bespoke strategic planning for managing UK property and international business interests while maintaining a non-resident status for tax purposes.

- Align your commercial objectives with private wealth protection through a collaborative partnership designed to provide stability in a volatile regulatory environment.

The Evolving Landscape of Cross-Border Taxation in 2026

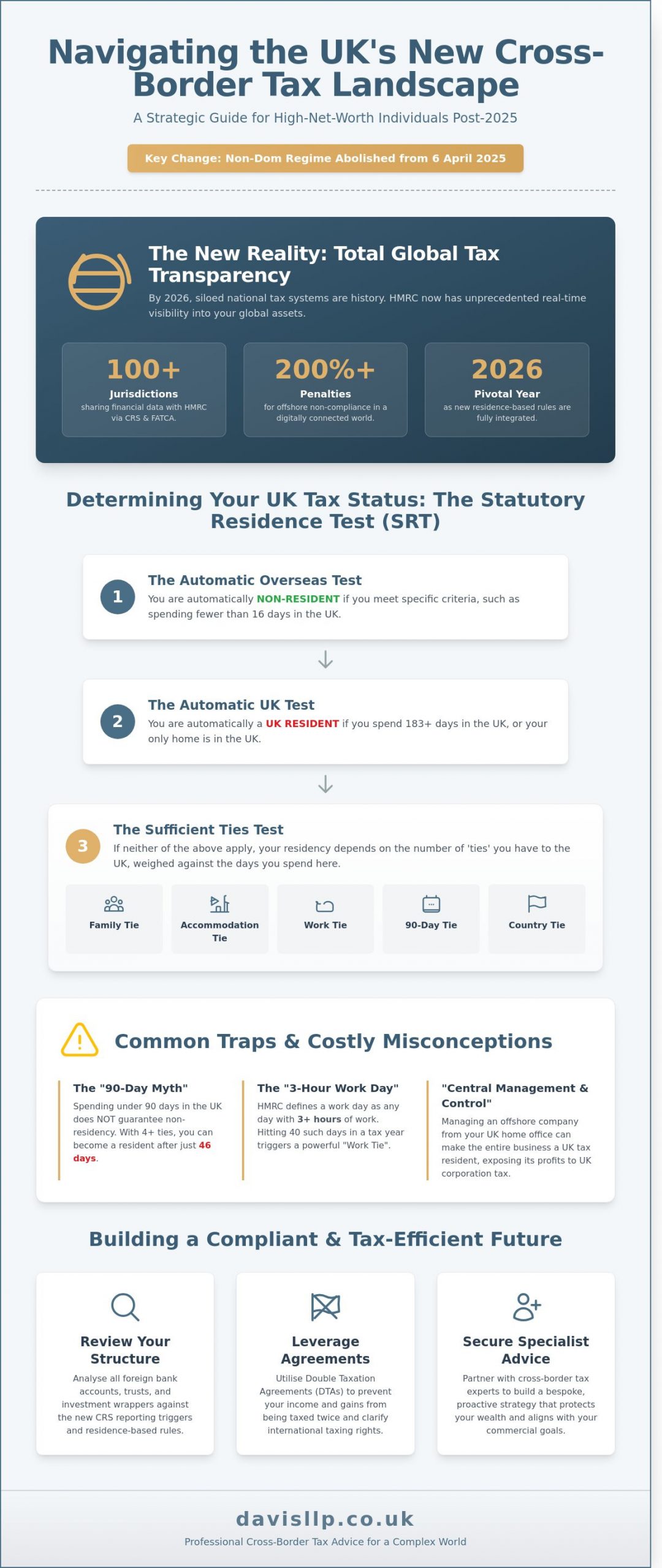

The global tax environment has reached a point of total visibility. By 2026, the era of siloed national tax authorities has effectively ended. HMRC now operates within a network of over 100 jurisdictions through the Common Reporting Standard (CRS) and FATCA. This automated data sharing ensures that offshore accounts, trusts, and complex investment structures are visible to the Revenue in real time. Relying on legacy structures is no longer a viable strategy for high-net-worth individuals or international corporations.

We’ve observed that traditional tax planning requires a complete refresh following the legislative overhaul that began in April 2025. The intersection of personal liability and corporate tax residency has become a primary focus for HMRC. If you’re a director managing an offshore entity from a UK home office, the Revenue may now seek to classify that business as a UK tax resident under the “central management and control” test. This makes seeking professional cross border tax advice early in the financial year a matter of risk mitigation rather than mere administrative preference.

The Impact of Global Tax Transparency

HMRC’s digital capabilities have expanded to process millions of data points from international financial institutions annually. The risks of non-disclosure in a digitally connected tax world are severe, with statutory penalties for offshore non-compliance often exceeding 200% of the tax due. We help clients move from reactive compliance to a proactive international strategy. This involves:

- Reviewing all foreign bank accounts and investment wrappers against CRS reporting triggers.

- Analysing the tax treaty network to prevent double taxation on dividends and capital gains.

- Implementing bespoke reporting frameworks that align with the 2026 transparency standards.

Why 2026 is a Pivotal Year for International Clients

The transition from the traditional domicile rules to a residence-based system, which was fully integrated by April 2026, has fundamentally changed the obligations of long-term UK residents. Under the new FIG (Foreign Income and Gains) regime, those who’ve been resident in the UK for more than 10 of the last 20 tax years can no longer shield offshore earnings from UK tax. It’s a significant departure from the old remittance basis that defined the last century of UK tax law. The modernised tax landscape for 2026 represents a shift toward transparency and residence-based assessment. Engaging with cross border tax advice allows for a pragmatic review of how these residence rules impact your global wealth and corporate holdings.

Determining Tax Residency: The Statutory Residence Test and Beyond

The Statutory Residence Test (SRT), established by the Finance Act 2013, serves as the definitive mechanism for determining UK tax liability. It’s a structured, three-part assessment that replaces the subjective “intent” of previous decades with clinical, day-count precision. Your residency status is the pivot upon which your global tax obligations turn. If you’re classified as a UK resident, HMRC typically claims taxing rights over your worldwide income and gains, making early cross border tax advice a strategic necessity for high-net-worth individuals.

- The Automatic Overseas Test: You’re generally non-resident if you spend fewer than 16 days in the UK, provided you were resident in any of the previous three tax years.

- The Automatic UK Test: Residency is triggered if you spend 183 days or more in the UK during the tax year or if your only home is in the UK for at least 91 days.

- The Sufficient Ties Test: This applies if neither of the above is met, weighing factors like family, accommodation, and work against the number of days spent in the country.

Navigating the Statutory Residence Test (SRT)

Misconceptions regarding the “90-day rule” often lead to costly compliance errors. While 90 days is a threshold for the “90-day tie,” it doesn’t grant automatic non-residency. We’ve seen cases where individuals became residents with only 46 days in the country because they held four or more specific ties. Substantive work is another frequent trap. HMRC defines a work day as any day where 3 hours or more of work are performed; reaching 40 such days in a tax year triggers a work tie. For 2026, maintaining a digital log of every midnight spent in the UK is the only way to ensure your position is defensible during an enquiry.

Split-Year Treatment and Leaving the UK

Leaving the UK for work or retirement requires careful timing to qualify for split-year treatment. This allows you to be taxed as a non-resident from the date of your departure, rather than the following April. However, the Temporary Non-Residence rules act as a safeguard for the Revenue. If you return to the UK within five years of leaving, certain capital gains realised on assets held before departure may be taxed in the year of your return. We provide bespoke solutions to help clients structure their exits so they don’t fall foul of these 5-year clawback provisions. This intellectual rigour ensures your transition remains a private, well-managed commercial objective.

Double Taxation Agreements: Protecting Your Global Assets

A Double Taxation Agreement is a bilateral treaty designed to prevent the same income from being taxed by two different countries. These instruments serve as the bedrock of cross border tax advice, providing a structured hierarchy that dictates which jurisdiction possesses the primary taxing right. Without these treaties, international investors would frequently face the prospect of paying tax on the same pound of profit in both the country of origin and their country of residence. By establishing these rules, DTAs ensure that the total tax burden remains equitable and predictable.

The mechanism for avoiding double payment is usually Foreign Tax Credit Relief (FTCR). Under this system, the tax paid in the source country is offset against the liability in the residence country. For corporate groups, we often utilise “Treaty Passport” schemes. These allow overseas entities to receive interest or royalty payments with a reduced rate of withholding tax applied at source, rather than waiting for a lengthy rebate process. As of 2024, HMRC’s Double Taxation Treaty Passport (DTTP) register includes over 2,500 active participants, reflecting its utility for modern commercial operations.

How DTAs Work in Practice

Residency disputes are resolved through “Tie-Breaker” clauses, typically following Article 4 of the OECD Model Tax Convention. These clauses prioritise a taxpayer’s permanent home and centre of vital interests over mere physical presence. Most agreements specifically address three core asset classes: dividends, interest, and royalties. For instance, the UK-US treaty can reduce dividend withholding tax from 30% to 15%, provided the claimant meets specific “Limitation on Benefits” criteria.

Claiming Relief and Compliance

Claiming treaty benefits is a proactive requirement, not an automatic entitlement. In the UK, individuals must report foreign income and claim FTCR on the SA106 supplementary pages of their tax return. HMRC demands precise documentation, including foreign tax vouchers and certificates of residence, to substantiate these claims. We find that neglecting these bespoke requirements can lead to effective tax rates exceeding 55% on certain portfolios. Providing rigorous cross border tax advice involves ensuring every document aligns with the specific treaty’s provisions to mitigate the risk of a discovery assessment.

Strategic Planning for Expats and International Businesses

Effective international expansion requires a granular understanding of the structural distinctions between foreign branches and subsidiaries. A subsidiary acts as a separate legal entity, often shielding the parent company from local liabilities, while a branch remains an extension of the UK head office. By April 2026, the choice between these structures often hinges on the specific double taxation treaty in place. We assist clients in navigating these choices to ensure that withholding tax on dividends, which can reach 30% in certain jurisdictions without treaty relief, is legally minimised. Our approach focuses on long term stability rather than temporary gains.

Tax-Efficient Business Expansion

Transfer pricing remains a focal point for HMRC. Since the 2023 introduction of stricter Transfer Pricing Documentation Requirements, businesses must maintain robust Master and Local files. Ensuring inter company charges reflect the “arm’s length” standard is not merely a compliance task; it’s a defensive strategy against costly audits. We help our clients establish pricing policies that satisfy the OECD’s 2026 guidelines while supporting commercial objectives. This precision prevents the double taxation of profits and ensures that cross border tax advice translates into tangible bottom line protection.

Personal Wealth and Property

Managing UK property from abroad involves specific statutory obligations that non-residents cannot afford to overlook. The Non-Resident Landlord Scheme requires letting agents to deduct 20% tax at source unless HMRC grants an express exemption. When selling, Non-Resident Capital Gains Tax applies to both residential and commercial assets. For non-domiciled individuals, 2026 marks a pivotal shift. Following the transition to a residence-based system, individuals may face a 40% Inheritance Tax charge on worldwide assets after 10 years of UK residence. We provide bespoke cross border tax advice to help families restructure their holdings, often utilising family offices or excluded property trusts to preserve wealth. Our international tax planning guide for 2026 sets out a comprehensive framework for adapting to these residence-based changes and protecting your global asset base.

To prepare for a 2026 tax review, we recommend expats compile the following documents:

- Annual income statements and P60 equivalents from all jurisdictions of residence.

- Comprehensive valuations for all UK-situs assets, including residential property and private shares.

- Detailed logs of days spent in the UK to satisfy the Statutory Residence Test.

- Current trust deeds and letters of wishes for any offshore structures.

If you require a bespoke strategy for your international assets, contact our private client team for a confidential consultation.

Bespoke Cross-Border Solutions with Davis & Co LLP

At Davis & Co LLP, our Chartered Certified Accountants provide more than technical compliance; we offer a composed partnership designed to withstand the complexities of global regulation. We understand that by 2026, the intersection of UK statutory requirements and international treaties requires a steady hand. Our approach focuses on the dual necessity of meeting your commercial objectives while ensuring robust private wealth protection. This “quiet excellence” ensures your financial security remains undisturbed by the volatility of shifting tax jurisdictions. We don’t just react to changes; we anticipate them to keep your interests secure.

Our International Tax Expertise

We’ve built a reputation for resolving complex HMRC enquiries, maintaining a success rate that reflects our intellectual rigour and attention to detail. Generic, off-the-shelf tax products often fail because they ignore the nuance of individual circumstances. Instead, we develop a tailored strategy for every client, ensuring that cross border tax advice is integrated into your broader financial life. We coordinate with a network of international partners in over 50 jurisdictions to ensure your global compliance is seamless. This proactive stance helps you avoid the 200% penalties often associated with undeclared offshore income under the Common Reporting Standard. If you are evaluating your options, our guide to selecting an international tax advisor in London provides a practical framework for identifying the right specialist for your circumstances.

- Detailed analysis of double taxation treaties to prevent overpayment.

- Strategic restructuring of international holdings for tax efficiency.

- Comprehensive support for high-net-worth individuals moving between jurisdictions.

- Expert representation during statutory audits and enquiries.

Commencing Your Tax Review

Your first advisory session is a structured exploration of your current position and future aspirations. We treat every matter with absolute discretion, applying the same precision to a family trust as we do to a multinational corporate structure. Our goal is to provide a clear, actionable roadmap that simplifies the intricacies of your international affairs. We’ve helped clients navigate the 2024 changes to non-domiciled status, and we’re ready to apply that same expertise to your 2026 planning. It’s a process rooted in clarity and professional distance.

Our firm operates as a strategic partner, ensuring your legacy and business interests remain protected for the decades ahead. To begin this process, you can enquire about our bespoke cross-border tax advice today. We’ll ensure your international transition is handled with the deliberate care it deserves.

Securing Your Global Interests for 2026 and Beyond

Navigating the complexities of international compliance in 2026 requires more than just awareness; it demands a proactive approach to the Statutory Residence Test and a precise application of Double Taxation Agreements. As global regulations tighten, the margin for error in your financial reporting diminishes. Protecting your assets across multiple jurisdictions hinges on strategic foresight and a deep understanding of evolving statutory requirements. Historical data shows how quickly these landscapes shift. Professional oversight isn’t just an option; it’s a necessity.

At Davis & Co LLP, we bring over 120 years of heritage as Chartered Certified Accountants to every engagement. We act as a strategic partner for both commercial entities and private clients, ensuring your international interests remain robust and compliant. Our specialists provide the expert cross border tax advice necessary to navigate these shifting landscapes with absolute discretion. We focus on delivering bespoke solutions that align with your specific commercial objectives while safeguarding your personal wealth.

We’re ready to ensure your transition into the 2026 tax year is seamless. Contact our international tax specialists for a bespoke consultation to discuss your global ambitions. You can move forward with total confidence in your international standing.

Frequently Asked Questions

Do I need to pay UK tax if I live abroad but have a UK rental property?

You’re required to pay UK income tax on any profit generated from UK rental property, regardless of your residence abroad. Under the Non-Resident Landlord Scheme, tenants or letting agents usually deduct a 20% basic rate tax before you receive payment. We provide bespoke cross border tax advice to help you claim your £12,570 personal allowance if you’re a British citizen or EEA national. This ensures your property portfolio remains commercially viable and compliant.

What happens if I am considered a tax resident in two different countries?

If you’re considered a resident in two jurisdictions, the relevant Double Taxation Agreement (DTA) determines where you pay tax. These treaties use tie-breaker rules, often found in Article 4, to assess your permanent home or centre of vital interests. It’s a complex area where we provide strategic guidance to prevent double exposure. We’ll examine your specific circumstances to ensure you’re not paying more than the law requires in either territory.

How does the Statutory Residence Test affect my tax status in 2026?

The Statutory Residence Test (SRT) functions as the primary mechanism for establishing your UK tax status through three distinct stages. In 2026, the 183-day rule remains the definitive threshold for automatic residency. If you spend fewer days in the UK, we’ll evaluate the sufficient ties test, which considers factors like your accommodation and work hours. Precise record-keeping is essential because even a single day can shift your entire fiscal responsibility.

Can I claim back tax paid in a foreign country against my UK tax bill?

You can generally claim Foreign Tax Credit Relief (FTCR) to reduce your UK tax bill by the amount of tax already paid overseas. This relief is restricted to the lower of the foreign tax paid or the UK tax due on that same income. It’s a vital tool for those seeking cross border tax advice to avoid being taxed twice on the same dividends or earnings. We’ll manage the HMRC filings to ensure these credits are applied accurately.

Are there special tax rules for digital nomads working for UK companies?

Digital nomads working for UK firms from abroad generally fall outside the UK tax net if they spend fewer than 183 days in the country. However, the UK employer might still need to operate PAYE unless they’ve secured an NT tax code from HMRC. Your tax liability usually shifts to your country of physical residence. We help individuals and companies navigate these remote working structures to maintain statutory compliance across borders.

What are the penalties for failing to declare offshore income to HMRC?

HMRC imposes stringent penalties for undeclared offshore income, which can reach 200% of the tax owed under the Requirement to Correct rules. Beyond these financial costs, you may face public naming and shaming or even criminal prosecution for deliberate evasion. Since the 2018 introduction of the Common Reporting Standard, HMRC receives automatic data from over 100 jurisdictions. We offer a discreet service to help you make voluntary disclosures and regularise your affairs.

How do the 2026 changes to non-dom status affect my existing tax plan?

The abolition of the remittance basis on 6 April 2025 means your existing tax plan likely needs an immediate, comprehensive review. From 2026, new residents only receive a 100% relief on foreign income for their first four years of residency. After this period, you’ll pay UK tax on your worldwide income regardless of where it’s held. We’ll help you restructure your assets to adapt to this residence-based system and protect your long-term wealth.

Is inheritance tax applicable to UK assets held by non-residents?

UK-situated assets, such as residential property or shares in UK companies, are subject to Inheritance Tax (IHT) even if you’re a non-resident. HMRC applies a 40% tax rate on the value of these assets exceeding the £325,000 nil-rate band. This rule applies regardless of your domicile status under the new 2025/2026 regulations. We provide pragmatic advice on using trusts or other structures to manage this potential liability for your beneficiaries.