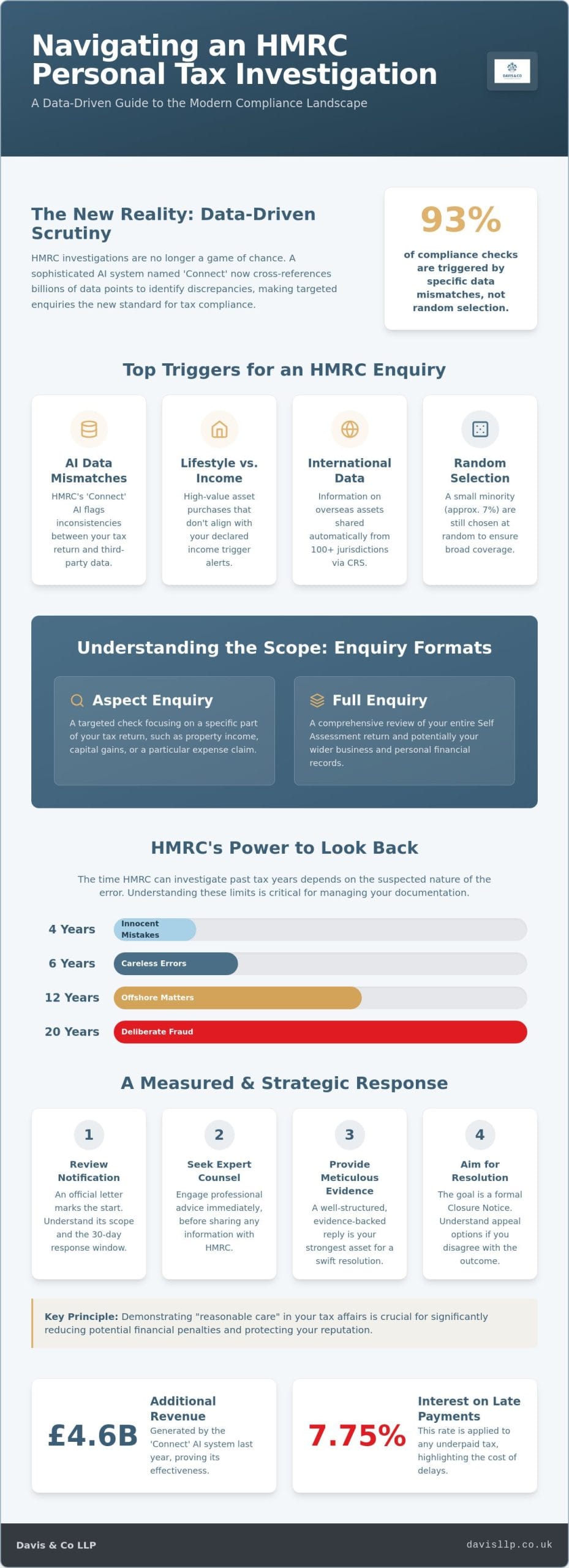

Approximately 93% of HMRC compliance checks are now triggered by specific data mismatches rather than random selection, often identified by a sophisticated AI system that monitors billions of financial transactions. If you’ve received notification of an hmrc personal tax investigation, it’s important to recognize that this is a technical challenge requiring a measured, expert response. We understand that the prospect of intrusive financial scrutiny can cause significant anxiety, particularly when you’re unsure how HMRC’s extensive data-gathering powers might impact your personal affairs.

We believe that an enquiry should be treated as a strategic negotiation where meticulous evidence and professional gravitas are your strongest assets. This guide provides a clear roadmap to help you navigate the complexities of the process with composure. We’ll examine the different types of enquiries, explain how to minimize potential penalties, and show you how to achieve an efficient resolution that protects your financial position. By understanding the current landscape, including the 7.75% interest rate on late payments and the implications of Making Tax Digital, you can move forward with confidence and clarity.

Key Takeaways

- Distinguish between routine compliance checks and targeted enquiries to understand the specific level of scrutiny applied to your financial affairs.

- Identify how HMRC’s Connect AI system cross-references data to trigger an hmrc personal tax investigation, allowing you to address discrepancies with technical precision.

- Compare the procedural requirements of aspect and full enquiries to ensure you provide the correct documentation, from bank statements to gift evidence.

- Implement a strategic response based on the principle of “reasonable care” to significantly reduce potential financial penalties and protect your professional reputation.

- Gain clarity on the resolution process, including the function of a formal Closure Notice and your options for appeal through the First-tier Tribunal.

Understanding the Scope of an HMRC Personal Tax Investigation

An hmrc personal tax investigation is a formal enquiry into the accuracy of a Self Assessment return. While the term often prompts immediate concern, it’s essentially a procedural mechanism used by HM Revenue and Customs (HMRC) to verify that the correct amount of tax has been declared and paid. In 2026, these enquiries are rarely random. Instead, they are increasingly driven by sophisticated data-matching algorithms that flag discrepancies between a taxpayer’s reported income and information held by third parties. Last year, the “Connect” AI system was credited with generating £4.6 billion in additional tax revenue, highlighting just how effective these digital tools have become at identifying potential non-compliance.

Distinguishing between a routine compliance check and a more serious fraud investigation is vital for determining your strategy. A standard enquiry usually focuses on specific entries in a return, such as property income or capital gains. In contrast, a targeted fraud investigation involves a deeper level of scrutiny into potential deliberate under-declarations. Regardless of the type, the underlying objective remains consistent: ensuring the Exchequer receives the “right amount of tax” based on current legislation. We approach these matters as a strategic partnership, aiming to resolve discrepancies before they escalate into more intrusive examinations of your wider financial affairs.

The Legal Basis for Tax Enquiries

The primary legislative framework governing these actions is the Taxes Management Act 1970. Under this act, HMRC typically has a “statutory window” of 12 months from the date a return was filed to open an enquiry. However, their reach extends much further if they suspect errors. Through “discovery assessment” powers, they can look back four years for innocent mistakes, six years for careless errors, and up to 12 years for offshore matters. If deliberate fraud is suspected, this window expands to 20 years. Understanding these time limits is crucial, as they dictate the volume of historical documentation you may be required to produce during an hmrc personal tax investigation.

Notification and the Initial Response

The process begins with an official notification letter. This document outlines the scope of the enquiry and usually provides a 30-day window for a response. Receiving this letter marks the start of a technical negotiation. We recommend an immediate professional review of the correspondence before any information is shared. A composed, professional tone from the outset is essential. It signals that you take your compliance obligations seriously and are prepared to engage with technical precision. Your initial response sets the stage for the entire enquiry, and a well-structured, evidence-backed reply can often resolve simple queries without the need for further meetings or extensive data requests.

Triggers and Selection: Why Individuals are Targeted

Understanding why a specific individual is selected for an hmrc personal tax investigation often reveals a logical, data-driven rationale. While approximately 7% of HMRC compliance checks are purely random, the vast majority are “risk-based” selections. This shift toward targeted enforcement is powered by the Connect AI system, which aggregates data from sources like the Land Registry, DVLA, and financial institutions. If your reported income doesn’t align with the acquisition of high-value assets or your general lifestyle, the system triggers a flag for human review. It’s no longer a matter of luck; it’s a matter of data parity.

Global transparency has significantly increased through the Common Reporting Standard (CRS). Over 100 jurisdictions now share financial account information automatically with UK authorities. This means HMRC has unprecedented visibility into overseas assets, making it almost impossible for foreign dividends or interest to remain undetected. For high-net-worth individuals, this international data sharing is a primary driver of modern enquiries. Discrepancies between what’s reported on a tax return and what’s received via CRS are often the first point of contact in a formal enquiry.

International and Cross-Border Complexities

Complex financial structures often attract closer attention. While robust international tax planning is entirely legitimate, it can occasionally trigger routine enquiries as HMRC seeks to verify the technical application of treaty reliefs or remittance basis claims. Scrutiny is particularly intense for offshore trusts and foreign property income. For those with non-domiciled status, ensuring that every remittance is correctly categorized is essential to prevent a procedural query from expanding in scope. We find that proactive documentation of these cross-border flows is the most effective way to maintain a quiet profile.

Sector-Specific Scrutiny: Professionals and Specialists

HMRC also employs sector-specific benchmarking to identify outliers. Professionals such as dental specialists or medical consultants often find their returns compared against industry averages for expenses and profit margins. If your figures deviate significantly from these established norms, it may prompt a request for further information. Similarly, directors of family-run companies must maintain impeccable records, as HMRC often looks for “private use” elements buried within business accounts. If you’re concerned about how your specific profile might be viewed, our personal tax services provide the technical oversight needed to ensure your filings are defensible and accurate.

Enquiry Formats: Aspect vs. Full Investigations

The procedural path of an hmrc personal tax investigation is typically defined by its breadth. While the legislation itself doesn’t always strictly categorize these checks, HMRC officers distinguish between aspect and full enquiries based on the perceived risk levels. An aspect enquiry is surgical. It targets a specific entry on your return, such as a capital gains tax calculation from a property disposal or a particular relief claim. Conversely, a full investigation is a holistic examination of your entire financial life. This often occurs when HMRC suspects that the return as a whole is unreliable or when their data-matching tools identify significant lifestyle-to-income mismatches.

Regardless of the format, you might encounter a Schedule 36 Information Notice. This is a powerful statutory tool that allows HMRC to demand documents and information they consider “reasonably required” to check your tax position. It’s a formal legal requirement, and non-compliance can lead to immediate financial penalties. We believe that managing these requests with technical precision is the only way to prevent a narrow query from evolving. “Scope creep” is a genuine risk. If your initial responses are inconsistent or lack supporting evidence, an officer may use that as justification to expand an aspect enquiry into a comprehensive review of multiple tax years.

Aspect Enquiries: Resolving Specific Discrepancies

In an aspect enquiry, the goal is a swift and quiet resolution. Common triggers include foreign interest income or specific deductions that look high relative to your profession. The strategy here is to provide precise, limited evidence that directly addresses the query. If HMRC asks for the completion statement of a property sale, we provide exactly that. Volunteering extraneous information often provides the officer with new threads to pull, potentially prolonging the process. We focus on closing these specific windows of enquiry as efficiently as possible to prevent them from becoming more intrusive.

Full Enquiries: Managing Comprehensive Financial Scrutiny

A full investigation is significantly more demanding, requiring a “private side” review of all personal bank accounts, including those held jointly. HMRC will look for evidence of lifestyle spending that exceeds your declared income, such as school fees, luxury travel, or significant asset purchases. In these instances, our role as a strategic partner is to act as a professional buffer. We handle all correspondence and information requests, ensuring that your rights are protected while satisfying HMRC’s statutory powers. Preparing for potential face-to-face meetings requires a composed approach, ensuring that every explanation is backed by a clear audit trail of your wealth and spending.

The Strategic Response: Protecting Your Interests

A strategic response to an hmrc personal tax investigation transforms a potentially volatile situation into a controlled, technical negotiation. We view professional mediation as the primary tool for achieving a “quiet resolution,” ensuring that procedural enquiries don’t escalate into wider financial crises. By managing the flow of information with precision, we protect your professional reputation and maintain the necessary distance between you and the investigating officer. This composed approach signals to HMRC that your affairs are handled with diligence and that any discrepancies are being addressed with technical rigour.

The concept of “reasonable care” is the pivot point of any enquiry. HMRC distinguishes between a simple mistake and a failure to take reasonable care when managing tax affairs. If we can demonstrate that you acted conscientiously, even if an error occurred, the financial consequences are significantly reduced. Tactical benefits often arise from making a voluntary disclosure if errors are identified early in the process. An unprompted disclosure not only demonstrates transparency but also serves as the most effective mechanism for minimizing penalty percentages before HMRC formalizes its findings.

Alternative Dispute Resolution (ADR) serves as a vital tool for complex technical standoffs. If a stalemate occurs regarding the interpretation of tax law, a neutral HMRC mediator who hasn’t been involved in your case can facilitate a fresh review. This process often avoids the time and expense of a formal tribunal. If you’re currently facing an enquiry, our Personal Tax Services team can provide the strategic oversight required to navigate these negotiations effectively.

Mitigating Penalties and Financial Impact

HMRC operates a behavioral penalty regime where the “quality of disclosure” dictates the final cost. For a careless error, penalties range from 0% to 30% of the extra tax due. However, deliberate errors can attract penalties between 20% and 70%, rising to 100% if the error was concealed. By “telling, helping, and giving,” we can often negotiate these figures down to the lower end of the statutory range. Securing expert tax advice in the UK is essential for these negotiations, particularly as late payment interest is currently set at 7.75% as of January 2026.

Reputational Management and Discretion

Maintaining professional distance through your chartered accountant is a defensive necessity. Direct, unmediated communication with HMRC often leads to “unforced errors” where casual remarks are misinterpreted as admissions of negligence. We ensure that the investigation remains a private commercial matter, handled through formal correspondence rather than informal dialogue. This level of discretion is essential for high-net-worth individuals and professionals whose reputations are as valuable as their financial assets. Our role is to ensure that every statement made is technically accurate and strategically sound.

Resolution and Future Compliance

The conclusion of an hmrc personal tax investigation is marked by a formal document, typically a Closure Notice. This letter signifies that HMRC has completed its enquiries and details any necessary amendments to your tax return. For many, this brings a significant sense of relief, but the technical work doesn’t end with the receipt of the letter. We meticulously review the final calculations to ensure that every adjustment and interest charge is mathematically and legally sound. If the investigation resulted in a settlement, this is often formalized through a “letter of offer” and acceptance, creating a legally binding contract that prevents HMRC from reopening the same issues for that specific period.

Disagreements over technical interpretations occasionally lead to a stalemate. If a mutually agreeable resolution isn’t possible through negotiation or Alternative Dispute Resolution, you have a statutory right to appeal to the First-tier Tribunal (Tax). While some firms focus on the adversarial nature of these hearings, we prioritize achieving an efficient settlement before reaching this stage. A tribunal is a public process, and for most high-net-worth individuals, a private, negotiated resolution offers far greater protection for their reputation and commercial interests. It’s about finding the most pragmatic path to closure without sacrificing your legal rights.

Closing the Investigation

Before signing any final agreement, it’s vital to confirm that the settlement reflects the “telling, helping, and giving” credits discussed in previous sections. In more complex scenarios where significant omissions were uncovered, you may be required to enter the Contractual Disclosure Facility (CDF). This is a formal process where HMRC agrees not to pursue a criminal investigation in exchange for a full and honest disclosure of all tax irregularities. Reaching this final written conclusion provides the definitive peace of mind needed to move forward with your financial affairs, knowing the matter is legally concluded.

Proactive Compliance for 2026 and Beyond

An investigation serves as a rigorous stress test of your existing financial systems. We use the findings of an hmrc personal tax investigation to refine your approach to future filings, ensuring that similar triggers don’t reappear in subsequent years. With the April 2026 mandatory introduction of Making Tax Digital for Income Tax Self-Assessment (MTD for ITSA) for those earning over £50,000, digital record-keeping is no longer optional. Implementing robust systems now helps you manage HMRC tax warnings and ensures your quarterly updates remain accurate. Regular tax health checks identify potential risks before they attract official scrutiny. If you require a strategic partner to manage your ongoing obligations, we invite you to contact Davis & Co LLP for a confidential consultation on tax compliance.

Securing Your Financial Future Through Strategic Compliance

An enquiry from HMRC is a technical challenge, but it doesn’t have to be a source of enduring stress. By understanding the data-driven triggers behind an hmrc personal tax investigation and responding with technical precision, you can protect both your assets and your reputation. We’ve explored how professional distance and the principle of reasonable care are essential for minimizing financial penalties and reaching a quiet, efficient resolution.

As we move toward a more digitized tax environment in 2026, proactive planning becomes your most reliable defense. At Davis & Co LLP, we’ve provided professional gravitas and specialist expertise since 1901. Our partner-led approach ensures that sensitive tax disputes, particularly those involving international assets or specialist professional sectors, are handled with the discretion they deserve. We act as your strategic partner, managing every technical detail to ensure your financial affairs remain secure and compliant.

Secure expert representation for your HMRC enquiry with Davis & Co LLP. We’re here to provide the steady, expert guidance you need to move forward with confidence.

Frequently Asked Questions

How far back can HMRC go in a personal tax investigation?

HMRC’s reach is determined by the perceived nature of the error. For innocent mistakes, the statutory limit is four years from the end of the tax year. This extends to six years for careless errors and 12 years for matters involving offshore income or assets. If they suspect deliberate under-declaration or fraud, they can investigate up to 20 years of historical filings.

Will I have to meet HMRC in person during an enquiry?

There is no statutory requirement to attend a face-to-face meeting with HMRC officers. Most enquiries are resolved through formal correspondence and the provision of requested documentation. While an officer may suggest a meeting to clarify your affairs, we often advise that all communication remains in writing to ensure technical precision and to maintain a clear audit trail of the hmrc personal tax investigation.

What is the difference between a tax enquiry and a tax investigation?

In technical terms, HMRC refers to these processes as compliance checks. An enquiry is the formal opening of a check into a specific Self Assessment return. The term “investigation” is often used for more serious, in-depth reviews into potential fraud or complex tax avoidance, such as those conducted under Code of Practice 8 or 9, where the financial stakes are significantly higher.

Can HMRC check my personal bank accounts if I am a company director?

HMRC has the power to request personal bank statements if they believe business records are insufficient to verify your true income. For company directors, they often look for evidence of private expenses being paid through the business or undeclared dividends. We ensure that any such request is “reasonably required” under Schedule 36 before any private information is disclosed.

How much does professional representation for a tax investigation cost?

Fees for professional representation are typically determined by the scope and technical complexity of the case. While costs reflect the time required to manage correspondence and negotiate settlement terms, they vary based on whether the enquiry is an aspect or full investigation. Many clients find that the resulting reduction in potential penalties and interest far outweighs the cost of securing expert advice.

What is the “Connect” system and how does it affect my tax return?

The Connect system is a sophisticated data-matching tool that cross-references your tax return against billions of third-party records, including bank interest, property transactions, and online marketplace activity. If a discrepancy is found, it can trigger an hmrc personal tax investigation by flagging your return for manual review. It’s the primary reason why modern enquiries are so highly targeted.

What happens if I cannot afford to pay the tax HMRC says I owe?

If you’re unable to settle the full amount immediately, a Time to Pay arrangement can often be negotiated. This allows you to pay the debt in monthly installments, typically over a period of up to 12 months. It’s important to act quickly, as late payment interest is currently set at 7.75% as of January 2026, and early engagement prevents more aggressive enforcement actions.

Can a tax investigation lead to criminal charges?

Criminal charges are generally reserved for the most serious cases of deliberate tax evasion or the provision of false information. While HMRC achieves a high prosecution success rate in criminal cases, the vast majority of personal tax enquiries are handled through civil procedures. Utilizing the Contractual Disclosure Facility is the standard method for securing immunity from prosecution in cases involving significant irregularities.