What if your annual tax return was not a source of administrative dread, but a strategic tool for long-term wealth preservation? For many, the transition to self-employment brings a welcome sense of clinical freedom, yet it often introduces a complex layer of fiscal responsibility that can feel overwhelming. We understand that the nuances of tax advice for associate dentists uk can be particularly challenging, especially as HMRC introduces the most significant changes to the self-assessment system in a generation. You likely entered this profession to focus on patient care, not to spend your evenings deciphering Making Tax Digital (MTD) protocols or worrying about whether you’ve correctly categorised your professional indemnity insurance.

This guide provides a definitive roadmap for the 2026 fiscal year, ensuring you remain fully compliant while optimising your financial position. We’ll explore the critical transition to digital record-keeping required by the April 2026 MTD deadline and provide a clear framework for identifying often-overlooked professional expenses. By the end of this article, you’ll have a structured plan to manage your tax obligations efficiently, allowing you to protect your earnings and focus on your clinical career with absolute confidence.

Key Takeaways

- Understand the specific legal nuances of the standard BDA contract and the necessary administrative steps for precise HMRC registration.

- Master the application of the “wholly and exclusively” rule to ensure the comprehensive recovery of professional expenses and capital allowances on clinical equipment.

- Prepare for the 2026 Making Tax Digital mandate by transitioning from annual filings to a structured rhythm of quarterly digital updates.

- Obtain specialised tax advice for associate dentists uk to evaluate whether a limited company or sole trader structure offers superior fiscal efficiency for your income level.

- Establish a framework for long-term wealth preservation by aligning private pension contributions with strategic tax relief opportunities.

Navigating the Transition to Self-Employment as an Associate Dentist

The transition from Foundation Training to a career as an associate dentist represents more than just a clinical advancement. It’s a fundamental shift in your legal and financial identity. While your training years were likely defined by the predictability of the PAYE system, your new role as an associate typically operates under a self-employed model. This shift offers significant clinical autonomy and potential for higher earnings, but it requires a sophisticated approach to fiscal management. Central to this transition is the standard British Dental Association (BDA) contract, which establishes you as an independent provider of services rather than an employee. This distinction is critical; it ensures you’re not caught by IR35 legislation, provided you maintain control over your clinical decisions and provide your own professional indemnity.

Seeking specialist tax advice for associate dentists uk early in this journey is essential for avoiding the pitfalls of non-compliance. One of the most immediate changes you’ll notice is the shift from net monthly pay to gross payments. You’re now responsible for calculating and setting aside your own tax and National Insurance contributions. For the 2026/2027 tax year, self-employed National Insurance has undergone significant simplification. Class 2 contributions are now abolished as a mandatory requirement. Instead, you’ll focus on Class 4 National Insurance, which is calculated at 6% on profits between £12,570 and £50,270, and 2% on any profits exceeding that higher threshold. Navigating these requirements necessitates a firm grasp of the broader UK Tax System Overview, particularly regarding how income tax and National Insurance interact for those outside traditional employment.

HMRC Registration and UTR Requirements

You must register as self-employed with HMRC by 5 October following the end of the tax year in which you started your associate work. Missing this deadline can result in immediate penalties. Upon registration, you’ll receive a ten-digit Unique Taxpayer Reference (UTR), which serves as your primary identifier for all future correspondence. During the “overlap” period where you might have both PAYE income from training and gross income from your new practice, it’s vital to maintain separate records. We strongly recommend opening a dedicated business bank account. It’s much easier to manage your cash flow and prepare for the 2026 Making Tax Digital (MTD) mandate when your professional income and clinical expenses aren’t entangled with your personal spending.

The Impact of Superannuation on Taxable Income

For those performing NHS work, superannuation remains a cornerstone of your long-term financial security. These pension contributions are deducted from your gross pay based on your Net Pensionable Earnings (NPE). It’s a common misconception that these deductions are simply a cost; in reality, they’re highly tax-efficient. Your taxable profit is calculated after these contributions are made, which effectively reduces the amount of income subject to the 40% or 45% tax brackets. By reducing your total taxable profit before the final calculation of income tax, superannuation contributions function as a highly efficient mechanism for deferred wealth building while lowering your immediate fiscal liability. Accurate reporting of your NPE on your tax return is vital to ensure you don’t overpay while securing your future entitlement.

Maximising Tax Efficiency through Professional Expenses and Deductions

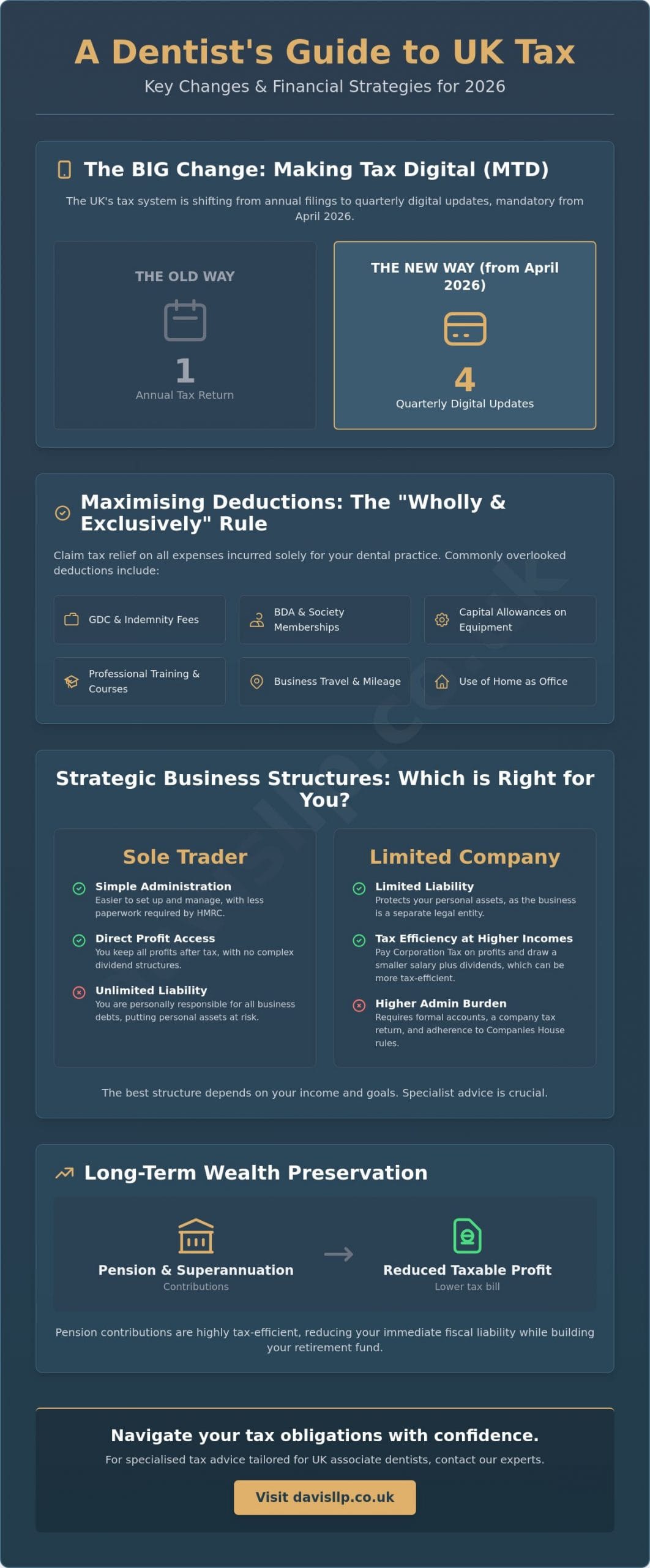

Achieving fiscal efficiency as an associate requires a precise application of HMRC’s “wholly and exclusively” rule. This principle is the cornerstone of any HMRC Self Assessment submission; it dictates that an expense must be incurred solely for the purpose of your dental trade. While professional indemnity insurance and GDC registration fees are standard deductions, we often see clinicians miss out on tax relief for BDA memberships or specialist society fees. Obtaining tailored tax advice for associate dentists uk ensures that these recurring professional costs are fully accounted for, preventing you from overpaying on your annual liability.

Modern dentistry is increasingly capital-intensive. If you invest in high-value equipment like digital scanners, surgical loupes, or specialised handpieces, you shouldn’t simply treat these as minor revenue expenses. Instead, these assets often qualify for capital allowances. This mechanism allows you to deduct the full cost of the equipment from your pre-tax profits in the year of purchase, providing a significant cash flow advantage. It’s a strategic way to reinvest in your clinical capabilities while simultaneously reducing your tax burden.

Travel and subsistence claims are a frequent point of confusion for many associates. Commuting from your home to your primary practice is generally viewed as personal travel and isn’t tax-deductible. However, if you provide services across multiple sites or attend off-site clinical training, the travel between these locations is a legitimate business expense. Keeping a detailed mileage log is essential for defending these claims. It’s these small, consistent records that protect your position if HMRC ever requests a review of your filings.

Clinical and Educational Deductions

Education is a career-long commitment in dentistry. You can claim for CPD courses and postgraduate diplomas that reinforce your existing clinical skills. Beyond education, don’t overlook tax relief on clinical scrubs and the specific cost of laundering them. If you pay lab bills directly for your private patients, these are direct costs of trade and should be deducted in full. These clinical costs quickly accumulate, making them vital components of your overall tax strategy.

Administrative and Home Office Claims

Even as a clinician, you perform significant administrative work away from the chair. If you use a portion of your home specifically for clinical note-taking or professional development, you’re entitled to a “use of home as office” deduction. Software costs, including clinical management systems and digital accounting tools, are also fully deductible. Our dental tax specialists can help you accurately apportion personal and professional use for mobile phone and internet contracts, ensuring your claims remain robust under scrutiny.

Compliance in 2026: Making Tax Digital (MTD) and HMRC Obligations

The landscape of UK taxation undergoes a fundamental transformation on 6 April 2026. For associate dentists with a qualifying gross income exceeding £50,000, the introduction of Making Tax Digital for Income Tax Self-Assessment (MTD for ITSA) marks the end of the traditional annual filing cycle. This shift isn’t merely a change in how you submit data; it’s a structural move toward real-time financial transparency. While the previous system allowed for a retrospective review of your financial year, the 2026 mandate requires a proactive, digital-first methodology that aligns your record-keeping with HMRC’s real-time expectations. Seeking specialized tax advice for associate dentists uk is no longer a year-end luxury but a continuous necessity to ensure these digital workflows remain accurate and compliant.

The new regime replaces the single annual tax return with a requirement for four quarterly updates followed by a final declaration. This “Final Declaration” serves as the year-end wrap-up where you’ll confirm the accuracy of your submitted data and make any necessary accounting adjustments. While HMRC provides a foundational Tax Guide for Dentists covering basic record-keeping, the 2026 digital requirements demand a much higher level of technical integration. You’ll need to select MTD-compatible software that can bridge the gap between your practice management systems and HMRC’s digital portal, ensuring that every patient fee and clinical expense is captured and categorised in real-time.

The Quarterly Update Cycle

Under MTD, you’ll submit digital updates of your income and expenditure every three months. These updates don’t require the same level of granular detail as a full tax return, but they must be submitted through functional compatible software. This new rhythm requires your bookkeeping to be “real-time” rather than retrospective. Engaging an expert tax advisor uk to review these quarterly submissions is a prudent step; it allows for the early identification of anomalies and ensures that your projected tax liabilities are managed effectively throughout the year, preventing unpleasant surprises during the final declaration phase.

Transitioning to Digital Record Keeping

The transition requires the complete elimination of paper-based systems for core accounting. You should adopt digital receipt storage solutions and ensure your practice management software integrates seamlessly with accounting platforms like Xero or QuickBooks. This integration allows for the automatic pulling of data, reducing the risk of manual entry errors that could trigger an HMRC inquiry. HMRC will implement a points-based penalty system for 2026, where late quarterly submissions or inaccurate digital records accrue financial charges once a specific threshold is reached. By digitising your clinical and administrative records now, you’ll build the resilience needed to navigate the 2026 mandate with absolute confidence.

Strategic Business Structures: Sole Trader vs. Limited Company for Dentists

Choosing between operating as a sole trader or incorporating as a limited company remains one of the most consequential decisions for a clinician. This choice isn’t merely a matter of tax arithmetic; it involves balancing regulatory constraints with administrative capacity. Under the 2026/2027 fiscal regime, the personal allowance remains frozen at £12,570. For many, the simplicity of the sole trader model is attractive. However, once profits consistently exceed the £50,000 to £60,000 threshold, the potential for tax mitigation via a limited company becomes harder to ignore. Seeking bespoke tax advice for associate dentists uk allows you to model these scenarios accurately. It’s particularly vital to ensure that any corporate structure doesn’t fall foul of the “GDC hurdle.” The General Dental Council has strict rules regarding dental bodies corporate; an associate must ensure their company is correctly registered and compliant with the Dentists Act to avoid professional complications.

Corporation Tax rates apply to company profits before you can extract income as dividends. While dividends still benefit from a lower tax rate than traditional salary, the gap has narrowed significantly in recent years. You must also account for the additional administrative overhead, including the preparation of annual accounts, confirmation statements, and corporation tax returns. These compliance costs can often erode the tax savings for part-time associates or those in the early stages of their career. Our dental tax specialist team can provide a side-by-side comparison of your projected take-home pay under both structures to ensure your choice remains fiscally sound.

When Incorporation Makes Financial Sense

Incorporation offers a strategic advantage for high earners who don’t need to draw all their profits for personal use immediately. By retaining funds within the company, you can defer personal tax liabilities and use the capital for equipment leasing or asset purchases. Income splitting, such as paying a spouse a salary for genuine administrative support, can also maximise the use of multiple personal allowances. This structure provides a level of financial control and long-term planning flexibility that the sole trader model simply cannot match.

The Sole Trader Advantage for Associates

For many associates, the sole trader route is the most pragmatic path. It allows for immediate access to cash without the need for formal dividend documentation or board minutes. The accountancy fees are typically lower because the filing requirements are less onerous than those for a limited company. If you’re unsure which path aligns with your career trajectory, refer to our guide on how to find a chartered accountant to evaluate your specific structure. A measured, well-researched decision today will prevent costly and complex restructuring in the future.

Long-Term Tax Planning and Wealth Preservation for Dental Professionals

Effective fiscal management extends beyond the immediate demands of quarterly digital filings. For the established associate, the focus naturally shifts toward the preservation of accumulated wealth and the mitigation of higher-rate liabilities. While previous sections detailed the operational aspects of tax advice for associate dentists uk, long-term success requires a broader perspective. This involves integrating tax-efficient investment vehicles like ISAs with more specialised options such as Enterprise Investment Schemes (EIS) or Venture Capital Trusts (VCTs). These instruments can offer significant relief, but they require a sophisticated understanding of risk and regulatory compliance to ensure they align with your overall financial objectives.

Inheritance Tax (IHT) also becomes a primary consideration as your career progresses and your asset base grows. Without a structured plan, a significant portion of your estate could be subject to a 40% tax charge upon your death. We work with our clients to implement strategies that protect their legacy, utilising gift allowances and life insurance policies held in trust to provide liquidity for future liabilities. This level of foresight ensures that the rewards of your clinical career are preserved for the next generation, rather than being eroded by avoidable fiscal charges.

Pension Planning as a Tax Mitigation Tool

Pensions remain one of the most powerful tools for reducing your taxable income. For those with NHS income, the superannuation scheme provides a robust foundation; however, supplementing this with a Self-Invested Personal Pension (SIPP) can offer additional flexibility. This is particularly relevant if your income approaches the £100,000 threshold. At this level, the personal allowance begins to taper by £1 for every £2 earned, effectively creating a 60% marginal tax rate. Strategic pension contributions can lower your adjusted net income below this “tax trap,” restoring your allowance and significantly enhancing your net position. We also monitor the interaction between your various pension pots to ensure you navigate the annual allowance limits without triggering unexpected charges.

Customised Advice for High-Earning Associates

As your career reaches its peak, your financial footprint may extend beyond the UK. Whether you hold property overseas or maintain a global investment portfolio, international tax planning becomes essential to prevent double taxation and ensure cross-border compliance. Trust structures also serve as a vital mechanism for family wealth protection, allowing for the orderly succession of assets while managing potential tax exposure. These complex arrangements require a partner who understands both the clinical realities of your profession and the intricacies of global tax law. Secure your financial future with Davis & Co LLP’s specialist dental tax services, where we provide the steady, expert guidance needed to navigate an increasingly volatile fiscal environment.

Securing Your Professional Legacy in a Digital Era

The transition to the 2026 fiscal year demands a move from retrospective accounting toward proactive financial management. By mastering digital record-keeping and selecting a business structure that aligns with your clinical goals, you can transform tax obligations into a strategic asset. We’ve explored how precise expense tracking and intentional pension planning serve as the foundation for long-term wealth preservation. Obtaining specialised tax advice for associate dentists uk ensures you remain compliant with HMRC’s evolving mandates while protecting the rewards of your clinical expertise.

As Chartered Certified Accountants with niche dental expertise, we provide the steady guidance required to navigate the MTD 2026 transition and complex international tax matters. We invite you to consult our dental tax specialists at Davis & Co LLP to develop a customised framework for your professional life. With the right strategic partner, you can focus on providing exceptional patient care while we ensure your financial interests are meticulously managed and secured for the years ahead.

Frequently Asked Questions

Is an associate dentist considered self-employed for tax purposes?

Most associate dentists in the UK operate as self-employed sole traders under the standard BDA contract. This status is defined by the clinical autonomy you exercise and the financial risks you undertake within a practice. While you provide services at a specific location, you’re an independent provider rather than an employee. This means you’re personally responsible for calculating and paying your own income tax and National Insurance contributions rather than having them deducted via PAYE.

What expenses can I claim back as a dental associate?

You can claim for any costs incurred “wholly and exclusively” for your clinical work. Common deductible items include General Dental Council (GDC) registration fees, professional indemnity insurance, and British Dental Association (BDA) memberships. You should also include clinical materials, laboratory bills if you pay them directly, and costs for continuing professional development (CPD). Maintaining digital records of these receipts is vital for securing accurate tax advice for associate dentists uk and ensuring compliance with modern standards.

How much should I set aside for my tax bill each month?

We recommend setting aside approximately 25% to 30% of your gross monthly income to cover your tax and National Insurance liabilities. This buffer accounts for the 20% basic rate or 40% higher rate tax, along with Class 4 National Insurance contributions. If your earnings exceed £125,140, the additional rate of 45% applies. Establishing a separate business savings account for these funds helps ensure you have sufficient liquidity when your payments on account fall due in January and July.

What is Making Tax Digital (MTD) and does it apply to me in 2026?

Making Tax Digital (MTD) for Income Tax Self-Assessment is a mandate requiring digital record-keeping and quarterly updates to HMRC. From 6 April 2026, it applies to all self-employed individuals, including associate dentists, with a qualifying gross income over £50,000. You’ll need to use compatible software to submit these summaries every three months. This shift replaces the single annual tax return with a more frequent, digital-first reporting cycle to improve accuracy and transparency across the profession.

Can I claim for the cost of my dental loupes?

Yes, dental loupes are considered high-value clinical equipment and typically qualify for capital allowances. Unlike minor revenue expenses, these are treated as capital assets used in your trade. You can often claim the full cost against your profits in the year of purchase through the Annual Investment Allowance. This provides a significant tax deduction, reflecting the essential nature of specialized magnification in modern clinical practice. Always retain the original invoice as evidence for your digital records.

Should I operate as a limited company or a sole trader as an associate?

The decision depends on your annual profit levels and long-term financial goals. While a limited company can be more tax-efficient for those earning over £50,000 to £60,000, it introduces higher administrative costs and stricter GDC regulatory requirements regarding corporate structures. Conversely, the sole trader model offers simplicity and lower accountancy fees. We provide tailored tax advice for associate dentists uk to help you weigh the corporation tax rates against the ease of the self-employed structure for your circumstances.

What happens if I miss the HMRC self-assessment deadline?

Missing the 31 January deadline results in an immediate £100 penalty, even if you have no tax to pay. If the return is more than three months late, HMRC applies daily penalties of £10, capped at £900. Further charges of 5% of the tax due are added at the six-month and twelve-month marks. Under the 2026 MTD regime, a points-based system will also penalize late quarterly updates, making consistent compliance and timely digital submissions more critical than ever before.

How do NHS pension contributions affect my tax return?

NHS pension contributions, known as superannuation, are deducted from your gross earnings based on your Net Pensionable Earnings (NPE). These contributions are highly tax-efficient because they reduce your total taxable profit. Effectively, you receive tax relief at your highest marginal rate on these payments. It’s essential to report your NPE accurately on your tax return to ensure your final liability reflects these deductions, as they significantly lower the income subject to the 40% or 42% brackets.