What if the most persistent drain on your practice profitability isn’t a rising clinical overhead, but a misunderstanding of how to claim tax deductible expenses for dentists under the 2026 regulations? We understand that for many clinicians, the “wholly and exclusively” rule feels less like a guideline and more like a source of professional anxiety. With the mandatory rollout of Making Tax Digital (MTD) for Income Tax Self Assessment on 6 April 2026, the administrative burden of record-keeping has reached a new level of complexity for those earning over £50,000. It’s natural to feel concerned about the precision of your digital submissions and the potential for HMRC scrutiny.

We’re here to help you master these intricacies so you can optimize your tax efficiency with absolute confidence. This guide provides a strategic framework for identifying allowable costs, from GDC fees and indemnity insurance to the nuanced application of the £1 million Annual Investment Allowance for clinical equipment. We’ll examine how to navigate the shifting landscape of dividend tax rates and capital allowances, ensuring your financial reporting is both compliant and advantageous. By the end of this article, you’ll have a clear roadmap to secure your practice’s financial health while maintaining total peace of mind.

Key Takeaways

- Master the application of the “wholly and exclusively” principle to ensure every claim withstands HMRC scrutiny in a clinical setting.

- Categorise your clinical and professional costs accurately, identifying which GDC fees and indemnity premiums qualify as tax deductible expenses for dentists.

- Optimise high-value practice investments by utilising the £1 million Annual Investment Allowance for digital scanners and essential dental equipment.

- Navigate the 2026 Making Tax Digital requirements with confidence, ensuring your digital record-keeping meets the new quarterly reporting standards.

- Shift from reactive bookkeeping to strategic tax planning by leveraging the deep-seated expertise of a specialist dental accountant.

The “Wholly and Exclusively” Principle for Dental Professionals

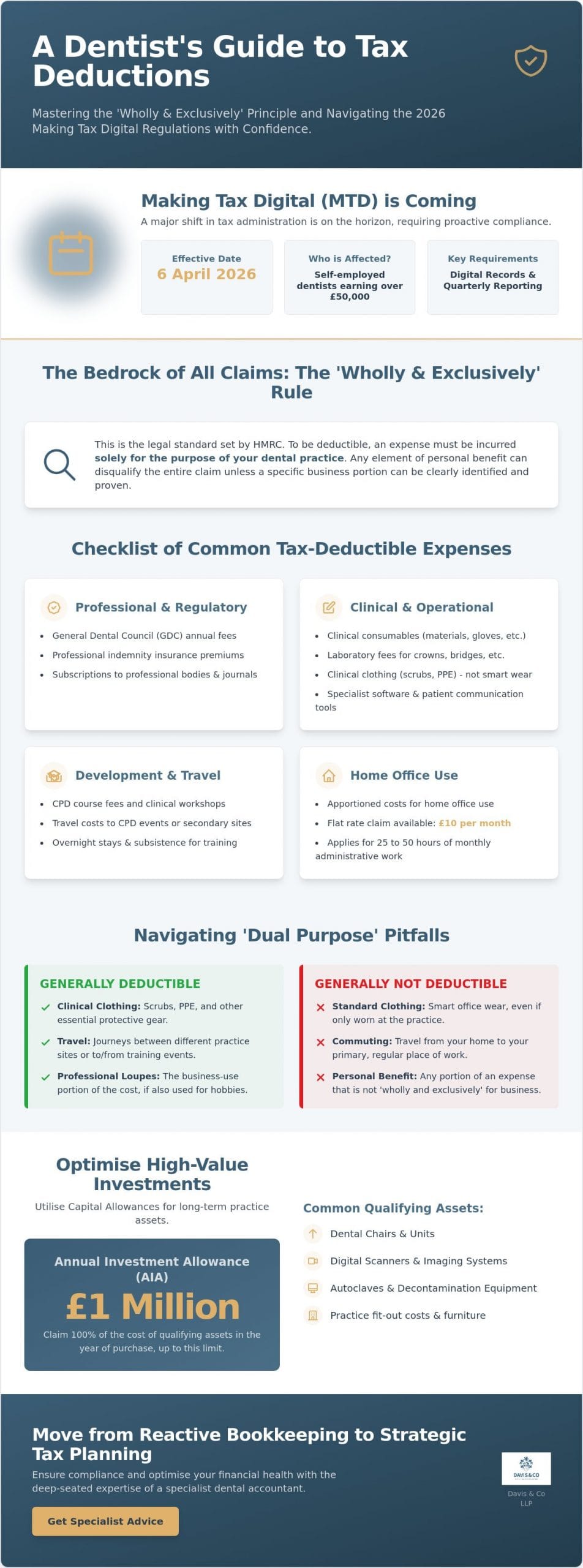

The bedrock of any claim for tax deductible expenses for dentists is a rigid adherence to the HMRC “wholly and exclusively” test. This isn’t merely a suggestion; it’s the legal standard that determines whether a cost is a legitimate business deduction or a personal expense in disguise. To qualify, an expense must be incurred solely for the purpose of your dental trade. If a payment contains even a minor element of personal benefit, HMRC may disqualify the entire amount unless a distinct, identifiable part is used for business. We’ve seen that a lack of clarity here is often what triggers deeper investigations.

Distinguishing between revenue and capital expenditure is equally vital for maintaining compliance. Revenue costs are day-to-day running expenses, such as surgery materials, clinical disposables, or laboratory fees. Capital costs, however, involve long-term assets like dental chairs, autoclaves, or digital imaging systems. While both offer tax relief, they’re handled through different mechanisms. Revenue costs are deducted directly from your income, while capital items typically fall under Capital Allowances. Understanding the ‘Wholly and Exclusively’ Principle ensures you don’t misclassify these investments, which could lead to significant errors in your 2026 digital submissions.

Defining Professional Necessity

Establishing a clear professional link requires more than just a receipt. For non-obvious costs, such as specialist software or bespoke patient communication tools, we recommend documenting the specific business case at the time of purchase. This proactive approach creates an audit trail that’s difficult to challenge. In the context of a 2026 dental associate contract, the “wholly and exclusively” rule dictates that an expense is only deductible if its sole purpose is the advancement of your clinical practice and the generation of professional turnover.

Navigating Dual-Purpose Pitfalls

HMRC often scrutinizes areas where personal and professional lives overlap. It’s easy to fall into traps with expenditures that seem professional but offer a “duality of purpose.” Common examples include:

- Clinical Clothing: Scrubs and protective gear are deductible, but standard “smart” office wear is not, even if you only wear it at the practice.

- Professional Loupes: While essential for surgery, if they’re also used for a private hobby, the claim must be strictly apportioned.

- Travel: Commuting to your regular practice isn’t deductible, but travel to a secondary site or a CPD event usually is.

We suggest a meticulous apportionment strategy for shared expenses. If you use a home office for 25 to 50 hours a month for clinical administration, the 2026 flat rate is £10 per month. By being precise now, you protect your practice profitability and ensure your records are ready for the MTD for ITSA transition on 6 April 2026. Maintaining a professional-first narrative for every claim is the most effective way to ensure long-term financial security.

Common Allowable Clinical and Professional Expenses

Identifying the full range of tax deductible expenses for dentists requires a shift from viewing costs as mere overheads to seeing them as strategic components of your practice’s financial structure. While the “wholly and exclusively” rule provides the framework, the practical application involves categorising clinical, administrative, and professional outgoings with precision. For self-employed associates and practice owners alike, these deductions are essential for mitigating the impact of frozen personal allowances and rising dividend tax rates in 2026.

Clinical consumables and laboratory fees represent a significant portion of an associate’s expenditure. Whether you’re paying for precious metal alloys, ceramic crowns, or everyday disposables like impression materials and gloves, these are direct revenue expenses. Similarly, professional indemnity insurance is a non-negotiable deduction. Given the litigious nature of modern healthcare, your premiums are a necessary cost of trade. We often find that clinicians overlook the travel and subsistence costs associated with Continuing Professional Development (CPD). If you’re attending a clinical workshop or a dental conference, the course fees, transport, and overnight stays are generally allowable, provided the primary purpose is professional advancement.

Professional Fees and Subscriptions

Mandatory professional fees form the core of your annual claims. This includes your General Dental Council (GDC) annual retention fee and memberships to the British Dental Association (BDA). Beyond these, subscriptions to specialist societies, such as the British Endodontic Society or the Faculty of General Dental Practice, are legitimate deductions. Identifying these often requires a nuanced approach, which is why many clinicians seek expert tax advice in the UK to ensure no professional membership is missed. Even subscriptions to peer-reviewed dental journals can be claimed if they’re used to maintain your clinical knowledge.

Clothing, Equipment, and Consumables

HMRC maintains a strict stance on clothing. While standard business suits are disqualified due to “duality of purpose,” the cost of scrubs, surgical gowns, and protective eyewear is fully deductible. You can also claim for the laundering and repair of this clinical attire. Small equipment items that fall below the capital threshold, such as handpieces, curing lights, or specific surgical kits, are treated as revenue expenses. Digital infrastructure is increasingly relevant; subscriptions for patient management software or clinical planning tools are vital tax deductible expenses for dentists. While regional rules vary, the general principles of Compliance in 2026: Making Tax Digital and Record Keeping highlight the necessity of meticulous documentation for all professional outgoings. Engaging a Dental tax specialist can provide the clarity needed to ensure these claims are both maximised and compliant with the 2026 digital reporting standards.

Capital Allowances: Optimising High-Value Investments

While associates often focus on the tactical management of professional fees, practice owners must address the more substantial capital requirements of a modern clinic. These high-value investments aren’t treated as day-to-day revenue costs. Instead, they’re managed through Capital Allowances. For the 2026/27 tax year, the Annual Investment Allowance (AIA) remains a cornerstone of fiscal planning, permitting a 100% deduction on qualifying plant and machinery up to a £1 million limit. This allows you to immediately offset the costs of digital scanners, X-ray systems, and dental chairs against your taxable profits, providing a vital lever for cash flow management.

Strategic timing is essential. We recommend aligning major acquisitions with years of peak profitability to maximise the tax relief. This isn’t just about immediate savings; the way you handle these tax deductible expenses for dentists can influence the long-term valuation of your practice. Misclassifying assets can create complexities during a future sale or transition. Following the core principles found in the IRS Tax Guide for Small Business, it’s clear that maintaining a rigorous distinction between operational costs and long-term capital investments is a universal standard for financial integrity. We’ve found that practice owners who plan their capital expenditure eighteen months in advance are significantly better positioned to weather economic volatility.

Major Clinical Equipment

It’s crucial to distinguish between a repair and an improvement. Replacing a single component on an existing dental chair is generally a revenue expense. Installing a completely new chair is a capital acquisition. When refurbishing a surgery, “integral features” such as electrical systems or specialist plumbing also qualify for relief, though they may fall into different pools with varying writing-down allowances. You should also consider the implications of asset disposal. If you sell a piece of equipment for which you’ve already claimed 100% AIA, a balancing charge may arise, effectively bringing that value back into your taxable income during the year of sale.

Practice Vehicles and Technology

The digital transformation of dentistry requires robust IT infrastructure. Servers, high-end workstations for CAD/CAM milling, and patient database security systems all fall under the umbrella of tax deductible expenses for dentists via capital allowances. Practice owners are also increasingly looking at electric vehicles (EVs) due to their favourable benefit-in-kind rates and capital allowance treatment compared to traditional combustion engines. For the 2026 tax year, the £1 million Annual Investment Allowance threshold continues to provide a vital mechanism for practice growth by allowing for the full, immediate deduction of most plant and machinery costs. This stability allows you to invest in the latest clinical technology without the burden of staggered tax relief over several years.

Compliance in 2026: Making Tax Digital and Record Keeping

The landscape of professional tax compliance undergoes a fundamental transformation on 6 April 2026. For self-employed dentists and practice owners with a gross income exceeding £50,000, the introduction of Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA) marks the end of traditional annual reporting. You’ll now be required to maintain digital records and submit quarterly updates of your income and tax deductible expenses for dentists to HMRC. The first quarterly deadline falls on 7 August 2026, covering the period from 6 April to 5 July. While HMRC has deferred penalties for the 2026/27 tax year to facilitate this transition, the expectation for precision remains high.

Adopting a real-time approach to expense logging is the most effective way to avoid year-end errors. Waiting until the final quarter to categorise complex clinical outgoings often leads to missed deductions or inaccurate classifications. By capturing data as it occurs, you ensure that your digital submissions provide an accurate, contemporaneous reflection of your practice’s financial health. This level of diligence is essential for protecting your practice profitability in an increasingly scrutinised environment.

Digital Record-Keeping Standards

Transitioning from manual spreadsheets to HMRC-compliant software is no longer optional. We recommend selecting platforms that integrate seamlessly with clinical management systems to ensure data flows accurately between your surgery and your financial records. Utilising professional bookkeeping services can significantly reduce the administrative friction of this new regime. By automating receipt capture through mobile applications, you ensure that every clinical consumable or professional fee is logged in real time. This prevents the common year-end scramble and ensures your quarterly submissions reflect the true state of your practice’s profitability.

HMRC Scrutiny and Investigation Protection

Digital records provide a level of transparency that serves as your primary defence during an enquiry. HMRC’s move toward digitisation allows them to identify “red flags” more efficiently, such as significant fluctuations in claimed costs or unusual ratios of expenses to turnover. Precise, time-stamped records demonstrate a commitment to compliance that often curtails the depth of an investigation. It’s also vital to remember that both digital and physical records must be retained for at least five years after the 31 January submission deadline. If you’re concerned about your practice’s readiness for the April 2026 deadline, our Dental tax specialist team can assist in implementing a compliant digital framework.

Professional representation during a compliance check is essential for maintaining the necessary distance between your clinical work and administrative scrutiny. We act as a strategic partner, ensuring that your narrative remains focused on professional necessity and clinical requirement. This composure is vital when justifying complex claims for tax deductible expenses for dentists, ensuring your practice remains secure and well-advised throughout any HMRC interaction.

Strategic Tax Planning with a Specialist Dental Accountant

Effective financial management in dentistry extends far beyond the quarterly logging of tax deductible expenses for dentists. While compliance with Making Tax Digital is a prerequisite for practice stability, true profitability is secured through proactive tax mitigation strategies. We view ourselves as strategic partners rather than mere service providers, offering the intellectual rigour necessary to navigate the unique financial structures of the dental sector. By looking ahead to the 2026/27 tax year, we help you anticipate fiscal shifts before they impact your personal or practice-wide wealth.

For clinicians with cross-border interests or those considering expansion, we integrate day-to-day expense management into a broader international tax planning strategy. This holistic approach ensures that your professional outgoings are optimised across all jurisdictions, maintaining a cohesive narrative that satisfies both domestic and international tax authorities. We believe that a practice’s financial health is a reflection of its long-term vision, and our role is to provide the clarity required to realise that ambition.

Tailored Solutions for Clinicians

The choice between operating as a sole trader or a limited company is increasingly complex. With dividend tax rates set at 10.75% for the basic rate and 35.75% for the higher rate in 2026, the traditional benefits of incorporation require a more nuanced analysis. We conduct highly individualised reviews to determine which structure best supports your clinical goals and lifestyle requirements. Pension contributions remain one of the most effective tax deductible expenses for dentists, serving as a significant deduction that secures your future while reducing your current tax bill. Whether you’re planning a practice acquisition or developing an exit strategy, our advice is designed to protect your interests at every stage of your career.

The Davis & Co LLP Partnership

Our commitment to professional gravitas and discretion is the hallmark of our service delivery. We provide a composed partnership that allows you to focus on clinical excellence while we manage the complexities of your financial reporting. We understand that dealing with sensitive commercial matters requires a trusted advisor who values intellectual rigour and reliability. Our approach is traditional in its values yet contemporary in its application, ensuring you’re always well-advised in a volatile fiscal environment. Consult our specialist dental tax team today to begin a collaborative partnership that prioritises your practice’s long-term success.

Securing Your Practice’s Financial Future in 2026

The transition to 2026 represents a significant milestone for the dental profession, moving from traditional annual reporting to the immediate demands of digital compliance. It’s a fundamental shift. Success in this new environment requires more than just a list of tax deductible expenses for dentists; it demands a rigorous understanding of HMRC’s evolving standards and the strategic timing of capital investments. By mastering the “wholly and exclusively” principle and embracing digital record-keeping now, you protect your practice against unnecessary scrutiny while maximising your professional tax efficiency.

We understand that your primary focus remains on clinical excellence and patient care. As Chartered Certified Accountants since 1901, we provide the steady, expert guidance needed to navigate complex HMRC compliance with absolute discretion. Our role as specialist dental tax advisors is to ensure your financial reporting remains robust and your practice profitability is secured through every quarterly submission. We invite you to secure your professional tax position with Davis & Co LLP. Together, we can build a resilient financial foundation that allows your clinical practice to thrive in the years ahead.

Frequently Asked Questions

Can I claim for the cost of my dental scrubs and laundering?

Yes, you’re entitled to claim for the purchase, repair, and laundering of specialist clinical clothing such as scrubs and protective gear. HMRC allows these deductions because the items are not part of an everyday wardrobe and are required for your clinical duties. You should keep digital records of these costs to ensure they’re included in your quarterly submissions.

Standard business attire, such as suits or smart shoes, remains disqualified even if you only wear them at the practice. The “wholly and exclusively” rule is strictly applied here; if the clothing could reasonably be worn outside of a clinical environment, the deduction will likely be challenged.

Are GDC and BDA fees fully tax-deductible?

GDC annual retention fees and BDA memberships are fully deductible as they are mandatory professional subscriptions. These are essential tax deductible expenses for dentists that every clinician should record to reduce their taxable income. Since these bodies are on HMRC’s approved list, the claims are straightforward and rarely questioned during an enquiry.

How do I claim for CPD courses and related travel expenses?

You claim for CPD by recording the course fees as a professional development expense in your digital accounts. Training that maintains or updates your existing clinical skills is fully allowable. This also extends to travel to the venue and reasonable subsistence costs, provided the trip’s primary purpose is professional advancement.

Can I deduct the cost of my Loupes if I also use them for a hobby?

No, you can’t claim the full cost of Loupes if they serve a dual purpose. HMRC’s rules require expenses to be incurred solely for the purpose of your dental trade. If there’s significant personal use, you must apportion the cost and only claim the percentage that relates to your clinical work. We recommend keeping a brief log of professional use to justify this split.

What are the 2026 Making Tax Digital (MTD) rules for dentists?

From 6 April 2026, self-employed dentists with a gross income over £50,000 must comply with MTD for Income Tax. This requires you to maintain digital records and send quarterly updates of your income and expenses to HMRC using compatible software. The first quarterly submission is due by 7 August 2026, replacing the traditional annual self-assessment process.

Is my home office deductible if I do my clinical notes there?

You can claim for a home office if you use a dedicated space for clinical administration and patient notes. For those working between 25 and 50 hours a month from home, the 2026 simplified flat rate is £10 per month. Identifying these small but consistent tax deductible expenses for dentists is a key part of an effective tax mitigation strategy.

Can I claim for my indemnity insurance even if my practice pays for it?

You can only claim for indemnity insurance if you personally incur the cost. If the practice pays the premium directly, or if it’s already deducted from your gross pay before tax is calculated, you haven’t made a personal payment to claim against. You should only record this as a deduction if the funds leave your post-tax bank account.

What equipment qualifies for the Annual Investment Allowance in 2026?

Most clinical plant and machinery qualify, including dental chairs, digital scanners, X-ray machines, and autoclaves. The Annual Investment Allowance (AIA) allows you to claim 100% first-year relief on these items up to a £1 million limit. This means the full cost of the equipment can be deducted from your taxable profits in the year of purchase, providing a significant cash flow advantage.