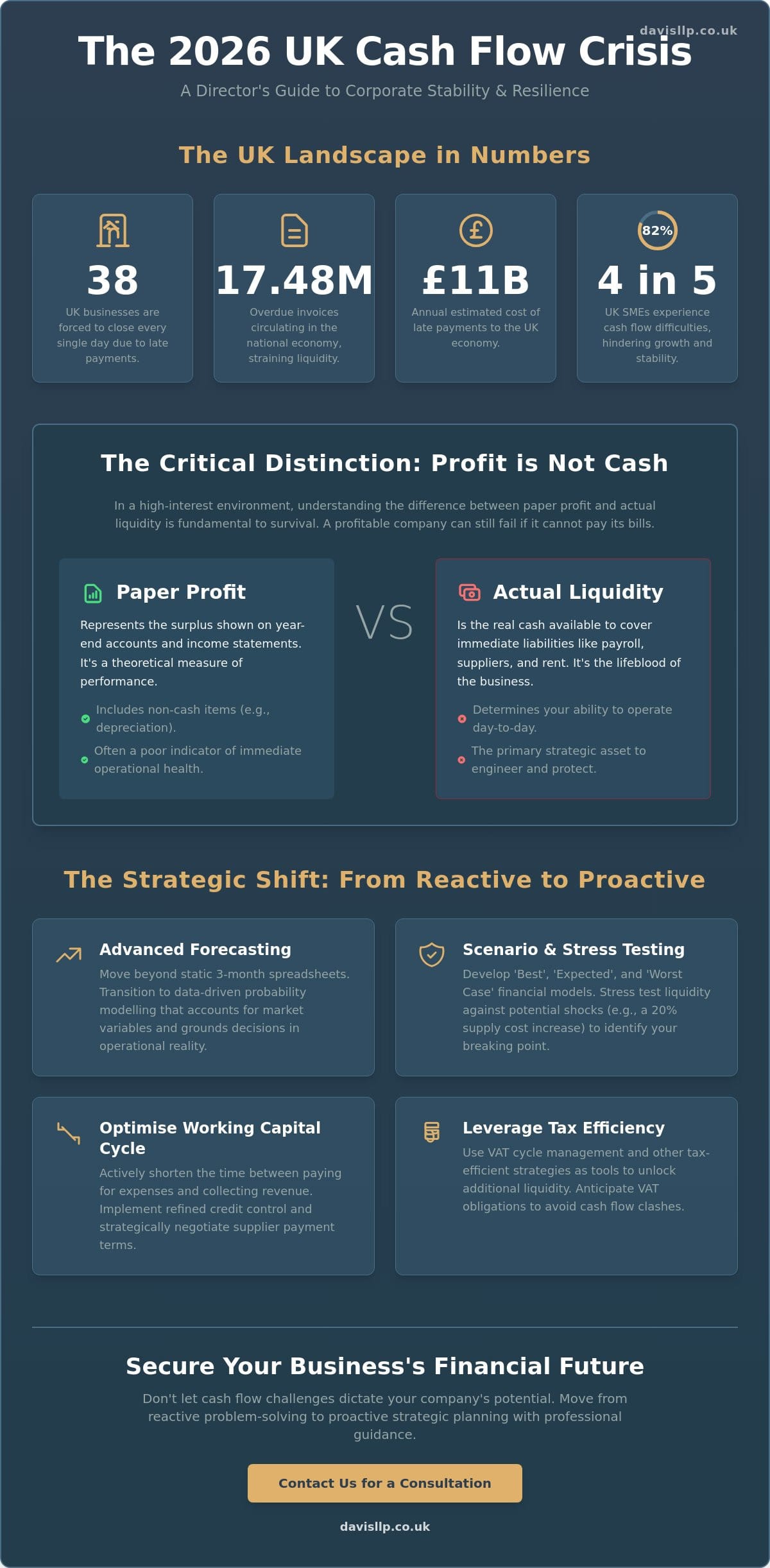

With 38 UK businesses forced to close every single day due to late payments, the margin for error in liquidity management has never been thinner. As a director, you likely feel the pressure of balancing ambitious growth plans against the 17.48 million overdue invoices currently circulating in the national economy. This represents a delicate equilibrium, especially as rising operational costs and a 3.75% base rate continue to test even the most robust balance sheets. Understanding how to improve business cash flow uk is no longer just an administrative task; it’s a fundamental requirement for corporate stability and success in 2026.

We understand that your priority is to maintain a resilient cash buffer while navigating the complexities of the new Small Business Protections Bill. This strategic guide provides professional insights into optimizing your liquidity, mitigating economic volatility, and utilizing tax-efficient cash management to support long-term expansion. We’ll examine how to leverage the latest legislative safeguards and the role of precise management accounts in creating predictable monthly liquidity.

Key Takeaways

- Understand the critical distinction between paper profit and actual liquidity to ensure your organization remains resilient in a high-interest economic environment.

- Discover how to improve business cash flow uk by moving beyond static spreadsheets toward real-time forecasting driven by professional management accounts.

- Implement practical steps to shorten your working capital cycle, including refined credit control and the strategic negotiation of supplier terms.

- Leverage tax efficiency and VAT cycle management as strategic tools to unlock additional liquidity and support your broader growth objectives.

- Identify the warning signs of overtrading to protect your margins while scaling operations through disciplined cash management and retained earnings.

The 2026 UK Economic Landscape: Why Cash Flow is Your Primary Strategic Asset

In the current fiscal environment, the distinction between a profitable company and a solvent one has become increasingly stark. While your year end accounts might show a healthy surplus, the reality of 82% of UK SMEs experiencing cash flow difficulties suggests that paper profit is often a poor indicator of operational health. In 2026, professional business management requires you to view liquidity not as a byproduct of sales, but as a primary strategic asset that must be actively engineered. With late payments costing the UK economy an estimated £11 billion annually, your ability to maintain a liquid reserve is what separates sustainable enterprises from the 38 businesses that fail every day.

Persistent inflation has fundamentally altered the cost of doing business in the UK. Fixed costs that were manageable two years ago have been replaced by variable expenses that demand constant oversight. Directors often ask how to improve business cash flow uk when facing these specific pressures; the answer lies in a psychological shift from reactive bookkeeping to proactive financial leadership. This involves moving beyond the basic recording of transactions to a model where every commercial decision is weighed against its impact on immediate liquidity.

Understanding the Liquidity Gap

Rapid growth is frequently the precursor to a liquidity crisis. When you scale operations, the requirement for upfront investment in payroll, inventory, and overheads often precedes the collection of revenue by weeks or months. This creates a growth vacuum that can swallow even the most promising firms if not managed with precision. The Liquidity Gap is the delta between operational investment and revenue realisation. Closing this gap requires a move away from static reporting toward integrated management accounts that provide real-time visibility into your working capital requirements.

External Volatility and Risk Mitigation

The Bank of England’s decision to hold the base rate at 3.75% in May 2026 underscores a period of stabilized yet elevated borrowing costs. For national UK enterprises, traditional cash buffers that once felt sufficient are now easily eroded by debt servicing and rising supply chain prices. Effective cash flow forecasting allows a director to anticipate these shifts rather than merely reacting to them. We recommend establishing a Resilience Ratio for your specific industry, which measures your available liquid assets against your projected short term liabilities. This ratio acts as an early warning system, ensuring you maintain the agility needed to navigate market shifts without compromising your core operations.

Advanced Forecasting: Moving Beyond the Three-Month Spreadsheet

Traditional three-month spreadsheets often fail because they treat the future as a linear progression. In reality, the 2026 UK market is defined by non-linear variables, from fluctuating energy prices to the sudden impact of the Small Business Protections Bill. Professional strategies regarding how to improve business cash flow uk now require a transition from best guess estimates to data-driven probability modelling. By applying professional audit standards to your internal projections, we ensure that the figures driving your boardroom decisions are grounded in verifiable operational reality rather than optimism. It’s about moving from a reactive stance to one of composed foresight.

This rigorous approach transforms the forecast from a static document into a dynamic tool for strategic planning. It allows you to anticipate the exact moment when capital expenditure might clash with quarterly VAT obligations, providing the lead time necessary to adjust your strategy. When your data is integrated and precise, you can manage your Cash Flow Management with the quiet excellence that modern business demands.

Scenario Planning and Stress Testing

Reliability comes from preparing for the improbable. We encourage directors to develop three distinct financial models: Best Case, Expected, and Worst Case. A critical exercise involves stress testing your liquidity against a hypothetical 20% increase in supply chain costs. Identifying this Breaking Point before it occurs allows you to establish contingency measures or secure facilities while your balance sheet is still strong. It turns a potential crisis into a managed event.

The Integration of Management Accounts

Monthly management accounts are the cornerstone of this proactive stance. They provide the real-time KPIs needed to identify cash flow bottlenecks, such as a creeping increase in debtor days, before they manifest as a crisis. By linking your rolling forecast to the oversight of a small business accountant, you gain an external layer of intellectual rigour. This partnership ensures that your growth remains sustainable and your liquidity remains predictable. If you require a more granular view of your current position, our team can assist in refining your how to improve business cash flow uk through bespoke Management Accounts reporting.

Optimising the Working Capital Cycle: Five Practical Steps

The working capital cycle represents the heartbeat of your operational liquidity. It’s the period between outgrowing cash for production and receiving it from customers. When considering how to improve business cash flow uk, directors must look beyond the balance sheet and examine the efficiency of this cycle. With 17.48 million overdue invoices currently circulating in the UK economy, the speed at which you convert unbilled work into cleared funds is a primary driver of your company’s resilience. Optimising this process requires a disciplined, five step approach to internal governance.

- Shorten Days Sales Outstanding (DSO): Implement a rigorous credit control function that initiates contact before an invoice becomes overdue, rather than reacting after the fact.

- Strategic Supplier Negotiation: Align your payment obligations with your revenue peaks. We recommend negotiating terms that respect your liquidity needs without compromising the integrity of your supply chain.

- Audit Work-in-Progress (WIP): Unbilled labour or excess inventory is essentially ‘trapped’ cash. Regular reviews of your WIP ensure that capital isn’t sitting idle on the warehouse floor or in unfinished projects.

- Automate Billing Systems: Since April 1, 2026, all VAT-registered businesses have been required to maintain digital records. Use this infrastructure to automate invoice delivery and follow up reminders, reducing the risk of human error.

- Rigorous KYC Checks: Before committing to significant contracts, perform thorough ‘Know Your Customer’ assessments. It’s better to decline a high-risk contract than to inherit a client’s liquidity crisis.

Refining Your Accounts Receivable Strategy

For long term projects, transitioning to milestone based billing is a vital strategy. It ensures a steady stream of inward cash flow that covers operational costs as they arise, rather than waiting for a final settlement. Professional communication plays a significant role here; a polite, firm inquiry regarding payment status often yields better results than aggressive litigation. If internal resources are stretched, involving an external partner for credit management allows your team to focus on Business Growth Acceleration while experts handle the complexities of debt recovery.

Supplier Management and Accounts Payable

Managing your payables is a delicate balancing act. While early payment discounts are attractive, they shouldn’t be pursued at the expense of your cash buffer. We suggest building a ‘preferred supplier’ list of partners who offer flexible credit terms in exchange for long term loyalty. Additionally, supply chain finance can be a sophisticated tool for liquidity preservation, allowing you to extend your payment terms while ensuring your suppliers are paid promptly by a third party. This maintains your reputation as a reliable partner while keeping your own capital accessible for strategic investment.

Tax Efficiency as a Cash Flow Driver

Many directors view tax obligations as a fixed, unavoidable drain on resources. However, professional tax advice uk reframes these liabilities as variables that can be managed to support your liquidity. In 2026, with the main rate of corporation tax at 25% for companies with profits exceeding £250,000, the timing and structure of your tax payments are critical. By aligning your tax strategy with your operational cycle, you can prevent large outflows from coinciding with periods of low revenue. This proactive orchestration is a fundamental component of how to improve business cash flow uk, ensuring that your capital remains available for reinvestment rather than sitting idle in HMRC accounts.

Strategic use of Capital Allowances also plays a significant role in liquidity preservation. By timing large asset purchases to coincide with the end of your financial year, you can accelerate tax relief and reduce your immediate corporation tax bill. This creates a tangible cash benefit that can be redirected into your Business Growth Acceleration initiatives. It’s about ensuring that every pound within the business is working toward your long-term stability.

VAT and Compliance Optimisation

The choice between cash and accrual accounting for VAT can have a profound impact on your monthly liquidity. For businesses with taxable turnover below the registration threshold of £90,000, or those experiencing slow payment cycles from major clients, cash accounting allows you to delay VAT payments until you’ve actually received funds from your customers. This eliminates the “tax gap” where you’re forced to pay VAT on invoices that haven’t yet been settled. Since the mandating of Making Tax Digital for all VAT-registered businesses on April 1, 2026, maintaining precise digital records is essential to avoid the cash-draining impact of compliance penalties. Accurate VAT Compliance ensures you stay on the right side of regulation while protecting your reserves.

R&D and Specialist Reliefs

Innovation isn’t limited to the laboratory; it often exists within the everyday problem-solving of your operations. Identifying these qualifying activities can lead to significant R&D tax credits, providing a substantial cash injection that many directors overlook. For firms with a global footprint, consulting with an international tax planning specialist is vital to ensure that cross-border reliefs are fully utilised. These specialist claims don’t just reduce your tax burden; they act as a non-dilutive source of funding for future projects. If you require a detailed review of your current tax position to enhance liquidity, explore our professional tax advice uk.

Growth Acceleration: Building a Sustainable Cash Buffer

Overtrading remains a primary risk for UK firms in 2026. It occurs when a business expands its operations too rapidly without the liquid capital to support increased overheads and inventory. Success, paradoxically, can lead to insolvency if your working capital isn’t professionally managed. When considering how to improve business cash flow uk, the focus should shift from simple volume to the quality of that volume. Sustainable growth requires a buffer that scales in proportion to your turnover, ensuring you don’t become a victim of your own success.

Securing the right balance between dividend extraction and retained earnings is equally vital. While it’s natural for directors to seek a return on their investment, depleting reserves can leave the company vulnerable to the 3.75% base rate pressures currently impacting debt servicing costs. Retaining a portion of profits within the business acts as a self-funding mechanism for Business Growth Acceleration, reducing your reliance on external financing. It’s about maintaining a level of quiet excellence that allows you to capitalize on opportunities without compromising your stability.

Financing Growth Without Sacrificing Stability

Choosing between debt and equity financing involves weighing immediate liquidity against long-term autonomy. Each path has distinct impacts on your monthly cash position:

- Debt Financing: Retains full ownership but introduces a fixed repayment obligation, which is particularly relevant given the current 3.75% base rate environment.

- Equity Financing: Offers a permanent capital injection without repayment pressure, though it dilutes ownership and future dividend potential.

Regardless of your choice, an emergency reserve that scales with your turnover is non-negotiable. Preparing your accounts for audit and assurance is the most effective way to build lender confidence and secure competitive rates. It demonstrates a level of financial discipline that suggests your growth is planned rather than accidental. This transparency is essential for national UK enterprises looking to navigate 2026 with confidence.

The Value of a Strategic Financial Partner

The transition from compliance-led bookkeeping to strategic advisory is often the turning point for a maturing business. Regular management meetings with your advisor transform financial performance by identifying trends before they impact your liquidity. This collaborative partnership moves your focus from past transactions to future possibilities, ensuring your cash flow remains a driver for growth rather than a constraint. We invite you to Contact Davis & Co LLP today to discuss how we can help you build a resilient cash buffer and implement a tailored 2026 strategy for how to improve business cash flow uk.

Mastering Strategic Liquidity for 2026 and Beyond

Managing the complexities of the 2026 fiscal landscape requires a shift from reactive accounting to proactive financial orchestration. By integrating advanced forecasting with a disciplined working capital cycle, you transform liquidity from a daily concern into a strategic engine for growth. We’ve explored how professional tax efficiency and robust management accounts provide the clarity needed to balance immediate operational needs with long term investment. Ultimately, understanding how to improve business cash flow uk is about building a foundation that remains stable despite external volatility.

As Chartered Certified Accountants since 1901, we bring a legacy of reliability and deep-seated expertise to your boardroom. Whether you require specialists in business growth acceleration or guidance on complex international tax planning, our team acts as a composed partner in your success. Secure your business future with expert cash flow management from Davis & Co LLP. We’re ready to help you translate these strategies into a resilient and prosperous commercial future.

Frequently Asked Questions

What is the difference between profit and cash flow in a business?

Profit represents the surplus remaining after all accounting expenses are deducted from total revenue, whereas cash flow is the physical movement of currency through your bank accounts. It’s entirely possible for a firm to report a healthy profit while lacking the liquidity to meet its immediate obligations. This discrepancy often arises when revenue is recognized on an accrual basis before the customer has actually settled the invoice.

How much cash reserve should a UK business ideally hold in 2026?

While a standard reserve of three to six months of operating expenses is often recommended, the specific requirements for a UK business in 2026 depend on your sector’s volatility. Directors should aim for a buffer that covers fixed overheads and debt servicing at the 3.75% base rate. Establishing a bespoke resilience ratio helps determine the exact level of liquidity needed to navigate market shifts without halting operations.

Can changing my VAT accounting method improve my cash flow?

Transitioning to the VAT Cash Accounting Scheme can significantly improve your liquidity if your customers are slow to pay. Under this method, you only account for VAT on your returns once you’ve received the payment, rather than when the invoice is issued. This is an effective strategy for how to improve business cash flow uk, particularly for firms with taxable turnover below the £1.35 million scheme limit.

What are the most common causes of cash flow problems for growing companies?

Overtrading is the most frequent cause of liquidity crises in expanding firms, where the cost of fulfilling new orders exceeds available cash reserves. Other common triggers include inadequate credit control leading to high debtor days and the liquidity gap created when capital expenditure precedes revenue realization. Without rigorous Cash Flow Management, even a successful company can find its growth restricted by a lack of accessible funds.

How does international tax planning affect my UK business cash flow?

International Tax Planning ensures that your global operations are structured to minimize tax leakage and avoid double taxation. By strategically managing where profits are recognized and utilizing cross-border reliefs, you can preserve more capital for reinvestment. This specialized oversight prevents cash from being unnecessarily trapped in foreign jurisdictions, ensuring it remains available to support your UK headquarters’ growth and stability.

Is it better to lease or buy equipment to maintain healthy liquidity?

Leasing equipment is generally more beneficial for maintaining liquidity as it spreads the cost over time rather than requiring a substantial upfront payment. While purchasing might allow for immediate capital allowances, the resulting cash drain can limit your ability to respond to unforeseen opportunities. Directors must weigh the tax benefits of ownership against the flexibility provided by retained earnings and predictable monthly lease payments.

How can I improve my credit control without damaging client relationships?

You can enhance credit control by shifting the focus to professional, proactive communication and automated systems. Establishing clear payment terms at the outset of a contract and sending polite reminders before the due date sets a standard of mutual respect. This approach positions your firm as a disciplined partner that values financial order, which actually strengthens rather than damages long term client relationships.

What role does a Chartered Accountant play in managing business cash flow?

A Chartered Accountant provides the intellectual rigour needed to move from basic bookkeeping to strategic financial leadership. By producing monthly Management Accounts and rolling 13 week forecasts, they identify potential bottlenecks before they manifest as crises. This partnership ensures your growth strategy is grounded in data, allowing you to make informed decisions about investment and tax efficiency with composed confidence.